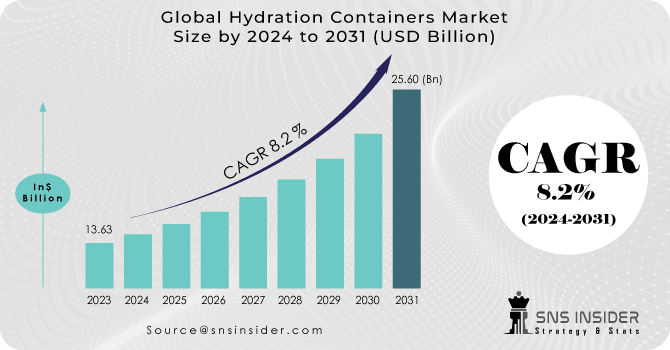

The Hydration Containers Market Size was valued at USD 13.63 billion in 2023 and is expected to reach USD 25.60 billion by 2031 and grow at a CAGR of 8.2 % over the forecast period 2024-2031.

The growth of the hydration containers market in the upcoming years is expected to be driven by manufacturers focusing on providing packaging alternatives that avoid single-use plastics. Government directives limiting plastic-based products are also anticipated to contribute to market growth. The increasing prevalence of sporting events and outdoor activities is predicted to further boost the demand for hydration containers. However, the market might face challenges due to rising manufacturing costs for certain types of containers.

Get More Information on Hydration Containers Market - Request Sample Report

Despite this, the market is likely to benefit from consumer acceptance of lightweight and user-friendly liquid packaging solutions, creating new opportunities for expansion. Concerns about the use of low-quality materials in container production for increased profit margins could present challenges in the future. Key industry drivers include the growing popularity of outdoor activities and effective manufacturer promotional strategies such as targeted marketing, product design, and increased shelf space for leading retail brands.

KEY DRIVERS:

Market growth stimulated by growing awareness and user friendly packaging solutions

The shift away from single-use plastic bottles towards more sustainable and reusable hydration containers is a significant driver. This change is fuelled by heightened environmental awareness and regulatory actions aimed at reducing plastic waste.

Increased disposable income has led consumers to allocate more funds towards convenience products.

RESTRAIN:

Low-quality alternatives being readily accessible pose a challenge in the market.

The increased price might discourage certain customers from buying hydration containers.

OPPORTUNITY:

Advancements in innovation and continuous product development are driving forces behind the evolution of industries.

Environmental considerations have impacted market demand.

Increasing environmental awareness is driving a transition towards reusable hydration containers, as consumers seek sustainable alternatives to single-use plastic bottles. Sustainability is becoming a priority for many, shaping their choices in hydration products. Environmental concerns are playing a significant role in shaping consumer preferences and impacting the hydration containers market. With a growing understanding of the environmental consequences of single-use plastics and a rising emphasis on sustainable living, there is a rising demand for eco-friendly hydration solutions.

CHALLENGES:

Rapid shifts in consumer preferences and trends can pose a challenge for companies to keep up with in terms of product design and features.

The Russia-Ukraine war has introduced significant challenges to the Hydration Containers Market. The conflict has the potential to disrupt supply chains, leading to increased costs for raw materials and logistical difficulties. The geopolitical tensions may also contribute to fluctuations in currency exchange rates, impacting global trade dynamics within the hydration container market. These disruptions pose challenges for manufacturers and distributors, affecting the industry's supply chain stability and potentially influencing pricing structures. Overall, the war has introduced uncertainties and complexities that can impact various aspects of the hydration container market.

Economic uncertainties can influence consumer spending behaviour, leading to a potential decrease in discretionary purchases, including premium hydration containers. The slowdown may result in reduced consumer confidence and willingness to invest in non-essential products. Additionally, the economic downturn could affect production costs and supply chain dynamics for hydration container manufacturers, potentially leading to challenges in maintaining competitive pricing. Overall, the economic slowdown poses challenges in terms of consumer demand, production costs, and market competitiveness within the hydration container industry.

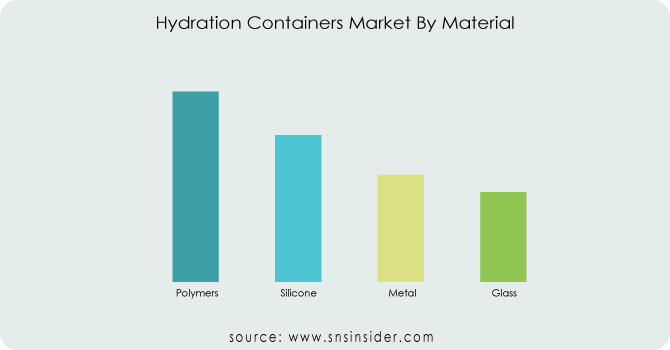

By Material

Polymers

Silicone

Metal

Glass

Polymer remains dominant in the hydration container market due to its affordability and convenience, with lightweight designs favoured for everyday use. Metal options like stainless steel offer durability, while glass appeals to eco-conscious consumers. Silicone bottles gain popularity for flexibility and safety. Market growth is bolstered by rising awareness and health concerns, driving industry adoption of alternative materials.

Get Customized Report as per Your Business Requirement - Request For Customized Report

By Product Type

Water Bottles

Cans

Shakers

Tumblers

Mason Jars

Others

Hydration containers, designed for water and beverage storage on-the-go, are gaining popularity thanks to rising health awareness and the demand for sustainable alternatives to disposable plastic bottles. This trend is driving revenue growth in the Hydration Containers Market.

By Capacity

Up to 20 oz

21-40 oz

41-60 oz

Above 60 oz

The up to 20 oz segment is popular in the hydration container market, favored for its small, lightweight design suitable for daily use and activities like commuting and exercising. It also includes kid-friendly options with colorful designs. On the other hand, the above 60 oz segment appeals to consumers needing larger water capacity for activities like hiking and camping, as well as group events. However, the 21-40 oz and 41-60 oz segments are less popular.

By Distribution Channel

Online

Direct Sales

Retailers

The retailers sector remains pivotal in the hydration container market, spanning specialty stores, department stores, supermarkets/hypermarkets, and outdoor retailers. These outlets provide consumers with a wide range of hydration containers, allowing them to compare and select products based on their preferences. Seasonal discounts, bundle deals, and promotions offered by retailers attract price-sensitive consumers. This sector's substantial market share is attributed to its ability to cater to consumers who prefer in-person shopping experiences.

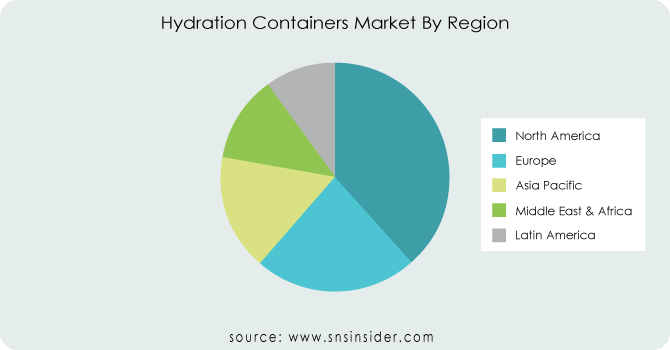

North America leads the Hydration Containers market due to heightened health awareness and active lifestyles. The region's demand is driven by specialized containers for athletes and outdoor enthusiasts, favored for their convenience. North Americans value on-the-go solutions, making portable hydration containers popular. Additionally, rising environmental consciousness fuels the adoption of reusable options, reducing reliance on single-use plastics.

Europe ranks second in the Hydration Containers market, driven by a focus on health, outdoor activities, and sports. Established brands and manufacturers bolster market growth, with the UK, Germany, and France leading in market share. Meanwhile, the Asia-Pacific region emerges as the fastest-growing market, fueled by urbanization, rising incomes, and a growing interest in health and outdoor pursuits. China leads in market share, with India showing rapid growth.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Some of the major players in the Hydration Containers Market are CamelBak Products, Brita GmbH, Klean Kanteen, Tupperware Brands Corporation, Contigo, Aquasana, Nathan Sports, Nalgen Nunc International, Cascade Designs, HydraPak and other players.

CamelBak Products -Company Financial Analysis

In November 2022, Nalgene launched a fresh series of reusable water bottles crafted from plant-derived materials such as sugarcane and corn. These BPA-free bottles are engineered to offer durability and longevity.

In July 2022, Hydro Flask revealed its collaboration with the National Park Foundation to introduce a special collection of water bottles showcasing designs inspired by national parks. A percentage of sales from each bottle will go towards supporting the National Park Foundation.

In March 2022, Brita launched a fresh range of water bottles equipped with built-in filters capable of eliminating chlorine, odors, and other impurities found in tap water. Available in different sizes and colors, these bottles are specifically designed for convenient hydration on the go.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 13.63 Billion |

| Market Size by 2031 | US$ 25.60 Billion |

| CAGR | CAGR of 8.2 % From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Polymers, Silicone, Metal, Glass) • By Product Type (Water Bottles, Cans, Shakers, Tumblers, Mason Jars, Others) • By Capacity (Up To 20 Oz, 21-40 Oz, 41-60 Oz, Above 60 Oz) • By Distribution Channel (Online, Direct Sales, Retailers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | CamelBak Products, Brita GmbH, Klean Kanteen, Tupperware Brands Corporation, Contigo, Aquasana, Nathan Sports, Nalgen Nunc International, Cascade Designs, HydraPak |

| Key Drivers | • Market growth stimulated by growing awareness and user friendly packaging solutions • Increased disposable income has led consumers to allocate more funds towards convenience products. |

| Challenges | • Rapid shifts in consumer preferences and trends can pose a challenge for companies to keep up with in terms of product design and features. |

Ans: The Hydration Containers Market is expected to grow at a CAGR of 8.2%.

Ans: The Hydration Containers Market size was USD 13.63 billion in 2023 and is expected to Reach USD 25.60 billion by 2031.

Ans: Market growth stimulated by growing awareness and user friendly packaging solutions.

Ans: Low-quality alternatives being readily accessible pose a challenge in the market.

Ans: The North America region held the largest market share and will continue to dominate the market.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Hydration Containers Market Segmentation, By Material

9.1 Introduction

9.2Trend Analysis

9.3 Polymers

9.4 Silicone

9.5 Metal

9.6 Glass

10. Hydration Containers Market Segmentation, By Product Type

10.1 Introduction

10.2 Trend Analysis

10.3 Water Capacitys

10.4 Cans

10.5 Shakers

10.6 Tumblers

10.7 Mason Jars

10.8 Others

11. Hydration Containers Market Segmentation, By Capacity

11.1 Introduction

11.2Trend Analysis

11.3 Up to 20 oz

11.4 21-40 oz

11.5 41-60 oz

11.6 Above 60 oz

12. Hydration Containers Market Segmentation, By Distribution Channel

12.1 Introduction

12.2 Trend Analysis

12.3 Online

12.4 Direct Sales

12.5 Retailers

13. Regional Analysis

13.1 Introduction

13.2 North America

13.2.1 Trend Analysis

13.2.2 North America Hydration Containers Market By Country

13.2.3 North America Hydration Containers Market By Material

13.2.4 North America Hydration Containers Market By Product Type

13.2.5 North America Hydration Containers Market By Capacity

13.2.6 North America Hydration Containers Market By Distribution Channel

13.2.7 USA

13.2.7.1 USA Hydration Containers Market By Material

13.2.7.2 USA Hydration Containers Market By Product Type

13.2.7.3 USA Hydration Containers Market By Capacity

13.2.7.4 USA Hydration Containers Market By Distribution Channel

13.2.8 Canada

13.2.8.1 Canada Hydration Containers Market By Material

13.2.8.2 Canada Hydration Containers Market By Product Type

13.2.8.3 Canada Hydration Containers Market By Capacity

13.2.8.4 Canada Hydration Containers Market By Distribution Channel

13.2.9 Mexico

13.2.9.1 Mexico Hydration Containers Market By Material

13.2.9.2 Mexico Hydration Containers Market By Product Type

13.2.9.3 Mexico Hydration Containers Market By Capacity

13.2.9.4 Mexico Hydration Containers Market By Distribution Channel

13.3 Europe

13.3.1 Trend Analysis

13.3.2 Eastern Europe

13.3.2.1 Eastern Europe Hydration Containers Market By Country

13.3.2.2 Eastern Europe Hydration Containers Market By Material

13.3.2.3 Eastern Europe Hydration Containers Market By Product Type

13.3.2.4 Eastern Europe Hydration Containers Market By Capacity

13.3.2.5 Eastern Europe Hydration Containers Market By Distribution Channel

13.3.2.6 Poland

13.3.2.6.1 Poland Hydration Containers Market By Material

13.3.2.6.2 Poland Hydration Containers Market By Product Type

13.3.2.6.3 Poland Hydration Containers Market By Capacity

13.3.2.6.4 Poland Hydration Containers Market By Distribution Channel

13.3.2.7 Romania

13.3.2.7.1 Romania Hydration Containers Market By Material

13.3.2.7.2 Romania Hydration Containers Market By Product Type

13.3.2.7.3 Romania Hydration Containers Market By Capacity

13.3.2.7.4 Romania Hydration Containers Market By Distribution Channel

13.3.2.8 Hungary

13.3.2.8.1 Hungary Hydration Containers Market By Material

13.3.2.8.2 Hungary Hydration Containers Market By Product Type

13.3.2.8.3 Hungary Hydration Containers Market By Capacity

13.3.2.8.4 Hungary Hydration Containers Market By Distribution Channel

13.3.2.9 Turkey

13.3.2.9.1 Turkey Hydration Containers Market By Material

13.3.2.9.2 Turkey Hydration Containers Market By Product Type

13.3.2.9.3 Turkey Hydration Containers Market By Capacity

13.3.2.9.4 Turkey Hydration Containers Market By Distribution Channel

13.3.2.10 Rest of Eastern Europe

13.3.2.10.1 Rest of Eastern Europe Hydration Containers Market By Material

13.3.2.10.2 Rest of Eastern Europe Hydration Containers Market By Product Type

13.3.2.10.3 Rest of Eastern Europe Hydration Containers Market By Capacity

13.3.2.10.4 Rest of Eastern Europe Hydration Containers Market By Distribution Channel

13.3.3 Western Europe

13.3.3.1 Western Europe Hydration Containers Market By Country

13.3.3.2 Western Europe Hydration Containers Market By Material

13.3.3.3 Western Europe Hydration Containers Market By Product Type

13.3.3.4 Western Europe Hydration Containers Market By Capacity

13.3.3.5 Western Europe Hydration Containers Market By Distribution Channel

13.3.3.6 Germany

13.3.3.6.1 Germany Hydration Containers Market By Material

13.3.3.6.2 Germany Hydration Containers Market By Product Type

13.3.3.6.3 Germany Hydration Containers Market By Capacity

13.3.3.6.4 Germany Hydration Containers Market By Distribution Channel

13.3.3.7 France

13.3.3.7.1 France Hydration Containers Market By Material

13.3.3.7.2 France Hydration Containers Market By Product Type

13.3.3.7.3 France Hydration Containers Market By Capacity

13.3.3.7.4 France Hydration Containers Market By Distribution Channel

13.3.3.8 UK

13.3.3.8.1 UK Hydration Containers Market By Material

13.3.3.8.2 UK Hydration Containers Market By Product Type

13.3.3.8.3 UK Hydration Containers Market By Capacity

13.3.3.8.4 UK Hydration Containers Market By Distribution Channel

13.3.3.9 Italy

13.3.3.9.1 Italy Hydration Containers Market By Material

13.3.3.9.2 Italy Hydration Containers Market By Product Type

13.3.3.9.3 Italy Hydration Containers Market By Capacity

13.3.3.9.4 Italy Hydration Containers Market By Distribution Channel

13.3.3.10 Spain

13.3.3.10.1 Spain Hydration Containers Market By Material

13.3.3.10.2 Spain Hydration Containers Market By Product Type

13.3.3.10.3 Spain Hydration Containers Market By Capacity

13.3.3.10.4 Spain Hydration Containers Market By Distribution Channel

13.3.3.11 Netherlands

13.3.3.11.1 Netherlands Hydration Containers Market By Material

13.3.3.11.2 Netherlands Hydration Containers Market By Product Type

13.3.3.11.3 Netherlands Hydration Containers Market By Capacity

13.3.3.11.4 Netherlands Hydration Containers Market By Distribution Channel

13.3.3.12 Switzerland

13.3.3.12.1 Switzerland Hydration Containers Market By Material

13.3.3.12.2 Switzerland Hydration Containers Market By Product Type

13.3.3.12.3 Switzerland Hydration Containers Market By Capacity

13.3.3.12.4 Switzerland Hydration Containers Market By Distribution Channel

13.3.3.13 Austria

13.3.3.13.1 Austria Hydration Containers Market By Material

13.3.3.13.2 Austria Hydration Containers Market By Product Type

13.3.3.13.3 Austria Hydration Containers Market By Capacity

13.3.3.13.4 Austria Hydration Containers Market By Distribution Channel

13.3.3.14 Rest of Western Europe

13.3.3.14.1 Rest of Western Europe Hydration Containers Market By Material

13.3.3.14.2 Rest of Western Europe Hydration Containers Market By Product Type

13.3.3.14.3 Rest of Western Europe Hydration Containers Market By Capacity

13.3.3.14.4 Rest of Western Europe Hydration Containers Market By Distribution Channel

13.4 Asia-Pacific

13.4.1 Trend Analysis

13.4.2 Asia-Pacific Hydration Containers Market By Country

13.4.3 Asia-Pacific Hydration Containers Market By Material

13.4.4 Asia-Pacific Hydration Containers Market By Product Type

13.4.5 Asia-Pacific Hydration Containers Market By Capacity

13.4.6 Asia-Pacific Hydration Containers Market By Distribution Channel

13.4.7 China

13.4.7.1 China Hydration Containers Market By Material

13.4.7.2 China Hydration Containers Market By Product Type

13.4.7.3 China Hydration Containers Market By Capacity

13.4.7.4 China Hydration Containers Market By Distribution Channel

13.4.8 India

13.4.8.1 India Hydration Containers Market By Material

13.4.8.2 India Hydration Containers Market By Product Type

13.4.8.3 India Hydration Containers Market By Capacity

13.4.8.4 India Hydration Containers Market By Distribution Channel

13.4.9 Japan

13.4.9.1 Japan Hydration Containers Market By Material

13.4.9.2 Japan Hydration Containers Market By Product Type

13.4.9.3 Japan Hydration Containers Market By Capacity

13.4.9.4 Japan Hydration Containers Market By Distribution Channel

13.4.10 South Korea

13.4.10.1 South Korea Hydration Containers Market By Material

13.4.10.2 South Korea Hydration Containers Market By Product Type

13.4.10.3 South Korea Hydration Containers Market By Capacity

13.4.10.4 South Korea Hydration Containers Market By Distribution Channel

13.4.11 Vietnam

13.4.11.1 Vietnam Hydration Containers Market By Material

13.4.11.2 Vietnam Hydration Containers Market By Product Type

13.4.11.3 Vietnam Hydration Containers Market By Capacity

13.4.11.4 Vietnam Hydration Containers Market By Distribution Channel

13.4.12 Singapore

13.4.12.1 Singapore Hydration Containers Market By Material

13.4.12.2 Singapore Hydration Containers Market By Product Type

13.4.12.3 Singapore Hydration Containers Market By Capacity

13.4.12.4 Singapore Hydration Containers Market By Distribution Channel

13.4.13 Australia

13.4.13.1 Australia Hydration Containers Market By Material

13.4.13.2 Australia Hydration Containers Market By Product Type

13.4.13.3 Australia Hydration Containers Market By Capacity

13.4.13.4 Australia Hydration Containers Market By Distribution Channel

13.4.14 Rest of Asia-Pacific

13.4.14.1 Rest of Asia-Pacific Hydration Containers Market By Material

13.4.14.2 Rest of Asia-Pacific Hydration Containers Market By Product Type

13.4.14.3 Rest of Asia-Pacific Hydration Containers Market By Capacity

13.4.14.4 Rest of Asia-Pacific Hydration Containers Market By Distribution Channel

13.5 Middle East & Africa

13.5.1 Trend Analysis

13.5.2 Middle East

13.5.2.1 Middle East Hydration Containers Market By Country

13.5.2.2 Middle East Hydration Containers Market By Material

13.5.2.3 Middle East Hydration Containers Market By Product Type

13.5.2.4 Middle East Hydration Containers Market By Capacity

13.5.2.5 Middle East Hydration Containers Market By Distribution Channel

13.5.2.6 UAE

13.5.2.6.1 UAE Hydration Containers Market By Material

13.5.2.6.2 UAE Hydration Containers Market By Product Type

13.5.2.6.3 UAE Hydration Containers Market By Capacity

13.5.2.6.4 UAE Hydration Containers Market By Distribution Channel

13.5.2.7 Egypt

13.5.2.7.1 Egypt Hydration Containers Market By Material

13.5.2.7.2 Egypt Hydration Containers Market By Material

13.5.2.7.3 Egypt Hydration Containers Market By Capacity

13.5.2.7.4 Egypt Hydration Containers Market By Distribution Channel

13.5.2.8 Saudi Arabia

13.5.2.8.1 Saudi Arabia Hydration Containers Market By Material

13.5.2.8.2 Saudi Arabia Hydration Containers Market By Product Type

13.5.2.8.3 Saudi Arabia Hydration Containers Market By Capacity

13.5.2.8.4 Saudi Arabia Hydration Containers Market By Distribution Channel

13.5.2.9 Qatar

13.5.2.9.1 Qatar Hydration Containers Market By Material

13.5.2.9.2 Qatar Hydration Containers Market By Product Type

13.5.2.9.3 Qatar Hydration Containers Market By Capacity

13.5.2.9.4 Qatar Hydration Containers Market By Distribution Channel

13.5.2.10 Rest of Middle East

13.5.2.10.1 Rest of Middle East Hydration Containers Market By Material

13.5.2.10.2 Rest of Middle East Hydration Containers Market By Product Type

13.5.2.10.3 Rest of Middle East Hydration Containers Market By Capacity

13.5.2.10.4 Rest of Middle East Hydration Containers Market By Distribution Channel

13.5.3 Africa

13.5.3.1 Africa Hydration Containers Market By Country

13.5.3.2 Africa Hydration Containers Market By Material

13.5.3.3 Africa Hydration Containers Market By Product Type

13.5.3.4 Africa Hydration Containers Market By Capacity

13.5.3.5 Africa Hydration Containers Market By Distribution Channel

13.5.3.6 Nigeria

13.5.3.6.1 Nigeria Hydration Containers Market By Material

13.5.3.6.2 Nigeria Hydration Containers Market By Product Type

13.5.3.6.3 Nigeria Hydration Containers Market By Capacity

13.5.3.6.4 Nigeria Hydration Containers Market By Distribution Channel

13.5.3.7 South Africa

13.5.3.7.1 South Africa Hydration Containers Market By Material

13.5.3.7.2 South Africa Hydration Containers Market By Product Type

13.5.3.7.3 South Africa Hydration Containers Market By Capacity

13.5.3.7.4 South Africa Hydration Containers Market By Distribution Channel

13.5.3.8 Rest of Africa

13.5.3.8.1 Rest of Africa Hydration Containers Market By Material

13.5.3.8.2 Rest of Africa Hydration Containers Market By Product Type

13.5.3.8.3 Rest of Africa Hydration Containers Market By Capacity

13.5.3.8.4 Rest of Africa Hydration Containers Market By Distribution Channel

13.6 Latin America

13.6.1 Trend Analysis

13.6.2 Latin America Hydration Containers Market By country

13.6.3 Latin America Hydration Containers Market By Material

13.6.4 Latin America Hydration Containers Market By Product Type

13.6.5 Latin America Hydration Containers Market By Capacity

13.6.6 Latin America Hydration Containers Market By Distribution Channel

13.6.7 Brazil

13.6.7.1 Brazil Hydration Containers Market By Material

13.6.7.2 Brazil Hydration Containers Market By Product Type

13.6.7.3 Brazil Hydration Containers Market By Capacity

13.6.7.4 Brazil Hydration Containers Market By Distribution Channel

13.6.8 Argentina

13.6.8.1 Argentina Hydration Containers Market By Material

13.6.8.2 Argentina Hydration Containers Market By Product Type

13.6.8.3 Argentina Hydration Containers Market By Capacity

13.6.8.4 Argentina Hydration Containers Market By Distribution Channel

13.6.9 Colombia

13.6.9.1 Colombia Hydration Containers Market By Material

13.6.9.2 Colombia Hydration Containers Market By Product Type

13.6.9.3 Colombia Hydration Containers Market By Capacity

13.6.9.4 Colombia Hydration Containers Market By Distribution Channel

13.6.10 Rest of Latin America

13.6.10.1 Rest of Latin America Hydration Containers Market By Material

13.6.10.2 Rest of Latin America Hydration Containers Market By Product Type

13.6.10.3 Rest of Latin America Hydration Containers Market By Capacity

13.6.10.4 Rest of Latin America Hydration Containers Market By Distribution Channel

14. Company Profiles

14.1 CamelBak Products

14.1.1 Company Overview

14.1.2 Financial

14.1.3 Products / Services Offered

14.1.4 SWOT Analysis

14.1.5 The SNS View

14.2 Brita GmbH

14.2.1 Company Overview

14.2.2 Financial

14.2.3 Products / Services Offered

14.2.4 SWOT Analysis

14.2.5 The SNS View

14.3 Klean Kanteen

14.3.1 Company Overview

14.3.2 Financial

14.3.3 Products / Services Offered

14.3.4 SWOT Analysis

14.3.5 The SNS View

14.4 Tupperware Brands Corporation

14.4.1 Company Overview

14.4.2 Financial

14.4.3 Products / Services Offered

14.4.4 SWOT Analysis

14.4.5 The SNS View

14.5 Contigo

14.5.1 Company Overview

14.5.2 Financial

14.5.3 Products / Services Offered

14.5.4 SWOT Analysis

14.5.5 The SNS View

14.6 Aquasana

14.6.1 Company Overview

14.6.2 Financial

14.6.3 Products / Services Offered

14.6.4 SWOT Analysis

14.6.5 The SNS View

14.7 Nathan Sports

14.7.1 Company Overview

14.7.2 Financial

14.7.3 Products / Services Offered

14.7.4 SWOT Analysis

14.7.5 The SNS View

14.8 Nalgen Nunc International

14.8.1 Company Overview

14.8.2 Financial

14.8.3 Products / Services Offered

14.8.4 SWOT Analysis

14.8.5 The SNS View

14.9 Cascade Designs

14.9.1 Company Overview

14.9.2 Financial

14.9.3 Products / Services Offered

14.9.4 SWOT Analysis

14.9.5 The SNS View

14.10 HydraPak

14.10.1 Company Overview

14.10.2 Financial

14.10.3 Products / Services Offered

14.10.4 SWOT Analysis

14.10.5 The SNS View

15. Competitive Landscape

15.1 Competitive Benchmarking

15.2 Market Share Analysis

15.3 Recent Developments

15.3.1 Industry News

15.3.2 Company News

15.3.3 Mergers & Acquisitions

16. Use Case and Best Practices

17. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Sterilized Packaging Market Share was USD 31.78 Billion in 2023 and will reach USD 50.27 Billion by 2032, growing at a CAGR of 5.24% by 2024-2032.

The Hazardous Disposal Bag Market size was valued at USD 0.99 Billion and expected to Reach USD 1.47 Billion by 2031 and grow at a CAGR of 4.45% over the forecast period of 2024-2031.

The Pressure-Sensitive Labels Market size was valued at USD 42.18 billion in 2023. It is expected to grow to USD 74.95 billion by 2032 and grow at a CAGR of 6.60% over the forecast period of 2024-2032.

The Food Service Packaging Market was valued at USD 123.29 billion in 2023 and to reach USD 178.10 billion by 2032, growing CAGR of 4.70% by 2032.

The Single-Use Packaging Market size was USD 26.12 billion in 2023 and is expected to Reach USD 42.27 billion by 2031 and grow at a CAGR of 6.2% over the forecast period of 2024-2031.

The Compostable Food Service Packaging Market size was USD 18.75 billion in 2023 and is expected to Reach USD 27.29 billion by 2031 and grow at a CAGR of 4.8% over the forecast period of 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd