The Light Field Market Size was valued at USD 1.44 Billion in 2023 and is expected to reach USD 4.92 Billion by 2032 and grow at a CAGR of 14.62% over the forecast period 2024-2032.

To get more information on Light Field Market - Request Sample Report

The light field market is experiencing significant growth, driven by the increasing demand for immersive AR/VR experiences, enhanced 3D imaging, and high-quality visual displays. As industries like healthcare, entertainment, and automotive seek more realistic and interactive digital environments, light field technology is becoming a key enabler of this transformation. Light field displays provide enhanced depth, realism, and interactivity, offering a superior viewing experience compared to traditional 2D displays. In the gaming and entertainment sectors, the demand for lifelike 3D visuals is propelling the adoption of light field technology for gaming consoles, VR headsets, and immersive experiences. Additionally, the rise in applications such as virtual surgery, medical imaging, and automotive design is expanding the use of light field cameras and displays, driving further market growth. Major technology companies, including Samsung, Sony, and LG Display, are investing in the development of next-generation light field technologies, with a focus on improving display resolution, brightness, and interactivity. As innovation continues to advance, the light field market is expected to see widespread adoption across multiple sectors, positioning it as a critical technology for the future of immersive media and digital experiences.

Drivers

Revolutionizing Imaging with the Growth of Light Field Technology in Photography and Beyond

The growing interest in advanced imaging and photography systems, particularly light field cameras, is significantly driving the market for light field technologies. Light field imaging provides unparalleled depth and focus adjustment capabilities, offering users the ability to capture and manipulate images in a way that traditional cameras cannot. This innovation is revolutionizing fields like photography, medical imaging, and microscopy by allowing for the capture of 3D images that can be refocused and adjusted after being taken. As more industries seek advanced imaging systems that offer enhanced visual experiences and detailed representation, light field technology has gained traction across sectors, including healthcare, entertainment, and scientific research. The applications of light field cameras in medical imaging, for example, are making surgeries more precise, while in the entertainment sector, they are contributing to more immersive VR/AR experiences. Additionally, the rise in demand for high-quality, multi-dimensional imaging in scientific research and commercial photography is pushing the adoption of light field technologies. With breakthroughs in computational photography and improved image quality through techniques such as deep learning-based enhancements, light field imaging is further elevating the standards of visual representation. Companies like Google, Stanford, and other leading research institutions continue to explore the potential of light field technology, with new innovations expected to revolutionize the way images are captured and processed. As these advancements continue, light field imaging is set to become a core component of next-generation imaging systems, making it a key driver for growth in the market.

Restraints

Challenges in Traditional Imaging Restraining Light Field Technology Adoption

The competition from traditional imaging technologies such as 3D photography, VR, and AR solutions presents a significant challenge for the adoption of light field technology. Established technologies have matured over the years, offering cost-effective alternatives that are widely available and easier to implement. For instance, VR and AR systems have become integral in sectors like entertainment, healthcare, and education, boasting proven effectiveness and lower costs compared to the newer, more complex light field solutions. As these traditional technologies continue to evolve, offering impressive realism and interactive experiences, light field cameras and systems are struggling to match their established popularity and market penetration. Additionally, traditional imaging technologies often require less computational power and simpler setups, making them more accessible to a broader range of industries. Despite the enhanced imaging capabilities offered by light field systems, such as the ability to manipulate focus and depth post-capture, the high costs and technical complexity associated with light field imaging make it a less attractive option for many industries. Furthermore, the lack of standardization and widespread content availability in the light field space also limits its ability to compete with traditional, mature technologies. As a result, the market for light field technology faces strong competition from established imaging systems, which may impede its widespread adoption and slow its growth in key sectors such as healthcare, entertainment, and photography.

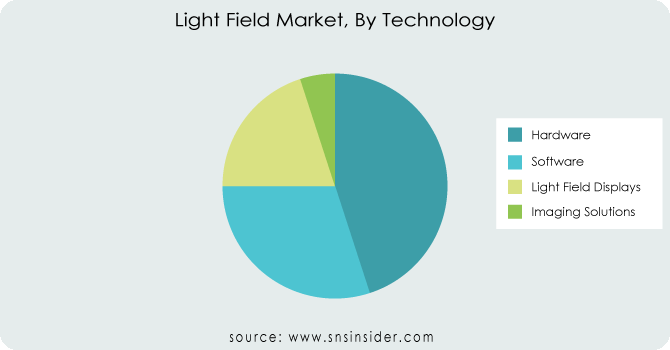

By Technology

In 2023, the hardware segment is the dominant force in the light field market, accounting for approximately 40% of the market share. This segment includes the development of light field cameras, lenses, and other imaging hardware crucial for capturing and processing multi-dimensional images. As the demand for high quality, 3D, and refocusable images grows across industries such as healthcare, entertainment, and scientific research, the role of specialized hardware has become increasingly vital. Advances in optical components, such as micro lenses and light field sensors, have enhanced the performance of these devices, contributing to their widespread adoption. Companies are focusing on improving hardware capabilities, enabling more accessible, accurate, and immersive imaging experiences. This growth in hardware development is expected to continue as innovations in computational photography further push the boundaries of light field technology.

