The Huntington’s Disease Treatment market size was USD 445.90 million in 2023 and is expected to reach USD 2670.13 million by 2032 and grow at a CAGR of 22.00% over the forecast period of 2024-2032. This report provides comprehensive insights into the Huntington’s disease treatment market, including detailed prevalence and incidence statistics across key regions and age groups. The report showcases the recent market trends in the diagnosed versus undiagnosed cases and the surging number of genetic carriers. The study also examines the growing clinical pipeline, with a strong focus on the ongoing trials and drug development stages. The surged burden of healthcare and treatment costs are analyzed in the report to assess the economic impact. Regulatory insights, such as approval timelines and orphan drug designations, are also covered in the report.

Additionally, the report explores the current trends in genetic screening uptake and patient support initiatives. Collectively, these insights also provide a well-rounded view of the market beyond standard sizing and segmentation.

The U.S. held the largest share in the Huntington’s disease treatment market in 2023, valued at USD 140.98 Million, and is projected to reach USD 862.29 Million by 2032, growing at an impressive CAGR of 22.29% during the forecast period. The dominance of the market is propelled by many major factors, such as the high Huntington’s disease prevalence in the U.S., ranging between 5 and 10 cases per 100,000 people globally. The country also benefits from strong diagnostic capabilities, advanced healthcare infrastructure, and global availability of genetic testing, further enabling for earlier and accurate detection.

Although, the U.S. has a highly active pipeline of drug development backed by substantial investments from both the private and public. Many regulatory incentives, including fast-track and orphan drug designation approvals by the U.S. FDA, further augmenting the therapeutic innovation. In addition, a well-established network of patient advocacy groups and clinical research institutions ensures large awareness, easy access to emerging treatments, and early intervention, further reinforcing the leading position of the U.S. in the global market.

Drivers

Rising Prevalence of Huntington’s Disease Drives Treatment Demand Globally

The Huntington’s disease treatment market growth is substantially driven by the surging prevalence of the Huntington’s disease and growing advancements in the genetic testing technologies. The accurate and early diagnosis via genetic screening has enhanced the disease management and treatment initiation, thus increasing the patient pool. In the developed regions, enhanced family history tracking, awareness campaigns, and high accessibility to genetic counseling, are all contributing to a surge in the diagnosis rates. However, investment in genetic therapies and research collaborations by the key players, such as Wave Life Sciences and Ionis Pharmaceuticals have further boosted the growth of the market. This surging burden of the disease, incorporate with the technological advances in disease diagnostics and a proactive healthcare system, continues to aid the Huntington’s disease treatment market growth.

Restraints:

High Treatment Costs and Limited Advanced Therapies’ Affordability Hinders Market Expansion Globally

One of the key restraints impeding the Huntington’s disease treatment market growth is the high cost of the therapies available and limited affordability in the low-income nations globally. Advanced therapies including antisense oligonucleotide and gene-silencing treatments, which generally cost tens of thousands of dollars per patient annually. The long-term disease management require continuous support, symptomatic treatment, and rehabilitation contributing to a high economic burden. In several regions, the lack of reimbursement frameworks in the public healthcare systems for rare diseases, such as Huntington’s disease, which makes treatment inaccessible to a substantial portion of the global population. Even in developed regions, the insurance coverage for emerging therapies is still uncertain, further hampering the patient access. As a result, even after the growing awareness and clinical advancements, the adoption rates of such treatments in the under-resourced nations remain low, curbing the overall global market penetration and negatively affecting the equitable treatment distribution across various regions.

Opportunities:

Emergence of Gene-Silencing and Disease-Modifying Therapies Offers Strong Growth Opportunities for Key Market Players

Significant growth opportunities in the Huntington’s disease treatment market are expected to arise due to the rising development of gene-silencing and disease-modifying therapies globally. Traditional treatments are initially focused on managing symptoms; however, the recent innovations are targeting the root genetic causes of Huntington’s disease. Several key players, such as Novartis, Roche, and Wave Life Sciences are actively engaged in the clinical trials to launch such therapies in the market. The burgeoning number of regulatory designations, including the Orphan Drug and Fast Track status also boosts the drug approvals and R&D efforts. These innovations have the potential to reduce the disease progression that can completely transform the treatment landscape of the disease. With the growing number of investments from the government and biotech firms, and strong pipeline of candidates, the launch of new and effective gene-targeting therapies can not only increase the life expectancy but also improve the quality of life for patients globally.

Challenges:

Lack of Curative Therapies and Limited Disease Progression’s Understanding Pose Substantial Challenges for Market Augmentation

A substantial challenge impacting the growth of the Huntington’s disease treatment market is the lack of disease’s complex progression understand and limited availability of curative therapies. Huntington’s Disease affects different neurological functions, which are progressing differently across patients, further complicating both diagnosis and treatment planning. In spite of the advancements in genetic testing, along with symptom severity, prediction of the exact onset age of onset, and progression speed remains difficult.

However, currently, there are no approved existing therapy, which fully curb or reverse the neurodegeneration related with the disease. The current medications only offer symptomatic relief, and several experimental drugs have not been able to generate results in the late-stage clinical trials owing to the safety concerns or limited efficacy. This scientific gap not only extends patient suffering but also have a major hurdle for pharmaceutical companies that are focusing on the development of breakthrough treatments, further decreasing the speed of clinical success and innovation in the field.

By Treatment

Based on treatment, the market is bifurcated into symptomatic treatment and disease-modifying therapies. The symptomatic treatment held the largest Huntington’s disease treatment market share of around 78% in 2023. The lack of approved disease-modifying therapies and the growing urgent need for managing the large range of debilitating symptoms related to the condition drive the segment’s expansion in the market. Huntington’s disease grows via progressive motor dysfunction, psychiatric disturbances, and cognitive decline, all of which substantially affecting the patient’s quality of life. As no cure for the disease currently exists, the treatment strategies are initially focused on reducing these symptoms by utilizing medications including antidepressants, antipsychotics, and mood stabilizers.

Additionally, supportive interventions, such as occupational therapy and physiotherapy are commonly adopted to improve patients’ daily functioning. The regulatory approval, accessibility, and established efficacy of these treatments have contributed to their large adoption in the clinical practices globally. As a result, symptomatic treatment remains the foundation of patient care, further boosting the segment in the market.

By End-Use Industry

On the basis of end-use industry, the market is divided into hospital pharmacy, retail pharmacy, and e-commerce. In 2023, the hospital pharmacy segment dominated the market holding a revenue share of around 57%. The segment’s expansion is propelled by the specialized and complex nature of managing the disease that generally requires coordinated care and advanced or high-cost therapies prescription. Patients suffering from Huntington’s disease frequently witness a range of serious psychiatric and neurological symptoms, which demand close monitoring, multidisciplinary support, and dose adjustments, which are easily available in the hospital settings.

Although, hospital pharmacies are considered to be the initial dispensing points for the latest or investigational treatments, which include gene-silencing therapies or drugs under concerned programs. These facilities also confirm compliance with the strict and regulatory, especially for the orphan drugs. In addition, the growing availability of neurologists and specialized care teams in hospitals makes hospital pharmacy, a preferred setting to initiate and manage treatment, further strengthening the dominance of hospital pharmacies in the market.

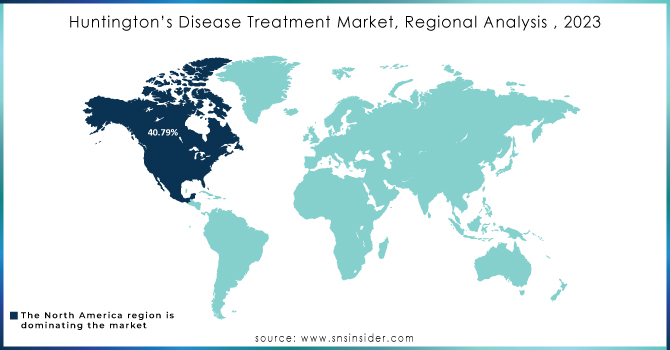

In 2023, North America was the dominating region in the market holding a revenue share of approximately. The region’s growth is driven by a combination of advanced healthcare infrastructure, strong research and development investments, and high disease prevalence. North America, particularly the U.S., has recorded some of the highest diagnosis rates across the globe, with approximately 10 cases per 100,000 people, propelled by the wide access to the early screening and genetic testing programs. North America is also benefited from a strong network of academic research centers and biopharmaceutical companies, which are actively engaged in the development of novel treatments, such as disease modifying drugs and gene therapies. Furthermore, several supportive regulatory frameworks, including the U.S. FDA’s Orphan Drug Designation and Fast Track programs, have boosted the drug development and approvals in the region. Strong insurance coverage, high healthcare spending, and well-established established treatment protocols further improve patients’ access to advanced therapies, setting North America’s leadership in the global market.

Asia Pacific held a substantial market share in the Huntington’s disease treatment market owing to its large population base, along with surging rare genetic disorders awareness, and enhancing healthcare infrastructure across multiple emerging economies. Nations including South Korea, China, and Japan, have been experiencing burgeoning efforts in the early diagnosis and genetic testing, backed by several government health initiatives and the neurology-focused healthcare services expansion. In addition, several international partnerships with the global pharmaceutical firms are allowing for faster access to innovative clinical trials and innovative treatments in the region. The increasing availability of specialized care in the urban centers, integrated with the growing healthcare expenditure, is further boosting the demand for Huntington’s disease treatment globally.

However, rising patient advocacy efforts and supportive regulatory reforms are encouraging earlier diagnosis and treatment adoption, making Asia Pacific an influential and rapidly emerging market globally.

Do You Need any Customization Research on Huntington’s Disease Treatment Market - Enquire Now

Neurocrine Biosciences (Ingrezza, Valbenazine)

NeuExcell Therapeutics Inc (NEU-CH16, NEU-CH20)

H. Lundbeck A/S (Xenazine, Austedo)

Teva Pharmaceutical Industries Ltd (Austedo, Azilect)

Bausch Health Companies Inc. (Tetrabenazine, Aplenzin)

Hetero (Tetrabenazine, Haloperidol)

Lupin (Risperidone, Haloperidol)

Hikma Pharmaceuticals PLC (Tetrabenazine, Quetiapine)

Dr. Reddy’s Laboratories Ltd. (Tetrabenazine, Risperidone)

Sun Pharmaceutical Industries Ltd. (Tetrabenazine, Olanzapine)

Novartis AG (Exelon, Tegretol)

Pfizer Inc. (Zoloft, Geodon)

Roche Holding AG (Tominersen, Madopar)

Ionis Pharmaceuticals, Inc. (IONIS-HTTRx, BIIB067)

Wave Life Sciences (WVE-003, WVE-120101)

Sage Therapeutics (SAGE-718, SAGE-324)

Azevan Pharmaceuticals (SRX246, SRX251)

Voyager Therapeutics (VY-HTT01, VY-AADC)

uniQure N.V. (AMT-130, Glybera)

PTC Therapeutics, Inc. (PTC518, Emflaza)

In December 2024, PTC Therapeutics signed a licensing deal with Novartis valued at up to USD 2.9 billion for PTC518, an experimental drug targeting Huntington’s disease. The drug has demonstrated potential in lowering mutant Huntingtin protein levels. Novartis will lead the drug’s development, manufacturing, and commercialization.

In May 2024, Teva received U.S. FDA approval for its extended-release Austedo (deutetrabenazine) tablets as a once-daily treatment for chorea linked to Huntington's disease. This milestone is anticipated to improve patient adherence. It also strengthens Teva's presence in the Huntington’s disease treatment market.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 445.90 Million |

| Market Size by 2032 | USD 2670.13 Million |

| CAGR | CAGR of 22.00% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment (Symptomatic Treatment, Disease-modifying Therapies) • By End-Use Industry (Hospital Pharmacy, Retail Pharmacy, E-commerce) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Neurocrine Biosciences, NeuExcell Therapeutics Inc, H. Lundbeck A/S, Teva Pharmaceutical Industries Ltd, Bausch Health Companies Inc., Hetero, Lupin, Hikma Pharmaceuticals PLC, Dr. Reddy’s Laboratories Ltd., Sun Pharmaceutical Industries Ltd, Novartis AG, Pfizer Inc., Roche Holding AG, Ionis Pharmaceuticals Inc., Wave Life Sciences, Sage Therapeutics, Azevan Pharmaceuticals, Voyager Therapeutics, uniQure N.V., PTC Therapeutics Inc. |

Ans: The Huntington’s Disease Treatment Market was valued at USD 445.90 Million in 2023.

Ans: The expected CAGR of the global Huntington’s Disease Treatment Market during the forecast period is 22%

Ans: Hospital Pharmacy will grow rapidly in the Huntington’s Disease Treatment Market from 2024 to 2032.

Ans: The increasing prevalence of huntington’s disease, coupled with advancements in genetic testing, drives market demand worldwide.

Ans: North America led the Huntington’s Disease Treatment Market in the region with the highest revenue share in 2023.

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Prevalence & Incidence Rates

5.2 Approval Timelines and Regulatory Statistics

5.3 Mergers & Acquisitions in the Medical Financing Sector

5.4 Diagnosed vs. Undiagnosed Cases

5.5 Innovation and R&D, Type, 2023

6. Competitive Landscape

6.1 List of Major Companies By Region

6.2 Market Share Analysis By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion Plans and New Product Launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Huntington’s Disease Treatment Market Segmentation By Treatment

7.1 Chapter Overview

7.2 Symptomatic Treatment

7.2.1 Symptomatic Treatment Trends Analysis (2020-2032)

7.2.2 Symptomatic Treatment Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 Disease-Modifying Therapies

7.3.1 Disease-modifying Therapies Market Trends Analysis (2020-2032)

7.3.2 Disease-modifying Therapies Market Size Estimates and Forecasts to 2032 (USD Million)

8. Huntington’s Disease Treatment Market Segmentation By End Use Industry

8.1 Chapter Overview

8.2 Hospital Pharmacy

8.2.1 Hospital Pharmacy Market Trends Analysis (2020-2032)

8.2.2 Hospital Pharmacy Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Retail Pharmacy

8.3.1 Retail Pharmacy Market Trends Analysis (2020-2032)

8.3.2 Retail Pharmacy Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 E-commerce

8.4.1 E-commerce Market Trends Analysis (2020-2032)

8.4.2 E-commerce Market Size Estimates and Forecasts to 2032 (USD Million)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Huntington’s Disease Treatment Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.2.3 North America Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.2.4 North America Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.2.5 USA

9.2.5.1 USA Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.2.5.2 USA Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.2.6 Canada

9.2.6.1 Canada Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.2.6.2 Canada Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.2.7 Mexico

9.2.7.1 Mexico Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.2.7.2 Mexico Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Huntington’s Disease Treatment Market Estimates and Forecasts by Country (2020-2032) (USD Million)

9.3.1.3 Eastern Europe Huntington’s Disease Treatment Market Estimates and Forecasts By Treatment (2020-2032) (USD Million)

9.3.1.4 Eastern Europe Huntington’s Disease Treatment Market Estimates and Forecasts By End Use Industry (2020-2032) (USD Million)

9.3.1.5 Poland

9.3.1.5.1 Poland Huntington’s Disease Treatment Market Estimates and Forecasts By Treatment (2020-2032) (USD Million)

9.3.1.5.2 Poland Huntington’s Disease Treatment Market Estimates and Forecasts By End Use Industry (2020-2032) (USD Million)

9.3.1.6 Romania

9.3.1.6.1 Romania Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.1.6.2 Romania Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.1.7.2 Hungary Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.1.8.2 Turkey Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.1.9.2 Rest of Eastern Europe Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Huntington’s Disease Treatment Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.3.2.3 Western Europe Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.4 Western Europe Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.5 Germany

9.3.2.5.1 Germany Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.5.2 Germany Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.6 France

9.3.2.6.1 France Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.6.2 France Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.7 UK

9.3.2.7.1 UK Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.7.2 UK Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.8 Italy

9.3.2.8.1 Italy Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.8.2 Italy Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.9 Spain

9.3.2.9.1 Spain Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.9.2 Spain Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.10.2 Netherlands Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.11.2 Switzerland Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.12 Austria

9.3.2.12.1 Austria Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.12.2 Austria Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.3.2.13.2 Rest of Western Europe Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific Huntington’s Disease Treatment Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.4.3 Asia Pacific Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.4 Asia Pacific Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.5 China

9.4.5.1 China Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.5.2 China Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.6 India

9.4.5.1 India Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.5.2 India Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.5 Japan

9.4.5.1 Japan Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.5.2 Japan Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.6 South Korea

9.4.6.1 South Korea Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.6.2 South Korea Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.7 Vietnam

9.4.7.1 Vietnam Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.2.7.2 Vietnam Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.8 Singapore

9.4.8.1 Singapore Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.8.2 Singapore Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.9 Australia

9.4.9.1 Australia Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.9.2 Australia Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.4.10.2 Rest of Asia Pacific Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Huntington’s Disease Treatment Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.5.1.3 Middle East Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.1.4 Middle East Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.1.5 UAE

9.5.1.5.1 UAE Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.1.5.2 UAE Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.1.6.2 Egypt Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.1.7.2 Saudi Arabia Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.1.8.2 Qatar Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.1.9.2 Rest of Middle East Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Huntington’s Disease Treatment Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.5.2.3 Africa Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.2.4 Africa Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.2.5.2 South Africa Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.5.2.6.2 Nigeria Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Huntington’s Disease Treatment Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

9.6.3 Latin America Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.6.4 Latin America Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.6.5 Brazil

9.6.5.1 Brazil Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.6.5.2 Brazil Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.6.6 Argentina

9.6.6.1 Argentina Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.6.6.2 Argentina Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.6.7 Colombia

9.6.7.1 Colombia Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.6.7.2 Colombia Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Huntington’s Disease Treatment Market Estimates and Forecasts, By Treatment (2020-2032) (USD Million)

9.6.8.2 Rest of Latin America Huntington’s Disease Treatment Market Estimates and Forecasts, By End Use Industry (2020-2032) (USD Million)

10. Company Profiles

10.1 Neurocrine Biosciences

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Product / Services Offered

10.1.4 SWOT Analysis

10.2 NeuExcell Therapeutics Inc

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Product/ Services Offered

10.2.4 SWOT Analysis

10.3 H. Lundbeck A/S

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Product/ Services Offered

10.3.4 SWOT Analysis

10.4 Teva Pharmaceutical Industries Ltd

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Product/ Services Offered

10.4.4 SWOT Analysis

10.5 Bausch Health Companies Inc.

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Product/ Services Offered

10.5.4 SWOT Analysis

10.6 Hetero

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Product/ Services Offered

10.6.4 SWOT Analysis

10.7 Lupin

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Product/ Services Offered

10.7.4 SWOT Analysis

10.8 Hikma Pharmaceuticals PLC

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Product/ Services Offered

10.8.4 SWOT Analysis

10.9 Dr. Reddy’s Laboratories Ltd.

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Product/ Services Offered

10.9.4 SWOT Analysis

10.10 Sun Pharmaceutical Industries Ltd

10.10.1 Company Overview

10.10.2 Financial

10.10.3 Product/ Services Offered

10.10.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Treatment

Symptomatic Treatment

Disease-modifying Therapies

By End Use Industry

Hospital Pharmacy

Retail Pharmacy

E-commerce

Request for Segment Customization as per your Business Requirement: Segment Customization Request

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Small Animal Imaging (In Vivo) Market Size was valued at USD 1.16 billion in 2023 and is expected to reach USD 2.27 billion by 2032 and grow at a CAGR of 7.76% over the forecast period 2024-2032.

The Interventional oncology Market Size was valued at USD 3.145 billion in 2023 and is expected to reach USD 6.862 billion by 2032 and grow at a CAGR of 9.07% over the forecast period 2024-2032.

Cell-based Assays Market was valued at USD 17.11 billion in 2023 and is expected to reach USD 35.34 billion by 2032, growing at a CAGR of 8.36% from 2024-2032.

Heating Pad Market size was valued at USD 51.78 billion in 2023 and is expected to grow to USD 81.52 billion by 2032 and grow at a CAGR of 5.19% from 2024-2032.

The ECG Patch & Holter Monitor Market size was valued at USD 1.60 Billion in 2023 and is expected to reach USD 7.78 Billion by 2032 and grow at a CAGR of 19.23% over the forecast period 2024-2032.

The Newborn Screening Market size was USD 880 million in 2023 and is expected to reach USD 1,710.7 million by 2032, growing at a 7.68% CAGR from 2024 to 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd