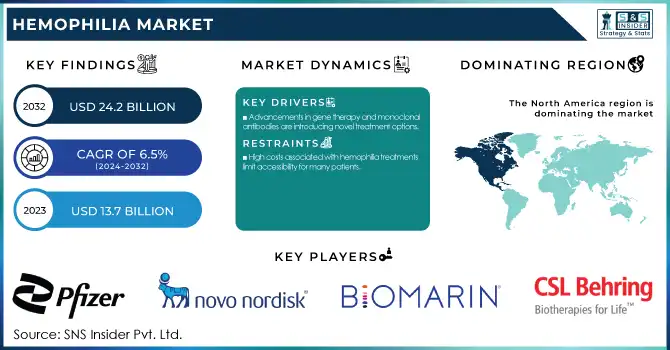

The Hemophilia Market Size was valued at USD 13.7 Billion in 2023 and is expected to reach USD 24.2 Billion by 2032, growing at a CAGR of 6.5% over the forecast period 2024-2032.

Get More Information on Hemophilia Market - Request Sample Report

The Hemophilia Market report offers key statistics and emerging trends that shaping the industry. It addresses incidence and prevalence figures, identifying diagnosed and undiagnosed patients throughout the world. The report reviews treatment adoption patterns with emphasis on the prescription behaviour of clotting factor therapies, gene therapy, and novel non-factor therapies. It also reviews drug volume forecasts, monitoring manufacturing and demand changes. Additionally, the report discusses therapeutic innovations, such as gene therapy breakthroughs, and evaluates the regulatory and reimbursement environment by region, providing insights on pricing, accessibility, and market dynamics. The hemophilia market is facing immense growth fueled by growing awareness, enhanced diagnostic methods, and advancements in treatment modalities.

Drivers

Advancements in gene therapy and monoclonal antibodies are introducing novel treatment options.

Advancements in gene therapy and monoclonal antibodies are significantly transforming hemophilia treatment, offering promising alternatives to traditional therapies. Recent developments have demonstrated substantial efficacy in reducing bleeding episodes and improving patient outcomes. Pfizer's hemophilia A gene therapy had an impressive annual bleeding rate in a key Phase III study. In an analysis of 75 patients, 84% sustained Factor VIII levels greater than 5% at 15 months after infusion, demonstrating durable efficacy.

In the same vein, CSL's HEMGENIX, Europe's first approved hemophilia B gene therapy showed a 64% reduction in annual bleeding rates. Cure of hemophilia following treatment enabled 96% of patients to stop routine Factor IX prophylaxis, underscoring the potential of this therapy to reduce treatment frequency. A landmark study from the Centre for Stem Cell Research at Christian Medical College, Vellore, India, treated five severe hemophilia A patients with gene transfer, and under a total follow-up of 81 months, there were zero bleeding events in any subject, demonstrating the efficacy of the therapy. Novo Nordisk's Alhemo, approved by the U.S. FDA in December 2024, provides another treatment alternative to patients with hemophilia aged 12 years and older with inhibitors to standard factor replacement therapies. Administered via subcutaneous injection, Alhemo is expected to be available by February 2025.

Restraints:

High costs associated with hemophilia treatments limit accessibility for many patients.

The high cost of hemophilia treatments significantly limits patient accessibility. For example, Roche's Hemlibra, a treatment for hemophilia, now costs about USD 600,000 annually after an 8% increase. Novel therapies will strain payers More recently, CSL Behring's gene therapy for hemophilia B, Hemgenix, has been just been listed at USD 3.5 million per dose, thus becoming the world's most expensive drug so far. That characteristic, along with considerable research, development, manufacturing, and regulatory compliance costs, is cited for these high costs of biologic drug development. As a result, these high-priced life-saving therapies are unattainable for significant proportions of patients, particularly in areas where the healthcare infrastructures are less developed. Even in developed countries, incomplete insurance coverage and variable access to financial assistance schemes increase the financial burden for patients. Not only does this economic barrier limit access to essential therapies but also causes disparities in health among hemophilia patients around the world.

Opportunities:

Emerging gene therapy approaches offer potential long-term solutions for hemophilia management.

Gene therapy is emerging as a transformative opportunity in hemophilia treatment, offering the potential for long-term solutions. The recent advances that have shown to markedly reduce bleeding and infrequent requirement for repeat infusions. Pfizer's gene therapy for hemophilia A significantly lessened annual bleeding compared to standard Factor VIII replacement therapy in a pivotal Phase III clinical trial. Importantly, 84% of participants had Factor VIII levels above 5% at 15 months post-infusion, indicating sustained therapeutic benefits. The same has been found for hemophilia B, where bleeds were reduced by 71% with a single infusion of the gene therapy fidanacogene elaparvovec (Beqvez, Pfizer) compared to conventional Factor IX prophylaxis. It achieved an annualized infusions reduction of 92.3% and also reduced Factor IX consumption by 92.4%, which suggests that the therapy has the potential to be life changing for patients. In India, a groundbreaking study by the Centre for Stem Cell Research at Christian Medical College, Vellore, successfully conducted the country's first in-human gene therapy for hemophilia A. With the innovative approach, five patients were treated, and there were no bleeding events observed among them for a total follow-up of 81 months, showing the efficacy and durability of the therapy.

Challenges:

Limited access to healthcare facilities in certain regions hinders effective hemophilia management.

Restricted access to healthcare centers considerably inhibits effective hemophilia management, particularly in nations such as India. Despite an estimated 80,000 to 100,000 severe hemophilia cases nationwide, only about 21,000 are registered, indicating that nearly 80% remain undiagnosed due to lack of awareness and diagnostic facilities. Treatment accessibility is also a concern. Currently, only 4% of Indian children with hemophilia are being given prophylactic treatment, compared to 80-90% are treated in developed nations. Such unevenness results in recurrent bleeding incidents and chronic deterioration of joints among untreated patients. The shortages of clotting factor concentrates contribute to the difficulties. Such difficulty leads to aggravated disability and reduced quality of life among hemophilia patients in communities with poor medical infrastructure.

By Type

In 2023, Hemophilia A accounted for the largest share at 73%. There are several reasons for this dominance, hemophilia A is more frequent than the other hemophilia types. Hemophilia A is three to four times as common as hemophilia B, according to the Centers for Disease Control and Prevention, and the larger share of Hemophilia A in the market can also be attributed to a higher number of treatment options and continued research that is focused on this type. The CDC estimates that among all males with hemophilia, slightly more than 4 in 10 have the severe form, which requires more intensive and frequent treatment. In addition, the major shares of Hemophilia A can be attributed to the fact that patients with severe forms tend to utilize more costly therapies which employ advanced technology. The market is further boosted due to growing approval of new treatments specifically for Hemophilia A by the FDA, which has provided more options available for patients.

Government initiatives have significantly contributed to the excellence of the Hemophilia A market segment. Data and algorithms to determine the future trajectory of hemophilia care development Hemophilia A, with its underdeveloped therapies, should benefit from time by focusing on strengthening surveillance and data and research capabilities of healthcare systems to rapidly respond to the treatment market.

By Treatment

The prophylaxis segment held the majority share of 47% in 2023. The large market share is due to increased focus on preventive care and the demonstrated success of prophylactic treatment in reducing bleeding episodes and improving the quality of life of hemophilia patients. According to the CDC, prophylaxis is now considered the standard of care for individuals with severe hemophilia, particularly in developed countries. The dominance of the prophylaxis segment is supported by clinical evidence and government recommendations. The CDC and other health organizations recommend prophylactic treatment, particularly in children, to avoid damage to the joints and other complications related to repeated bleeding. The results have been proven to drastically minimize the number of hemorrhagic occurrences as well as the hospitalization rates of hemophiliacs.

Furthermore, government initiatives to improve access to prophylactic treatment have contributed to its market dominance. National hemophilia programs, which are now being established in many countries, have a strong emphasis on prophylaxis for pediatric patients in particular. Combined with growing awareness in healthcare providers and patients regarding the advantages of prophylaxis, these programs have fueled the growth of this segment.

By Therapy

In 2023, factor replacement therapy segment captured the largest market share of 60%. The major share can be attributed to the established effectiveness of factor replacement therapy and its long-established use in the management of the disorder. In the case of hemophilia, factor replacement therapy involves infusing the missing clotting factor into the patient’s bloodstream to treat or prevent bleeding episodes. The dominance of factor replacement therapy is supported by extensive clinical data and recommendations from health authorities. The CDC and other organizations recognize factor replacement as the primary treatment for hemophilia, particularly for severe cases. Overwhelming clinical evidence and guidance from health authorities support the use of factor replacement therapy as the standard of care. According to CDC data, among all males with hemophilia, just over 4 in 10 have the severe form of the disorder, necessitating regular factor replacement therapy.

The continuous improvements in factor replacement products. Improved treatment efficacy with recombinant factors and their extended half-life counterparts have revolutionised the treatment of patients with bleeding disorders and facilitated a shift from intravenous injections to subcutaneous infusions, helping to improve patient adherence and quality of life. These advancements have kept factor replacement therapy at the forefront of hemophilia treatment, despite the emergence of newer therapies.

By Distribution Channel

The specialty pharmacies segment held a 62% market share of the hemophilia market in 2023. The treatment of hemophilia is highly specialized, and the management of patients with hemophilia is complex, contributing to this large market share. Role of specialty pharmacies in dispensing hemophilia medications, patient education, and support services needed for disease management Government data and health practice make it clear that specialty pharmacies dominate care for people with hemophilia. The CDC states that the majority of hemophilia patients in the United States receive treatment through a system of federally funded hemophilia treatment centers (HTCs) These centers typically collaborate with specialty pharmacies, ensuring that patients have access to needed medicines and supplies.

Another significant factor leading to the rise of specialty pharmacies in hemophilia care is due to different companies and governments creating policies and regulations that require strict adherence to treatment protocols. State Medicaid programs and other government healthcare initiative have acknowledged the advantages of using specialty pharmacy services and have linked their increasing use in the distribution of hemophilia medications.

In 2023, North America region dominated and held the largest market share 45%. There are several factors contributing to this dominance, such as an advanced healthcare infrastructure, high levels of awareness, and considerable research and development spending. As per the CDC, approximately 33,000 males are living with hemophilia in the United States alone, which shows that a large patient population is present who is driving the market growth. Government initiatives in both regions have played crucial roles in shaping the market. In North America, the CDC's efforts in surveillance and research have led to better understanding and management of hemophilia.

The Asia-Pacific region is projected to grow at the highest CAGR over the forecast period. The rapid growth is mainly driven by the enhancing healthcare infrastructure, increasing diagnosis rate, and rising awareness of hemophilia in countries such as China and India. According to the World Federation of Hemophilia, these nations have experienced a notable surge in identified cases of hemophilia in recent years, indicating a growing market for hemophilia treatments. Government initiatives in the Asia-Pacific region focused on enhancing access to hemophilia care in rural parts of the region are also supporting the growth of the market. Such as the inclusion of hemophilia in India's National Health Mission priority disease list resulting in increased funding and awareness campaigns.

Need any customization research on Hemophilia Market - Enquiry Now

Key Service Providers/Manufacturers

Pfizer Inc. (Hympavzi, Beqvez)

Novo Nordisk A/S (Alhemo, NovoEight)

BioMarin Pharmaceutical Inc. (Roctavian)

CSL Behring (Hemlibra, Idelvion)

Swedish Orphan Biovitrum AB (Sobi) (Elocta, Alprolix)

Sanofi S.A. (Efanesoctocog alfa, Alprolix)

Roche Holding AG (Hemlibra)

Takeda Pharmaceutical Company Limited (Advate, Adynovate)

Octapharma AG (Nuwiq, Wilate)

Grifols S.A. (Alphanate, Alphanine SD)

Users

Mayo Clinic

Cleveland Clinic

Great Ormond Street Hospital

St. Jude Children's Research Hospital

Royal Free Hospital

Apollo Hospitals

Fortis Healthcare

AIIMS (All India Institute of Medical Sciences)

National Hemophilia Center,

Haemophilia Treatment Centre, Alfred Hospital

Recent Developments:

In August 2023, the Food and Drug Administration (FDA) approved Hemgenix, the initial gene therapy for hemophilia B, a transformative treatment option from CSL Behring that can potentially cure patients with hemophilia B in a single administration and also represents an exciting evolution in hemophilia care.

In February 2024, Novo Nordisk released positive clinical trial data for concizumab, which is a subcutaneous treatment indicated for both hemophilia A and B, from a phase 3 trial showing that the dose for concizumab prevents bleeding episodes and offering potential convenience versus infusion treatment for patients.

| Report Attributes | Details |

|---|---|

|

Market Size in 2023 |

USD 13.7 Billion |

|

Market Size by 2032 |

USD 24.2 Billion |

|

CAGR |

CAGR of 6.5% From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Type (Hemophilia A, Hemophilia B, Others) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Pfizer Inc., Novo Nordisk A/S, BioMarin Pharmaceutical Inc., CSL Behring, Swedish Orphan Biovitrum AB (Sobi), Sanofi S.A., Roche Holding AG, Takeda Pharmaceutical Company Limited, Octapharma AG, Grifols S.A. |

Ans. The projected market size for the Hemophilia Market is USD 24.2 Billion by 2032.

Ans: The North American region dominated the Hemophilia Market in 2023.

Ans. The CAGR of the Hemophilia Market is 6.5% During the forecast period of 2024-2032.

Ans: The major key players in the market are Pfizer Inc., Novo Nordisk A/S, BioMarin Pharmaceutical Inc., CSL Behring, Swedish Orphan Biovitrum AB (Sobi), Sanofi S.A., Roche Holding AG, Takeda Pharmaceutical Company Limited, Octapharma AG, Grifols S.A., and others in the final report.

Ans: The Hemophilia A Type segment dominated the Hemophilia Market.

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023)

5.2 Treatment Adoption Trends (2023), by Region

5.5 Healthcare Spending on Hemophilia (2023)

5.6 Therapeutic Advancements and Innovation Trends

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Hemophilia Market Segmentation, By Type

7.1 Chapter Overview

7.2 Hemophilia A

7.2.1 Hemophilia A Market Trends Analysis (2020-2032)

7.2.2 Hemophilia A Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Hemophilia B

7.3.1 Hemophilia B Market Trends Analysis (2020-2032)

7.3.2 Hemophilia B Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Others

7.4.1 Others Market Trends Analysis (2020-2032)

7.4.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Hemophilia Market Segmentation, By Treatment Type

8.1 Chapter Overview

8.2 On-demand

8.2.1 On-demand Market Trends Analysis (2020-2032)

8.2.2 On-demand Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Cure

8.3.1 Cure Market Trends Analysis (2020-2032)

8.3.2 Cure Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Prophylaxis

8.4.1 Prophylaxis Market Trends Analysis (2020-2032)

8.4.2 Prophylaxis Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Hemophilia Market Segmentation, By Distribution Channel

9.1 Chapter Overview

9.2 Hospital Pharmacies

9.2.1 Hospital Pharmacies Market Trends Analysis (2020-2032)

9.2.2 Hospital Pharmacies Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Specialty Pharmacies

9.3.1 Specialty Pharmacies Market Trends Analysis (2020-2032)

9.3.2 Specialty Pharmacies Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Hemophilia Market Segmentation, By Therapy

10.1 Chapter Overview

10.2 Factor Replacement Therapy

10.2.1 Factor Replacement Therapy Market Trends Analysis (2020-2032)

10.2.2 Factor Replacement Therapy Market Size Estimates and Forecasts to 2032 (USD Billion)

10.2.3 Plasma-derived Factor Concentrates

10.2.3.1 Plasma-derived Factor Concentrates Market Trends Analysis (2020-2032)

10.2.3.2 Plasma-derived Factor Concentrates Market Size Estimates and Forecasts to 2032 (USD Billion)

10.2.3.3 Factor VIII

10.2.3.3.1 Factor VIII Market Trends Analysis (2020-2032)

10.2.3.3.2 Factor VIII Market Size Estimates and Forecasts to 2032 (USD Billion)

10.2.3.4 Factor IX

10.2.3.4.1 Factor IX Market Trends Analysis (2020-2032)

10.2.3.4.2 Factor IX Market Size Estimates and Forecasts to 2032 (USD Billion)

10.2.4 Recombinant Factor Concentrates

10.2.4.1 Recombinant Factor Concentrates Market Trends Analysis (2020-2032)

10.2.4.2 Recombinant Factor Concentrates Market Size Estimates and Forecasts to 2032 (USD Billion)

10.2.4.3 Factor VIII

10.2.4.3.1 Factor VIII Market Trends Analysis (2020-2032)

10.2.4.3.2 Factor VIII Market Size Estimates and Forecasts to 2032 (USD Billion)

10.2.4.4 Factor VII

10.2.4.4.1 Factor VII Market Trends Analysis (2020-2032)

10.2.4.4.2 Factor VII Market Size Estimates and Forecasts to 2032 (USD Billion)

10.2.4.5 Factor IX

10.2.4.5.1 Factor IX Market Trends Analysis (2020-2032)

10.2.4.5.2 Factor IX Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Desmopressin & Fibrin Sealants

10.3.1 Desmopressin & Fibrin Sealants Market Trends Analysis (2020-2032)

10.3.2 Desmopressin & Fibrin Sealants Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Gene Therapy & Monoclonal Antibodies

10.4.1 Gene Therapy & Monoclonal Antibodies Market Trends Analysis (2020-2032)

10.4.2 Gene Therapy & Monoclonal Antibodies Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Hemophilia Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.2.4 North America Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.2.5 North America Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.2.6 North America Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.2.7.2 USA Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.2.7.3 USA Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.2.7.4 USA Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.2.7 Canada

11.2.7.1 Canada Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.2.7.2 Canada Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.2.7.3 Canada Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.2.7.3 Canada Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.2.8 Mexico

11.2.8.1 Mexico Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.2.8.2 Mexico Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.2.8.3 Mexico Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.2.8.3 Mexico Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Hemophilia Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.1.6 Poland

11.3.1.6.1 Poland Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.1.6.2 Poland Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.1.6.3 Poland Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.1.6.3 Poland Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.1.7 Romania

11.3.1.7.1 Romania Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.1.7.2 Romania Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.1.7.3 Romania Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.1.7.3 Romania Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.1.8 Hungary

11.3.1.8.1 Hungary Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.1.8.2 Hungary Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.1.8.3 Hungary Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.1.8.3 Hungary Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.1.9 Turkey

11.3.1.9.1 Turkey Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.1.9.2 Turkey Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.1.9.3 Turkey Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.1.9.3 Turkey Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Hemophilia Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.4 Western Europe Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.5 Western Europe Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.5 Western Europe Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.6 Germany

11.3.2.6.1 Germany Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.6.2 Germany Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.6.3 Germany Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.6.3 Germany Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.7 France

11.3.2.7.1 France Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.7.2 France Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.7.3 France Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.7.3 France Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.8 UK

11.3.2.8.1 UK Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.8.2 UK Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.8.3 UK Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.8.3 UK Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.9 Italy

11.3.2.9.1 Italy Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.9.2 Italy Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.9.3 Italy Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.9.3 Italy Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.11.2 Spain Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.11.3 Spain Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.11.3 Spain Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.11 Netherlands

11.3.2.11.1 Netherlands Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.11.2 Netherlands Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.11.3 Netherlands Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.11.3 Netherlands Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.12 Switzerland

11.3.2.12.1 Switzerland Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.12.2 Switzerland Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.12.3 Switzerland Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.12.3 Switzerland Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.13 Austria

11.3.2.13.1 Austria Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.13.2 Austria Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.13.3 Austria Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.13.3 Austria Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.3.2.14 Rest of Western Europe

11.3.2.14.1 Rest of Western Europe Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.3.2.14.2 Rest of Western Europe Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.3.2.14.3 Rest of Western Europe Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.3.2.14.3 Rest of Western Europe Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Hemophilia Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.4 Asia Pacific Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.5 Asia Pacific Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.5 Asia Pacific Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.6 China

11.4.6.1 China Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.6.2 China Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.6.3 China Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.6.3 China Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.7 India

11.4.7.1 India Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.7.2 India Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.7.3 India Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.7.3 India Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.8 Japan

11.4.8.1 Japan Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.8.2 Japan Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.8.3 Japan Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.8.3 Japan Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.9 South Korea

11.4.9.1 South Korea Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.9.2 South Korea Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.9.3 South Korea Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.9.3 South Korea Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.11.2 Vietnam Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.11.3 Vietnam Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.11.3 Vietnam Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.11 Singapore

11.4.11.1 Singapore Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.11.2 Singapore Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.11.3 Singapore Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.11.3 Singapore Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.12 Australia

11.4.12.1 Australia Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.12.2 Australia Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.12.3 Australia Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.12.3 Australia Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.4.13 Rest of Asia Pacific

11.4.13.1 Rest of Asia Pacific Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.4.13.2 Rest of Asia Pacific Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.4.13.3 Rest of Asia Pacific Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.4.13.3 Rest of Asia Pacific Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Hemophilia Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.1.4 Middle East Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.1.5 Middle East Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.1.5 Middle East Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.1.6 UAE

11.5.1.6.1 UAE Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.1.6.2 UAE Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.1.6.3 UAE Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.1.6.3 UAE Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.1.7 Egypt

11.5.1.7.1 Egypt Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.1.7.2 Egypt Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.1.7.3 Egypt Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.1.7.3 Egypt Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.1.8 Saudi Arabia

11.5.1.8.1 Saudi Arabia Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.1.8.2 Saudi Arabia Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.1.8.3 Saudi Arabia Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.1.8.3 Saudi Arabia Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.1.9 Qatar

11.5.1.9.1 Qatar Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.1.9.2 Qatar Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.1.9.3 Qatar Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.1.9.3 Qatar Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Hemophilia Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.2.4 Africa Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.2.5 Africa Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.2.8.3 Africa Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.2.6 South Africa

11.5.2.6.1 South Africa Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.2.6.2 South Africa Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.2.6.3 South Africa Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.2.8.3 South Africa Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.2.7 Nigeria

11.5.2.7.1 Nigeria Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.2.7.2 Nigeria Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.2.7.3 Nigeria Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.5.2.8 Rest of Africa

11.5.2.8.1 Rest of Africa Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.5.2.8.2 Rest of Africa Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.5.2.8.3 Rest of Africa Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.5.2.8.3 Rest of Africa Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Hemophilia Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.6.4 Latin America Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.6.5 Latin America Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.6.5 Latin America Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.6.6 Brazil

11.6.6.1 Brazil Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.6.6.2 Brazil Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.6.6.3 Brazil Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.6.6.3 Brazil Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.6.7 Argentina

11.6.7.1 Argentina Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.6.7.2 Argentina Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.6.7.3 Argentina Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.6.7.3 Argentina Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.6.8 Colombia

11.6.8.1 Colombia Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.6.8.2 Colombia Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.6.8.3 Colombia Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.6.8.3 Colombia Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

11.6.9 Rest of Latin America

11.6.9.1 Rest of Latin America Hemophilia Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

11.6.9.2 Rest of Latin America Hemophilia Market Estimates and Forecasts, By Treatment Type (2020-2032) (USD Billion)

11.6.9.3 Rest of Latin America Hemophilia Market Estimates and Forecasts, By Distribution Channel (2020-2032) (USD Billion)

11.6.9.3 Rest of Latin America Hemophilia Market Estimates and Forecasts, By Therapy (2020-2032) (USD Billion)

12. Company Profiles

12.1 Pfizer Inc.

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Novo Nordisk A/S

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 BioMarin Pharmaceutical Inc.

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 CSL Behring

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Swedish Orphan Biovitrum AB (Sobi)

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Sanofi S.A.

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Roche Holding AG

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Takeda Pharmaceutical Company Limited

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Octapharma AG

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Grifols S.A.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Type

Hemophilia A

Hemophilia B

Others

By Treatment Type

On-demand

Cure

Prophylaxis

By Distribution Channel

Hospital Pharmacies

Specialty Pharmacies

By Therapy

Factor Replacement Therapy

Plasma-derived Factor Concentrates

Factor VIII

Factor IX

Recombinant Factor Concentrates

Factor VIII

Factor VII

Factor IX

Desmopressin & Fibrin Sealants

Gene Therapy & Monoclonal Antibodies

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

Therapeutic Bed Market Size was valued at USD 4.65 Billion in 2023 and is expected to reach USD 7.19 Billion by 2032, growing at a CAGR of 4.98% over the forecast period 2024-2032.

The Sanger Sequencing Market Size was valued at USD 2,901.15 Million in 2023, and is expected to reach USD 12,356.57 Million by 2032, and grow at a CAGR of 18.63% Over the Forecast Period of 2024-2032.

The Data Monetization in Healthcare Market Size was valued at USD 472.7 Million in 2023 and will reach $2169.8 Mn by 2032, with a CAGR of 18.47% over the forecast period of 2024-2032.

The Biopharmaceutical Market Size was valued at USD 486.15 Billion in 2023, and is expected to reach USD 1039.14 Billion by 2032, and grow at a CAGR of 8.82%.

The Epilepsy Device Market Size was valued at USD 0.75 billion in 2023 and is expected to reach USD 1.18 billion by 2032 and grow at a CAGR of 5.15% over the forecast period 2024-2032.

The 5G In Healthcare Market Size was valued at USD 50.64 Bn in 2023 and will reach to USD 834.24 Bn by 2032 and grow at a CAGR of 36.56% by 2024 to 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd