Get more information on Geographic Atrophy (GA) Market - Request Sample Report

The Geographic Atrophy (GA) Market Size was valued at USD 23.7 Billion in 2023 and is expected to reach USD 50.0 Billion by 2032 and grow at a CAGR of 8.6% over the forecast period 2024-2032.

Robust Growth in the Geographic Atrophy Market Driven by Aging Population and Technological Advances

Heightened Focus on R&D and Novel Therapies Propel Market Expansion

The Geographic Atrophy (GA) market is experiencing robust growth, fueled by several dynamic factors. Geographic atrophy, a severe form of age-related macular degeneration (AMD), poses a significant global health challenge. According to the American Academy of Ophthalmology, over 8 million people worldwide suffer from GA, which constitutes approximately 20% of all AMD cases. The prevalence of GA is anticipated to rise due to the expanding geriatric population, which is more vulnerable to age-related diseases. The increasing age burden in developed nations amplifies the need for effective GA treatments, driving market growth.

A major catalyst for market expansion is the heightened focus on research and development (R&D) by pharmaceutical and biopharmaceutical companies. These entities are investing heavily in innovative therapies to address GA, spurred by the growing incidence of the condition and the urgent need for effective treatment options. Recent advancements in healthcare technology and novel drug development are accelerating market growth. Despite these advancements, the market faces challenges, including limited awareness about GA and disappointing outcomes from some investigational drugs. These challenges have occasionally hindered market progress, yet ongoing R&D and increased health awareness are expected to address these gaps and drive growth.

| Category | Key Drivers/Opportunities | Expected Impact (2024–2032) | Remarks |

|---|---|---|---|

| Aging Population | Increasing global geriatric population | High: Boosting demand for GA therapies | Rising AMD prevalence among elderly |

| FDA Approvals | Approval of novel treatments like IZERVAY | High: Accelerates access to advanced treatments | Improves patient outcomes and treatment reach |

| R&D Investment | Increased focus on research and innovative therapies | Moderate-High: Supports development of new drugs | Leading to breakthrough therapies |

| Gene Therapy Advancements | Innovations in gene and stem cell therapies | High: Potential for disease-modifying solutions | Emerging field with long-term potential |

| Growing Healthcare Awareness | Improved awareness & early diagnosis | Moderate: Enhances early-stage detection | Leads to timely intervention and better management |

| Healthcare Infrastructure | Expansion of healthcare systems in emerging markets | Moderate-High: Expands treatment access globally | Key regions: Asia-Pacific, Latin America |

| Collaborations & Partnerships | Global pharma collaborations on clinical trials | High: Strengthens drug development pipelines | Facilitates faster innovation |

A significant recent development is the FDA's approval of IZERVAY (avacincaptad pegol intravitreal solution) in August 2023. This novel complement C5 inhibitor, developed by Astellas Pharma Inc., has shown promising results in clinical trials. The GATHER1 and GATHER2 Phase 3 trials, assessing the safety and efficacy of monthly 2 mg intravitreal administration of IZERVAY, demonstrated a statistically significant reduction in GA progression. Patients receiving IZERVAY exhibited a slower GA growth rate compared to those receiving sham treatment, marking a milestone in the treatment of this debilitating condition. This approval underscores the market's potential for new and effective therapies, with regulatory bodies playing a crucial role in facilitating development. The market also benefits from rising health awareness and growing healthcare infrastructure globally. As healthcare systems expand and awareness about GA increases, the demand for effective treatments is expected to rise. The growth rate reflects the increased focus on developing novel therapies and the growing incidence of GA due to an aging population. Overall, the geographic atrophy treatment market is poised for substantial growth, driven by increased disease prevalence, advancements in treatment options, and significant R&D investments. The recent FDA approval of IZERVAY highlights the market's potential for new therapies, while regional dynamics and healthcare advancements continue to shape its trajectory.

| Company | Product/Drug | Innovation/Technology | Positive Impact on GA Market |

|---|---|---|---|

| Iveric Bio | Zimura (avacincaptad pegol) | Complement C5 inhibitor targeting GA | FDA approval demonstrates effectiveness in slowing GA progression |

| Apellis Pharmaceuticals | Pegcetacoplan (Syfovre) | Inhibition of complement protein C3 | Approved as a new treatment for slowing GA progression |

| Alkeus Pharmaceuticals | ALK-001 | Vitamin A deuterium-based therapy to protect retinal cells | Innovative approach reduces toxicity, preserving visual function |

| Gyroscope Therapeutics | GT005 | Gene therapy for complement system regulation | Potential long-term impact on preventing GA progression |

| Stealth BioTherapeutics | Elamipretide | Mitochondria-targeted therapy to protect photoreceptors | First-of-its-kind therapy aimed at cellular energy restoration |

| NGM Biopharmaceuticals | NGM621 | Anti-complement C3 monoclonal antibody | Promising results in targeting complement pathways to slow GA |

| Astellas Pharma | IZERVAY (avacincaptad pegol) | Complement C5 inhibitor | Statistically significant reduction in GA progression in clinical trials |

| Ocugen | OCU410 | Modifier gene therapy for GA | Innovative gene therapy addressing underlying causes of GA |

| Annexon Biosciences | ANX007 | Complement C1q inhibitor targeting early stages of GA | First drug to target complement component C1q in GA |

Market Dynamics

Drivers

Surging Demand for Geographic Atrophy Treatments Driven by Aging Population and Technological Advances

The geographic atrophy (GA) market is witnessing significant growth due to several key drivers. One primary factor fueling market expansion is the rising prevalence of age-related macular degeneration (AMD), the leading cause of GA. As the global population ages, the incidence of AMD and consequently GA is increasing, creating a higher demand for effective treatments. Advances in medical research and technology are also driving market growth. The development of novel therapies, including gene therapies, stem cell treatments, and targeted drug delivery systems, offers hope for more effective GA management. Increased investment in R&D by pharmaceutical companies and healthcare organizations is accelerating innovation in treatment options.

Furthermore, growing awareness and early diagnosis of GA contribute to market growth. Improved diagnostic tools and increased screening programs help identify GA earlier, allowing for timely intervention and treatment. The expansion of healthcare infrastructure and advanced medical facilities in emerging markets also contribute to market growth. Additionally, rising healthcare expenditure and favorable reimbursement policies in various regions support patient access to innovative treatments. The convergence of these factors creates a robust environment for the geographic atrophy treatment market, driving the development of new therapies and the expansion of existing treatment options.

Restraints

High Costs of Novel Therapies Restrict Patient Access and Widespread Adoption

A significant challenge is the high cost associated with novel therapies and advanced treatments, which limits patient access and can be a barrier to widespread adoption. Additionally, the complexity and prolonged development timelines of cutting-edge treatments, such as gene and stem cell therapies, contribute to delays in market availability. Regulatory hurdles and stringent approval processes further complicate the introduction of innovative treatments. A lack of awareness and understanding of GA among the general population and some healthcare providers can lead to underdiagnosis and delayed treatment. These factors collectively constrain the growth potential of the GA treatment market, despite the overall positive outlook.

By Age Group

In the Geographic Atrophy (GA) market, segmentation by age group reveals that individuals aged 75 years and older dominate the market. This segment held the largest market share in 2023 with a 54.7% share due to the higher prevalence of geographic atrophy in this age group, driven primarily by age-related factors. According to the Retina Study Group of Portugal, geographic atrophy affects 1.3% of adults aged 75 to 84, with prevalence increasing to approximately 22% by the age of 90. This trend underscores the significant market potential within the older age bracket. The segment of individuals aged 75 and older is not only the largest but also the fastest-growing segment in the GA market, reflecting the growing need for targeted treatments for this demographic. In a notable development, Iveric Bio's investigational drug, avacincaptad pegol (ACP), also known as Zimura, received the Breakthrough Therapy designation from the U.S. Food and Drug Administration (FDA) in November 2021. This novel complement C5 inhibitor is specifically designed for the treatment of geographic atrophy secondary to age-related macular degeneration (AMD), highlighting the market's focus on advanced treatments for this high-prevalence age group.

By Diagnosis

In the Geographic Atrophy (GA) market, segmentation by diagnostic methods reveals that optical coherence tomography angiography (OCT-A) is the dominant and fastest-growing segment. In 2023, OCT-A led the market with 38.6% due to its advanced, non-invasive technology that offers detailed imaging of the retina's and choroid's microvasculature. This capability makes OCT-A essential for diagnosing and understanding various retinal conditions, including geographic atrophy, diabetic retinopathy, and both dry and wet age-related macular degeneration. The technology’s growing importance is reflected in its projected rapid expansion through 2030. OCT-A’s ability to provide high-resolution images and its utility in monitoring disease progression are key factors driving its market dominance. For instance, the AngioVue OCTA system from Optovue, Inc. (US) exemplifies how OCT-A technology is utilized to enhance diagnostic precision and patient care in retinal disorders.

By Therapeutic Agents

In the Geographic Atrophy (GA) market, the segmentation by clinical development stage includes late-stage (Phase III), Phase II, Phase I, and pre-clinical stage & discovery candidates. The late-stage (Phase III) segment was the market leader in 2023 with 34.5% and is anticipated to be the fastest-growing segment from 2024 to 2032. This growth is driven by the pivotal role of Phase III clinical trials, which assess whether new treatments or drug combinations are more effective or comparable to existing therapies. For example, Galderma Laboratories LP (US) is conducting Phase III trials of an anti-inflammatory doxycycline for GA treatment. Additionally, Apellis Pharmaceuticals, Inc. (US) reported promising results from its Phase III trial for APL-2 Therapy in September 2021 and planned to submit a new drug application to the FDA in early 2022. The increasing number of late-stage clinical trials is a significant factor contributing to the expansion of this segment in the GA market.

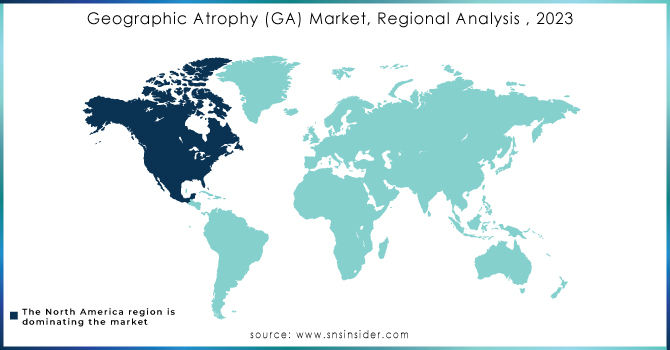

Regional Analysis

North America, particularly the United States, held the largest share 43.6% of the Geographic Atrophy (GA) market in 2023 and is expected to maintain its dominance through the forecast period of 2024-2032. The region's leadership is attributed to the high prevalence of geographic atrophy, significant investments in healthcare infrastructure, and robust R&D activities. The FDA’s approval of innovative treatments, such as the Phase III trials for APL-2 Therapy by Apellis Pharmaceuticals, further fuels market growth. Additionally, the presence of leading pharmaceutical companies and advanced healthcare systems enhances North America's market position.

The Asia-Pacific region is emerging as a rapidly growing market for geographic atrophy treatments. The region’s growth is fueled by increasing healthcare awareness, expanding healthcare infrastructure, and rising prevalence of age-related diseases. Countries such as China and Japan are leading in market expansion due to their large geriatric populations and significant investments in healthcare technology. The presence of local pharmaceutical companies and increasing collaborations with global firms contribute to the region's rapid market development.

Need any customization research on Geographic Atrophy (GA) Market - Enquiry Now

Iveric Bio (Zimura (avacincaptad pegol))

Alkeus Pharmaceuticals, Inc. (ALK-001)

Apellis Pharmaceuticals, Inc. (APL-2)

Genentech, Inc. (OpRegen)

Stealth BioTherapeutics (Elamipretide)

Allegro Ophthalmics, LLC (Risuteganib)

Gyroscope Therapeutics Limited (GT005)

Regenerative Patch Technologies, LLC (CPCB-RPE1)

NGM Biopharmaceuticals Inc. (NGM621)

Novartis (PPY988)

Perceive Biotherapeutics, Inc. (VOY-101)

Annexon, Inc. (ANX007)

Aviceda Therapeutics (AVD-104)

Ionis Pharmaceuticals, Inc. (IONIS-FB-LRx)

Astellas Pharma Inc. (ASP7317), and others.

Recent Developments

In April 2024, Ocugen completed dosing for Cohort 2 of the Phase 1/2 Arcellx study on their novel therapy for GA.

In July 2024, the National Eye Institute announced a new research initiative to explore gene therapy options for geographic atrophy.

In August 2024, Apellis Pharmaceuticals reported successful results from their Phase III clinical trial of APL-2, advancing toward potential FDA approval.

In September 2024, Iveric Bio received FDA approval for Zimura, a complement C5 inhibitor, marking a significant milestone in GA treatment.

February 2023: Pegcetacoplan (Syfovre) received approval as a new treatment for dry AMD, which can progress to geographic atrophy and cause vision loss. This newly approved medication aims to slow disease progression.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 23.7 Billion |

| Market Size by 2032 | US$ 50.0 billion |

| CAGR | CAGR of 8.6% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Age Group (Above 60 Years, Above 75 Years) • By Diagnosis (Fundus Autofluorescence (FAF), Optical Coherence Tomography Angiography (OCT-A), Multifocal Electroretinography (mfERG)) • By Therapeutic Agents (Late-stage (Phase III), Phase II, Phase I, Pre-clinical stage & Discovery candidates) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Iveric Bio, Alkeus Pharmaceuticals, Inc., Apellis Pharmaceuticals, Inc., Hemera Biosciences LLC, Genentech, Inc., F. Hoffmann-La Roche AG, Stealth BioTherapeutics, Allegro Ophthalmics, LLC, Gensight Biologics SA, Gyroscope Therapeutics Limited, Regenerative Patch Technologies, LLC, NGM Biopharmaceuticals Inc., Novartis, Perceive Biotherapeutics, Inc., Annexon, Inc., Aviceda Therapeutics, Astellas Pharma Inc and others. |

| Key Drivers | • Surging Demand for Geographic Atrophy Treatments Driven by Aging Population and Technological Advances |

| Restraints | • High Costs of Novel Therapies Restrict Patient Access and Widespread Adoption |

Ans: The Geographic Atrophy (GA) Market is growing at a CAGR of 8.6% over the forecast period 2024-2032.

Ans. Geographic atrophy, a severe form of age-related macular degeneration (AMD), causes the macula to continuously deteriorate over time.

Ans. Surging Demand for Geographic Atrophy Treatments Driven by Aging Population and Technological Advances.

Ans. Above 60 Years, and Above 75 Years are the sub segments of Geographic Atrophy (GA) market.

Ans. The geographic atrophy industry's value chain analysis is divided into four main sections that start with R&D and product creation, go through manufacture, distribution, and post-marketing surveillance.

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023)

5.2 Prescription Trends, (2023), by Region

5.3 Drug Volume: Production and usage volumes of pharmaceuticals.

5.4 Healthcare Spending: Expenditure data by government, insurers, and out-of-pocket by patients.

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new Product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Geographic Atrophy (GA) Market Segmentation, by Age Group

7.1 Chapter Overview

7.2 Above 60 Years

7.2.1 Above 60 Years Market Trends Analysis (2020-2032)

7.2.2 Above 60 Years Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Above 75 Years

7.3.1 Above 75 Years Market Trends Analysis (2020-2032)

7.3.2 Above 75 Years Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Geographic Atrophy (GA) Market Segmentation, by Diagnosis

8.1 Chapter Overview

8.2 Fundus Autofluorescence (FAF)

8.2.1 Fundus Autofluorescence (FAF) Market Trends Analysis (2020-2032)

8.2.2 Fundus Autofluorescence (FAF) Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Optical Coherence Tomography Angiography (OCT-A)

8.3.1 Optical Coherence Tomography Angiography (OCT-A) Market Trends Analysis (2020-2032)

8.3.2 Optical Coherence Tomography Angiography (OCT-A) Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 Multifocal Electroretinography (mfERG)

8.4.1 Multifocal Electroretinography (mfERG) Market Trends Analysis (2020-2032)

8.4.2 Multifocal Electroretinography (mfERG) Market Size Estimates and Forecasts to 2032 (USD Million)

9. Geographic Atrophy (GA) Market Segmentation, by Therapeutic Agents

9.1 Chapter Overview

9.2 Late-stage (Phase III)

9.2.1 Late-stage (Phase III) Market Trends Analysis (2020-2032)

9.2.2 Late-stage (Phase III) Market Size Estimates and Forecasts to 2032 (USD Million)

9.3 Phase II

9.3.1 Phase II Market Trends Analysis (2020-2032)

9.3.2 Phase II Market Size Estimates and Forecasts to 2032 (USD Million)

9.4 Phase I

9.4.1 Phase I Market Trends Analysis (2020-2032)

9.4.2 Phase I Market Size Estimates and Forecasts to 2032 (USD Million)

9.5 Pre-clinical stage & Discovery candidates

9.5.1 Pre-clinical stage & Discovery candidates Market Trends Analysis (2020-2032)

9.5.2 Pre-clinical stage & Discovery candidates Market Size Estimates and Forecasts to 2032 (USD Million)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Geographic Atrophy (GA) Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.2.3 North America Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.2.4 North America Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.2.5 North America Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.2.6 USA

10.2.6.1 USA Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.2.6.2 USA Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.2.6.3 USA Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.2.7 Canada

10.2.7.1 Canada Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.2.7.2 Canada Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.2.7.3 Canada Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.2.8 Mexico

10.2.8.1 Mexico Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.2.8.2 Mexico Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.2.8.3 Mexico Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.1.3 Eastern Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.1.4 Eastern Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.1.5 Eastern Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.1.6 Poland

10.3.1.6.1 Poland Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.1.6.2 Poland Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.1.6.3 Poland Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.1.7 Romania

10.3.1.7.1 Romania Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.1.7.2 Romania Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.1.7.3 Romania Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.1.8.2 Hungary Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.1.8.3 Hungary Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.1.9 turkey

10.3.1.9.1 Turkey Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.1.9.2 Turkey Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.1.9.3 Turkey Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.1.10.2 Rest of Eastern Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.1.10.3 Rest of Eastern Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.2.3 Western Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.4 Western Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.5 Western Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.6 Germany

10.3.2.6.1 Germany Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.6.2 Germany Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.6.3 Germany Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.7 France

10.3.2.7.1 France Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.7.2 France Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.7.3 France Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.8 UK

10.3.2.8.1 UK Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.8.2 UK Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.8.3 UK Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.9 Italy

10.3.2.9.1 Italy Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.9.2 Italy Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.9.3 Italy Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.10 Spain

10.3.2.10.1 Spain Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.10.2 Spain Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.10.3 Spain Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.11.2 Netherlands Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.11.3 Netherlands Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.12.2 Switzerland Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.12.3 Switzerland Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.13 Austria

10.3.2.13.1 Austria Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.13.2 Austria Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.13.3 Austria Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.3.2.14.2 Rest of Western Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.3.2.14.3 Rest of Western Europe Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Geographic Atrophy (GA) Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.4.3 Asia Pacific Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.4 Asia Pacific Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.5 Asia Pacific Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.6 China

10.4.6.1 China Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.6.2 China Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.6.3 China Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.7 India

10.4.7.1 India Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.7.2 India Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.7.3 India Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.8 Japan

10.4.8.1 Japan Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.8.2 Japan Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.8.3 Japan Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.9 South Korea

10.4.9.1 South Korea Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.9.2 South Korea Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.9.3 South Korea Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.10 Vietnam

10.4.10.1 Vietnam Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.10.2 Vietnam Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.10.3 Vietnam Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.11 Singapore

10.4.11.1 Singapore Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.11.2 Singapore Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.11.3 Singapore Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.12 Australia

10.4.12.1 Australia Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.12.2 Australia Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.12.3 Australia Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.4.13.2 Rest of Asia Pacific Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.4.13.3 Rest of Asia Pacific Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Geographic Atrophy (GA) Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.1.3 Middle East Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.1.4 Middle East Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.1.5 Middle East Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.1.6 UAE

10.5.1.6.1 UAE Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.1.6.2 UAE Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.1.6.3 UAE Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.1.7.2 Egypt Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.1.7.3 Egypt Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.1.8.2 Saudi Arabia Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.1.8.3 Saudi Arabia Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.1.9.2 Qatar Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.1.9.3 Qatar Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.1.10.2 Rest of Middle East Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.1.10.3 Rest of Middle East Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.2.3 Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.2.4 Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.2.5 Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.2.6.2 South Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.2.6.3 South Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.2.7.2 Nigeria Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.2.7.3 Nigeria Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.5.2.8.2 Rest of Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.5.2.8.3 Rest of Africa Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Geographic Atrophy (GA) Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.6.3 Latin America Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.6.4 Latin America Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.6.5 Latin America Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.6.6 Brazil

10.6.6.1 Brazil Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.6.6.2 Brazil Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.6.6.3 Brazil Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.6.7 Argentina

10.6.7.1 Argentina Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.6.7.2 Argentina Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.6.7.3 Argentina Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.6.8 Colombia

10.6.8.1 Colombia Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.6.8.2 Colombia Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.6.8.3 Colombia Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Geographic Atrophy (GA) Market Estimates and Forecasts, by Age Group (2020-2032) (USD Million)

10.6.9.2 Rest of Latin America Geographic Atrophy (GA) Market Estimates and Forecasts, by Diagnosis (2020-2032) (USD Million)

10.6.9.3 Rest of Latin America Geographic Atrophy (GA) Market Estimates and Forecasts, by Therapeutic Agents (2020-2032) (USD Million)

11. Company Profiles

11.1 Iveric Bio

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 Alkeus Pharmaceuticals, Inc.

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Apellis Pharmaceuticals, Inc.

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Hemera Biosciences LLC

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Genentech, Inc.

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 F. Hoffmann-La Roche AG

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Stealth BioTherapeutics

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Allegro Ophthalmics, LLC

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Gensight Biologics SA

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Gyroscope Therapeutics Limited

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segmentation

By Age Group

Above 60 Years

Above 75 Years

By Diagnosis

Fundus Autofluorescence (FAF)

Optical Coherence Tomography Angiography (OCT-A)

Multifocal Electroretinography (mfERG)

By Therapeutic Agents

Late-stage (Phase III)

Phase II

Phase I

Pre-clinical stage & Discovery candidates

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Medical Aesthetics market size was USD 19.28 billion in 2023 and is expected to reach USD 56.41 billion by 2032 and grow at a CAGR of 12.67% over the forecast period of 2024-2032.

The Blood Pressure Cuffs Market size was valued at USD 192.81 Million in 2023 and is expected to reach USD 355.00 Million by 2032 and grow at a CAGR of 7.04% over the forecast period 2024-2032.

The Neuroendoscopy Devices Market was valued at USD 358.13 million in 2023 and is expected to reach USD 890.14 million by 2032, growing at a CAGR of 10.66% over the forecast period of 2024-2032.

The Cancer Stem Cells Market Size was USD 4.06 billion in 2023 and is expected to reach USD 8.41 billion by 2032, growing at a CAGR of 8.43% by 2024-2032.

Veterinary CRO and CDMO Market was valued at USD 6.23 billion in 2023 and is expected to reach USD 13.3. billion by 2032, growing at a CAGR of 8.84% over the forecast period of 2024-2032.

The Trypsin Market was valued at USD 90.31 million in 2023 and is expected to reach USD 147.46 million by 2032, growing at a CAGR of 5.62% from 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd