Get E-PDF Sample Report on Green Building Materials Market - Request Sample Report

The Green Building Materials Market size was USD 371.25 billion in 2023 and is expected to Reach USD 1020.53 billion by 2032 and grow at a CAGR of 11.89% over the forecast period of 2024-2032.

The Green Building Materials market is experiencing significant growth as the demand for sustainable construction practices increases. These materials, derived from renewable resources such as bamboo, wood, hempcrete, mycelium, and recycled plastic, offer an eco-friendlier alternative to traditional building products. Green building materials are gaining traction due to heightened awareness of the environmental consequences of conventional construction materials. Manufacturing, transportation, and disposal of traditional building materials contribute significantly to carbon emissions and environmental degradation. In contrast, green materials reduce the carbon footprint and mitigate global warming effects. Products such as green insulation boards, timbercrete, green roofs, and wooden houses are increasingly being adopted, demonstrating their relevance in the modern construction landscape.

The push for sustainability is also being bolstered by governmental and corporate initiatives. The U.S. Department of Energy is funding early-stage carbon capture and storage (CCS) projects, while China’s large-scale carbon trading market is expected to cover 40% of global CO2 emissions by 2023. These efforts reflect a broader commitment to reducing carbon footprints, which in turn boosts the demand for eco-friendly building materials. Furthermore, a significant portion of Fortune 500 companies have set ambitious carbon reduction goals, further emphasizing the market’s momentum. As green building materials continue to evolve, they offer long-term benefits in terms of cost-efficiency and environmental sustainability, making them a growing preference for environmentally conscious construction projects.

DRIVERS

The green building material market is experiencing significant growth, driven by heightened environmental awareness and sustainability concerns. As climate change and the environmental impact of construction come to the forefront, both consumers and businesses are increasingly prioritizing eco-friendly solutions. Green building materials help reduce carbon footprints, promote energy efficiency, and support sustainable construction practices. This shift in consumer behavior is further fueled by the growing desire to minimize environmental harm, lower energy costs, and meet sustainability goals. Additionally, regulatory frameworks and green building certifications, such as LEED, are encouraging the adoption of these materials in both residential and commercial construction projects. The market is expected to expand as more builders, developers, and architects integrate sustainable practices into their designs. This trend aligns with the global movement towards reducing environmental impact and fostering long-term energy savings, making green building materials a key element of the evolving construction landscape.

RESTRAINT

The high initial cost of green building materials is a significant barrier to their widespread adoption. These materials, such as energy-efficient windows, sustainable insulation, and eco-friendly flooring, typically come at a premium compared to traditional options. While they offer long-term savings through energy efficiency, reduced maintenance, and lower operational costs, the upfront investment can be a deterrent for builders and property developers, especially for those working with tight budgets or looking for immediate returns. Many developers may prioritize cost-effective solutions in the short term, overlooking the long-term financial and environmental benefits that green materials offer. This financial hesitation can be particularly pronounced in markets where green construction practices are not yet the norm, making it harder to justify the initial investment. Despite these challenges, as awareness grows and demand for sustainable buildings increases, the cost of green materials is expected to decrease, driving broader adoption.

BY APPLICATION

The Roofing segment dominated with the market share over 32% in 2023, due to the growing preference for sustainable roofing solutions. As concerns about energy efficiency, environmental impact, and building longevity increase, eco-friendly roofing options have gained significant traction. Cool roofs, which reflect sunlight and reduce heat absorption, help lower building temperatures, decreasing energy consumption for cooling. Additionally, the integration of solar panels in roofing systems enables buildings to generate renewable energy, further contributing to sustainability goals. These roofing materials not only reduce environmental footprints but also enhance the overall durability of structures by providing weather resistance and improved insulation. The rising adoption of such solutions in both new constructions and retrofitting projects reflects a shift toward environmentally conscious building practices.

BY END USER

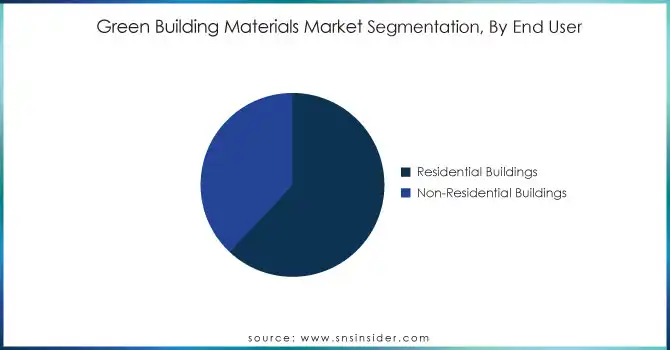

The Residential Buildings segment dominated with the market share over 62% in 2023, due to a surge in consumer demand for eco-friendly homes and energy-efficient solutions. As awareness of environmental issues rises, homeowners and developers are increasingly prioritizing sustainability in construction. In developed markets, such as North America and Europe, the adoption of green building materials is particularly prominent. These materials, such as energy-efficient windows, insulation, and sustainable flooring, help reduce the carbon footprint of homes, lower energy costs, and improve indoor air quality. Additionally, there is growing recognition of the long-term benefits of green buildings, including reduced maintenance costs and enhanced comfort for occupants. Homebuyers are increasingly seeking properties with environmentally conscious features, driven by both ethical considerations and financial incentives such as tax rebates and lower utility bills.

North America region dominated with the market share over 38% in 2023. The region benefits from stringent environmental regulations and numerous government incentives aimed at promoting sustainability in construction. Both the U.S. and Canada have been at the forefront of adopting energy-efficient materials, such as insulated concrete forms, green roofs, and sustainable insulation, due to a growing emphasis on reducing carbon footprints and energy consumption. Additionally, increasing demand for eco-friendly buildings from commercial, residential, and institutional sectors has further propelled market growth. Governments have introduced various initiatives like tax credits, rebates, and grants to encourage the use of green materials in construction, strengthening the region's position.

Asia-Pacific is witnessing rapid growth in the Green Building Materials Market, driven by the region’s accelerated urbanization and booming construction activities. Countries such as China, India, and Japan are focusing on developing sustainable infrastructure to support their expanding urban populations. The adoption of green building materials is further encouraged by government policies and regulations aimed at reducing carbon emissions and promoting energy-efficient construction practices. In addition to governmental support, the rising awareness of environmental issues among consumers and developers has significantly contributed to the demand for eco-friendly building materials. The push for energy-efficient buildings, improved indoor air quality, and the reduction of resource consumption are key drivers in this region's transition to greener construction methods.

Get Customized Report as Per Your Business Requirement - Request For Customized Report

Some of the major key players of the Green Building Materials Market

Suppliers for (Sustainable building solutions like energy-efficient windows, energy-efficient insulation, coatings, sealants) of Green Building Materials Market

RECENT DEVELOPMENT

In April 18, 2024: Armstrong World Industries has launched Ultima LEC ceiling panels, made from 54% recycled content, offering a 43% reduction in embodied carbon. The use of sustainably sourced wood-generated biochar supports the company’s commitment to sustainable building products and aligns with growing demand for low-carbon solutions in construction.

In November 7, 2024: DuPont has launched Tyvek with Renewable Attribution, a sustainable healthcare packaging solution that reduces carbon footprint by replacing fossil fuel feedstocks with certified bio-circular materials. This innovation aligns with the growing demand for eco-friendly solutions in the green building market, supporting sustainability goals while maintaining Tyvek superior performance.

In 2023 Holcim: Holcim launched ECOCycle, a technology platform designed to transform recycled demolition materials into new building solutions. Using ECOCycle, Holcim can recycle 100% of construction and demolition waste, starting with decarbonized raw materials for low-carbon cement formulations.

In 2023 Holcim: Holcim acquired PASA, a global leader in innovation, sustainability, and quality, which enhances Holcim's roofing and waterproofing portfolio and expands its regional business presence.

| Report Attributes | Details |

| Market Size in 2023 | USD 371.25 billion |

| Market Size by 2032 | USD 1020.53 billion |

| CAGR | CAGR of 11.89% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Interior Product, Exterior Products, Solar Products, Building Systems, Other) • By Application (Roofing, Framing, Insulation, Exterior Sliding, Interior Finishing) • By End User (Residential Buildings, Non-Residential Buildings) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF, DuPont, Holcim, Kingspan Group, Green Building Solutions, Lhoist, Lafarge, Kingspan Group plc, RedBuilt LLC, Binderholz GmbH, Alumasc Group Plc, Bauder Limited, PPG Industries, CertainTeed Corporation, Interface, Inc., Saint-Gobain, Armstrong World Industries, Tata Steel, USG Corporation, CSR Limited. |

| Key Drivers | • The green building material market is growing rapidly as environmental awareness and sustainability concerns drive the demand for eco-friendly solutions, energy efficiency, and regulatory compliance in construction. |

| RESTRAINTS | • The high initial cost of green building materials, despite offering long-term savings, deters builders and developers from adopting them, particularly in markets where sustainability is not yet prioritized. |

Ans: North America dominated the Green Building Materials Market in 2023.

Ans: The “Roofing” segment dominated the Green Building Materials Market.

Ans. The green building material market is growing rapidly as environmental awareness and sustainability concerns drive the demand for eco-friendly solutions, energy efficiency, and regulatory compliance in construction.

Ans: The Green Building Materials Market was USD 371.25 billion in 2023 and is expected to Reach USD 1020.53 billion by 2032.

Ans: The Green Building Materials Market is expected to grow at a CAGR of 11.89% during 2024-2032.

TABLE OF CONTENTS:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics

4.1 Market Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Production Capacity and Utilization, by Country, By Type, 2023

5.2 Feedstock Prices, by Country, By Type, 2023

5.3 Regulatory Impact, by Country, By Type, 2023

5.4 Environmental Metrics: Emissions Data, Waste Management Practices, and Sustainability Initiatives, by Region

5.5 Innovation and R&D, By Type, 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Green Building Materials Market Segmentation, By Product Type

7.1 Chapter Overview

7.2 Interior Product

7.1 Interior Product Market Trends Analysis (2020-2032)

7.2 Interior Product Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Exterior Products

7.3.1 Exterior Products Market Trends Analysis (2020-2032)

7.3.2 Exterior Products Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Solar Products

7.4.1 Solar Products Market Trends Analysis (2020-2032)

7.4.2 Solar Products Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Building Systems

7.4.1 Building Systems Market Trends Analysis (2020-2032)

7.4.2 Building Systems Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Other

7.4.1 Other Market Trends Analysis (2020-2032)

7.4.2 Other Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Green Building Materials Market Segmentation, By Application

8.1 Chapter Overview

8.2 Roofing

8.2.1 Roofing Market Trends Analysis (2020-2032)

8.2.2 Roofing Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Framing

8.3.1 Framing Market Trends Analysis (2020-2032)

8.3.2 Framing Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Insulation

8.4.1 Insulation Market Trends Analysis (2020-2032)

8.4.2 Insulation Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Exterior Sliding

8.5.1 Exterior Sliding Market Trends Analysis (2020-2032)

8.5.2 Exterior Sliding Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Interior Finishing

8.6.1 Interior Finishing Market Trends Analysis (2020-2032)

8.6.2 Interior Finishing Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Green Building Materials Market Segmentation, By End User

9.1 Chapter Overview

9.2 Residential Buildings

9.2.1 Residential Buildings Market Trends Analysis (2020-2032)

9.2.2 Residential Buildings Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Non-Residential Buildings

9.3.1 Non-Residential Buildings Market Trends Analysis (2020-2032)

9.3.2 Non-Residential Buildings Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Green Building Materials Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.2.4 North America Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.5 North America Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.2.6.2 USA Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.6.3 USA Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.2.7.2 Canada Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.7.3 Canada Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.2.8.2 Mexico Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.8.3 Mexico Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Green Building Materials Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.1.6.2 Poland Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.6.3 Poland Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.1.7.2 Romania Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.7.3 Romania Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Green Building Materials Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.4 Western Europe Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.5 Western Europe Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.6.2 Germany Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.6.3 Germany Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.7.2 France Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.7.3 France Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.8.2 UK Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.8.3 UK Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.9.2 Italy Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.9.3 Italy Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.10.2 Spain Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.10.3 Spain Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.13.2 Austria Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.13.3 Austria Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4 Asia-Pacific

10.4.1 Trends Analysis

10.4.2 Asia-Pacific Green Building Materials Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia-Pacific Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.4 Asia-Pacific Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.5 Asia-Pacific Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.6.2 China Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.6.3 China Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.7.2 India Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.7.3 India Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.8.2 Japan Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.8.3 Japan Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.9.2 South Korea Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.9.3 South Korea Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.10.2 Vietnam Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.10.3 Vietnam Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.11.2 Singapore Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.11.3 Singapore Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.12.2 Australia Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.12.3 Australia Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.4.13 Rest of Asia-Pacific

10.4.13.1 Rest of Asia-Pacific Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia-Pacific Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia-Pacific Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Green Building Materials Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.1.4 Middle East Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.5 Middle East Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.1.6.2 UAE Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.6.3 UAE Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Green Building Materials Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.2.4 Africa Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.5 Africa Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Green Building Materials Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.6.4 Latin America Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.5 Latin America Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.6.6.2 Brazil Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.6.3 Brazil Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.6.7.2 Argentina Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.7.3 Argentina Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.6.8.2 Colombia Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.8.3 Colombia Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Green Building Materials Market Estimates and Forecasts, By Products Type (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Green Building Materials Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Green Building Materials Market Estimates and Forecasts, By End-User (2020-2032) (USD Billion)

11. Company Profiles

11.1 BASF

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 DuPont

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Holcim

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Kingspan Group

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 green building solutions

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 Lhoist

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Lafarge

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Kingspan Group plc

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 RedBuilt LLC

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Binderholz GmbH

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Product Type

Interior Product

Exterior Products

Solar Products

Building Systems

Other

By Application

Roofing

Framing

Insulation

Exterior Sliding

Interior Finishing

By End User

Residential Buildings

Non-Residential Buildings

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Biodegradable Films Market size was USD 1.3 billion in 2023 and is expected to reach USD 2.3 billion by 2032, growing at a CAGR of 6.7% from 2024 to 2032.

Iron Ore Market size was valued at USD 309.7 billion in 2023 and is expected to reach USD 392.4 billion by 2032, growing at a CAGR of 2.7% from 2024 to 2032.

The propylene glycol market size was valued at USD 4.12 billion in 2023 and is expected to reach USD 6.59 billion by 2032 and grow at a CAGR of 5.38% over the forecast period 2024-2032.

The Hydrophilic Coating Market Size was valued at USD 16.59 Billion in 2023 and is expected to reach USD 27.23 Billion by 2032, growing at a CAGR of 5.66% over the forecast period of 2024-2032.

The Cold Flow Improver Market size was USD 812.49 Million in 2023 and is expected to reach USD 1348.74 Million by 2032, at a CAGR of 5.79 % from 2024-2032.

Tow Prepreg Market Size was valued at USD 534.6 million in 2023 and is expected to reach USD 1526.0 million by 2032 and grow at a CAGR of 12.4% from 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd