Healthcare Supply Chain Management Market Size & Trends

Get more information on Healthcare Supply Chain Management Market - Request Free Sample Report

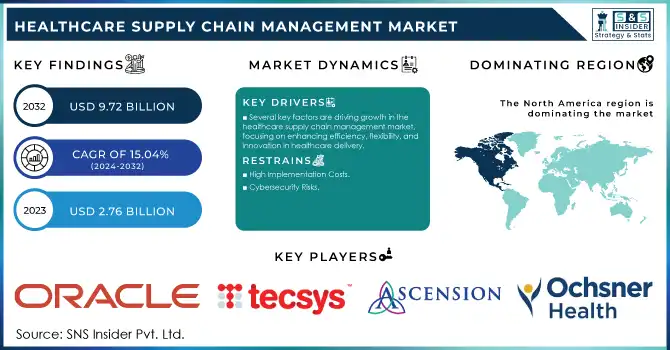

The Healthcare Supply Chain Management Market Size was valued at USD 2.76 billion in 2023 and is expected to reach USD 9.72 billion by 2032, growing at a CAGR of 15.04% over the forecast period 2024-2032.

The Healthcare Supply Chain Management Market is undergoing rapid transformation, driven by the need for operational efficiency and the integration of advanced technologies. Technological advancements are revolutionizing the market. For instance, AI-powered supply chain solutions have demonstrated up to a 25% reduction in inventory costs. Blockchain technology is also gaining traction, particularly in pharmaceutical supply chains, where it has been instrumental in ensuring product authenticity and traceability. Blockchain can also reduce counterfeit drugs by 50%, addressing a significant global healthcare challenge.

The COVID-19 pandemic exposed vulnerabilities in healthcare supply chains, prompting organizations to prioritize resilience and adaptability. For example, during the height of the pandemic, Pfizer and Moderna implemented real-time tracking technologies to monitor vaccine distribution, ensuring cold chain compliance. This effort contributed to the successful delivery of billions of doses worldwide, showcasing the critical role of supply chain management innovation. Cybersecurity remains a pressing concern, with 43% of healthcare organizations experiencing cyberattacks on their supply chain systems in 2023, according to a study by the Ponemon Institute. These threats underscore the importance of investing in secure digital infrastructure to safeguard sensitive data and maintain service continuity.

The rising global healthcare expenditure further drives the adoption of efficient SCM practices. The World Health Organization (WHO) reports that global health spending reached USD 8.5 trillion in 2022, emphasizing the need for cost-effective supply chain strategies. For instance, Kaiser Permanente reduced procurement costs by USD 200 million annually through centralized supply chain management, demonstrating the financial benefits of an optimized approach.

Overall, the healthcare supply chain management market is poised for significant growth, fueled by technological innovation, increased focus on resilience, and the drive to control healthcare costs.

Healthcare Supply Chain Management Market Dynamics

Drivers

-

Several key factors are driving growth in the healthcare supply chain management market, focusing on enhancing efficiency, flexibility, and innovation in healthcare delivery.

One major driver is the increasing focus on regulatory compliance and quality control. Governments and regulatory agencies worldwide are enforcing strict standards for the procurement, storage, and distribution of medical products to ensure safety and effectiveness. For instance, the U.S. Drug Supply Chain Security Act (DSCSA) mandates comprehensive traceability within the pharmaceutical supply chain, encouraging the adoption of advanced supply chain management technologies.

Another important driver is the rising demand for personalized medicine and patient-centric healthcare. These trends require agile supply chain systems capable of managing smaller, more frequent shipments while maintaining product quality, particularly for temperature-sensitive biologics. Innovations in cold chain logistics, supported by IoT-enabled sensors, are crucial to meet these evolving needs.

The increasing prevalence of chronic diseases, such as diabetes and cardiovascular conditions, further boosts the need for efficient supply chains to deliver medical devices, medications, and monitoring equipment. With the International Diabetes Federation predicting that nearly 783 million people will have diabetes by 2045, the demand for effective supply chain management solutions is expected to grow.

Additionally, the rise of e-commerce in healthcare, including online pharmacies and telemedicine services, is reshaping supply chain dynamics. Companies like Amazon Care are using digital platforms to deliver healthcare products directly to consumers, driving innovation in last-mile logistics.

Restraints

-

High Implementation Costs

The adoption of advanced healthcare supply chain technologies, such as AI, blockchain, and IoT, requires significant investment in infrastructure, training, and system integration, which can be a barrier for smaller healthcare providers and organizations with limited budgets.

-

Cybersecurity Risks

The increasing digitization of healthcare supply chains has raised concerns about data security and privacy. Cyberattacks targeting supply chain systems can disrupt operations and compromise sensitive patient and product information, creating significant challenges for healthcare organizations.

Segmentation Analysis

By Component

The Software segment accounted for approximately 65.0% of the market share in 2023. The growing reliance on software solutions such as advanced SCM platforms, inventory management tools, and supply chain analytics is a key factor behind this dominance. Software allows healthcare organizations to optimize their supply chain by providing real-time tracking, improving demand forecasting, and enhancing operational efficiency. The demand for integrated software solutions is driven by the need for greater automation, data-driven decision-making, and the increasing complexity of healthcare supply chains.

The Cloud-based Software segment is the fastest-growing in the Healthcare supply chain management market. Cloud-based solutions offer significant advantages, such as scalability, flexibility, and cost-effectiveness. As healthcare organizations embrace digital transformation, cloud-based supply chain management solutions have gained popularity for their ability to provide real-time data access, promote collaboration among stakeholders, and reduce the need for substantial infrastructure investments. The shift to cloud technology is being driven by the growing need for remote access and more agile supply chain management systems.

By Delivery Mode

In 2023, On-premise solutions represented approximately 60.0% of the market share. On-premise systems offer healthcare organizations greater control and security over their data, which is especially important for managing sensitive patient information and critical medical supplies. Large healthcare providers and hospitals typically prefer on-premise solutions because they allow for customizability, higher data security, and better compliance with regulatory requirements.

The Cloud-based delivery mode emerged as the fastest-growing segment throughout the forecast period. This growth is largely driven by the increasing adoption of cloud technologies, which provide healthcare organizations with flexible, scalable, and cost-effective solutions. Cloud-based systems allow real-time data access and collaboration, which are essential for streamlining supply chain operations. As healthcare systems increasingly move towards digital solutions, cloud-based delivery modes are expected to continue their rapid growth.

Regional Analysis

North America held the largest market share, primarily driven by advanced healthcare infrastructure, high technological adoption, and a focus on cost-effective solutions. The United States is the primary contributor, where healthcare providers increasingly integrate supply chain management solutions to enhance operational efficiency, regulatory compliance, and supply chain visibility. The region also sees growing demand for cloud-based solutions and automation, ensuring further market dominance.

Europe followed as a strong contender, with countries like Germany, the UK, and France embracing digital transformation in healthcare. The region's focus on sustainability and regulatory compliance is driving the adoption of advanced supply chain management technologies. Europe's healthcare providers and manufacturers are increasingly moving towards integrated cloud-based solutions, promoting agility and scalability in their operations. The rising cost pressures and need for transparency in supply chains further fuel growth in this market.

The Asia Pacific region is experiencing the fastest growth, attributed to rapid economic development, rising healthcare expenditures, and a shift towards digital technologies in countries such as China, India, and Japan. As the healthcare industry modernizes, there is an increasing demand for efficient supply chain solutions to handle the complexities of growing populations and medical needs. The region’s expanding healthcare infrastructure and digital healthcare adoption make it a key area for future market growth.

Need any customization research on Healthcare Supply Chain Management Market - Enquiry Now

Key Players

-

Oracle - Oracle Healthcare Supply Chain Management

-

Tecsys Inc. - Tecsys Healthcare Supply Chain Solutions

-

Global Healthcare Exchange, LLC (GHX) - GHX Healthcare Supply Chain Solutions

-

Ascension - Ascension Supply Chain Services

-

Ochsner Health - Ochsner Health Supply Chain Solutions

-

Banner Health - Banner Health Supply Chain Solutions

-

Henry Schein, Inc. - Henry Schein Healthcare Supply Chain Solutions

-

McKesson Corporation - McKesson Supply Chain Management Solutions

-

Cardinal Health - Cardinal Health Supply Chain Solutions

-

Epicor Software Corporation - Epicor Healthcare Supply Chain Solutions

-

SAP - SAP Integrated Business Planning for Healthcare

-

Infor - Infor Healthcare Supply Chain Solutions

-

Manhattan Associates - Manhattan Active Supply Chain for Healthcare

-

Jump Technologies - JumpStock Healthcare Inventory Management

-

JDA Software - JDA Healthcare Supply Chain Solutions

-

LogiTag Systems - LogiTag Healthcare Supply Chain Solutions

-

Advocate Health Care - Advocate Health Care Supply Chain Solutions

Recent Development

In November 2024, Blue Ocean Corporation introduced its Global Healthcare Supply Chain Training and Consulting Program, targeting the transformation of India’s healthcare sector. With a focus on the dynamic and expanding market, the company aims to tailor its services to meet the sector’s specific needs and challenges.

In Nov 2024, Inspirity Health Partners, a collaboration between HumanityCorp and Mayo Clinic Supply Chain Management, emerged as a key player in helping healthcare providers improve efficiency and financial alignment. This partnership gained momentum by offering solutions that addressed the unique challenges faced by independent healthcare organizations, particularly in navigating compressed operating margins.

In Aug 2024, Clarium secured a USD 10.5 million strategic financing round, led by General Catalyst, to accelerate the modernization of healthcare supply chains. The company also launched Astra OS, an AI-powered workflow platform and data ecosystem, designed to transform and streamline supply chain management for hospitals and health systems.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 2.76 billion |

| Market Size by 2032 | USD 9.72 Billion |

| CAGR | CAGR of 15.04% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Hardware, Services) • By Delivery Mode (On-premise, Cloud-based) • By End-user (Healthcare Providers, Healthcare Manufacturers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Oracle, Tecsys Inc., Global Healthcare Exchange (GHX), Ascension, Ochsner Health, Banner Health, Henry Schein, Inc., McKesson Corporation, Cardinal Health, Epicor Software Corporation, SAP, Infor, Manhattan Associates, Jump Technologies, JDA Software, LogiTag Systems, Advocate Health Care |

| Key Drivers | • Several key factors are driving growth in the healthcare supply chain management market, focusing on enhancing efficiency, flexibility, and innovation in healthcare delivery. |

| Restraints | • High Implementation Costs • Cybersecurity Risks |

Frequently Asked Questions

Ans: North America is the dominant region in the Healthcare Supply Chain Management market.

Ans: The adoption of advanced healthcare supply chain technologies, such as AI, blockchain, and IoT, requires significant investment in infrastructure, training, and system integration, which can be a barrier for smaller healthcare providers and organizations with limited budgets.

Ans: Several key factors are driving growth in the healthcare supply chain management market, focusing on enhancing efficiency, flexibility, and innovation in healthcare delivery.

Ans: The estimated compound annual growth rate is 15.04% during the forecast period for the Healthcare Supply Chain Management market.

Ans: The projected market value of the Healthcare Supply Chain Management market is estimated at USD 2.76 billion in 2023 and is expected to reach USD 9.72 billion by 2032.

Get in touch