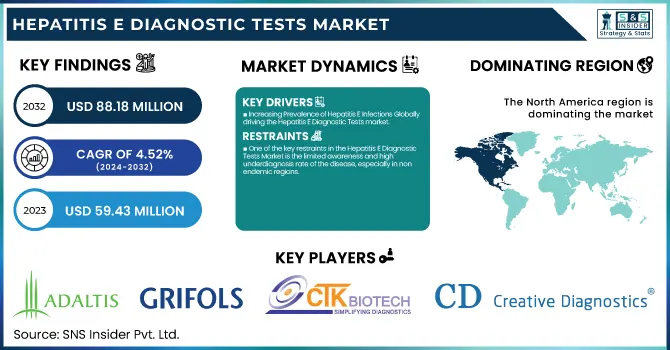

The Hepatitis E Diagnostic Tests Market was valued at USD 59.43 million in 2023 and is expected to reach USD 88.18 million by 2032, growing at a CAGR of 4.52% from 2024-2032.

To Get more information on Hepatitis E Diagnostic Tests Market - Request Free Sample Report

The Hepatitis E Diagnostic Tests Market report offers insights by concentrating on regional disease burden analysis, outlining incidence and prevalence trends among major markets in 2023. It assesses diagnostic test adoption rates and regional preferences for ELISA, PCR, and rapid tests. The report further provides a complete review of testing volumes and future demand forecasts to analyze market growth dynamics. One of the distinguishing factors is the detailed examination of healthcare expenditure on HEV testing, dividing investments into government, commercial, private, and out-of-pocket spending. These data guarantee a data-driven strategy in understanding market dynamics, adoption trends, and financial allocation in HEV diagnostics.

Drivers

Increasing Prevalence of Hepatitis E Infections Globally driving the Hepatitis E Diagnostic Tests market.

The increasing number of cases of hepatitis E virus (HEV) infections is one of the key growth drivers for the Hepatitis E Diagnostic Tests Market. The World Health Organization (WHO) reports that hepatitis E is responsible for an estimated 20 million cases of infection per year, with an estimated 70,000 deaths and 3,000 stillbirths. The infection is highly endemic in countries with low levels of sanitation and unsafe water supplies, e.g., South Asia and Africa. The increasing HEV burden has, in turn, resulted in a higher demand for early and precise diagnostic solutions. The approval of recent HEV diagnostic assays, including Roche's Elecsys Anti-HEV IgM and IgG immunoassays, in November 2023 has also consolidated the market by enhancing testing potentials. Expansion of diagnostic laboratory networks and government schemes for viral hepatitis screening also drive market growth.

Advancements in Diagnostic Technologies and Rapid Testing Solutions accelerating the market growth.

Advances in technology in hepatitis E diagnostics, especially molecular and immunoassay-based tests, are driving market growth. PCR-based tests and ELISA kits are highly sensitive and specific and are the first choice for precise HEV detection. Rapid diagnostic tests (RDTs) are also gaining popularity because they can deliver rapid and affordable results, particularly in resource-poor environments. DiaSorin launched the LIAISON Murex Anti-HEV IgG and IgM tests in December 2023, improving laboratory test efficiency. In addition, AI-based diagnostic systems and automation of diagnostic platforms simplify HEV testing, shorten turnaround times, and enhance accuracy. The increased demand for point-of-care (POC) tests in hospitals and blood banks and rising investment in diagnostic research fuel the growth in hepatitis E tests globally.

Restraint

One of the key restraints in the Hepatitis E Diagnostic Tests Market is the limited awareness and high underdiagnosis rate of the disease, especially in non-endemic regions.

Hepatitis E is frequently misdiagnosed or underdiagnosed because it is confused with other viral hepatitis infections and influenza-like illnesses. The World Health Organization (WHO) states that hepatitis E is still underreported in most countries because healthcare professionals may not consistently test for HEV, resulting in delayed or missed diagnoses. Furthermore, the absence of uniform screening programs and the limited availability of sophisticated diagnostic equipment in low-income areas further inhibit market growth. Although there has been a recent development, such as Roche's Elecsys Anti-HEV assays released in 2023, the reluctance of HEV testing to take off is still causing challenges. Improving awareness and incorporating HEV testing into the normal diagnosis process is imperative in breaking this limitation.

Opportunities

A significant market opportunity for Hepatitis E diagnostic tests lies in the increasing focus on HEV screening in blood banks and organ transplantation.

A huge market potential for Hepatitis E tests exists in the growing interest for HEV screening among blood banks and organ transplants. Research suggests that HEV is spread via contaminated blood transfusions and organ transplantation, creating serious health hazards for immunocompromised recipients. Regulatory agencies such as the European Medicines Agency (EMA) have highlighted the importance of routine HEV screening in blood donations, which has encouraged diagnostic firms to create more sensitive and affordable HEV assays. The launch of high-sensitivity nucleic acid testing (NAT)--based HEV assays by firms such as Grifols and Roche has further consolidated this segment. As the regulations around blood safety increase and awareness around the world for transfusion-transmitted diseases increases, diagnostic players stand to extend their product portfolio, which can boost the uptake of Hepatitis E diagnostic tests among clinical and blood screening laboratories.

Challenges

A key challenge in the Hepatitis E Diagnostic Tests Market is the limited availability of advanced diagnostic infrastructure in developing and underdeveloped regions.

One of the challenges that lie ahead for the Hepatitis E Diagnostic Tests Market is that few sophisticated diagnostic infrastructure facilities exist in developing and underdeveloped economies. HEV diagnostics, especially molecular tests such as polymerase chain reaction (PCR) and nucleic acid testing (NAT), demand sophisticated laboratory facilities, qualified staff, and sound cold chain logistics, all of which are not usually available in resource-poor environments. Those countries that bear a heavy burden of hepatitis E, notably South Asia and sub-Saharan Africa, are afflicted with weak health infrastructure, reducing the affordability and accessibility of correct HEV diagnosis. Although firms such as Siemens Healthineers and Abbott have launched rapid and automated diagnostic solutions, penetration is low in areas with limited resources. It will take joint efforts from governments, international health organizations, and diagnostic firms to enhance access to credible HEV testing solutions.

By Test Type

The ELISA HEV IgM test segment dominated the Hepatitis E Diagnostic Tests Market with around 47.12% market share in 2023 with its high sensitivity, specificity, and prevalence in clinical diagnostics. This test is the reference standard for recent HEV infection diagnosis as IgM antibodies are produced early in infection, thus a valuable tool for early diagnosis. Healthcare professionals prefer ELISA-based tests due to their precise and reliable results, minimizing the possibility of false negatives or delayed treatment. Moreover, numerous hospitals, diagnostic laboratories, and blood banks use ELISA HEV IgM tests as a part of routine screening programs, further increasing their market share. The growing worldwide burden of hepatitis E, especially among immunocompromised individuals and pregnant women, has also driven demand for ELISA HEV IgM tests, reinforcing their market dominance. In addition, regulatory clearances and ELISA technology advancements have enhanced test efficiency and availability, making them widely adopted. The increase in government efforts to contain hepatitis epidemics has also contributed heavily to the growing use of these tests in various healthcare facilities.

By Sample Type

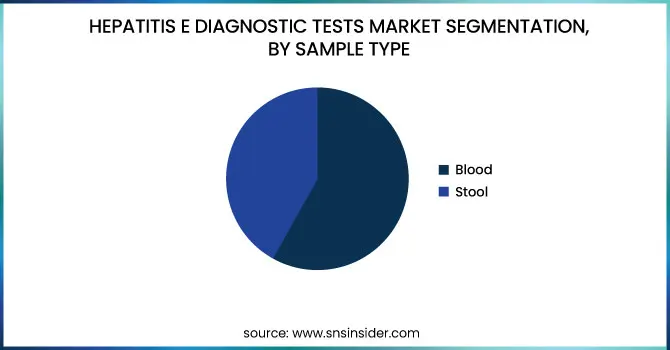

The Blood segment dominated the market with around 75.26% market share in 2023 because of its high reliability, accuracy, and extensive application in the detection of HEV infections. Blood samples are the preferred option for HEV diagnosis because they enable the detection of HEV RNA, IgM, and IgG antibodies, which give complete information about both acute and past infections. ELISA and PCR-based assays, being the main diagnostic methods for hepatitis E, are also heavily dependent on blood samples because of their capability to provide accurate and early results. Blood tests are also heavily incorporated into hospital routine screenings, diagnostic labs, and blood banks, further establishing their dominance. The increasing incidence of hepatitis E, particularly in immunocompromised patients and pregnant women, has increased the demand for blood-based testing. In addition, technological advancements in automated blood diagnostic platforms and increased use of point-of-care testing solutions have increased accessibility, further supporting the dominance of the blood segment as the top sample type in the market.

By End-use

The Hospitals segment dominated the Hepatitis E Diagnostic Tests Market with around 52.14% market share in 2023 on account of increased patient inflow, access to state-of-the-art diagnostic equipment, and amalgamation of expansive testing facilities. Hospitals are general healthcare centers that cater to suspected cases of hepatitis E infections where the initial diagnosis and treatment of the infection occurs, making it the most desired location for HEV testing employing ELISA, PCR, and rapid tests. Moreover, hospitals are equipped with high-tech laboratory centers, professional healthcare personnel, and computerized diagnostic machines to provide quick and precise results.

In addition, increased cases of hepatitis E infections, especially among immunocompromised individuals and pregnant women, have influenced early diagnosis and hospitalization for complicated cases. The rising government support and funding for infectious disease management, combined with the collaborations of hospitals with research institutions in conducting HEV surveillance, further strengthen their position as market leaders. Additionally, large-scale seroprevalence studies and epidemiological studies are mostly performed by hospital laboratories, strengthening their position as leaders in hepatitis E diagnosis.

North America dominated the Hepatitis E Diagnostic Tests Market with around 40% market share in 2023, because of its established healthcare infrastructure, sophisticated diagnostic technologies, and robust regulatory environment. The region is highly aware of infectious diseases, and thus HEV diagnostic tests are used extensively, especially in blood screening and organ transplantation facilities. The dominance of prominent market players like Abbott Laboratories, Roche Diagnostics, and Siemens Healthineers further reinforces North America's dominance, as these players keep investing in innovative HEV testing solutions. Furthermore, the stringent regulations of organizations like the FDA and CDC require regular screening for infectious diseases, which supports market growth. The growing prevalence of hepatitis E among immunocompromised individuals, along with research and development in molecular diagnostics, further establishes North America's leadership in the market.

Asia Pacific is the fastest-growing region with a 5.60% CAGR throughout the forecast period, mainly because of the high prevalence of HEV infections, growing healthcare expenditure, and heightened awareness of viral hepatitis. India and China frequently experience HEV outbreaks, most notably in the regions with less sanitation and cleaner water access. With governments and international health institutions intensifying action against HEV, demand for accurate diagnostic technology is increasing exponentially. The increased healthcare infrastructure coverage and access to affordable rapid diagnostic tests (RDTs) are also fast-tracking market expansion. The growing use of polymerase chain reaction (PCR)-based HEV testing, aided by public health authority initiatives, also increases market growth. With diagnostic firms increasing their presence in emerging markets, Asia Pacific will see significant growth in HEV diagnostics.

Get Customized Report as per Your Business Requirement - Enquiry Now

ADALTIS (EIAgen HEV IgM ELISA Kit, EIAgen HEV IgG ELISA Kit)

Grifols (Procleix HEV Assay, Procleix Panther System)

CTK Biotech (HEV IgM Rapid Test CE, HEV IgG Rapid Test)

Creative Diagnostics (HEV-Ag ELISA Kit, HEV IgM Antibody ELISA Kit)

Roche Diagnostics (Elecsys HEV IgM Assay, Elecsys HEV IgG Assay)

DiaSorin (LIAISON Murex Anti-HEV IgG Assay, LIAISON Murex Anti-HEV IgM Assay)

Fortress Diagnostics (HEV IgM ELISA Kit, HEV IgG ELISA Kit)

Launch Diagnostics (Diapro HEV IgM ELISA, amplitude HEV 2.0 Quant)

AdvaCare Pharma (AccuQuik HEV IgM Rapid Test, AccuQuik HEV IgG Rapid Test)

Beijing Zhongjian Antai Diagnosis Technology Co., Ltd. (Hepatitis E Detection Kit, HEV IgM ELISA Kit)

Bio-Rad Laboratories (HEV IgM ELISA Kit, HEV IgG ELISA Kit)

Abbott Laboratories (ARCHITECT HEV IgM Assay, ARCHITECT HEV IgG Assay)

Siemens Healthineers (Enzygnost HEV IgM Assay, Enzygnost HEV IgG Assay)

Thermo Fisher Scientific (HEV IgM ELISA Kit, HEV IgG ELISA Kit)

PerkinElmer (HEV IgM Rapid Test, HEV IgG Rapid Test)

BioCheck, Inc. (HEV IgM ELISA Test Kit, HEV IgG ELISA Test Kit)

MP Biomedicals (HEV IgM ELISA Kit, HEV IgG ELISA Kit)

Euroimmun AG (Anti-HEV IgM ELISA, Anti-HEV IgG ELISA)

DRG International, Inc. (HEV IgM ELISA Kit, HEV IgG ELISA Kit)

Wantai BioPharm (HEV IgM ELISA Kit, HEV IgG ELISA Kit)

Suppliers (These suppliers provide critical raw materials, reagents, assay components, and laboratory instruments essential for Hepatitis E diagnostic tests.)

Merck KGaA

Agilent Technologies, Inc.

Qiagen N.V.

Thermo Fisher Scientific Inc.

PerkinElmer Inc.

Bio-Rad Laboratories, Inc.

Luminex Corporation (DiaSorin Group)

Tecan Group Ltd.

R&D Systems (Bio-Techne Corporation)

GE Healthcare

November 16, 2023 – Roche launched its Elecsys Anti-HEV IgM and Elecsys Anti-HEV IgG immunoassays to detect hepatitis E virus (HEV) infection in CE-marking countries. These assays allow clinicians to accurately diagnose HEV infections, facilitate the identification of symptoms, selection of suitable treatments, and monitoring of disease progression. Early detection with these assays may prevent severe complications and enable early antiviral treatment, which in turn may enhance patient outcomes.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 59.43 million |

| Market Size by 2032 | US$ 88.18 million |

| CAGR | CAGR of 4.52% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Test Type (ELISA HEV IgM Test, ELISA HEV IgG Test, Rapid Diagnostics Test, Polymerase Chain Reaction (PCR)) • By Sample Type (Blood, Stool) • By End-use (Hospitals, Diagnostic Laboratories, Blood Banks, Other End-users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ADALTIS, Grifols, CTK Biotech, Creative Diagnostics, Roche Diagnostics, DiaSorin, Fortress Diagnostics, Launch Diagnostics, AdvaCare Pharma, Beijing Zhongjian Antai Diagnosis Technology Co., Ltd., Bio-Rad Laboratories, Abbott Laboratories, Siemens Healthineers, Thermo Fisher Scientific, PerkinElmer, BioCheck, Inc., MP Biomedicals, Euroimmun AG, DRG International, Inc., Wantai BioPharm, and other players. |

Ans: The Hepatitis E Diagnostic Tests Market is expected to grow at a CAGR of 4.52% during 2024-2032.

Ans: The Hepatitis E Diagnostic Tests Market was USD 59.43 million in 2023 and is expected to Reach USD 88.18 million by 2032.

Ans: A significant market opportunity for Hepatitis E diagnostic tests lies in the increasing focus on HEV screening in blood banks and organ transplantation.

Ans: The “ELISA HEV IgM test” segment dominated the Hepatitis E Diagnostic Tests Market.

Ans: North America dominated the Hepatitis E Diagnostic Tests Market in 2023

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023), by Region

5.2 Diagnostic Test Adoption and Utilization Trends (2023), by Region

5.3 Testing Volume and Demand for HEV Diagnostic Kits, by Region (2020-2032)

5.4 Healthcare Spending on HEV Testing, by Region (Government, Commercial, Private, Out-of-Pocket), 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Hepatitis E Diagnostic Tests Market Segmentation, by Test Type

7.1 Chapter Overview

7.2 ELISA HEV IgM test

7.2.1 ELISA HEV IgM test Market Trends Analysis (2020-2032)

7.2.2 ELISA HEV IgM test Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 ELISA HEV IgG test

7.3.1 ELISA HEV IgG test Market Trends Analysis (2020-2032)

7.3.2 ELISA HEV IgG test Market Size Estimates and Forecasts to 2032 (USD Million)

7.4 Rapid diagnostics test

7.4.1 Rapid Diagnostics Test Market Trends Analysis (2020-2032)

7.4.2 Rapid Diagnostics Test Market Size Estimates and Forecasts to 2032 (USD Million)

7.5 Polymerase chain reaction (PCR)

7.5.1 Polymerase Chain Reaction (PCR) Market Trends Analysis (2020-2032)

7.5.2 Polymerase Chain Reaction (PCR) Market Size Estimates and Forecasts to 2032 (USD Million)

8. Hepatitis E Diagnostic Tests Market Segmentation, by Sample Type

8.1 Chapter Overview

8.2 Blood

8.2.1 Blood Market Trends Analysis (2020-2032)

8.2.2 Blood Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Stool

8.3.1 Stool Market Trends Analysis (2020-2032)

8.3.2 Stool Market Size Estimates and Forecasts to 2032 (USD Million)

9. Hepatitis E Diagnostic Tests Market Segmentation, by End User

9.1 Chapter Overview

9.2 Hospitals

9.2.1 Hospitals Market Trends Analysis (2020-2032)

9.2.2 Hospitals Market Size Estimates and Forecasts to 2032 (USD Million)

9.3 Diagnostic laboratories

9.3.1 Diagnostic Laboratories Market Trends Analysis (2020-2032)

9.3.2 Diagnostic Laboratories Market Size Estimates and Forecasts to 2032 (USD Million)

9.4 Blood banks

9.4.1 Blood Banks Market Trends Analysis (2020-2032)

9.4.2 Blood Banks Market Size Estimates and Forecasts to 2032 (USD Million)

9.5 Other end-users

9.5.1 Other end-users Market Trends Analysis (2020-2032)

9.5.2 Other end-users Market Size Estimates and Forecasts to 2032 (USD Million)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.2.3 North America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.2.4 North America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.2.5 North America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.2.6 USA

10.2.6.1 USA Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.2.6.2 USA Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.2.6.3 USA Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.2.7 Canada

10.2.7.1 Canada Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.2.7.2 Canada Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.2.7.3 Canada Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.2.8 Mexico

10.2.8.1 Mexico Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.2.8.2 Mexico Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.2.8.3 Mexico Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.1.3 Eastern Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.1.4 Eastern Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.1.5 Eastern Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.6 Poland

10.3.1.6.1 Poland Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.1.6.2 Poland Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.1.6.3 Poland Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.7 Romania

10.3.1.7.1 Romania Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.1.7.2 Romania Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.1.7.3 Romania Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.1.8.2 Hungary Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.1.8.3 Hungary Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.9 turkey

10.3.1.9.1 Turkey Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.1.9.2 Turkey Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.1.9.3 Turkey Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.1.10.2 Rest of Eastern Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.1.10.3 Rest of Eastern Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.2.3 Western Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.4 Western Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.5 Western Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.6 Germany

10.3.2.6.1 Germany Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.6.2 Germany Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.6.3 Germany Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.7 France

10.3.2.7.1 France Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.7.2 France Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.7.3 France Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.8 UK

10.3.2.8.1 UK Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.8.2 UK Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.8.3 UK Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.9 Italy

10.3.2.9.1 Italy Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.9.2 Italy Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.9.3 Italy Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.10 Spain

10.3.2.10.1 Spain Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.10.2 Spain Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.10.3 Spain Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.11.2 Netherlands Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.11.3 Netherlands Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.12.2 Switzerland Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.12.3 Switzerland Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.13 Austria

10.3.2.13.1 Austria Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.13.2 Austria Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.13.3 Austria Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.3.2.14.2 Rest of Western Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.3.2.14.3 Rest of Western Europe Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.4.3 Asia Pacific Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.4 Asia Pacific Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.5 Asia Pacific Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.6 China

10.4.6.1 China Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.6.2 China Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.6.3 China Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.7 India

10.4.7.1 India Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.7.2 India Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.7.3 India Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.8 japan

10.4.8.1 Japan Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.8.2 Japan Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.8.3 Japan Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.9 South Korea

10.4.9.1 South Korea Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.9.2 South Korea Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.9.3 South Korea Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.10 Vietnam

10.4.10.1 Vietnam Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.10.2 Vietnam Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.10.3 Vietnam Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.11 Singapore

10.4.11.1 Singapore Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.11.2 Singapore Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.11.3 Singapore Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.12 Australia

10.4.12.1 Australia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.12.2 Australia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.12.3 Australia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.4.13.2 Rest of Asia Pacific Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.4.13.3 Rest of Asia Pacific Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.1.3 Middle East Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.1.4 Middle East Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.1.5 Middle East Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.6 UAE

10.5.1.6.1 UAE Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.1.6.2 UAE Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.1.6.3 UAE Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.1.7.2 Egypt Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.1.7.3 Egypt Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.1.8.2 Saudi Arabia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.1.8.3 Saudi Arabia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.1.9.2 Qatar Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.1.9.3 Qatar Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.1.10.2 Rest of Middle East Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.1.10.3 Rest of Middle East Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.2.3 Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.2.4 Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.2.5 Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.2.6.2 South Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.2.6.3 South Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.2.7.2 Nigeria Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.2.7.3 Nigeria Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.5.2.8.2 Rest of Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.5.2.8.3 Rest of Africa Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.6.3 Latin America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.6.4 Latin America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.6.5 Latin America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.6 brazil

10.6.6.1 Brazil Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.6.6.2 Brazil Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.6.6.3 Brazil Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.7 Argentina

10.6.7.1 Argentina Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.6.7.2 Argentina Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.6.7.3 Argentina Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.8 Colombia

10.6.8.1 Colombia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.6.8.2 Colombia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.6.8.3 Colombia Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Test Type (2020-2032) (USD Million)

10.6.9.2 Rest of Latin America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by Sample Type (2020-2032) (USD Million)

10.6.9.3 Rest of Latin America Hepatitis E Diagnostic Tests Market Estimates and Forecasts, by End User (2020-2032) (USD Million)

11. Company Profiles

11.1 ADULTS

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 Grifols

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 CTK Biotech

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Creative Diagnostics

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Roche Diagnostics

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 DiaSorin

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Fortress Diagnostics

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Launch Diagnostics

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 AdvaCare Pharma

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Beijing Zhongjian Antai Diagnosis Technology Co., Ltd.

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Test Type

ELISA HEV IgM test

ELISA HEV IgG test

Rapid diagnostics test

Polymerase chain reaction (PCR)

By Sample Type

Blood

Stool

By End-use

Hospitals

Diagnostic laboratories

Blood banks

Other end-users

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Nuclear Magnetic Resonance Spectroscopy Market size was USD 1.31 billion in 2023, expected to reach USD 2.08 billion by 2032 and grow at a CAGR of 5.26%.

The Tissue Engineering Market was valued at USD 16.8 Billion in 2023 and will reach USD 56.2 Billion by 2032, with a CAGR of 14.3% from 2024-2032.

The Biopharmaceutical Excipients Market Size was valued at USD 2.57 billion in 2023 and is expected to reach USD 4.04 billion by 2032 and grow at a CAGR of 5.18% over the forecast period 2024-2032.

The Urgent Care Apps Market Size was valued at USD 2230.17 million in 2023 and is expected to reach USD 31983.94 million by 2031 and grow at a CAGR of 39.5% over the forecast period 2024-2031.

The Hospital Information System Market Size was valued at USD 56.84 billion in 2023 and is projected to reach USD 100.66 billion by 2032, with a CAGR of 6.58% over the forecast period 2024-2032.

The Antimicrobial Susceptibility Testing Market Size was valued at USD 3.87 Billion in 2023 and is expected to reach USD 6.04 Billion by 2032, growing at a CAGR of 5.1% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd