The Injectable Cytotoxic Drugs Market Report Scope & Overview:

To Get More Information on Injectable Cytotoxic Drugs Market - Request Sample Report

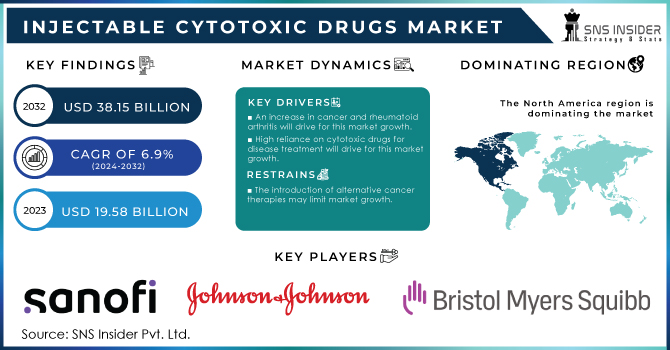

The Injectable Cytotoxic Drugs Market size was USD 19.58 Billion in 2023 and is expected to Reach USD 38.15 Billion by 2032 and grow at a CAGR of 6.9% over the forecast period of 2024-2032.

The Injectable Cytotoxic Drugs Market refers to the pharmaceutical sector that focuses on the production, distribution, and sale of cytotoxic drugs in injectable forms. Cytotoxic drugs, also known as antineoplastic or chemotherapy drugs, are medications used in the treatment of cancer. They work by inhibiting the growth and division of cancer cells, ultimately leading to their destruction. The market for injectable cytotoxic drugs is primarily driven by the increasing prevalence of cancer worldwide. As the incidence of cancer continues to rise, there is a growing demand for effective chemotherapy treatments. Injectable cytotoxic drugs play a crucial role in various cancer treatment regimens, including standalone chemotherapy and combination therapies. Several factors contribute to the growth of the Injectable Cytotoxic Drugs Market. These include advancements in drug delivery techniques, the development of targeted therapies, increasing research and development activities in oncology, and the introduction of novel cytotoxic agents. Additionally, the expanding geriatric population, which is more susceptible to cancer, also drives market growth.

The Injectable Cytotoxic Drugs Market is composed of various types of drugs, including alkylating agents, antimetabolites, anthracyclines, taxanes, vinca alkaloids, and others. These drugs are administered through different routes, primarily intravenous (IV), but also intramuscular (IM) and subcutaneous (SC) injections. Cytotoxic medicines are an important pharmacological class used to treat common diseases such as oncology problems. These medications are recognised for their cellular degeneration properties, which aid in the elimination of malignant cells. Cytotoxic injectable medications are used as first-line therapy for several forms of cancer. The bulk of off-patent injectable cytotoxic medicines are accessible in the worldwide market as generics. Cytotoxic medications, generally known as chemotherapy, are recognised for causing significant side effects including bone marrow depression, follicular toxicity, and anaemia. The rising frequency of cancer and the increased reliance on cytotoxic medications for treatment are major drivers driving market expansion in the next years.

MARKET DYNAMICS

DRIVERS:

-

An increase in cancer and rheumatoid arthritis will drive for this market growth.

-

High reliance on cytotoxic drugs for disease treatment will drive for this market growth.

Cancer is a severe disease, and because of disease heterogeneity, traditional therapies such as chemotherapy or radiation are effective and widely used. Furthermore, for newly diagnosed cancer patients, cytotoxic medicines are commonly utilised as the initial line of treatment. Targeted treatment and immunotherapy, for example, are presently only licenced to treat particular cancer types. Furthermore, the majority of targeted and immunotherapy medications are administered in conjunction with cytotoxic/chemotherapy treatments. In individuals with worsened types of multiple sclerosis, cytotoxic medications are also specified.

RESTRAIN:

-

Injectable cytotoxic drugs can have significant side effects and toxicities. These drugs target rapidly dividing cells, including cancer cells, but they can also affect healthy cells in the body, leading to adverse reactions.

-

The introduction of alternative cancer therapies may limit market growth.

The future revolutionary immunotherapy and targeted therapy medications are very effective and have fewer adverse effects than cytotoxic drugs. These concerns are anticipated to stifle the market for injectable cytotoxic medicines in the next years. Cancer's intrinsic unpredictability adds to the expanding area of precision and personalized medicine (PPM). PPM cancer therapies have been shown to provide significant patient advantages; hence several pharmaceutical firms are investing in this area.

OPPORTUNITY:

-

The growing prevalence of cancer in emerging markets presents an opportunity for the expansion of the Injectable Cytotoxic Drugs Market.

-

Expansion of oncology research and clinical trials is a good opportunity for this market.

The expansion of oncology research and clinical trials presents opportunities for the Injectable Cytotoxic Drugs Market. Clinical trials allow for the evaluation of new drug candidates, novel combinations, and innovative treatment regimens. Pharmaceutical companies can invest in research and collaborate with academic institutions and research organizations to advance the development of injectable cytotoxic drugs. The availability of robust clinical data can support regulatory approvals and market penetration.

CHALLENGES:

-

Injectable cytotoxic drugs can cause significant toxicity and side effects due to their mechanism of action, which targets rapidly dividing cells. Common side effects include nausea, vomiting, hair loss, fatigue, and immunosuppression.

-

Alternative treatment approaches have also emerged as a major challenge in this market.

The emergence of alternative treatment approaches, such as targeted therapies, immunotherapies, and precision medicine, poses a challenge to the Injectable Cytotoxic Drugs Market. These therapies offer potentially more precise and personalized treatment options for cancer patients, reducing the reliance on traditional chemotherapy. The competition from these alternative approaches necessitates innovation and differentiation within the injectable cytotoxic drugs market.

IMPACT OF RUSSIA-UKRAINE WAR

Russia's assault on Ukraine has far-reaching global ramifications. The majority of the world's top economies have slapped severe economic sanctions on Russia. Many major brands, including but not limited to PepsiCo, McDonald's, Marriott, Shell, British, H&M, IKEA, American Tobacco, Nestlé, & Nike, are shutting or have closed their Russian stores/offices and/or have suspended planned investments. When Russia invaded Ukraine, there were 1,253 active CTs involving 10,168 locations in Russia. Russia ranked 11th in terms of worldwide biopharma CT market share in 2021, with 2.54% of the global share. But now CT’s market share is down by a rate of 0.4%.

Ukraine's iBPCT market was around one-twelfth the size of Russia's. When the conflict broke out, there were 614 ongoing studies in Ukraine, spread among 5,018 locations. Ukraine was placed 18th in terms of worldwide biopharma CT market share in 2021, with 1.20% of the global share. But now CT’s market share is down by a rate of 0.2%.

IMPACT OF ONGOING RECESSION

The US Federal Reserve hiked interest rates for the seventh time this year last week, in an effort to allay fears of a recession. The International Monetary Fund expects that due to tightening monetary and financial conditions, real GDP growth in the United States would decrease from 1.8% in 2022 to 1.2% in 2023. Furthermore, some financial organisations, including Bank of America and JP Morgan, have been predicting a mild recession in the United States in 2023. While the effects of such an occurrence are likely to be felt across industries, small and mid-sized companies (SMEs) in the pharmaceutical industry are projected to be substantially hit since the economic slump impacts efforts to obtain financing, among other things.

KEY MARKET SEGMENTATION

By Drug Class

-

Antimetabolites

-

Alkylating Drugs

-

Plant Alkaloids

-

Cytotoxic Antibodies

-

Others

By Application

-

Multiple Sclerosis

-

Oncology

-

Rheumatoid Arthritis

-

Others

By End-user

-

Retail Pharmacy

-

Hospital Pharmacy

REGIONAL ANALYSIS

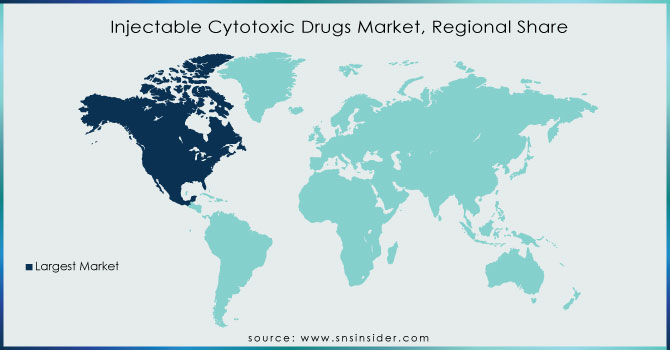

North America: North America's market size was USD 8.79 billion in 2021 and is expected to rise significantly during the projected period. The increase is due to an increase in the number of cancer patients and more widespread access to cancer medications. According to the American Cancer Society, an estimated 368,800 new cases of invasive breast cancer were identified in women in 2021 & around 2,570 cases were detected in males in the United States alone.

Asia Pacific: The Asia Pacific market, on the other hand, is expected to rise significantly throughout the projected period. Factors such as a rising patient pool and increased healthcare spending in the region are boosting Asia Pacific market expansion. Furthermore, the rising purchasing power of the masses in emerging economies such as India and China presents a great possibility for injectable cytotoxic drugs market expansion.

Do You Need any Customization Research on Injectable Cytotoxic Drugs Market - Enquire Now

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

Key Players

The major key players in Injectable Cytotoxic Drugs Market are Sanofi, Johnson and Johnson Services Inc., Bristol-Myers Squibb Company, Eli Lilly and Company, F. Hoffmann-La Roche Ltd., Pfizer, Inc, Novartis AG, Abbie Inc, Amgen, Merck & Co. Inc, and other players.

RECENT DEVELOPMENTS

Innovent Biologies, Inc. and Eli Lilly and Company: In 2021, Innovent Biologies, Inc. and Eli Lilly and Company announced that the United States Food and Drug Administration (FDA) has approved their Biologics Licence Application for their investigational sintilimab injection in combination.

Bristol-Myers Squibb: In 2021, Bristol-Myers Squibb stated that Opdivo (nivolumab injectable for intravenous usage) has been approved. The medicine is licenced for adjuvant treatment of individuals with fully resected oesophagus and gastroesophageal junction cancer with persistent pathogenic disease who have received neoadjuvant chemotherapy.

F. Hoffmann-La Roche Ltd: In 2020, F. Hoffmann-La Roche Ltd announced that their investigational drug Phesgo (fixed-dose combination of Perjeta and Herceptin for subcutaneous injection) has been approved by the US Food and Drug Administration for the treatment of patients with HERZ-positive breast cancer.

| Report Attributes | Details |

| Market Size in 2023 | US$ 19.58 Bn |

| Market Size by 2032 | US$ 38.15 Bn |

| CAGR | CAGR of 6.9% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Drug Class (Antimetabolites, Alkylating Drugs, Plant Alkaloids, Cytotoxic Antibodies, Others) • By Application (Multiple Sclerosis, Oncology, Rheumatoid Arthritis, Others) • By End-user (Online Pharmacy, Retail Pharmacy, and Hospital Pharmacy) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | Sanofi, Johnson and Johnson Services Inc., Bristol-Myers Squibb Company, Eli Lilly and Company, F. Hoffmann-La Roche Ltd., Pfizer, Inc, Novartis AG, Abbie Inc, Amgen, Merck & Co. Inc |

| Key Drivers | • An increase in cancer and rheumatoid arthritis will drive for this market growth. • High reliance on cytotoxic drugs for disease treatment will drive for this market growth. |

| Market Restraints | • Injectable cytotoxic drugs can have significant side effects and toxicities. These drugs target rapidly dividing cells, including cancer cells, but they can also affect healthy cells in the body, leading to adverse reactions. • The introduction of alternative cancer therapies may limit market growth. |