Get E-PDF Sample Report on Internal Combustion Engine (ICE) Market - Request Sample Report

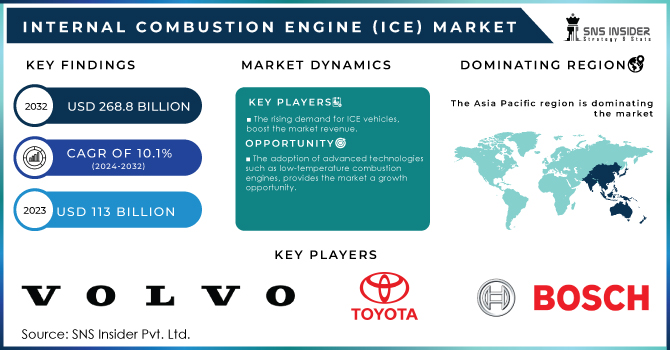

The Internal Combustion Engine (ICE) Market demand size was recorded at USD 113 Bn by 2023 and is expected to reach USD 268.8 Bn during 2032, growing at a CAGR of 10.1% over the forecast period 2024-2032.

This growth is driven by a growing focus on clean, sustainable energy solutions and increasing demand from sectors including cleaner transportation. Hydrogen ICE technology is a big improvement in reducing carbon emissions and increasing energy efficiency, so this innovative performance has enabled huge investments shaping technological development in automotive as well as the entire global energy consequences.

Moreover, because of the increasing adoption of ICEs in numerous automotive and non-automotive applications such as cars, motorcycles, aircraft, boats, diesel generators, lawnmowers locomotives ships airplanes in countries like China, Japan, India expected to hold substantial market share, thus further fuelling growth prospects in internal combustion engine market. The internal combustion engine (ICE) sector has recorded a lot of developments in recent times Low-temperature combustion, including Homogeneous charge compression Ignition (HCCI) and Premixed charge compression ignition(PCCI )has been able to improve engine efficiency by 20 % while emitting less toxins as well. For Instance, Low temperature Combustion(LTC) had made strategies to improve engine efficiency by up to 20% compared to conventional diesel engines. This is because LTC reduces emissions of particulate matter and nitrogen oxides by lowering combustion temperatures and avoiding fuel-rich regions. By helping engines meet increasingly stringent emissions regulations, LTC is enabling the continued growth and development of the ICE market.

The recent technological advancement in combustion engine design and material that leads to improvement in efficiency and effectiveness, have boosted the market in recent years .For Instance, Toyota is also planning to reveal a new in-built-powertrain (or internal combustion engine, ICE) which includes a 1.5- and four-liter cylinders that will be used in vehicles from July 2024. The new innovations that driving this momentum are Variable Displacement Engines (VDE) and high-performance hybrid electric powertrains.

Lightweight, high-strength composite materials and electronic controls are helping manufacturers improve engine. NVH as well as move advanced technologies into these fast-moving marine propulsion power plants for commercial fleet operations. In addition to electrification efforts, alternative fuels such as biofuels and hydrogen are becoming more widespread for fossil-fueled ICE technologies is helping the newest-generation internal combustion engines make up ground in a move toward sustainability.

Market Dynamics:

Driver

The rising demand for ICE vehicles, boost the market revenue.

The rising demand for vehicles globally and the growing need to expand transportation infrastructure, consequently projecting significant growth in the internal combustion engine market. Road vehicles are key in almost all trade since they play such an important role as facilitative agents for the global supply chain to provide regional connectivity and timely goods delivery. For Instance, Nearly 14 million new electric passenger cars were registered in the world during the year, making it a total of 40 million that are now driving on roads around almost at a sales-forecast movement track from last year's outcome, splitting up to two times the normal level. Almost 18% of cars sold were electric, compared to an average of just over 14% in 2022. These trends show that growth is healthy as electric car markets head out of the initial market phase in 2022.

On the other hand, Mercedes-Benz revealed its new efficient gasoline-powered E-Class model in April 2023 reflecting the industry's gradual shift towards electrification

Restrain

The high cost associated with purchase, fuel, and maintenance, reduces the demand for ICE vehicles.

Opportunity

The adoption of advanced technologies such as low-temperature combustion engines, provides the market a growth opportunity.

Challenge

Strict government regulation regarding emissions affects and balances efficiency and performance, hindering the market.

Market Segmentation

By Fuel

Petroleum

Natural Gas

The petroleum segment contributed to the largest share of more than 80% in 2023 and is anticipated to register the highest growth rate over the forecast period owing to benefits offered by petroleum internal combustion engines which include low vibration, noise among others In addition, the segment is anticipated to generate revenue due rise in technological developments within automobile industry. This growth is due to their efficiency, low cost, lightweight nature, and emission reduction capability as compared with other fuels that we use in engines.

By End-User

Automotive

Marine

Aircraft

By End-User, the automotive segment held the highest volume share of more than 68% in 2023 and is anticipated to grow with significant rate during forecast period. This growth is associated with the rising spending power of consumers. Vehicle makers are currently fine-tuning new efficient internal combustion engines that deliver the highest returns on manufacturing investments. Additionally, adopting advanced technology for enhancing IC engine fuel economy, emission and performance is anticipated to create growth opportunities in the market across its forecast period.

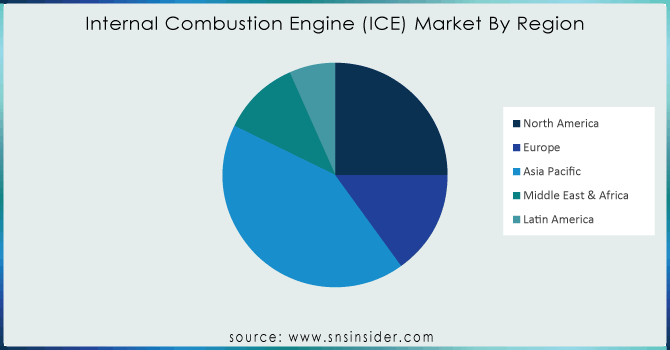

Asia-Pacific region dominates the Internal Combustion Engine market with more than 40% of the market share in the global market in 2023. The presence of a large number of automotive manufacturers and growing demand for passenger automobiles in major countries including China and India are expected to influence the growth prospects. Moreover, the non-availability of electric vehicle charging infrastructure due to the absence of power distribution agreements in countries is another major constraint, and the very high cost for development when compared with other car accessories is supporting market growth. In addition to considering that ICE emits less harmful gases, it is aimed at making itself a viable option as the next alternative over EVs by using natural gas in IC engines.

According to geography, North America is expected to increase at a rapid pace during the course of the projection period due to the country's growing automotive use. We should use the North American region, home to renowned automakers like General Motors Company and Ford Motor Corporation, as an example. The automotive industry is changing the way that cars are built, leading to fewer and smaller engines for better performance so similar it becomes lightweight which paves another reason for efficiency. Therefore, these innovations in technology fuel the growth of the market. European Government rules on emissions have been the strictest globally and more gravitate to electric cars will be found in Europe, thus it should see a higher internal combustion share.

Get Customized Report as Per Your Business Requirement - Request For Customized Report

REGIONAL COVERAGE

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major key players are as follows Volvo AB, Toyota, Volkswagen, Renault SA, MAN SE, General Motors Co, Ford Motor, Fiat, Robert Bosch, and others.

Recent Developments

In June 2023, General Motors revealed plans to invest $632 million for the enhancement of its Fort Wayne Assembly facility located in Indiana. This investment will rebuild the plant to build America's next generation of full-size ICE pickups. This important strategic move is taken by company for expanding production capacities and meeting the changing requirements of one of its automotive customers

In April 2023, Mercedes' sixth-generation E-Class introduced the automaker's last new combustion engine model. The next generations of the E-Class will be based on a new platform designed to cater for electric powertrains but this current generation matters right now.

| Report Attributes | Details |

| Market Size in 2023 | USD 113.0 Bn |

| Market Size by 2032 | USD 268.8 Bn |

| CAGR | CAGR of 10.1 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Fuel: Petroleum, Natural Gas By End-User: Automotive, Marine, Aircraft |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Volvo AB, Toyota, Volkswagen, Renault SA, MAN SE, General Motors Co, Ford Motor, Fiat, Robert Bosch, and others. |

| Key Drivers | The rising percentage of demand for ICE vehicles |

| Market Restraints | The high entry barriers and the increase in operating expenses because of geopolitical pressures. |

Ans: The Internal Combustion Engine (ICE) Market size is expected to reach USD 268.8 Bn by 2032, the value for the year 2023 was recorded at USD 113 Bn the market is expected to grow at a CAGR of 10.1% over the forecast period 2024-2032.

Ans; The rising percentage of demand for ICE vehicles

Ans: The high entry barriers and the increase in operating expenses because of geopolitical pressures.

Ans; APAC region will be dominating the market during the forecasted period.

The major key players are as follows Volvo AB, Toyota, Volkswagen, Renault SA, MAN SE, General Motors Co, Ford Motor, Fiat, Robert Bosch, and others.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Internal Combustion Engine Market Segmentation, By Fuel Type

7.1 Introduction

7.2 Petroleum

7.3 Natural Gas

8. Internal Combustion Engine Market Segmentation, By End-user

8.1 Introduction

8.2 Automotive

8.3 Marine

8.4 Aircraft

9. Regional Analysis

9.1 Introduction

9.2 North America

9.2.1 Trend Analysis

9.2.2 North America Internal Combustion Engine Market by Country

9.2.3 North America Internal Combustion Engine Market By Fuel Type

9.2.4 North America Internal Combustion Engine Market By End-user

9.2.5 USA

9.2.5.1 USA Internal Combustion Engine Market By Fuel Type

9.2.5.2 USA Internal Combustion Engine Market By End-user

9.2.6 Canada

9.2.6.1 Canada Internal Combustion Engine Market By Fuel Type

9.2.6.2 Canada Internal Combustion Engine Market By End-user

9.2.7 Mexico

9.2.7.1 Mexico Internal Combustion Engine Market By Fuel Type

9.2.7.2 Mexico Internal Combustion Engine Market By End-user

9.3 Europe

9.3.1 Trend Analysis

9.3.2 Eastern Europe

9.3.2.1 Eastern Europe Internal Combustion Engine Market by Country

9.3.2.2 Eastern Europe Internal Combustion Engine Market By Fuel Type

9.3.2.3 Eastern Europe Internal Combustion Engine Market By End-user

9.3.2.4 Poland

9.3.2.4.1 Poland Internal Combustion Engine Market By Fuel Type

9.3.2.4.2 Poland Internal Combustion Engine Market By End-user

9.3.2.5 Romania

9.3.2.5.1 Romania Internal Combustion Engine Market By Fuel Type

9.3.2.5.2 Romania Internal Combustion Engine Market By End-user

9.3.2.6 Hungary

9.3.2.6.1 Hungary Internal Combustion Engine Market By Fuel Type

9.3.2.6.2 Hungary Internal Combustion Engine Market By End-user

9.3.2.7 turkey

9.3.2.7.1 Turkey Internal Combustion Engine Market By Fuel Type

9.3.2.7.2 Turkey Internal Combustion Engine Market By End-user

9.3.2.8 Rest of Eastern Europe

9.3.2.8.1 Rest of Eastern Europe Internal Combustion Engine Market By Fuel Type

9.3.2.8.2 Rest of Eastern Europe Internal Combustion Engine Market By End-user

9.3.3 Western Europe

9.3.3.1 Western Europe Internal Combustion Engine Market by Country

9.3.3.2 Western Europe Internal Combustion Engine Market By Fuel Type

9.3.3.3 Western Europe Internal Combustion Engine Market By End-user

9.3.3.4 Germany

9.3.3.4.1 Germany Internal Combustion Engine Market By Fuel Type

9.3.3.4.2 Germany Internal Combustion Engine Market By End-user

9.3.3.5 France

9.3.3.5.1 France Internal Combustion Engine Market By Fuel Type

9.3.3.5.2 France Internal Combustion Engine Market By End-user

9.3.3.6 UK

9.3.3.6.1 UK Internal Combustion Engine Market By Fuel Type

9.3.3.6.2 UK Internal Combustion Engine Market By End-user

9.3.3.7 Italy

9.3.3.7.1 Italy Internal Combustion Engine Market By Fuel Type

9.3.3.7.2 Italy Internal Combustion Engine Market By End-user

9.3.3.8 Spain

9.3.3.8.1 Spain Internal Combustion Engine Market By Fuel Type

9.3.3.8.2 Spain Internal Combustion Engine Market By End-user

9.3.3.9 Netherlands

9.3.3.9.1 Netherlands Internal Combustion Engine Market By Fuel Type

9.3.3.9.2 Netherlands Internal Combustion Engine Market By End-user

9.3.3.10 Switzerland

9.3.3.10.1 Switzerland Internal Combustion Engine Market By Fuel Type

9.3.3.10.2 Switzerland Internal Combustion Engine Market By End-user

9.3.3.11 Austria

9.3.3.11.1 Austria Internal Combustion Engine Market By Fuel Type

9.3.3.11.2 Austria Internal Combustion Engine Market By End-user

9.3.3.12 Rest of Western Europe

9.3.3.12.1 Rest of Western Europe Internal Combustion Engine Market By Fuel Type

9.3.2.12.2 Rest of Western Europe Internal Combustion Engine Market By End-user

9.4 Asia-Pacific

9.4.1 Trend Analysis

9.4.2 Asia Pacific Internal Combustion Engine Market by Country

9.4.3 Asia Pacific Internal Combustion Engine Market By Fuel Type

9.4.4 Asia Pacific Internal Combustion Engine Market By End-user

9.4.5 China

9.4.5.1 China Internal Combustion Engine Market By Fuel Type

9.4.5.2 China Internal Combustion Engine Market By End-user

9.4.6 India

9.4.6.1 India Internal Combustion Engine Market By Fuel Type

9.4.6.2 India Internal Combustion Engine Market By End-user

9.4.7 japan

9.4.7.1 Japan Internal Combustion Engine Market By Fuel Type

9.4.7.2 Japan Internal Combustion Engine Market By End-user

9.4.8 South Korea

9.4.8.1 South Korea Internal Combustion Engine Market By Fuel Type

9.4.8.2 South Korea Internal Combustion Engine Market By End-user

9.4.9 Vietnam

9.4.9.1 Vietnam Internal Combustion Engine Market By Fuel Type

9.4.9.2 Vietnam Internal Combustion Engine Market By End-user

9.4.10 Singapore

9.4.10.1 Singapore Internal Combustion Engine Market By Fuel Type

9.4.10.2 Singapore Internal Combustion Engine Market By End-user

9.4.11 Australia

9.4.11.1 Australia Internal Combustion Engine Market By Fuel Type

9.4.11.2 Australia Internal Combustion Engine Market By End-user

9.4.12 Rest of Asia-Pacific

9.4.12.1 Rest of Asia-Pacific Internal Combustion Engine Market By Fuel Type

9.4.12.2 Rest of Asia-Pacific Internal Combustion Engine Market By End-user

9.5 Middle East & Africa

9.5.1 Trend Analysis

9.5.2 Middle East

9.5.2.1 Middle East Internal Combustion Engine Market by Country

9.5.2.2 Middle East Internal Combustion Engine Market By Fuel Type

9.5.2.3 Middle East Internal Combustion Engine Market By End-user

9.5.2.4 UAE

9.5.2.4.1 UAE Internal Combustion Engine Market By Fuel Type

9.5.2.4.2 UAE Internal Combustion Engine Market By End-user

9.5.2.5 Egypt

9.5.2.5.1 Egypt Internal Combustion Engine Market By Fuel Type

9.5.2.5.2 Egypt Internal Combustion Engine Market By End-user

9.5.2.6 Saudi Arabia

9.5.2.6.1 Saudi Arabia Internal Combustion Engine Market By Fuel Type

9.5.2.6.2 Saudi Arabia Internal Combustion Engine Market By End-user

9.5.2.7 Qatar

9.5.2.7.1 Qatar Internal Combustion Engine Market By Fuel Type

9.5.2.7.2 Qatar Internal Combustion Engine Market By End-user

9.5.2.8 Rest of Middle East

9.5.2.8.1 Rest of Middle East Internal Combustion Engine Market By Fuel Type

9.5.2.8.2 Rest of Middle East Internal Combustion Engine Market By End-user

9.5.3 Africa

9.5.3.1 Africa Internal Combustion Engine Market by Country

9.5.3.2 Africa Internal Combustion Engine Market By Fuel Type

9.5.3.3 Africa Internal Combustion Engine Market By End-user

9.5.2.4 Nigeria

9.5.2.4.1 Nigeria Internal Combustion Engine Market By Fuel Type

9.5.2.4.2 Nigeria Internal Combustion Engine Market By End-user

9.5.2.5 South Africa

9.5.2.5.1 South Africa Internal Combustion Engine Market By Fuel Type

9.5.2.5.2 South Africa Internal Combustion Engine Market By End-user

9.5.2.6 Rest of Africa

9.5.2.6.1 Rest of Africa Internal Combustion Engine Market By Fuel Type

9.5.2.6.2 Rest of Africa Internal Combustion Engine Market By End-user

9.6 Latin America

9.6.1 Trend Analysis

9.6.2 Latin America Internal Combustion Engine Market by Country

9.6.3 Latin America Internal Combustion Engine Market By Fuel Type

9.6.4 Latin America Internal Combustion Engine Market By End-user

9.6.5 brazil

9.6.5.1 Brazil Internal Combustion Engine Market By Fuel Type

9.6.5.2 Brazil Internal Combustion Engine Market By End-user

9.6.6 Argentina

9.6.6.1 Argentina Internal Combustion Engine Market By Fuel Type

9.6.6.2 Argentina Internal Combustion Engine Market By End-user

9.6.7 Colombia

9.6.7.1 Colombia Internal Combustion Engine Market By Fuel Type

9.6.7.2 Colombia Internal Combustion Engine Market By End-user

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Internal Combustion Engine Market By Fuel Type

9.6.8.2 Rest of Latin America Internal Combustion Engine Market By End-user

10. Company Profiles

10.1 Volvo AB

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 The SNS View

10.2 Toyota

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 The SNS View

10.3 Volkswagen

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 The SNS View

10.4 Renault SA

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 The SNS View

10.5 MAN SE

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 The SNS View

10.6 General Motors Co

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 The SNS View

10.7 Ford Motor

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 The SNS View

10.8 Fiat

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 The SNS View

10.9 Robert Bosch

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 The SNS View

10.10 Caterpillar

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Products/ Services Offered

10.10.4 The SNS View

11. Competitive Landscape

11.1 Competitive Benchmarking

11.2 Market Share Analysis

11.3 Recent Developments

11.3.1 Industry News

11.3.2 Company News

11.3.3 Mergers & Acquisitions

12. USE Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Automotive Emission Test Equipment Market Size was valued at USD 772.33 Million in 2023 and is expected to reach USD 1185.07 Million by 2032 and grow at a CAGR of 4.89% over the forecast period 2024-2032.

The Industrial Vehicles Market Size was valued at USD 41.5 billion in 2023 and is expected to reach USD 61.67 billion by 2032 and grow at a CAGR of 4.5% over the forecast period 2024-2032.

Automotive Heat Shield Market Size was valued at USD 12.83 billion in 2023 and is expected to reach USD 17.59 billion by 2031 and grow at a CAGR of 3.78% over the forecast period 2024-2031.

The Torque Vectoring Market Size was USD 10.5 Billion in 2023. It is expected to grow to USD 28.5 Billion by 2032 and grow at a CAGR of 11.7% by 2024-2032.

The Rail Infrastructure Market Size was valued at USD 53.93 Billion in 2023 and is expected to reach USD 73.95 Billion by 2032 and grow at a CAGR of 3.61% over the forecast period 2024-2032.

The Deck Boat Market size was valued at USD 3.04 Billion in 2023 and is expected to reach USD 6.30 Billion by 2032 and grow at a CAGR of 8.47% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd