Get E-PDF Sample Report on Flat Steel Market - Request Sample Report

The Hot Melt Adhesives (HMA) Market was valued at USD 8.44 billion in 2023 and is expected to reach USD 12.10 Billion by 2032, growing at a CAGR of 4.11 % over the forecast period 2024-2032.

Rising demand within varied verticals including packaging, electronics, automobile, and pressure-sensitive products drives HMA market expansion. This growth can be largely attributed to the large use of HMAs in the packaging sector for carton sealing, labeling, and flexible packaging. Growing online shopping and online retail are driving the need for cost-effective, durable, and fast-bonding adhesives, boosting the market further. Apart from this, HMAs provide benefits like a fast cure period, flexibility, and very low Volatile Organic Compounds (VOCs) emissions, making it an environment-friendly and efficient alternative over traditional adhesives. Worldwide consumption of HMAs was +3 million tonnes in 2023 with 30-35% in packaging. 60% of HMA demand comes from e-commerce, with the automotive sector growing at 5-7% annually The HMAs have proven to cut VOC emissions by as much as 95%, cure in 1-2 seconds, and provide over a 20% savings in production costs.

Market growth is also driven by the increasing usage of HMAs in pressure-sensitive applications, such as tapes, labels, and medical products. Growing demand for lightweight high-strength adhesives, particularly in the automotive and electronics industries, is driving advances in product performance and durability. Novel formulations such as amorphous poly-alpha-olefin (AMOP) and metallocene polyolefins (MPO) have further enhanced thermal properties, flexibility, and adhesion force for targeted applications. Furthermore, increasing sustainable and bio-based adhesives interest leads to innovation as manufacturers now need to tackle sustainability concerns while adhering to the tough regulatory standards, which opens up even more opportunities for the market. Packaging accounted for 28% of the global PSA market in 2023, while medical products accounted for another 6%. The global adhesive ended demand was driven by the automotive industry which accounted for greater than 30% of the demand at 92 million vehicle productions. The adhesive demand from the electronics sector increased by 15% between 2022 and 2023, and growing trends towards the use of HMAs remain a part of this increase of durable adhesive and fast-curing properties present in HMAs.

KEY DRIVERS

HMA Market is poised to grow as innovation in automated manufacturing processes and increasing demand for lightweight materials from various industries. Due to the increasing adoption of automation for production lines such as automotive, furniture, textiles, etc., demand for fast, reliable, and efficient bonding adhesives is increasing. HMAs can fill this gap owing to their rapid curing time and simple application enabling manufacturers to achieve optimized production rates with no sacrifice in quality. Moreover, HMAs can be used with automated dispensing systems for unwanted accuracy and low material wastage which is very important for a high-volume production industry. The trend toward automation improves overall efficiency and cost-effectiveness leading to increased penetration of hot melt adhesives. Compared to conventional solvent-based adhesives, HMAs cut down material waste by 20% or more. More than 60% of production lines in sectors such as automotive, electronics, and furniture will be automated and supported by HMAs featuring fast, efficient bonding, through 2024. Also, the medical adhesives market is accounted by HMAs ranging between 25-30% that have contributed to the growth of demand for medical adhesives over the forecast period attributed to their application for non-invasive and skin-friendly applications such as wound care and medical devices.

A major factor contributing to this market growth is the rapid growth of the renewable energy and sustainable construction sectors. With the shift of the construction industry towards green and energy-efficient buildings, HMAs have been utilized for insulation products, flooring systems, and window assembly. These qualities, along with the ability to form durable weather-resistant bonds, make them valuable in modern construction solutions. The same goes for the renewable energy field, especially the solar energy field, which is experiencing significant amounts of growth. Hot melt adhesives are widely used in the assembly of solar panels, particularly for their performance of high bonding strength and resistance to environmental factors. In addition to the environmental benefits of such adhesives in manufacturing processes, the increasing growth of the eco-friendly consumer and government product market has propelled manufacturers to develop bio-based hot melt adhesives. The seamless recommendation of these developments in line with overall sustainability goals globally and environmental concerns is also expected to accelerate market growth. The world's renewable energy capacity passed the 3,400 GW mark in 2023, with more than a third of this comprising solar energy. Approximately 250 GW of solar panels were installed, which drove the growth of hot melt adhesives (for bonding and weather resistance). Global energy consumption and CO2 emissions are rising, but the construction sector has begun to transition toward energy-efficient buildings, employing HMAs in insulation, flooring, and window systems. In 2023, adhesives based on renewable sources were only responsible for 15% of the total HMA market, so they are considered bio-based HMAs.

RESTRAIN

Hold temperatures are one of the main problems faced due to the temperature resistance limitation of HMAs. They lose their adhesion upon exposure to high temperatures which makes them unsuitable for high thermal stability applications such as those found in aerospace or heavy industrial settings. However, this limited their adoption of heat-sensitive applications and also reduced their competitiveness versus other adhesive technologies such as epoxies or solvent-based adhesives. The second and another one of the crucial problems is a change in the price of raw materials. HMAs are mainly made from petroleum-based products, including ethylene-vinyl acetate (EVA) and polyolefins. Crude oil price variation causes production cost fluctuations, leading to price instability and profit margin pressure on producers. Moreover, the need for sustainability, tied together with the regulatory concerns regarding ecological implications of petroleum-based adhesives along with the rise in R&D investments for developing sustainable alternatives add to the cost and time spent towards the said approach.

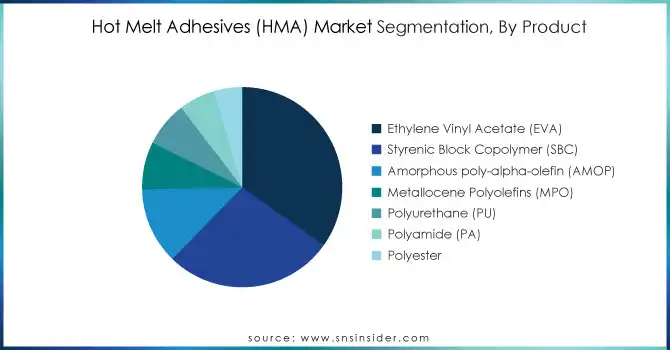

BY PRODUCT

In 2023, Ethylene Vinyl Acetate (EVA) accounted for the largest share of 34.8% of the Hot Melt Adhesives (HMA) Market share and is a preferred choice of hot melt adhesive owing to its versatility, price-performance relation, and broad-based application in key industries including packaging, footwear and automotive among others. Packaging applications consume a large share of the market and, therefore, EVA-based adhesives are preferred for use here. These features make it ideal for carton sealing, labeling, and flexible packaging due to its wide applicability in several different industries as a result of rapid growth in e-commerce and other retail sectors thanks to excellent flexibility, adhesion, and compatibility with an array of substrates. Additionally, EVA being less costly than other forms of adhesive attracts many price-sensitive sectors & industries to manufacture on a mass scale.

Amorphous Poly-Alpha-Olefin (AMOP) will grow at a significant CAGR during 2024-2032 owing to its advantages like superior thermal stability excellent adhesion, and resistance against moisture and chemicals. Moreover, these properties make it well-suited for rapid growth in specialized and high-performance applications such as automotive, electronics, and construction sectors. AMOP-based adhesives are also gaining traction as they generate low odor and very low VOC emissions, thus catering to rising environmental concerns and stringent regulatory standards. With the gradual shift of industries towards sustainable and high-performance adhesive solutions, AMOP will become the preferred adhesive, which in turn brings up the demand for AMOP during the period of forecast.

BY APPLICATION

In 2023, packaging accounted for 39.2% hot melt adhesives (HMA) market share. This is primarily attributed to the wide adoption of HMAs in packaging applications, which comprise carton sealing, labeling, and food packaging. With quick-drying characteristics, they excel in bond strength, durability, and packaging speed which makes HMAs suitable for high-speed packaging operations. The growth of HMAs in packaging is mainly due to the increasing demand for packaged goods, particularly in the food and beverage industry. The growing international e-commerce and retail industry fuels the demand for secure and effective packaging solutions thereby propelling the growth of the market for these adhesives.

The fastest growth in the HMA market during the period 2024 to 2032 is anticipated for pressure-sensitive products. The rising adoption of HMAs in adhesive tape, label, and sticker production processes where high-end convenience and ease of use are relevant to drive this growth. The most prevalent are modified with human mucosal antigen (HMA) because of their properties, which include the ability to bind at room temperature without requiring heat or moisture, resulting in more versatile and easier-to-apply products. Moreover, the increasing use of smart packaging, medical devices, and electronics that utilize Hot Melt Adhesives need accurate and long-lasting adhesion solutions, which in turn contributes to the strengthening demand for pressure-sensitive products.

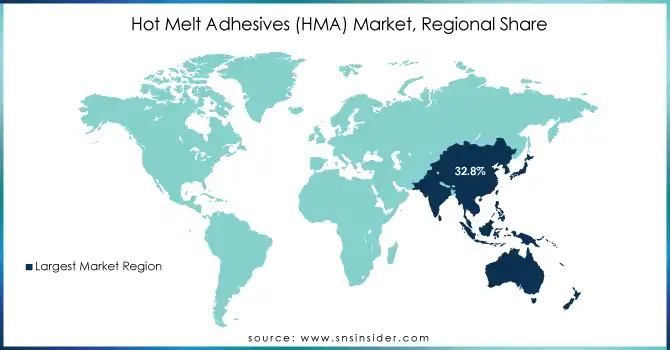

The market share in 2023 was led by Asia Pacific, accounting for 32.8% of the market share in 2023, and it is anticipated to register the highest CAGR from 2024 to 2032. The surge in regional growth can be attributed to the swift industrialization, trends in urbanization, and the growth of major industries like packaging, automotive, construction, and electronics across the region. The steady growth of end-use industries such as textile, automotive, and packaging along with the increasing number of new entrants from the above-mentioned region has become key factors driving the market all around the world, especially for emerging countries such as China, India, Japan, and South Korea. This is particularly evident in China, where demand for hot melt adhesives (HMAs) in packaging applications has surged due to the e-commerce boom driven by companies such as Alibaba and JD. Full-com truck driving scarcity and the requirement for secure and efficient packaging solutions. In addition, the demand for HMAs for bonding lightweight materials and fixtures and fasteners used in interior components has been driven by the mass production of cars in China.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players:

Some of the major players in the Hot Melt Adhesives (HMA) Market are:

Some of the Raw Material Suppliers for Hot Melt Adhesives (HMA) companies:

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 8.44 Billion |

| Market Size by 2032 | USD 12.10 Billion |

| CAGR | CAGR of 4.11% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Ethylene Vinyl Acetate (EVA), Styrenic Block Copolymer (SBC), Amorphous poly-alpha-olefin (AMOP), Metallocene Polyolefins (MPO), Polyurethane (PU), Polyamide (PA), Polyester) • By Application (Pressure sensitive products, Packaging, Disposables, Book Binding, Furniture, Footwear, Textile, Automobiles, Electronics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Henkel AG & Co. KGaA, H.B. Fuller Company, Dow Chemical Company, Exxon Mobil Corporation, Arkema Group, Jowat SE, LyondellBasell Industries, 3M Company, Bostik, Beardow Adams, Sika AG, Avery Dennison, Evans Adhesive Corporation, Ashland Global Holdings Inc., Sika AG, Toyobo Co., Ltd., Huntsman Corporation, Eastman Chemical Company, Sinopec Limited, Adtek Malaysia Sdn Bhd |

| Key Drivers | • Automation and Lightweight Materials Drive Hot Melt Adhesive Growth in Automotive Furniture and Medical Applications • Renewable Energy and Sustainable Construction Drive Hot Melt Adhesive Growth in Solar and Green Building Markets |

| Restraints | • Challenges in HMA Adoption Heat Sensitivity Raw Material Price Fluctuations and Sustainability Concerns Impact Growth |

Ans: Asia Pacific dominated the Hot Melt Adhesives (HMA) Market in 2023.

Ans: The Ethylene Vinyl Acetate (EVA) segment dominated the Hot Melt Adhesives (HMA) Market in 2023.

Ans: The major growth factor of the Hot Melt Adhesives (HMA) market is the increasing demand for lightweight, high-performance materials in industries like automotive, aerospace, and medical.

Ans: Hot Melt Adhesives (HMA) Market size was USD 8.44 Billion in 2023 and is expected to Reach USD 12.10 Billion by 2032.

Ans: The Hot Melt Adhesives (HMA) Market is expected to grow at a CAGR of 4.11% during 2024-2032.

TABLE OF CONTENTS:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Hot Melt Adhesives (HMA) Export and Import Analysis (2023)

5.2 Hot Melt Adhesives (HMA) Environmental and Sustainability Metrics (2023)

5.3 Hot Melt Adhesives (HMA) Regulatory Metrics

5.4 Hot Melt Adhesives (HMA) Innovation and R&D Investment

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Hot Melt Adhesives (HMA) Market Segmentation, By Product

7.1 Chapter Overview

7.2 Ethylene Vinyl Acetate (EVA)

7.2.1 Ethylene Vinyl Acetate (EVA) Market Trends Analysis (2020-2032)

7.2.2 Ethylene Vinyl Acetate (EVA) Market Size Estimates and Forecasts to 2032 (USD BILLION)

7.3 Styrenic Block Copolymer (SBC)

7.3.1 Styrenic Block Copolymer (SBC) Market Trends Analysis (2020-2032)

7.3.2 Styrenic Block Copolymer (SBC) Market Size Estimates and Forecasts to 2032 (USD BILLION)

7.4 Amorphous poly-alpha-olefin (AMOP)

7.4.1 Amorphous poly-alpha-olefin (AMOP) Market Trends Analysis (2020-2032)

7.4.2 Amorphous poly-alpha-olefin (AMOP) Market Size Estimates and Forecasts to 2032 (USD BILLION)

7.5 Metallocene Polyolefins (MPO)

7.5.1 Metallocene Polyolefins (MPO) Market Trends Analysis (2020-2032)

7.5.2 Metallocene Polyolefins (MPO) Market Size Estimates and Forecasts to 2032 (USD BILLION)

7.6 Polyurethane (PU)

7.6.1 Polyurethane (PU) Market Trends Analysis (2020-2032)

7.6.2 Polyurethane (PU) Market Size Estimates and Forecasts to 2032 (USD BILLION)

7.7 Polyamide (PA)

7.7.1 Polyamide (PA) Market Trends Analysis (2020-2032)

7.7.2 Polyamide (PA) Market Size Estimates and Forecasts to 2032 (USD BILLION)

7.8 Polyester

7.8.1 Polyester Market Trends Analysis (2020-2032)

7.8.2 Polyester Market Size Estimates and Forecasts to 2032 (USD BILLION)

8. Hot Melt Adhesives (HMA) Market Segmentation, By Application

8.1 Chapter Overview

8.2 Pressure-sensitive products

8.2.1 Pressure sensitive Products Market Trends Analysis (2020-2032)

8.2.2 Pressure sensitive Products Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.3 Packaging

8.3.1 Packaging Market Trends Analysis (2020-2032)

8.3.2 Packaging Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.4 Disposables

8.4.1 Disposables Market Trends Analysis (2020-2032)

8.4.2 Disposables Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.5 Book Binding

8.5.1 Book Binding Market Trends Analysis (2020-2032)

8.5.2 Book Binding Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.6 Furniture

8.6.1 Furniture Market Trends Analysis (2020-2032)

8.6.2 Furniture Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.7 Footwear

8.7.1 Footwear Market Trends Analysis (2020-2032)

8.7.2 Footwear Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.8 Textile

8.8.1 Textile Market Trends Analysis (2020-2032)

8.8.2 Textile Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.9 Automobiles

8.9.1 Automobiles Market Trends Analysis (2020-2032)

8.9.2 Automobiles Market Size Estimates and Forecasts to 2032 (USD BILLION)

8.10 Electronics

8.10.1 Electronics Market Trends Analysis (2020-2032)

8.10.2 Electronics Market Size Estimates and Forecasts to 2032 (USD BILLION)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, by Country (2020-2032) (USD BILLION)

9.2.3 North America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.2.4 North America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.2.5 USA

9.2.5.1 USA Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.2.5.2 USA Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.2.6 Canada

9.2.6.1 Canada Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.2.6.2 Canada Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.2.7 Mexico

9.2.7.1 Mexico Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.2.7.2 Mexico Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, by Country (2020-2032) (USD BILLION)

9.3.1.3 Eastern Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.1.4 Eastern Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.1.5 Poland

9.3.1.5.1 Poland Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.1.5.2 Poland Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.1.6 Romania

9.3.1.6.1 Romania Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.1.6.2 Romania Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.1.7.2 Hungary Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.1.8 turkey

9.3.1.8.1 Turkey Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.1.8.2 Turkey Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.1.9.2 Rest of Eastern Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, by Country (2020-2032) (USD BILLION)

9.3.2.3 Western Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.4 Western Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.5 Germany

9.3.2.5.1 Germany Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.5.2 Germany Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.6 France

9.3.2.6.1 France Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.6.2 France Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.7 UK

9.3.2.7.1 UK Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.7.2 UK Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.8 Italy

9.3.2.8.1 Italy Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.8.2 Italy Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.9 Spain

9.3.2.9.1 Spain Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.9.2 Spain Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.10.2 Netherlands Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.11.2 Switzerland Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.12 Austria

9.3.2.12.1 Austria Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.12.2 Austria Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.3.2.13.2 Rest of Western Europe Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific Hot Melt Adhesives (HMA) Market Estimates and Forecasts, by Country (2020-2032) (USD BILLION)

9.4.3 Asia Pacific Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.4 Asia Pacific Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.5 China

9.4.5.1 China Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.5.2 China Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.6 India

9.4.5.1 India Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.5.2 India Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.5 japan

9.4.5.1 Japan Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.5.2 Japan Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.6 South Korea

9.4.6.1 South Korea Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.6.2 South Korea Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.7 Vietnam

9.4.7.1 Vietnam Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.2.7.2 Vietnam Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.8 Singapore

9.4.8.1 Singapore Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.8.2 Singapore Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.9 Australia

9.4.9.1 Australia Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.9.2 Australia Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.4.10.2 Rest of Asia Pacific Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Hot Melt Adhesives (HMA) Market Estimates and Forecasts, by Country (2020-2032) (USD BILLION)

9.5.1.3 Middle East Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.1.4 Middle East Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.1.5 UAE

9.5.1.5.1 UAE Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.1.5.2 UAE Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.1.6.2 Egypt Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.1.7.2 Saudi Arabia Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.1.8.2 Qatar Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.1.9.2 Rest of Middle East Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Hot Melt Adhesives (HMA) Market Estimates and Forecasts, by Country (2020-2032) (USD BILLION)

9.5.2.3 Africa Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.2.4 Africa Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.2.5.2 South Africa Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.2.6.2 Nigeria Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.5.2.7.2 Rest of Africa Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, by Country (2020-2032) (USD BILLION)

9.6.3 Latin America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.6.4 Latin America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.6.5 brazil

9.6.5.1 Brazil Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.6.5.2 Brazil Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.6.6 Argentina

9.6.6.1 Argentina Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.6.6.2 Argentina Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.6.7 Colombia

9.6.7.1 Colombia Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.6.7.2 Colombia Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Product (2020-2032) (USD BILLION)

9.6.8.2 Rest of Latin America Hot Melt Adhesives (HMA) Market Estimates and Forecasts, By Application (2020-2032) (USD BILLION)

10. Company Profiles

10.1 Henkel AG & Co. KGaA

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

110.1.4 SWOT Analysis

10.2 H.B. Fuller Company

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Dow Chemical Company

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Exxon Mobil Corporation

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Arkema Group

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Jowat SE.

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 LyondellBasell Industries

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 3M Company

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Bostik

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Beardow Adams

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

KEY SEGMENTS:

By Product

Ethylene Vinyl Acetate (EVA)

Styrenic Block Copolymer (SBC)

Amorphous poly-alpha-olefin (AMOP)

Metallocene Polyolefins (MPO)

Polyurethane (PU)

Polyamide (PA)

Polyester

By Application

Pressure sensitive products

Packaging

Disposables

Book Binding

Furniture

Footwear

Textile

Automobiles

Electronics

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

AVAILABLE CUSTOMIZATION:

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Isostatic Pressing Market Size was valued at USD 7.52 Billion in 2023 and is expected to grow at a CAGR of 6.86% to reach USD 13.66 Billion by 2032.

The copper foil market size was valued at USD 7.28 billion in 2024 and is expected to reach USD 14.41 billion by 2032 expanding at a CAGR of 7.88% over the forecast period.

The Chitosan Market Size was valued at USD 12.7 billion in 2023 and is expected to reach USD 71.5 billion by 2032 and grow at a CAGR of 21.2% by 2024-2032.

The Sodium Nitrate Market size was USD 136.22 Million in 2023 and is expected to reach USD 231.47 Million by 2032, growing at a CAGR of 6.07% from 2024-2032.

The Mussel Oil Market Size was valued at USD 41.7 billion in 2023 and is expected to reach USD 66.1 billion by 2032 and grow at a CAGR of 5.3% by 2024-2032.

The Cold Chain Monitoring Market Size was USD 5.7 Billion in 2023 and is expected to reach $22.1 Billion by 2032 and grow at a CAGR of 16.2% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd