Get more information on Healthcare Cyber Security Market - Request Sample Report

The Healthcare Cyber Security Market size was valued at USD 17.10 Billion in 2023 and is expected to reach USD 80.60 Billion by 2032 and grow at a CAGR of 18.8% over the forecast period 2024-2032.

The healthcare industry is witnessing a high demand for effective solutions against cybersecurity threats. The major aspect that has been clearly analysed here has been the increasing incidents of cybercrimes targeting health care providers. Patient’s data was compromised in 45% of the total breaches in 2022 according to the Department of Human and Health Services (HHS) wherein 40 million people were affected. In terms of compromised patient records, this means that there was an almost 30% increase from those of 2021. Furthermore, the Federal Bureau of Investigation (FBI’s) report on ransomware attacks in 2023 revealed that cybercriminals have grown more advanced with a 67% increase in attacks on the healthcare sector. These attacks interfere with patient care and also cause significant financial losses since it takes over USD 9.3 million as an average cost for a breach involving healthcare data. As such, increased attack rates, escalating demand for securing information, as well as high expense of violations are forcing medical organizations across America to focus more on investing in security systems. Also, the high adoption rates of AI in healthcare in developed nations is playing a major role in improving the overall demand landscape for healthcare cyber security market. For instance, 90% of nursing tasks will be done by artificial intelligence by 2030 which will ultimately force the need for healthcare cyber security solutions.

Moreover, government regulations are similarly serving a very imperative function. Health Insurance Portability and Accountability Act (HIPAA) is crucial as it requires strong data security measures while the Department of Justice (DOJ) goes after criminals in the healthcare cyber fraud sector. Thus, such combinations are pushing the healthcare cyber security market to its next stage of substantial growth. Having this in mind, US health care industry due to some factors coming together has been witnessing an upswing regarding demanding strong cybersecurity solutions. The main one among them is the disturbing growth of cyber-attacks on health care providers.

Market Dynamics:

Drivers:

The regulatory bodies across the globe have started applying even tighter rules regarding the protection of data like HIPAA in the US and GDPR regulation in EU.

The use of invasive and wearable medical low-power devices in healthcare palate the Internet of things (IoT). Moreover, the use of clouds for storage is now being practices with EHRs, although it remains common.

The rising technological advancements and the increased in the use of IT solutions particularly for outpatient services among healthcare workers.

The enhancement of technology has led to the simplification of healthcare personnel's procedures for outpatient care through an increase in IT solutions. Electronic health records allow secure access to patient data, enabling drug management and virtual medical appointments. Telehealth services enable virtual appointments, enhancing accessibility for patients residing at a distance or facing mobility constraints. However, this compromising factor presents the healthcare cybersecurity market at risk because, as time passes, the dependency on technology increases. Proper implementations of cybersecurity are essential because reported major breaches doubled from 2018 and 2022 with 93% in rate. The need for enhancing the security arrangements is believed by the healthcare facilities to be on the rise following the deployment of the IT solutions.

Restrains:

Many health professionals are unaware about cyber threats such as scam that may occur due to human errors leading to cyber-attacks or leaking data.

A lack of cybersecurity training is evident as less than a third of the health workers claiming to have had any training at all, but a significant number of them also seem to have little knowledge concerning the existence of cyber threats in the first place. This leads to a rather risky position when it comes to financial operations. The employees for instance when conducted through phishing, they can be made to release certain key information or click some certain links which can effectively launch a cyber-attack or release sensitive information.

Such lack of preparation boosts the healthcare cyber security market. Since patient data is often under attack, the necessity for formidable protection is without doubt. For instance, in May 2024 when a hospital chain largely failed the test on a vulnerability that had become apparent. Cyber criminals we’re able to breach the system through a phishing email, violating the patients’ records and thereby placing the lives of thousands at risk due to the treatments that were made to be delayed. This incident supports the very much needed cybersecurity education in healthcare organizations.

On The Basis of Component

Solutions

Antivirus and Antimalware

Identity and Access Management Solutions

Encryption and Data Loss Protection Solutions

Other solutions

Services

Consulting

Managed Security Services

Others Services

On The Basis of Security Type

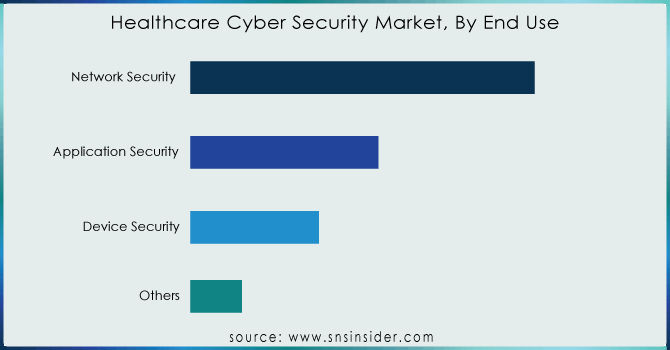

Network Security

Application Security

Device Security

Others

Network Security held around 60% share in 2023, is indeed the largest segment and it gives rise to firewalls, intrusion detection/prevention systems (IDS/IPS) and data loss prevention (DLP) among others. Such tools keep off unauthorized admission, malicious code infestation as well as these tools help in keeping away hackers from accessing healthcare data.

Application Security accounted for 25% of share, this segment looks at how to protect healthcare applications that hold and process sensitive patient information. It contains products such as web application firewall, source code scanners, or API security that do not allow attackers take advantage of weak points in healthcare apps. According to SNS Insider study Device Security held around 15% share in 2023. With connected medical devices like pacemakers and insulin pumps on the rise, securing them becomes very important. This section also covers end point security software, device authentication protocols and encryption keys which secure these gadgets from any form of manipulation and access by unauthorized parties.

Get more information on Healthcare Cyber Security Market - Enquiry Now

On The Basis of Deployment

On-premises

Cloud-based

In 2023 on-premises solutions were dominant approximately holding around 65% share for the healthcare organizations that wanted total control of their security systems. This was attractive to institutions with strict regulatory demands or fears of cloud privacy invasion. Recently, the use of cloud-based solutions which is expected to reach 35% by 2032 is growing due to the advantages of scalability, cost savings, and ease in implementation particularly for small practices. Furthermore, initial fears are being addressed through improved cloud protection protocols and expanding faith in reputable cloud service providers. Thus, a mixture of on-premises and cloud-based solutions is formed by this situation where some companies match them with their specific safety needs and infrastructure capabilities.

On The Basis of End-use

Pharma & Chemicals

Medical Devices

Health Insurance

Hospitals

Others

Hospitals are one of the major platforms for cyberattacks, accounted for approximately 35% of the market share due to their vast stores of electronic health records (EHRs) and dependence on interlinked medical devices. For Pharma & Chemicals segment which held 20% share in 2023, industrial espionage is a known threat that steals intellectual property and research data.

Manufacturers of medical devices is growing segment which held 15% share in 2023 and is expected to be the fastest segment over the forecast period, have difficulties in securing connected devices from vulnerabilities capable to disrupt patient care or compromise safety. Health insurance companies accounted for approximately 10% share regard the protection of sensitive financial information and prevention of fraudulent claims as key.

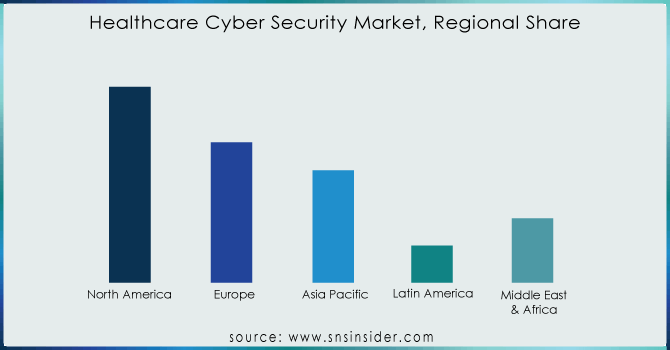

The North American healthcare cybersecurity was a market leader globally with over 40% market share in 2023. Many top healthcare cybersecurity companies are based in the United States which is a powerhouse in North America, making the U.S. marketplace highly competitive and full of opportunities. These companies provide cutting edge solutions for an extensive healthcare infrastructure including hospitals, clinics and pharmaceutical giants. Secondly, North America has a high level of consciousness about cyber threats. At least one cyber-attack has been experienced by 75% of healthcare organizations in the region. Increased awareness of this has prompted more investment into cybersecurity solutions, thus driving market growth. Furthermore, stringent government regulations exist in North America concerning patient data privacy (HIPAA) that require strong cybersecurity measures. These regulations mixed with a rapidly changing threat landscape repeat the position of North America as the leading healthcare cybersecurity market.

Asia-Pacific’s healthcare sector is undergoing a transition to an interconnected system with an increased usage of EHRs, telehealth & telemedicine and internet connected medical devices. The digitalization process however not only improves patients’ care but also increases the chances for cyber-criminals to sneak into an organization’s systems. In Asia, it is shocking that as high as 75% of its people do not have basic knowledge on how to stay safe online therefore making them vulnerable to social engineering tactics and phishing attacks. This loophole is further increased since at least some underdeveloped countries within APAC still lack the required network infrastructure capable of protecting their systems from sophisticated cyber-attacks. But the scenario is not completely vulnerable, a recent study stated there has been an increase in the number of cyberattacks up to 80% further causing a boom in health care security cognizance. Solutions such as Identity and Access Management (IAM) would be mainly used by governments and healthcare providers to enhance safety for access to patient’s sensitive data.

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major key players are Northrop Grumma Corporation, Palo Alto Networks, Inc., Sensato investors, Symantec Corporation, Cisco Systems, Inc., FireEye, Inc., IBM Corporation, Kaspersky Lab, Lockheed Martin Corporation, MACAFEE, INC. & Other Players

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 17.10 Billion |

| Market Size by 2032 | USD 80.60 Billion |

| CAGR | CAGR 18.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solution and services) • by Security Type (Network Security, Application Security, Device Security, and Others) • by Deployment (On-premises and Cloud-based) • by End-use (Pharma & Chemicals, Medical Devices, Health Insurance, Hospitals, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Northrop Grumma Corporation, Palo Alto Networks, Inc., sensato investors, Symantec Corporation, Cisco Systems, Inc., FireEye, Inc., IBM Corporation, Kaspersky Lab, Lockheed Martin Corporation, and MACAFEE, INC. |

| Key Drivers |

|

| Market Restraints |

|

Ans: - The Healthcare Cyber Security Market size was valued at USD 17.10 Bn in 2023.

Ans: - The Healthcare Cyber Security Market is to grow at CAGR of a 18.8% over the forecast period 2024-2032.

Ans: - North America is expected to account for the greatest proportion of the global healthcare cybersecurity market.

Ans: - The major key players are Northrop Grumma Corporation, Palo Alto Networks, Inc., sensato investors, Symantec Corporation, Cisco Systems, Inc., FireEye, Inc., IBM Corporation, Kaspersky Lab, Lockheed Martin Corporation, and MACAFEE, INC.

Ans: - Key Stakeholders Considered in the study are Raw material vendors, Regulatory authorities, including government agencies and NGOs, Commercial research, and development (R&D) institutions, Importers and exporters, etc.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Healthcare Cyber Security Market Segmentation, By Component

7.1 Introduction

7.2 Solutions

7.2.1 Antivirus and Antimalware

7.2.2 Identity and Access Management Solutions

7.2.3 Encryption and Data Loss Protection Solutions

7.2.4 Other solutions

7.3 Services

7.3.1 Consulting

7.3.2 Managed Security Services

7.3.3 Others Services

8. Healthcare Cyber Security Market Segmentation, By Security Type

8.1 Introduction

8.2 Network Security

8.3 Application Security

8.4 Device security

8.5 Others

9. Healthcare Cyber Security Market Segmentation, By Deployment

9.1 Introduction

9.2 On-Premises

9.3 Cloud-based

10. Healthcare Cyber Security Market Segmentation, By End User

10.1 Introduction

10.2 Pharma & Chemicals

10.3 Medical Devices

10.4 Health Insurance

10.5 Hospitals

10.6 Others

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 Trend Analysis

11.2.2 North America Healthcare Cyber Security Market by Country

11.2.3 North America Healthcare Cyber Security Market By Component

11.2.4 North America Healthcare Cyber Security Market By Security Type

11.2.5 North America Healthcare Cyber Security Market By Deployment

11.2.6 North America Healthcare Cyber Security Market By End User

11.2.7 USA

11.2.7.1 USA Healthcare Cyber Security Market By Component

11.2.7.2 USA Healthcare Cyber Security Market By Security Type

11.2.7.3 USA Healthcare Cyber Security Market By Deployment

11.2.7.4 USA Healthcare Cyber Security Market By End User

11.2.8 Canada

11.2.8.1 Canada Healthcare Cyber Security Market By Component

11.2.8.2 Canada Healthcare Cyber Security Market By Security Type

11.2.8.3 Canada Healthcare Cyber Security Market By Deployment

11.2.8.4 Canada Healthcare Cyber Security Market By End User

11.2.9 Mexico

11.2.9.1 Mexico Healthcare Cyber Security Market By Component

11.2.9.2 Mexico Healthcare Cyber Security Market By Security Type

11.2.9.3 Mexico Healthcare Cyber Security Market By Deployment

11.2.9.4 Mexico Healthcare Cyber Security Market By End User

11.3 Europe

11.3.1 Trend Analysis

11.3.2 Eastern Europe

11.3.2.1 Eastern Europe Healthcare Cyber Security Market by Country

11.3.2.2 Eastern Europe Healthcare Cyber Security Market By Component

11.3.2.3 Eastern Europe Healthcare Cyber Security Market By Security Type

11.3.2.4 Eastern Europe Healthcare Cyber Security Market By Deployment

11.3.2.5 Eastern Europe Healthcare Cyber Security Market By End User

11.3.2.6 Poland

11.3.2.6.1 Poland Healthcare Cyber Security Market By Component

11.3.2.6.2 Poland Healthcare Cyber Security Market By Security Type

11.3.2.6.3 Poland Healthcare Cyber Security Market By Deployment

11.3.2.6.4 Poland Healthcare Cyber Security Market By End User

11.3.2.7 Romania

11.3.2.7.1 Romania Healthcare Cyber Security Market By Component

11.3.2.7.2 Romania Healthcare Cyber Security Market By Security Type

11.3.2.7.3 Romania Healthcare Cyber Security Market By Deployment

11.3.2.7.4 Romania Healthcare Cyber Security Market By End User

11.3.2.8 Hungary

11.3.2.8.1 Hungary Healthcare Cyber Security Market By Component

11.3.2.8.2 Hungary Healthcare Cyber Security Market By Security Type

11.3.2.8.3 Hungary Healthcare Cyber Security Market By Deployment

11.3.2.8.4 Hungary Healthcare Cyber Security Market By End User

11.3.2.9 Turkey

11.3.2.9.1 Turkey Healthcare Cyber Security Market By Component

11.3.2.9.2 Turkey Healthcare Cyber Security Market By Security Type

11.3.2.9.3 Turkey Healthcare Cyber Security Market By Deployment

11.3.2.9.4 Turkey Healthcare Cyber Security Market By End User

11.3.2.10 Rest of Eastern Europe

11.3.2.10.1 Rest of Eastern Europe Healthcare Cyber Security Market By Component

11.3.2.10.2 Rest of Eastern Europe Healthcare Cyber Security Market By Security Type

11.3.2.10.3 Rest of Eastern Europe Healthcare Cyber Security Market By Deployment

11.3.2.10.4 Rest of Eastern Europe Healthcare Cyber Security Market By End User

11.3.3 Western Europe

11.3.3.1 Western Europe Healthcare Cyber Security Market by Country

11.3.3.2 Western Europe Healthcare Cyber Security Market By Component

11.3.3.3 Western Europe Healthcare Cyber Security Market By Security Type

11.3.3.4 Western Europe Healthcare Cyber Security Market By Deployment

11.3.3.5 Western Europe Healthcare Cyber Security Market By End User

11.3.3.6 Germany

11.3.3.6.1 Germany Healthcare Cyber Security Market By Component

11.3.3.6.2 Germany Healthcare Cyber Security Market By Security Type

11.3.3.6.3 Germany Healthcare Cyber Security Market By Deployment

11.3.3.6.4 Germany Healthcare Cyber Security Market By End User

11.3.3.7 France

11.3.3.7.1 France Healthcare Cyber Security Market By Component

11.3.3.7.2 France Healthcare Cyber Security Market By Security Type

11.3.3.7.3 France Healthcare Cyber Security Market By Deployment

11.3.3.7.4 France Healthcare Cyber Security Market By End User

11.3.3.8 UK

11.3.3.8.1 UK Healthcare Cyber Security Market By Component

11.3.3.8.2 UK Healthcare Cyber Security Market By Security Type

11.3.3.8.3 UK Healthcare Cyber Security Market By Deployment

11.3.3.8.4 UK Healthcare Cyber Security Market By End User

11.3.3.9 Italy

11.3.3.9.1 Italy Healthcare Cyber Security Market By Component

11.3.3.9.2 Italy Healthcare Cyber Security Market By Security Type

11.3.3.9.3 Italy Healthcare Cyber Security Market By Deployment

11.3.3.9.4 Italy Healthcare Cyber Security Market By End User

11.3.3.10 Spain

11.3.3.10.1 Spain Healthcare Cyber Security Market By Component

11.3.3.10.2 Spain Healthcare Cyber Security Market By Security Type

11.3.3.10.3 Spain Healthcare Cyber Security Market By Deployment

11.3.3.10.4 Spain Healthcare Cyber Security Market By End User

11.3.3.11 Netherlands

11.3.3.11.1 Netherlands Healthcare Cyber Security Market By Component

11.3.3.11.2 Netherlands Healthcare Cyber Security Market By Security Type

11.3.3.11.3 Netherlands Healthcare Cyber Security Market By Deployment

11.3.3.11.4 Netherlands Healthcare Cyber Security Market By End User

11.3.3.12 Switzerland

11.3.3.12.1 Switzerland Healthcare Cyber Security Market By Component

11.3.3.12.2 Switzerland Healthcare Cyber Security Market By Security Type

11.3.3.12.3 Switzerland Healthcare Cyber Security Market By Deployment

11.3.3.12.4 Switzerland Healthcare Cyber Security Market By End User

11.3.3.13 Austria

11.3.3.13.1 Austria Healthcare Cyber Security Market By Component

11.3.3.13.2 Austria Healthcare Cyber Security Market By Security Type

11.3.3.13.3 Austria Healthcare Cyber Security Market By Deployment

11.3.3.13.4 Austria Healthcare Cyber Security Market By End User

11.3.3.14 Rest of Western Europe

11.3.3.14.1 Rest of Western Europe Healthcare Cyber Security Market By Component

11.3.3.14.2 Rest of Western Europe Healthcare Cyber Security Market By Security Type

11.3.3.14.3 Rest of Western Europe Healthcare Cyber Security Market By Deployment

11.3.3.14.4 Rest of Western Europe Healthcare Cyber Security Market By End User

11.4 Asia-Pacific

11.4.1 Trend Analysis

11.4.2 Asia-Pacific Healthcare Cyber Security Market by Country

11.4.3 Asia-Pacific Healthcare Cyber Security Market By Component

11.4.4 Asia-Pacific Healthcare Cyber Security Market By Security Type

11.4.5 Asia-Pacific Healthcare Cyber Security Market By Deployment

11.4.6 Asia-Pacific Healthcare Cyber Security Market By End User

11.4.7 China

11.4.7.1 China Healthcare Cyber Security Market By Component

11.4.7.2 China Healthcare Cyber Security Market By Security Type

11.4.7.3 China Healthcare Cyber Security Market By Deployment

11.4.7.4 China Healthcare Cyber Security Market By End User

11.4.8 India

11.4.8.1 India Healthcare Cyber Security Market By Component

11.4.8.2 India Healthcare Cyber Security Market By Security Type

11.4.8.3 India Healthcare Cyber Security Market By Deployment

11.4.8.4 India Healthcare Cyber Security Market By End User

11.4.9 Japan

11.4.9.1 Japan Healthcare Cyber Security Market By Component

11.4.9.2 Japan Healthcare Cyber Security Market By Security Type

11.4.9.3 Japan Healthcare Cyber Security Market By Deployment

11.4.9.4 Japan Healthcare Cyber Security Market By End User

11.4.10 South Korea

11.4.10.1 South Korea Healthcare Cyber Security Market By Component

11.4.10.2 South Korea Healthcare Cyber Security Market By Security Type

11.4.10.3 South Korea Healthcare Cyber Security Market By Deployment

11.4.10.4 South Korea Healthcare Cyber Security Market By End User

11.4.11 Vietnam

11.4.11.1 Vietnam Healthcare Cyber Security Market By Component

11.4.11.2 Vietnam Healthcare Cyber Security Market By Security Type

11.4.11.3 Vietnam Healthcare Cyber Security Market By Deployment

11.4.11.4 Vietnam Healthcare Cyber Security Market By End User

11.4.12 Singapore

11.4.12.1 Singapore Healthcare Cyber Security Market By Component

11.4.12.2 Singapore Healthcare Cyber Security Market By Security Type

11.4.12.3 Singapore Healthcare Cyber Security Market By Deployment

11.4.12.4 Singapore Healthcare Cyber Security Market By End User

11.4.13 Australia

11.4.13.1 Australia Healthcare Cyber Security Market By Component

11.4.13.2 Australia Healthcare Cyber Security Market By Security Type

11.4.13.3 Australia Healthcare Cyber Security Market By Deployment

11.4.13.4 Australia Healthcare Cyber Security Market By End User

11.4.14 Rest of Asia-Pacific

11.4.14.1 Rest of Asia-Pacific Healthcare Cyber Security Market By Component

11.4.14.2 Rest of Asia-Pacific Healthcare Cyber Security Market By Security Type

11.4.14.3 Rest of Asia-Pacific Healthcare Cyber Security Market By Deployment

11.4.14.4 Rest of Asia-Pacific Healthcare Cyber Security Market By End User

11.5 Middle East & Africa

11.5.1 Trend Analysis

11.5.2 Middle East

11.5.2.1 Middle East Healthcare Cyber Security Market by Country

11.5.2.2 Middle East Healthcare Cyber Security Market By Component

11.5.2.3 Middle East Healthcare Cyber Security Market By Security Type

11.5.2.4 Middle East Healthcare Cyber Security Market By Deployment

11.5.2.5 Middle East Healthcare Cyber Security Market By End User

11.5.2.6 UAE

11.5.2.6.1 UAE Healthcare Cyber Security Market By Component

11.5.2.6.2 UAE Healthcare Cyber Security Market By Security Type

11.5.2.6.3 UAE Healthcare Cyber Security Market By Deployment

11.5.2.6.4 UAE Healthcare Cyber Security Market By End User

11.5.2.7 Egypt

11.5.2.7.1 Egypt Healthcare Cyber Security Market By Component

11.5.2.7.2 Egypt Healthcare Cyber Security Market By Security Type

11.5.2.7.3 Egypt Healthcare Cyber Security Market By Deployment

11.5.2.7.4 Egypt Healthcare Cyber Security Market By End User

11.5.2.8 Saudi Arabia

11.5.2.8.1 Saudi Arabia Healthcare Cyber Security Market By Component

11.5.2.8.2 Saudi Arabia Healthcare Cyber Security Market By Security Type

11.5.2.8.3 Saudi Arabia Healthcare Cyber Security Market By Deployment

11.5.2.8.4 Saudi Arabia Healthcare Cyber Security Market By End User

11.5.2.9 Qatar

11.5.2.9.1 Qatar Healthcare Cyber Security Market By Component

11.5.2.9.2 Qatar Healthcare Cyber Security Market By Security Type

11.5.2.9.3 Qatar Healthcare Cyber Security Market By Deployment

11.5.2.9.4 Qatar Healthcare Cyber Security Market By End User

11.5.2.10 Rest of Middle East

11.5.2.10.1 Rest of Middle East Healthcare Cyber Security Market By Component

11.5.2.10.2 Rest of Middle East Healthcare Cyber Security Market By Security Type

11.5.2.10.3 Rest of Middle East Healthcare Cyber Security Market By Deployment

11.5.2.10.4 Rest of Middle East Healthcare Cyber Security Market By End User

11.5.3 Africa

11.5.3.1 Africa Healthcare Cyber Security Market by Country

11.5.3.2 Africa Healthcare Cyber Security Market By Component

11.5.3.3 Africa Healthcare Cyber Security Market By Security Type

11.5.3.4 Africa Healthcare Cyber Security Market By Deployment

11.5.3.5 Africa Healthcare Cyber Security Market By End User

11.5.3.6 Nigeria

11.5.3.6.1 Nigeria Healthcare Cyber Security Market By Component

11.5.3.6.2 Nigeria Healthcare Cyber Security Market By Security Type

11.5.3.6.3 Nigeria Healthcare Cyber Security Market By Deployment

11.5.3.6.4 Nigeria Healthcare Cyber Security Market By End User

11.5.3.7 South Africa

11.5.3.7.1 South Africa Healthcare Cyber Security Market By Component

11.5.3.7.2 South Africa Healthcare Cyber Security Market By Security Type

11.5.3.7.3 South Africa Healthcare Cyber Security Market By Deployment

11.5.3.7.4 South Africa Healthcare Cyber Security Market By End User

11.5.3.8 Rest of Africa

11.5.3.8.1 Rest of Africa Healthcare Cyber Security Market By Component

11.5.3.8.2 Rest of Africa Healthcare Cyber Security Market By Security Type

11.5.3.8.3 Rest of Africa Healthcare Cyber Security Market By Deployment

11.5.3.8.4 Rest of Africa Healthcare Cyber Security Market By End User

11.6 Latin America

11.6.1 Trend Analysis

11.6.2 Latin America Healthcare Cyber Security Market by Country

11.6.3 Latin America Healthcare Cyber Security Market By Component

11.6.4 Latin America Healthcare Cyber Security Market By Security Type

11.6.5 Latin America Healthcare Cyber Security Market By Deployment

11.6.6 Latin America Healthcare Cyber Security Market By End User

11.6.7 Brazil

11.6.7.1 Brazil Healthcare Cyber Security Market By Component

11.6.7.2 Brazil Healthcare Cyber Security Market By Security Type

11.6.7.3 Brazil Healthcare Cyber Security Market By Deployment

11.6.7.4 Brazil Healthcare Cyber Security Market By End User

11.6.8 Argentina

11.6.8.1 Argentina Healthcare Cyber Security Market By Component

11.6.8.2 Argentina Healthcare Cyber Security Market By Security Type

11.6.8.3 Argentina Healthcare Cyber Security Market By Deployment

11.6.8.4 Argentina Healthcare Cyber Security Market By End User

11.6.9 Colombia

11.6.9.1 Colombia Healthcare Cyber Security Market By Component

11.6.9.2 Colombia Healthcare Cyber Security Market By Security Type

11.6.9.3 Colombia Healthcare Cyber Security Market By Deployment

11.6.9.4 Colombia Healthcare Cyber Security Market By End User

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Healthcare Cyber Security Market By Component

11.6.10.2 Rest of Latin America Healthcare Cyber Security Market By Security Type

11.6.10.3 Rest of Latin America Healthcare Cyber Security Market By Deployment

11.6.10.4 Rest of Latin America Healthcare Cyber Security Market By End User

12. Company Profiles

12.1 Northrop Grumma Corporation

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 The SNS View

12.2 Palo Alto Networks, Inc.,

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 The SNS View

12.3 Sensato investors

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 The SNS View

12.4 Symantec Corporation

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 The SNS View

12.5 Cisco Systems, Inc.,

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 The SNS View

12.6 FireEye, Inc.,

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 The SNS View

12.7 IBM Corporation

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 The SNS View

12.8 Kaspersky Lab

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 The SNS View

12.9 Lockheed Martin Corporation

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 The SNS View

12.10 MACAFEE, INC.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. Use Case and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Vendor Risk Management Market was valued at USD 8.6 billion in 2023 and is expected to reach USD 30.3 billion by 2032, growing at a CAGR of 14.98% from 2024-2032.

The Wireless Testing Market was valued at USD 15.2 Billion in 2023 and is expected to reach USD 45.0 Billion by 2032, growing at a CAGR of 12.83% by 2032.

Data Center Networking Market was worth USD 27.37 billion in 2023 and is predicted to be worth USD 76.87 billion by 2032, growing at a CAGR of 12.19% between 2024 and 2032.

The Student Information System Market was valued at USD 10.73 billion in 2023 and is expected to reach USD 48.08 billion by 2032, growing at a CAGR of 18.18% over the forecast period 2024-2032.

Customer Information System Market was valued at USD 1.26 billion in 2023 and is expected to reach USD 3.54 billion by 2032, growing at a CAGR of 12.23% from 2024-2032

The Smart Enterprise Market was valued at USD 0.32 billion in 2023 and is expected to reach USD 0.99 billion by 2032, growing at a CAGR of 13.44% by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd