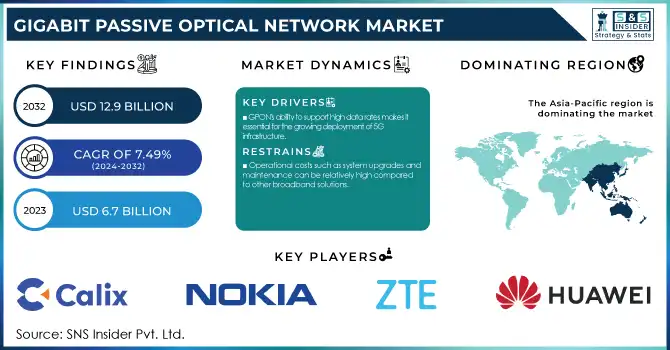

The Gigabit Passive Optical Network Market was valued at USD 6.7 Billion in 2023 and is expected to reach USD 12.9 Million by 2032, growing at a CAGR of 7.49% from 2024-2032.

To get more information on Gigabit Passive Optical Network Market - Request Free Sample Report

The adoption of emerging technologies such as AI-driven network optimization and software-defined GPON solutions is accelerating the market's expansion. Regional network infrastructure investments vary, with Asia-Pacific leading due to rapid urbanization and fiber deployment initiatives. Cybersecurity incidents affecting GPON networks have increased, driving demand for enhanced encryption and authentication measures, while cloud services integration is rising, enabling seamless remote network management. The report consists of sustainability initiatives in GPON deployment, AI-driven network automation, the impact of 5G backhaul on GPON demand, and regulatory policies shaping fiber-optic network expansion.

Drivers

GPON's ability to support high data rates makes it essential for the growing deployment of 5G infrastructure.

The Gigabit Passive Optical Network is set to play an integral part in 5G infrastructure deployments thanks to G-PON's ability to deliver high data speeds, scaling ability, and cost-effectiveness. In particular, GPON with a max of 2.5 Gbps downstream and a maximum of 1.25 Gbps upstream is bandwidth available for 5G that would make it capable of well able to support the types of high-bandwidth applications characteristic of augmented reality, virtual reality, Internet of Things devices, and low-latency real-time communication between 5G BS and the core network.

GPON was designed with point-to-multipoint architecture, making it ideal for 5G small cell dense deployments, drastically reducing 5G backhaul costs and traditional backhauling system complexity. Moreover, GPON networks are extremely scalable and can be evolved to address higher speed needs via XGS-PON or NG-PON2 enabling speeds of 10 Gbps or more and GPON is crafted to be future-ready to meet 5G consumption and delivery challenges. Besides the obvious performance benefits, GPON has the added advantage of being energy-efficient compared to other broadband technologies, thus meeting the sustainability goals of the telecom operators while reducing operational costs. This energy efficiency makes it an ideal solution for deploying 5G infrastructure most efficiently and cost-effectively, particularly in large-scale connectivity applications.

|

Gigabit Passive Optical Network Features |

Benefits of 5G |

|

High Bandwidth |

Supports data-intensive 5G applications like IoT, AR, and VR. |

|

Symmetrical Data Speeds |

Ensures low latency for real-time applications. |

|

Scalability |

Can be upgraded to XGS-PON or NG-PON2 for future 5G needs. |

|

Energy Efficiency |

Minimizes power consumption, supporting sustainable network expansion. |

Restraints

Operational costs such as system upgrades and maintenance can be relatively high compared to other broadband solutions.

Gigabit Passive Optical Networks are widely regarded as cost-effective in the long run, but they come with substantial ongoing operational expenses, especially when compared to alternative broadband technologies. A key factor driving these costs is the need for regular system upgrades and maintenance, which require specialized skills and expensive equipment. In contrast to traditional copper broadband, GPON relies on fiber-optic infrastructure that demands careful installation, continuous monitoring, and frequent maintenance to ensure high-quality performance. As technology evolves, upgrading GPON networks is essential, particularly with the rollout of faster standards like XGS-PON and NG-PON2, which can handle speeds greater than 10 Gbps. These upgrades often involve replacing outdated components, leading to additional costs for telecom providers. Moreover, fiber-optic networks are more susceptible to physical damage from environmental conditions or construction activities, which necessitates ongoing maintenance to prevent service disruptions. The shortage of skilled technicians trained in fiber-optic installation and GPON-specific technologies is another challenge that raises operational costs.

Opportunity

The increasing need for high-speed internet across residential, commercial, and industrial sectors is driving the demand for GPON technology.

Growing demand for GPON technology can be attributed to its increased need for high-speed internet in residential, commercial, and industrial sectors. Until now, fiber-optic networks are likely to be one of the important infrastructures for increasing smart cities and IoT applications and actually expanding 5G deployment. GPON provides higher bandwidth, more scalability, and low-cost fiber to the home solutions that appeal to telecom operators and ISPs. Fiber, and massive investments geared towards the construction of broadband infrastructure by the government, for its part, are opening up wide opportunities for both GPON solutions providers and network operators across the globe.

Challenge

The high capital investment required for fiber deployment and network upgrades poses a challenge for widespread GPON adoption.

The initial investment to deploy fiber and network infrastructure for GPON technology is high, which is a barrier to GPON technology adoption. No wonder, laying fiber-optic cables is a complex process that requires significant investment, a skilled workforce & regulatory approval which makes it a time-consuming affair primarily in underdeveloped regions. Also, it takes a lot of time and money to update the older technology of copper networks to fiber. Market adoption will also be hampered because the price may be a burden for honest operators, especially SMEs and rural operators. Overcoming costs through government subsidies and innovative financing models will be key for the widespread deployment of GPON.

By Component

The product segment dominated the Market and represented a significant revenue share of 60% in 2023, aiding in the deployment of high-speed infrastructure for broadband. It comprises vital hardware components required for the operable consumption of GPON systems, including optical line terminals (OLTs), optical network units (ONUs), and crucial components like optical splitters. The high-speed internet driven by video streaming, remote work, telemedicine, and other bandwidth-intensive applications has generated a significant demand for these goods. And, the continuous movement towards faster speeds and wider area coverage, particularly in underdeveloped areas, also helps to amplify the demand for GPON products. The demand is only expected to grow as telecom operators transition towards an XGS-PON solution that delivers greater than 10 Gbps speeds.

The service segment of the GPON market is expected to register the fastest compound annual growth rate during the forecast period, Due to the increasing need for installation, maintenance, and optimization services, the Telecom providers are adding new GPON infrastructure in the field, but the addition of this equipment increases the complexity of system deployment, and the move away from GPON to higher-speed technologies such as XGS-PON creates a demand for specialized services such as network management, troubleshooting, and continual hardware and software upgrades. This need for solution is further expedited with the expansion of GPON networks, both in urban and rural areas. Also, the growing dependence on GPON for the 5G backhaul solution promotes the growth of this market.

By Application

The Fiber To The Home segment dominated the market and represented a significant revenue share of 46% in 2023. owing to the rising need for high-speed internet worldwide for business and domestic applications. FTTH technology provides dedicated fiber-optic connections directly to homes or businesses, enabling improved speed and reliability in Internet access over broadband solutions previously available. As more and more bandwidth-hungry services come to the fore over the Internet — including video streaming, online gaming, and remote work — FTTH can play an integral role in the digital infrastructure. Moreover, FTTH networks are driven by government-led programs for boosting broadband access inclusion, especially in neglected areas.

The mobile backhaul segment is expected to witness the highest compound annual growth rate in the GPON market, owing to the rapid deployment of 5G networks. Mobile backhaul is the connectivity between mobile base stations and the core network and is a key enabler for the migration to high-speed mobile services. The sharp uptick in mobile data traffic, especially created by IoT, AR, and VR, means mobile backhaul infrastructure now requires high-capacity solutions such as GPON. The increase in 5G subscriptions will drive the demand for mobile backhaul services, which will make this segment one of the fastest-growing parts of the market.

By Technology

The 2.5 GPON segment dominated the market and accounted for the largest market share owing to its extensive utilization in fiber-to-the-home and fibre-to-the-building applications. Costs are stable, performance unstable and so is the 2.5 GPON which is still being used by many of the telecom operators and the ISPs when we talk about Gigabit-speed broadband. Even with the new technology developments, 2.5 GPON is still extremely common for home and small-business broadband connections. Nonetheless, the rapid growth in high-bandwidth and super-high-speed Internet demand is likely to spark an uptick in next-gen GPON deployment shortly.

NG-PON2 is expected to experience the fastest CAGR growth. With capabilities of 40Gpbs, this technology is suited for enterprise and smart city applications, allowing the delivery of multi-gigabit broadband services to consumers by service providers. NG-PON2 is gaining traction with the increasing deployment of 5G networks, cloud computing and other high-bandwidth applications.

By End-Use

The IT & Telecom segment dominated the market and captured the largest market share in 2023. Due to the increasing demand for high-speed internet and network reliability from telecom operators and data centers, The accelerated growth of 5G networks, cloud services, and data-hungry applications has facilitated the deployment of GPON in this area. Telecoms are continuously updating their infrastructure to accommodate the increased data traffic and make sure that connectivity never breaks down.

Healthcare is projected to have the fastest CAGR because there is an increasing need for high-speed secure data transfer in hospitals, clinics, and research institutions. As telemedicine, digital health records, and AI-driven diagnostics become commonplace, healthcare facilities will need their broadband infrastructure to be turbocharged to manage the massive throughput of data from an increasingly high patient turnover.

Regional Analysis

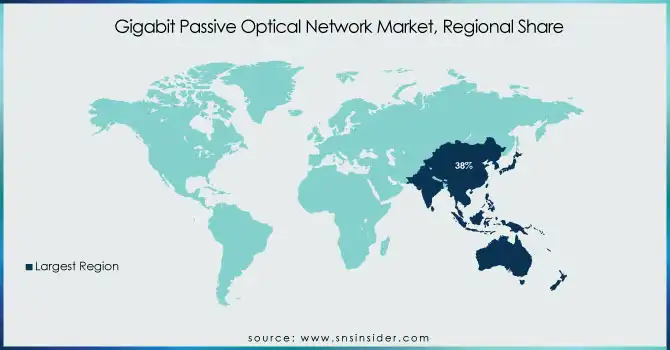

In 2023, Asia-Pacific dominated the market and represented a significant revenue share of 38%, growing due to the rising demand for high-speed internet in the APAC region, along with government initiatives to support broadband penetration. China, India, Japan, and South Korea are at the forefront of implementing FTTH and GPON infrastructure, removing barriers that have had in providing high-speed services to urban and rural areas. Governments are focused on expanding broadband access to citizens—for example, India has started BharatNet—but nothing can reach the scale of incumbents who are pouring money into building these networks.

North America is expected to register the highest CAGR during the forecast period, Owing to the uninterrupted deployment of fiber-optic networks across the region as well as the introduction of 5G infrastructure. With both the public and private sector news focused on next-generation broadband technologies, the U.S. and Canada are investing heavily in new technologies to improve overall internet speeds and coverage. With the rise in remote working, telemedicine, and e-learning, the need for high-speed internet services is driving the adoption of GPON systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key players

The major key players along with their products are

Huawei Technologies – MA5800 GPON OLT

ZTE Corporation – ZXA10 C300 GPON OLT

Nokia Corporation – 7360 ISAM FX GPON

FiberHome Telecommunication Technologies Co. Ltd. – AN6000 GPON OLT

Calix Inc. – GigaCenter GPON

Cisco Systems, Inc. – ASR 9000 Series Aggregation Services Routers

Palo Alto Networks, Inc. – GPON Security Gateway

Adtran, Inc. – Total Access 5000 GPON OLT

Juniper Networks, Inc. – MX Series 3D Universal Edge Routers (GPON support)

Vertiv Co. – Liebert EXM2 (used in GPON backhaul)

Tellabs, Inc. – Tellabs 8600 GPON Series

Mitsubishi Electric Corporation – MELCO GPON OLT

Samsung Electronics Co., Ltd. – Samsung GPON OLT

Marconi Communications Ltd. – GPON OLT Systems

NEC Corporation – GPON OLT solutions

Prysmian Group – Fiber Optic Cables for GPON networks

Dasan Zhone Solutions – GX Series GPON OLT

Arris International – E6000 CER (GPON support)

Tatung Company – GPON ONU (Optical Network Units)

AFL Telecommunications – GPON Network Solutions

Recent Developments

January 2024 – Huawei has advanced its XGS-PON solutions to support higher bandwidth demands for smart city initiatives and broadband expansions

February 2024 – Calix introduced innovations focused on scaling GPON deployments and improving fiber-to-the-home (FTTH) services for underserved areas

|

Report Attributes |

Details |

|

Market Size in 2023 |

USD 6.7 Billion |

|

Market Size by 2032 |

USD 12.9 Billion |

|

CAGR |

CAGR of 7.49% From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Component (Product, Service) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Huawei Technologies, ZTE Corporation, Nokia Corporation, FiberHome Telecommunication Technologies Co. Ltd., Calix Inc., Cisco Systems, Inc., Palo Alto Networks, Inc., Adtran, Inc., Juniper Networks, Inc., Vertiv Co., Tellabs, Inc., Mitsubishi Electric Corporation, Samsung Electronics Co., Ltd., Marconi Communications Ltd., NEC Corporation, Prysmian Group, Dasan Zhone Solutions, Arris International, Tatung Company, AFL Telecommunications |

Ans: - The deployment of GPON infrastructure requires significant upfront capital investment, including costs for fiber optic cables, equipment, and installation, which can be a barrier for smaller service providers and emerging markets.

Ans: -

The increasing global need for ultra-fast and reliable internet connectivity, driven by data-intensive activities like streaming, remote work, and online education.

Ans: - Asia Pacific dominated the market and represented a significant revenue share in 2023

Ans: - The CAGR of the Gigabit Passive Optical Network Market during the forecast period is 7.49% from 2024-2032.

Ans: - Gigabit Passive Optical Network Market was valued at USD 6.7 Billion in 2023 and is expected to reach USD 12.9 Million by 2032, growing at a CAGR of 7.49% from 2024-2032.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates of Emerging Technologies

5.2 Network Infrastructure Expansion, by Region

5.3 Cybersecurity Incidents, by Region (2020-2023)

5.4 Cloud Services Usage, by Region

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Gigabit Passive Optical Network Market Segmentation, by Component

7.1 Chapter Overview

7.2Product

7.2.1 Product Market Trends Analysis (2020-2032)

7.2.2 Product Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.3 Optical Line Terminal (OLT)

7.2.3.1 Optical Line Terminal (OLT) Market Trends Analysis (2020-2032)

7.2.3.2 Optical Line Terminal (OLT) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.4 Optical Network Terminal (ONT)

7.2.4.1 Optical Network Terminal (ONT) Market Trends Analysis (2020-2032)

7.2.4.2 Optical Network Terminal (ONT) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3Services

7.3.1Services Market Trends Analysis (2020-2032)

7.3.2Services Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3.3 Professional service

7.3.3.1Professional service Market Trends Analysis (2020-2032)

7.3.3.2Professional service Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3.4 Managed service

7.3.4.1Managed service Market Trends Analysis (2020-2032)

7.3.4.2Managed service Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Gigabit Passive Optical Network Market Segmentation, by Technology

8.1 Chapter Overview

8.2 2.5 GPON

8.2.1 2.5 GPON Market Trends Analysis (2020-2032)

8.2.2 2.5 GPON Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 XG-PON

8.3.1 XG-PON Market Trends Analysis (2020-2032)

8.3.2 XG-PON Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 XGS-PON

8.4.1 XGS-PON Market Trends Analysis (2020-2032)

8.4.2 XGS-PON Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 NG-PON2

8.5.1 NG-PON2 Market Trends Analysis (2020-2032)

8.5.2 NG-PON2 Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Gigabit Passive Optical Network Market Segmentation, by Application

9.1 Chapter Overview

9.2 Fiber To The Home (FTTH)

9.2.1 Fiber To The Home (FTTH) Market Trends Analysis (2020-2032)

9.2.2 Fiber To The Home (FTTH) Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Mobile backhaul

9.3.1 Mobile backhaul Market Trends Analysis (2020-2032)

9.3.2 Mobile backhaul Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Other FTTX

9.4.1 Other FTTX Market Trends Analysis (2020-2032)

9.4.2 Other FTTX Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Gigabit Passive Optical Network Market Segmentation, by End-Use

10.1 Chapter Overview

10.2 BFSI

10.2.1 BFSI Market Trends Analysis (2020-2032)

10.2.2 BFSI Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Retail

10.3.1 Retail Market Trends Analysis (2020-2032)

10.3.2 Retail Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 IT & Telecom

10.4.1 IT & Telecom Market Trends Analysis (2020-2032)

10.4.2 IT & Telecom Market Size Estimates and Forecasts to 2032 (USD Billion)

10.5 Healthcare

10.5.1 Healthcare Market Trends Analysis (2020-2032)

10.5.2 Healthcare Market Size Estimates and Forecasts to 2032 (USD Billion)

10.6 Government

10.6.1 Government Market Trends Analysis (2020-2032)

10.6.2 Government Market Size Estimates and Forecasts to 2032 (USD Billion)

10.7 Others

10.7.1 Others Market Trends Analysis (2020-2032)

10.7.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Gigabit Passive Optical Network Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.2.4 North America Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.5 North America Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.6 North America Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.2.7.2 USA Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.7.3 USA Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.7.4 USA Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.2.8.2 Canada Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.8.3 Canada Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.8.4 Canada Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.2.9.2 Mexico Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.2.9.3 Mexico Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.9.4 Mexico Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.7.2 Poland Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.7.3 Poland Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.7.4 Poland Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.8.2 Romania Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.8.3 Romania Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.8.4 Romania Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.4 Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.5 Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.6 Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.7.2 Germany Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.7.3 Germany Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.7.4 Germany Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.8.2 France Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.8.3 France Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.8.4 France Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.9.2 UK Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.9.3 UK Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.9.4 UK Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.10.2 Italy Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.10.3 Italy Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.10.4 Italy Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.11.2 Spain Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.11.3 Spain Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.11.4 Spain Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.14.2 Austria Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.14.3 Austria Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.14.4 Austria Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.4 Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.5 Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.6 Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.7.2 China Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.7.3 China Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.7.4 China Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.8.2 India Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.8.3 India Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.8.4 India Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.9.2 Japan Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.9.3 Japan Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.9.4 Japan Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.10.2 South Korea Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.10.3 South Korea Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.10.4 South Korea Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.11.2 Vietnam Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.11.3 Vietnam Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.11.4 Vietnam Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.12.2 Singapore Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.12.3 Singapore Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.12.4 Singapore Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.13.2 Australia Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.13.3 Australia Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.13.4 Australia Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.4 Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.5 Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.6 Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.7.2 UAE Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.7.3 UAE Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.7.4 UAE Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2.4 Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.5 Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.6 Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.4 Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.5 Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.6 Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.7.2 Brazil Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.7.3 Brazil Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.7.4 Brazil Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.8.2 Argentina Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.8.3 Argentina Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.8.4 Argentina Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.9.2 Colombia Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.9.3 Colombia Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.9.4 Colombia Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Gigabit Passive Optical Network Market Estimates and Forecasts, by End-Use (2020-2032) (USD Billion)

12. Company Profiles

12.1 Huawei Technologies

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 ZTE Corporation

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Nokia Corporation

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 FiberHome Telecommunication Technologies Co. Ltd.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Calix Inc.

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Cisco Systems, Inc.

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Palo Alto Networks, Inc.

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Adtran, Inc.

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Juniper Networks, Inc

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Vertiv Co

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Component

Product

Optical Line Terminal (OLT)

Optical Network Terminal (ONT)

Others

Service

Professional service

Managed service

By Technology

2.5 GPON

XG-PON

XGS-PON

NG-PON2

By Application

Fiber To The Home (FTTH)

Other FTTX

Mobile backhaul

By End-Use

Retail

IT & Telecom

BFSI

Healthcare

Government

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Data Loss Prevention (DLP) Solutions market size was valued at US$ 2.29 Bn in 2023 and is expected to reach USD 13.66 Bn by 2032 and grow at a CAGR of 21.95 % over the forecast period 2024-2032.

The Payment Processing Solutions Market size was valued at USD 52.1 billion in 2023 and will grow to USD 139.7 billion by 2032 and grow at a CAGR of 11.6 % by 2032.

The Case Management Market Size was valued at USD 7.89 Billion in 2023 and is expected to reach USD 17.43 Billion by 2032 and grow at a CAGR of 9.32% by 2032.

Digital Printing Market was worth USD 33.07 billion in 2023 and is predicted to be worth USD 70.48 billion by 2032, growing at a CAGR of 8.79% between 2024 and 2032.

The Quality Management Software (QMS) Market was valued at USD 9.6 billion in 2023 and is expected to reach USD 24.0 billion & CAGR of 10.70% by 2032.

The Artificial Neural Network Market size was valued at USD 248 million in 2023 and is expected to reach USD 1256 million by 2032, growing at a CAGR of 19.79% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd