The eye care services market size was valued at USD 156.28 billion in 2024 and is expected to reach USD 328.72 billion by 2032, growing at a CAGR of 9.81% over the forecast period of 2025-2032.

The global eye care services market has been witnessing rapid growth owing to the increasing prevalence of vision disorders globally, including refractive errors, cataracts, and age-related macular degeneration. This can be attributed to the rising geriatric population, increasing screen time, and heightened awareness regarding eye health, which is resulting in the increased demand for routine eye check-ups, surgical procedures, and preventive care. Increasing access to specialized services in urban and rural populations, supported by technological advancements in diagnostics and treatment, continues to propel the market growth, especially in developed and emerging economies.

The U.S. eye care services market size was valued at USD 47.55 billion in 2024 and is expected to reach USD 97.69 billion by 2032, growing at a CAGR of 9.48% over the forecast period of 2025-2032.

The North American eye care services market is predominantly driven by the U.S., with advanced healthcare infrastructure, high awareness regarding vision health, and high availability of specialized eye care professionals. It is also a leader in new surgical technology and performs cataract and LASIK procedures in volume regularly.

Perfluorohexyloctane (Miebo/Evotears) was approved in the U.S. in 2023 and represents a growing class of novel preservative-free dry eye treatments.

In April 2024, the FDA cleared an autonomous handheld camera by AEYE Health. It allows for no-human-in-the-loop, highly accurate (sensitivity 92–93%) diabetic retinopathy screening in primary care, and can therefore augment accessibility.

Drivers:

Increasing Prevalence of Vision Problems Aids the Market Growth

The global prevalence of vision disorders is one of the key drivers of the eye care services market. As the global population continues to age, the incidence of various medical conditions, for instance, refractive errors (myopia, hyperopia, astigmatism), cataract, glaucoma, diabetic retinopathy, and age-related macular degeneration (AMD), is reported to be increasing. Moreover, owing to lifestyle diseases, such as diabetes and hypertension, vision complications also include retinal diseases. The increasing number of people experiencing vision loss or at risk of it has created an urgent need for early diagnosis, regular monitoring, and timely intervention, making both public and private eye-caring services a massive eye care services market growth.

More than 2.2 billion people around the world experience vision impairment or blindness, according to the World Health Organization (WHO), the leading causes include refractive errors, cataracts, and retinal diseases.

Technological Advancements in Diagnosis and Treatment are Accelerating the Market Growth

Ophthalmic technology is rapidly advancing, which is changing the delivery of eye care services market trends. Real-time high-resolution imaging of ocular structures, such as in OCT and fundus cameras, provides the means for earlier and more precise diagnosis of retinal and optic nerve illnesses. Advancements in surgery, including laser-assisted cataract surgery, femtosecond laser technology, and minimally invasive glaucoma surgeries (MIGS), allow for safer and quicker recovery times. In addition, the new vision stage of Industries' global enablement within Teleophthalmology, and helping enhance access to specialist care, especially in areas where this is notably lacking or in rural areas, and opening up a wider scope of appeal for eye care services globally.

FDA cleared in May 2024, Notal Vision's SCANLY Home OCT is the basis for remote self-monitoring of retinal health by patients, particularly those with neovascular AMD (nAMD), and automated AI diagnostics help reduce clinic visits and increase precision medicine.

Restraints:

Market Restraints Due to High Cost of Advanced Treatments & Diagnostic Equipment

The high cost of advanced diagnostic devices and surgical procedures is one of the key restraining factors in the eye care services market analysis. Innovative technologies, including Optical Coherence Tomography (OCT), femtosecond lasers, intraoperative aberrometry, and Artificial Intelligence-powered screening systems, are necessary for the timely and accurate identification of eye diseases. Nevertheless, the startup costs of high-quality healthcare, along with keeping such devices, are great and likely beyond the capacity of small clinics or healthcare providers located in developing areas of the world.

Moreover, LASIK, premium cataract surgery with advanced IOLs, or MIGS are also costly surgical alternatives for the patient, especially in the absence of complete insurance coverage. In many instances, they are not defined by specialty guidelines as medically necessary, thus are not covered by insurance, so their availability is restricted to the population with disposable cash, a privilege mostly unattainable by people in low- and middle-income countries. Hence, the growth potential of the market will be limited due to cost-based disparities in access to contemporary eye care.

By Service Type

The surgical interventions segment dominated the eye care services market with a 42.8% market share in 2024, owing to significant demand for cataract surgeries, LASIK, and glaucoma treatment. Age-related vision disorders, especially cataracts, which are amongst the most common causes of blindness worldwide, are increasing in both the developed and developing world, given the growing elderly population. Procedural improvements in surgery, such as those involving femtosecond lasers, minimally invasive and intraocular lenses, have improved postoperative results and time to recovery. This increase in access to specialized ophthalmic surgical centers and other enabling developments has cemented the leadership of this segment.

The primary care services segment is anticipated to gain the fastest growth in the forecast years because of greater awareness concerning preventive eye care and the early detection of vision defects. While digital eye strain, dry eye, and refractive errors have become more common, growing expenses for routine eye programs imply that more people are searching for the help of professionals when such issues occur. The increasing availability and affordability of primary eye care in community clinics, optical chains, and retail health stores has also contributed to this trend. This growth is driven by things, such as the increase of all these things in emerging markets.

By Indication

In 2024, the refractive errors segment accounted for the largest share with a 40.11% market share, owing to the high prevalence of myopia, hyperopia, astigmatism, and presbyopia globally. The growth is also driven by lifestyle-related hazards, such as too much screen time and less time outdoors, which can cause vision problems in people of all ages, especially children and young adults. There are a variety of ways to correct vision, including eyeglasses, contact lenses, and refractive surgeries. Diagnosis and treatment are easy and commonplace. Apart from this, early diagnosis and treatment have also balanced out the segment growth, owing to routine checking of vision across the schools and workplaces.

Glaucoma is estimated to be the fastest-growing segment in the forecast years, owing to the increasing prevalence of this condition, especially among the elderly and also among patients with a chronic disease, such as diabetes and hypertension. Glaucoma is referred to as the silent thief of sight, as it usually develops slowly and damages eyesight. If untreated, it can lead to vision loss. Increased awareness, better screening methods (optical coherence tomography), and surgical and drug therapies are prompting more patients to seek treatment.

By Provider Type

In the 2024 eye care services market, the standalone eye clinics segment held the largest market share of 36.12% due to their concentrated nature of the services provided for comprehensive vision care, diagnosis and medical management, and surgical services. Staffed by experienced ophthalmologists and optometrists, these clinics offer focused services that cover everything from routine eye exams to advanced treatments for cataracts, glaucoma, and refractive errors. For such patients who either need preventive or corrective eye care, the personalized care, shorter wait times, and continuity of services offered by these practices make them the preferred option. In addition, the fact that specialized eye hospitals are equipped with the needed infrastructure and advanced diagnostic tools further solidifies their status as a tertiary center for eye care.

Optical retail chains with eye care services segment are anticipated to experience the highest growth on account of the growing presence of affordability and convenience. Long relegated to the basement of malls and urban retail strips, these chains are adding an element of optometry into the mix, including vision testing, prescriptions, and even corrective lenses, all in one trip. This creates an appeal for consumers who prefer an eyecare option that is highly accessible and time-efficient. This segment is anticipated to see rapid growth globally in both developed and emerging markets, driven by increasing demand for routine examination, particularly among younger, millennial, and Gen Z populations who are comfortable with technology, and strategic collaborations between retail chains and certified eye care professionals.

The eye care services market in North America accounted for the largest market share with 41.05% market share in 2024, owing to well-established healthcare infrastructure, high per capita healthcare expenditure, and the presence of leading eye care providers and institutions. Advanced, emerging diagnostic and surgical technologies differentiate the region, such as femtosecond lasers and point of care, AI-based imaging, with these technologies integrated as a standard of care into many clinical practices. Furthermore, periodic eye examinations among the geriatric population and public awareness initiatives promote the early identification and treatment of eye diseases, such as cataracts, glaucoma, and macular degeneration, thereby supporting its dominance in the regional market.

In April 2025, Alcon’s Voyager DSLT, a contactless, frequency-doubled Nd:YAG laser, is commercially available in the U.S. Works without gonioscopy to streamline early glaucoma treatment, enabling the innovation of an efficient, precise trabeculoplasty.

The eye care services market in Asia Pacific is growing at a fast pace with a 10.63% CAGR as Asia Pacific has a large population of older people, which is going to grow rapidly in the coming years, together with the increasing prevalence of vision problems and great accessibility to health care components and services. The high demand for vision testing, surgeries, and optical services can be attributed to the rising rate of urbanization, an increase in awareness toward eye wellbeing, and government initiatives to minimize avoidable blindness. China, India, and South Korea are advancing in eye care with the support of public and private infrastructure, while digital and teleophthalmology adapting solutions have widened the reach in underserved rural areas, which is propelling growth in the region.

Substantial growth of the eye care services market in Europe is driven by a strong presence of various public healthcare systems across countries, a large geriatric population, and a high prevalence of chronic eye diseases, viz. glaucoma, cataract, and diabetic retinopathy. Due to the early adoption of advanced diagnostic technologies, surgical procedures, and established referral schemes, the region has benefited from extremely short symptomatic-to-treatment times.

Additionally, the increasing need for regular vision care due to a rising ageing population and the use of electronic devices is propelling the uptake of services. The growing importance of Europe in the global eye care services market will be augmented by the concerted efforts of the government to ensure preventive eye care and vision rehabilitation, and the presence of prominent ophthalmology centers in countries, such as Germany, the U.K., and France.

The market is significantly growing due to the rise in visual disorders such as cataracts, glaucoma, and refractive errors in the region of Latin America. Increasing usage of digital devices and growing disposable income are boosting the market for eye care services. Telemedicine and vision screening programs such as Operation Miracle have also expanded access to diagnostic and surgical care.

The increase in healthcare investments, the rising incidences of age-related eye diseases (ISS, AMD, and dry eye), and increasing diagnosis capabilities in countries, such as Saudi Arabia, UAE, and South Africa are supporting the MEA region's growth. Expanding penetration of private eye-care providers and use of new diagnostic technologies such as meibomian gland expression, and the use of OCT scanners are increasing treatment capacity. However, imbalances in access between rural and underserved areas and a shortage of specialists in some nations still restrict growth speed.

The major players operating in the market are Alcon, Johnson & Johnson Vision Care, Bausch & Lomb Incorporated, Carl Zeiss Meditec AG, EssilorLuxottica, CooperVision, HOYA Corporation, Rayner Intraocular Lenses, STAAR Surgical Company, Eyetec, and other players.

June 2024 – Alcon, the world leader in eye care, today announced that its UNITY Vitreoretinal Cataract System (VCS) and UNITY Cataract System (CS) have been granted 510(k) clearance by the U.S. Food and Drug Administration (FDA). The systems are the first product launches introduced under Alcon's eagerly awaited UNITY portfolio, designed to improve surgical performance in cataract and vitreoretinal surgery.

September 2024 – Johnson & Johnson Vision, a global eye health company, declared the expanded U.S. launch of its new presbyopia-correcting intraocular lens, the TECNIS Odyssey. The new full-range IOL provides patients with constant, high-quality vision for distance through to near, greatly diminishing their reliance on glasses and improving visual outcomes at multiple focal lengths.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 156.28 Billion |

| Market Size by 2032 | USD 328.72 Billion |

| CAGR | CAGR of 9.81% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Vision Testing & Eye Exams, Surgical Interventions, Primary Care Services, Others) • By Indication (Refractive Errors, Cataracts, Glaucoma, Age-related Macular Degeneration (AMD), Diabetic Retinopathy, Dry Eye Syndrome, Others) • By Provider Type (Standalone Eye Clinics, Multispecialty Hospitals, Optical Retail Chains with Eye Care Services, Academic & Research Institutions, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Alcon, Johnson & Johnson Vision Care, Bausch & Lomb Incorporated, Carl Zeiss Meditec AG, EssilorLuxottica, CooperVision, HOYA Corporation, Rayner Intraocular Lenses, STAAR Surgical Company, Eyetec, and other players |

Ans: The Eye Care Services Market is expected to grow at a CAGR of 9.81% from 2025 to 2032.

Ans: The Eye Care Services Market was USD 156.28 billion in 2024 and is expected to reach USD 328.72 billion by 2032.

Ans: The Increasing prevalence of vision problems aids the market growth.

Ans: The “Surgical Interventions” segment dominated the Eye Care Services Market.

Ans: North America dominated the Eye Care Services Market in 2024.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2024)

5.2 Utilization & Referral Trends (2024), by Region

5.3 Eye Care Spending, by Region (Government, Private, Out-of-Pocket) – 2024

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new Product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Eye Care Services Market Segmentation By Type

7.1 Chapter Overview

7.2 Vision Testing & Eye Exams

7.2.1 Vision Testing & Eye Exams Market Trends Analysis (2021-2032)

7.2.2 Vision Testing & Eye Exams Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Surgical Interventions

7.3.1 Surgical Interventions Market Trends Analysis (2021-2032)

7.3.2 Surgical Interventions Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Primary care services

7.4.1 Primary care services Market Trends Analysis (2021-2032)

7.4.2 Primary care services Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Others

7.5.1 Others Market Trends Analysis (2021-2032)

7.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Eye Care Services Market Segmentation By Indication

8.1 Chapter Overview

8.2 Refractive Errors

8.2.1 Refractive Errors Market Trend Analysis (2021-2032)

8.2.2 Refractive Errors Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Cataracts

8.3.1 Cataracts Market Trends Analysis (2021-2032)

8.3.2 Cataracts Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Glaucoma

8.4.1 Glaucoma Market Trends Analysis (2021-2032)

8.4.2 Glaucoma Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Age-related Macular Degeneration (AMD)

8.5.1 Age-related Macular Degeneration (AMD) Market Trends Analysis (2021-2032)

8.5.2 Age-related Macular Degeneration (AMD) Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Diabetic Retinopathy

8.6.1 Diabetic Retinopathy Market Trends Analysis (2021-2032)

8.6.2 Diabetic Retinopathy Market Size Estimates and Forecasts to 2032 (USD Billion)

8.7 Dry Eye Syndrome

8.7.1 Dry Eye Syndrome Market Trends Analysis (2021-2032)

8.7.2 Dry Eye Syndrome Market Size Estimates and Forecasts to 2032 (USD Billion)

8.8 Others

8.8.1 Others Market Trends Analysis (2021-2032)

8.8.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Eye Care Services Market Segmentation By Provider Type

9.1 Chapter Overview

9.2 Standalone Eye Clinics

9.2.1 Standalone Eye Clinics Market Trends Analysis (2021-2032)

9.2.2 Standalone Eye Clinics Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Multispecialty Hospitals

9.3.1 Multispecialty Hospitals Market Trends Analysis (2021-2032)

9.3.2 Multispecialty Hospitals Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Optical Retail Chains with Eye Care Services

9.4.1 Optical Retail Chains with Eye Care Services Market Trends Analysis (2021-2032)

9.4.2 Optical Retail Chains with Eye Care Services Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Academic & Research Institutions

9.5.1 Academic & Research Institutions Market Trends Analysis (2021-2032)

9.5.2 Academic & Research Institutions Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Other

9.6.1 Other Market Trends Analysis (2021-2032)

9.6.2 Other Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Eye Care Services Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.2.3 North America Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.2.4 North America Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.2.5 North America Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.2.6.2 USA Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.2.6.3 USA Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.2.7.2 Canada Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.2.7.3 Canada Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.2.8.2 Mexico Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.2.8.3 Mexico Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3 Europe

10.3.1 Trends Analysis

10.3.2 Europe Eye Care Services Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.3.3 Europe Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.4 Europe Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.5 Europe Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.6 Germany

10.3.6.1 Germany Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.6.2 Germany Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.6.3 Germany Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.7 France

10.3.7.1 France Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.7.2 France Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.7.3 France Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.8 UK

10.3.8.1 UK Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.8.2 UK Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.8.3 UK Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.9 Italy

10.3.9.1 Italy Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.9.2 Italy Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.9.3 Italy Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.10 Spain

10.3.10.1 Spain Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.10.2 Spain Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.10.3 Spain Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.11 Poland

10.3.11.1 Poland Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.11.2 Poland Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.11.3 Poland Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.12 Turkey

10.3.12.1 Turkey Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.12.2 Turkey Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.12.3 Turkey Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.3.13 Rest of Europe

10.3.13.1 Rest of Europe Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.3.13.2 Rest of Europe Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.3.13.3 Rest of Europe Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Eye Care Services Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.4.3 Asia Pacific Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.4 Asia Pacific Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.5 Asia Pacific Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.6.2 China Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.6.3 China Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.7.2 India Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.7.3 India Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.8.2 Japan Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.8.3 Japan Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.9.2 South Korea Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.9.3 South Korea Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4.10 Singapore

10.4.10.1 Singapore Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.10.2 Singapore Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.10.3 Singapore Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4.11 Australia

10.4.11.1 Australia Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.11.2 Australia Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.11.3 Australia Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.4.12 Rest of Asia Pacific

10.4.12.1 Rest of Asia Pacific Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.4.12.2 Rest of Asia Pacific Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.4.12.3 Rest of Asia Pacific Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Trends Analysis

10.5.2 Middle East and Africa Eye Care Services Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.5.3 Middle East and Africa Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.5.4 Middle East and Africa Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.5.5 Middle East and Africa Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.5.6 UAE

10.5.6.1 UAE Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.5.6.2 UAE Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.5.6.3 UAE Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.5.7 Saudi Arabia

10.5.7.1 Saudi Arabia Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.5.7.2 Saudi Arabia Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.5.7.3 Saudi Arabia Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.5.8 Qatar

10.5.8.1 Qatar Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.5.8.2 Qatar Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.5.8.3 Qatar Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.5.9 South Africa

10.5.9.1 South Africa Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.5.9.2 South Africa Eye Care Services Market Estimates and Forecasts by Indication (2021-2032) (USD Billion)

10.5.9.3 South Africa Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.5.10 Rest of Middle East & Africa

10.5.10.1 Rest of Middle East & Africa Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.5.10.2 Rest of Middle East & Africa Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.5.10.3 Rest of Middle East & Africa Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Eye Care Services Market Estimates and Forecasts, by Country (2021-2032) (USD Billion)

10.6.3 Latin America Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.6.4 Latin America Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.6.5 Latin America Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.6.6.2 Brazil Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.6.6.3 Brazil Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.6.7.2 Argentina Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.6.7.3 Argentina Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

10.6.8 Rest of Latin America

10.6.8.1 Rest of Latin America Eye Care Services Market Estimates and Forecasts, by Type (2021-2032) (USD Billion)

10.6.8.2 Rest of Latin America Eye Care Services Market Estimates and Forecasts, by Indication (2021-2032) (USD Billion)

10.6.8.3 Rest of Latin America Eye Care Services Market Estimates and Forecasts, by Provider Type (2021-2032) (USD Billion)

11. Company Profiles

11.1 Alcon

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Product/ Services Offered

11.1.4 SWOT Analysis

11.2 Johnson & Johnson Vision Care

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Product/ Services Offered

11.2.4 SWOT Analysis

11.3 Bausch & Lomb Incorporated

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Product/ Services Offered

11.3.4 SWOT Analysis

11.4 Carl Zeiss Meditec AG

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Product/ Services Offered

11.4.4 SWOT Analysis

11.5 EssilorLuxottica,

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Product/ Services Offered

11.5.4 SWOT Analysis

11.6 CooperVision

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Product/ Services Offered

11.6.4 SWOT Analysis

11.7 HOYA Corporation

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Product/ Services Offered

11.7.4 SWOT Analysis

11.8 Rayner Intraocular Lenses

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Product/ Services Offered

11.8.4 SWOT Analysis

11.9 STAAR Surgical Company

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Product/ Services Offered

11.9.4 SWOT Analysis

11.10 Eyetec.

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Product/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

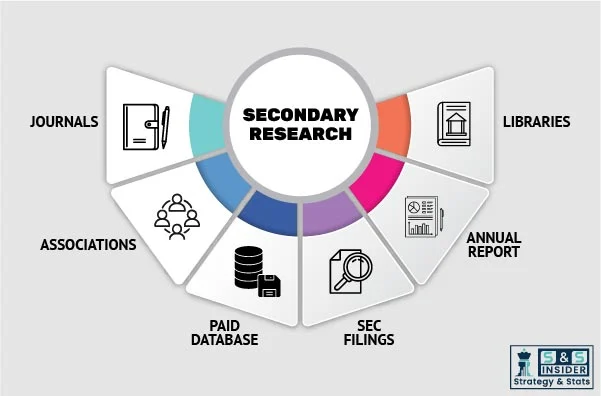

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Service Type

Vision Testing & Eye Exams

Surgical Interventions

Cataract Surgery

Refractive Surgery

Glaucoma Surgery

Retinal Surgery

Corneal Surgery

Others

Primary care services

Others

By Indication

Refractive Errors

Cataracts

Glaucoma

Age-related Macular Degeneration (AMD)

Diabetic Retinopathy

Dry Eye Syndrome

Others

By Provider Type

Standalone Eye Clinics

Multispecialty Hospitals

Optical Retail Chains with Eye Care Services

Academic & Research Institutions

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Poland

Turkey

Rest of Europe

Asia Pacific

China

India

Japan

South Korea

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

UAE

Saudi Arabia

Qatar

South Africa

Rest of Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g., Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players