By Vertical

In 2023, the media and entertainment segment leads the light field market, holding a share of around 35%. The adoption of light field technology in this sector is driven by the increasing demand for immersive experiences in virtual reality (VR), augmented reality (AR), and 3D content creation. Light field technology enhances the visual quality of media by enabling lifelike 3D imaging, precise depth perception, and dynamic focus adjustments, significantly improving user engagement. This technology is being increasingly used in filmmaking, gaming, and interactive media, offering realistic effects and immersive experiences. As the entertainment industry explores new frontiers in digital content, the ability to create hyper-realistic visuals with light field cameras is gaining traction. The growing popularity of VR/AR applications in entertainment further fuels market expansion in this vertical.

To Get Customized Report as per your Business Requirement - Request For Customized Report

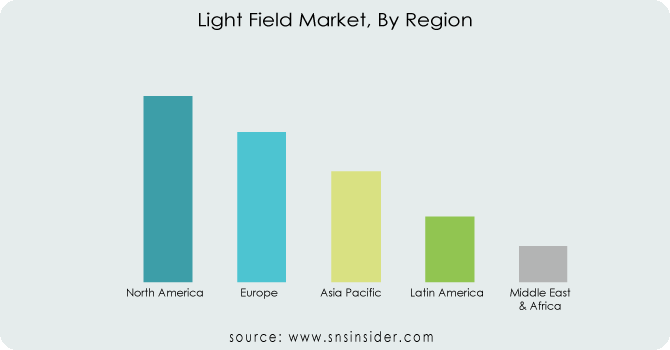

In 2023, North America holds the dominant share of approximately 40% in the light field market, fueled by its advanced technological infrastructure and significant investments in research and development. The region's leadership is supported by the presence of major tech giants such as Google, Microsoft, and Apple, who are pioneering advancements in light field imaging and photography technologies. The U.S. and Canada are particularly influential in driving innovation across various sectors like media and entertainment, healthcare, and scientific research. The demand for immersive experiences in virtual reality (VR) and augmented reality (AR), as well as the increasing adoption of light field cameras in professional photography, has accelerated market growth. strategic collaborations between academic institutions and technology companies further solidify North America's position as a key player in the light field market.

The Asia-Pacific region is the fastest-growing market for light field market from 2024 to 2032, driven by rapid advancements in technological infrastructure and increasing demand for immersive media experiences. Key countries like China, Japan, and South Korea are leading the charge, with China investing heavily in research and development, while Japan focuses on integrating light field imaging in sectors such as robotics, healthcare, and entertainment. South Korea is also expanding its presence, especially in the development of AR/VR applications and consumer electronics. The growing adoption of 5G technology is enhancing the region’s ability to deliver high quality, real-time light field experiences. Additionally, the expansion of the film, gaming, and healthcare industries in the region is fostering demand for innovative imaging technologies. With substantial government support and rapid technological advancements, Asia-Pacific is expected to maintain its position as the fastest-growing market for light field technology.

Some of the major players in Light Field Market with product:

Raytrix GmbH (Light Field Cameras)

FoVI 3D, Inc. (3D Light Field Displays)

Google LLC (Light Field Technologies for AR/VR)

Avegant Corp. (Light Field Headsets)

Lumii Inc. (Light Field Technology for Displays)

Holografika (Light Field Displays for 3D Imaging)

OTOY Inc. (Light Field Rendering Software and Cloud Solutions)

Nvidia Corp (Graphics Processing Units for Light Field Rendering)

Panasonic Corporation (Light Field Cameras and Displays)

Leia (Light Field Displays for Consumer Devices)

Samsung Display. (Light Field Display Technology)

Light Field Lab, Inc. (Holographic Light Field Displays)

Ricoh Innovations Corporation (Light Field Cameras and Solutions)

TOSHIBA CORPORATION (Light Field Imaging Technology)

Sony Corporation (Light Field Cameras and Display Technology)

Apple Inc. (AR/VR Devices and Light Field Technologies)

Pelican Imaging Corporation (Light Field Cameras)

Lytro, Inc. (Light Field Cameras and Photography Technology)

Japan Display . (Light Field Displays)

LG Display Co., Ltd. (OLED and Light Field Display Technologies)’

List of Suppliers who supplies Raw Material and Component

Corning Incorporated

3M Company

DuPont

Sony Corporation

Samsung Electronics

Sharp Corporation

Nippon Electric Glass Co., Ltd.

Panasonic Corporation

LG Display Co., Ltd.

Qualcomm Incorporated

August 2024: Samsung Electronics unveiled its groundbreaking Odyssey 3D gaming monitor at Gamescom 2024, featuring glasses-free 3D viewing with Eye Tracking and View Mapping technology. This innovation marks a significant step forward in immersive gaming experiences.

May 2024: LG Display unveiled its next-generation OLED technologies at SID Display Week 2024, including the new OLEDoS for VR. This technology boasts a 1.3-inch display with ultra-high brightness of 10,000 nits, 4,000 ppi resolution, and 97% DCI-P3 color accuracy, offering lifelike virtual reality experiences.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.44 Billion |

| Market Size by 2032 | USD 4.92 Billion |

| CAGR | CAGR of 14.62% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Hardware, Software, Light Field Displays, Imaging Solutions) • By Vertical (Media & Entertainment, Healthcare, Architecture, Industrial, Defense) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Raytrix GmbH, FoVI 3D, Inc., Google LLC, Avegant Corp., Lumii Inc., Holografika, OTOY Inc., NVIDIA Corporation, Panasonic Corporation, Leia Inc., Samsung Display Co., Ltd., Light Field Lab, Inc., Ricoh Innovations Corporation, TOSHIBA CORPORATION, Sony Corporation, Apple Inc., Pelican Imaging Corporation, Lytro, Inc., Japan Display Inc., LG Display Co., Ltd. |

| Key Drivers | • Revolutionizing Imaging with the Growth of Light Field Technology in Photography and Beyond |

| Restraints | • Challenges in Traditional Imaging Restraining Light Field Technology Adoption |

Ans: The Light Field Market size was valued at USD 1.44 billion in 2023 at a CAGR of 14.62%.

Ans: The market value is expected to reach USD 4.92 billion by 2032.

Ans: The key driver in the Light Field Market will be the increasing demand for immersive AR/VR experiences and advanced 3D display technologies.

Ans: North America is dominating in Light Field Market

Ans: Hardware Segment is dominating in Light Field Market

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Patent Counts and Innovations, 2020-2032

5.2 Investment Trends, by Region

5.3 Technology Integration Rates, by Region

5.4 Consumer Engagement:, by Region

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Light Field Market Segmentation, by Technology

7.1 Chapter Overview

7.2 Hardware

7.2.1 Hardware Market Trends Analysis (2020-2032)

7.2.2 Hardware Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Software

7.3.1 Software Market Trends Analysis (2020-2032)

7.3.2 Software Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Light Field Displays

7.4.1 Light Field Displays Market Trends Analysis (2020-2032)

7.4.2 Light Field Displays Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Imaging Solutions

7.5.1 Imaging Solutions Market Trends Analysis (2020-2032)

7.5.2 Imaging Solutions Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Light Field Market Segmentation, by Vertical

8.1 Chapter Overview

8.2 Media & Entertainment

8.2.1 Media & Entertainment Market Trends Analysis (2020-2032)

8.2.2 Media & Entertainment Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Healthcare

8.3.1HealthcareMarket Trends Analysis (2020-2032)

8.3.2 Healthcare Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Architecture

8.4.1ArchitectureMarket Trends Analysis (2020-2032)

8.4.2 Architecture Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Industrial

8.5.1Industrial Market Trends Analysis (2020-2032)

8.5.2 Industrial Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Defense

8.6.1Defense Market Trends Analysis (2020-2032)

8.6.2 Defense Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

b

10. Company Profiles

10.1 Raytrix GmbH

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 SWOT Analysis

10.2 FoVI 3D, Inc.

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Google LLC

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Avegant Corp.

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Lumii Inc.

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Holografika

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 OTOY Inc.

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 NVIDIA Corporation

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Panasonic Corporation

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Leia Inc.

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Technology

Hardware

Software

Light Field Displays

Imaging Solutions

By Vertical

Media & Entertainment

Healthcare

Architecture

Industrial

Defense

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia-Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Building Automation System Market Size was valued at USD 81.75 billion in 2023 and is expected to grow at 9.92% CAGR to reach USD 190.99 billion by 2032.

The Smart Home Projector Market size was valued at USD 761.40 million in 2023. It is expected to hit USD 3250.52 million by 2032 and grow at a CAGR of 17.5% over the forecast period of 2024-2032.

The Crystal Oscillators Market Size was valued at USD 3.35 billion in 2023 and is expected to reach USD 4.07 billion by 2032 and grow at a CAGR of 2.01% over the forecast period 2024-2032.

The Intruder Alarm System Market size was valued at USD 2.52 Billion in 2023 and is expected to grow to USD 5.91 Billion at a CAGR of 9.9% By 2024-2032

Optocoupler IC Market Size was valued at USD 2.5 billion in 2023 and is expected to reach USD 3.9 billion by 2032, and grow at a CAGR of 5% over the forecast period 2024-2032.

The IO-Link Market was valued at USD 13.9 Billion in 2023 and is expected to reach USD 70.5 Billion by 2032, growing at a CAGR of 19.79% from 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd