Market Scope:

Get More Information on EV Composites Market - Request Sample Report

The EV Composites Market size is projected to reach USD 6.45 billion by 2032, was valued at USD 1.8 billion in 2023 and will grow at a CAGR of 17.3% over the forecast period.

Globally, the EV composites market is presently experiencing an upswing due to a combination of factors. Fuel efficiency and emission reduction standards set by governments are the main contributing factors for this growth, accounting for about 35% of it. Automakers have been forced to adopt lighter materials by these regulations to increase electric vehicle (EV) range. Another important factor is rising fuel costs that affect approximately 20% of the market drivers. With high gasoline prices, customers demand better fuel economy leading them to consider EVs as an alternative. Additionally, there is also a growing consumer preference for sustainable mobility solutions which accounts for 18% of the force driving this market. They are seen as cleaner compared to gasoline powered vehicles and thus preferred by environment conscious consumers among other factors such as government regulations on emissions. Technological advances also play a critical role with about 17% contribution towards driving the market forward. Battery technology improvements enabling longer-distance travel and lighter and stronger composites materials development are some examples of these advances being referred here. Lastly, nearly 10% of the market drivers consist of government incentives targeting EV adoption and infrastructure development which stimulate both manufacturers and consumers through financial encouragements.

The rise of carbon fiber over fiberglass is another trend. These two materials are light, but carbon fiber has a better strength-to-weight ratio, which makes it a favorite for high-performance EVs. Here, the growing premium and luxury EV segment will be interested in this because customers are looking for high-end electric vehicles. A move towards lighter and intricate designs may also be achieved through using 3D printing technology for manufacturing complex composite parts in EVs. This would make them not only more environment-friendly and efficient but also lighter.

Drivers:

Composites, notably such as carbon fibers are far much lighter than steel or aluminum that have traditionally been used without compromising on strength. This enables the car manufacturers to squeeze more power into the batteries of the vehicle without losing on performance.

Many countries are now enforcing stricter emission limits thereby compelling automakers to produce more electric vehicles (EVs). Also, consumers’ interest about EV’s is increasing due to their environmental concerns and potential savings they can make.

Automakers innovate and shift production towards electric vehicles due to stricter emission standards. For instance, the European Union set a 45% reduction in CO2 emissions from new cars by 2030 as opposed to its 2019 levels. On another front, the US Environmental Protection Agency (EPA) has adopted rules aimed at increasing the number of EVs sold such that by 2032 it is estimated that 70% of all sales will be electric. This regulatory pressure coincides with a growing consumer interest in EVs. Environmental consciousness as well as potential cost savings are driving this demand. Customers want to reduce their carbon footprints and see electric cars as being cheaper in terms of running costs because electricity is typically less expensive than gasoline. This combination of factors has led to an EV boom and its reverberations have been felt in the types of materials used for making them.

Restrain:

Composite materials generally cost more than traditional ones such as steel or aluminum metals.

There are currently no adequate recycling methods available for composite materials. This can pose a challenge for manufacturers who wish to minimize their environmental impact.

As opposed to traditional materials such as steel and aluminum that enjoy well-established recycling systems, composites tend to be broken down into fibers and resins in use hence making separation for reprocessing difficult and costly. Further, lower production volumes together with an emerging stage of recycling technology has seen less economically viable recycled composites compared to virgin materials. In addition, the absence of a widespread understanding and knowledge on options available when it comes to composite recycling is among the reasons why closed-loop system creation for these substances has been hindered. As a result, overcoming these obstacles is important for reducing manufacturers’ environmental footprint while keeping pace with increasing demand for environmentally friendly products by consumers.

Market Segmentation:

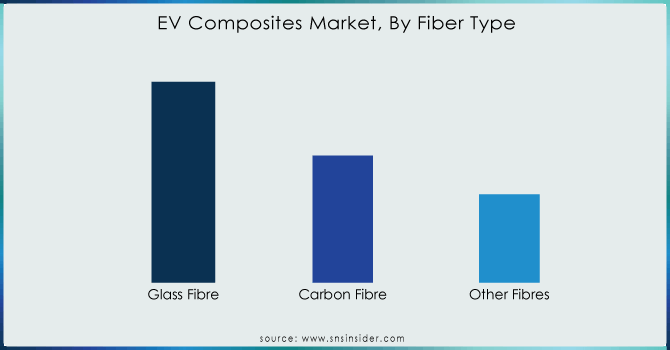

By Fiber Type

The glass fiber is the king of the hill with around 65% of market share. It is this dominance that can be ascribed to because it is cheap, easy to process and has well-established manufacturing processes. However, its use in high-performance EVs may be limited by its relatively lower strength-to-weight ratio compared to carbon fiber. The premium applications are covered by carbon fibers which constitute about 20% of the market share. This means that it’s a good material for lighter components in order to improve driving range and general vehicle performance due to its excellent strength-to-weight ratio. Consequently, manufacturers of high-end electric vehicles and racing cars find it more appealing. On the other hand, expensive cost and complex manufacturing processes hinder a wider adoption of carbon fiber. Other fibers take up 15% of the EV composites market such as natural fibers like flax, basalt fiber, aramid fibers amongst others.

Need any customization research on EV Composites Market - Enquiry Now

By Resin Type

Approximately 65% of material segment accounts show that thermoplastics are favored by EV composites market. Such dominance is due to their recyclable nature, flexibility in design, and high-volume manufacturing processes like injection molding which are efficient enough. On the other hand, 35% still remains of thermosets. This makes them a perfect choice for high performance EV components that experience extreme thermal stress because they have great heat resistance and structural rigidity. Nevertheless, their cross-linked molecular structure hampers recyclability.

By Type

The overall market is expected to be dominated by the non-premium segment which will occupy up to 25% of the total market. This domination is mainly driven by a high-production-volume of electric vehicles targeting mass markets where cost effectiveness is a major factor. By contrast, niche ultra-premium EVs that have advanced technology and are also very fast, will have approximately 35% market share. In this category, lightweighting and superior mechanical properties are crucial which has caused an increase in demand for high performance composites such as carbon fiber. The premium segment makes up about 40 percent of the market striking a balance between affordability and performance using various composite materials combinations for weight reduction and aesthetics.

By Application

It is the exterior segment of EV composites that takes the largest share of 30%, due to a demand for lightweight and fashionable car designs. It is closely followed by powertrain and chassis sector registering at 25% where composites improve handling and overall vehicle performance. Battery enclosures, which are critical for safety and range account for 20% of the market with a lot of growth potential ahead. Lastly, interior segment captures a quarter of the market, which will likely see more use of composite materials in things like headliners and seat parts as passenger comfort and cabin acoustics take center stage there. This segmentation shows how composites play many roles in EVs; they must be able to lose weight, increase speeds and allow flexible design changes since these factors are crucial in the changing electric mobility scene.

Regional Analysis:

The area of the APAC is the leader in the EV composites market, with many things put together. One of these factors is government policies that are tightening towards environmental protection as such the Chinese legislation mandates 35% of all new car sales to be electric by 2030. The increase in China’s projected electric vehicle production by 2025 will be approximately 80%. Additionally, cost competitiveness is a crucial factor. This directly translates into an up to 50% weight reduction compared to traditional steel thereby substantially increasing driving range which remains a chief consumer concern for EVs. Research conducted by SNS Insider indicated that reducing vehicle weight by 10% could extend battery life by around six percent. In light of this, there is a growing demand for affordable electric cars among APAC’s emerging middle class especially those in India. These markets can substitute expensive carbon fiber or fiberglasses used in manufacturing vehicles making them more appealing to producers who target budget-conscious customers and hence go for composites as a solution. Therefore, APAC’s EV composites market has great prospects for growth beyond today.

Key Players:

Toray Industries, Teijin Limited, Syensqo, Piran Advanced Composites, HRC, Envalior, Exel Composites, Kautex Textron, SGL Carbon, Polytec Holding AG, Plastic Omnium and others.

Recent Developments:

Toray Industries Inc.: In February 2023, it provided a new method of joining Carbon Fiber Reinforced Plastic (CFRP) for molding automotive parts. The technology is expected to speed up the process of molding in comparison with traditional processes.

Hexcel Corporation: Hexcel worked together with HP Composites S.p.A. on the development of class A body panels for supercars using advanced composites and technology from Hexcel. Class A panels are those that have a high-quality surface finish, suitable for the exterior of a vehicle.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 1.8 billion |

| Market Size by 2032 | US$ 6.45 Billion |

| CAGR | CAGR of 17.3 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | By Fiber Type (Glass Fibre, Carbon Fibre, Other Fibres) By Resin Type (Thermoplastics, Thermosets) By Manufacturing Process (Compression Molding, Injection Molding, RTM) By Type (Ultra-Premium, Premium, Non-Premium) By Application (Interior, Exterior, Battery Enclosure, Powertrain & Chassis) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Toray Industries, Teijin Limited, Syensqo, Piran Advanced Composites, HRC, Envalior, Exel Composites, Kautex Textron, SGL Carbon, Polytec Holding AG, Plastic Omnium and others. |

| Key Drivers | Many countries are now enforcing stricter emission limits thereby compelling automakers to produce more electric vehicles (EVs). Also, consumers’ interest about EV’s is increasing due to their environmental concerns and potential savings they can make |

| RESTRAINTS | Composite materials generally cost more than traditional ones such as steel or aluminum metals. |

Ans: The EV Composites Market size is projected to reach USD 6.45 billion by 2032, was valued at USD 1.8 billion in 2023

Ans: There are currently no adequate recycling methods available for composite materials. This can pose a challenge for manufacturers who wish to minimize their environmental impact.

Ans: The market will grow at a CAGR of 17.3% over the forecast period.

Ans: EV Composites Market key segmentation By Fiber Type, By Resin Type, By Manufacturing Process, By Type, By Application

Ans: Composites, notably such as carbon fibers are far much lighter than steel or aluminum that have traditionally been used without compromising on strength. This enables the car manufacturers to squeeze more power into the batteries of the vehicle without losing on performance.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. EV Composites Market Segmentation, By Fiber Type

7.1 Introduction

7.2 Glass Fibre

7.3 Carbon Fibre

7.4 Other Fibres

8. EV Composites Market Segmentation, By Resin Type

8.1 Introduction

8.2 Thermoplastics

8.3 Thermosets

9. EV Composites Market Segmentation, By Manufacturing Process

9.1 Introduction

9.2 Compression Molding

9.3 Injection Molding

9.4 RTM

10. EV Composites Market Segmentation, By Type

10.1 Introduction

10.2 Ultra-Premium

10.3 Premium

10.4 Non-Premium

11. EV Composites Market Segmentation, By Application

11.1 Introduction

11.2 Interior

11.3 Exterior

11.4 Battery Enclosure

11.5 Powertrain & Chassis

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 Trend Analysis

12.2.2 North America EV Composites Market By Country

12.2.3 North America EV Composites Market By Fiber Type

12.2.4 North America EV Composites Market By Resin Type

12.2.5 North America EV Composites Market By Manufacturing Process

12.2.6 North America EV Composites Market, By Type

12.2.7 North America EV Composites Market, By Application

12.2.8 USA

12.2.8.1 USA EV Composites Market By Fiber Type

12.2.8.2 USA EV Composites Market By Resin Type

12.2.8.3 USA EV Composites Market By Manufacturing Process

12.2.8.4 USA EV Composites Market, By Type

12.2.8.5 USA EV Composites Market, By Application

12.2.9 Canada

12.2.9.1 Canada EV Composites Market By Fiber Type

12.2.9.2 Canada EV Composites Market By Resin Type

12.2.9.3 Canada EV Composites Market By Manufacturing Process

12.2.9.4 Canada EV Composites Market, By Type

12.2.9.5 Canada EV Composites Market, By Application

12.2.10 Mexico

12.2.10.1 Mexico EV Composites Market By Fiber Type

12.2.10.2 Mexico EV Composites Market By Resin Type

12.2.10.3 Mexico EV Composites Market By Manufacturing Process

12.2.10.4 Mexico EV Composites Market, By Type

12.2.10.5 Mexico EV Composites Market, By Application

12.3 Europe

12.3.1 Trend Analysis

12.3.2 Eastern Europe

12.3.2.1 Eastern Europe EV Composites Market By Country

12.3.2.2 Eastern Europe EV Composites Market By Fiber Type

12.3.2.3 Eastern Europe EV Composites Market By Resin Type

12.3.2.4 Eastern Europe EV Composites Market By Manufacturing Process

12.3.2.5 Eastern Europe EV Composites Market By Type

12.3.2.6 Eastern Europe EV Composites Market, By Application

12.3.2.7 Poland

12.3.2.7.1 Poland EV Composites Market By Fiber Type

12.3.2.7.2 Poland EV Composites Market By Resin Type

12.3.2.7.3 Poland EV Composites Market By Manufacturing Process

12.3.2.7.4 Poland EV Composites Market By Type

12.3.2.7.5 Poland EV Composites Market, By Application

12.3.2.8 Romania

12.3.2.8.1 Romania EV Composites Market By Fiber Type

12.3.2.8.2 Romania EV Composites Market By Resin Type

12.3.2.8.3 Romania EV Composites Market By Manufacturing Process

12.3.2.8.4 Romania EV Composites Market By Type

12.3.2.8.5 Romania EV Composites Market, By Application

12.3.2.9 Hungary

12.3.2.9.1 Hungary EV Composites Market By Fiber Type

12.3.2.9.2 Hungary EV Composites Market By Resin Type

12.3.2.9.3 Hungary EV Composites Market By Manufacturing Process

12.3.2.9.4 Hungary EV Composites Market By Type

12.3.2.9.5 Hungary EV Composites Market, By Application

12.3.2.10 Turkey

12.3.2.10.1 Turkey EV Composites Market By Fiber Type

12.3.2.10.2 Turkey EV Composites Market By Resin Type

12.3.2.10.3 Turkey EV Composites Market By Manufacturing Process

12.3.2.10.4 Turkey EV Composites Market By Type

12.3.2.10.5 Turkey EV Composites Market, By Application

12.3.2.11 Rest of Eastern Europe

12.3.2.11.1 Rest of Eastern Europe EV Composites Market By Fiber Type

12.3.2.11.2 Rest of Eastern Europe EV Composites Market By Resin Type

12.3.2.11.3 Rest of Eastern Europe EV Composites Market By Manufacturing Process

12.3.2.11.4 Rest of Eastern Europe EV Composites Market By Type

12.3.2.11.5 Rest of Eastern Europe EV Composites Market, By Application

12.3.3 Western Europe

12.3.3.1 Western Europe EV Composites Market By Country

12.3.3.2 Western Europe EV Composites Market By Fiber Type

12.3.3.3 Western Europe EV Composites Market By Resin Type

12.3.3.4 Western Europe EV Composites Market By Manufacturing Process

12.3.3.5 Western Europe EV Composites Market By Type

12.3.3.6 Western Europe EV Composites Market, By Application

12.3.3.7 Germany

12.3.3.7.1 Germany EV Composites Market By Fiber Type

12.3.3.7.2 Germany EV Composites Market By Resin Type

12.3.3.7.3 Germany EV Composites Market By Manufacturing Process

12.3.3.7.4 Germany EV Composites Market By Type

12.3.3.7.5 Germany EV Composites Market, By Application

12.3.3.8 France

12.3.3.8.1 France EV Composites Market By Fiber Type

12.3.3.8.2 France EV Composites Market By Resin Type

12.3.3.8.3 France EV Composites Market By Manufacturing Process

12.3.3.8.4 France EV Composites Market By Type

12.3.3.8.5 France EV Composites Market, By Application

12.3.3.9 UK

12.3.3.9.1 UK EV Composites Market By Fiber Type

12.3.3.9.2 UK EV Composites Market By Resin Type

12.3.3.9.3 UK EV Composites Market By Manufacturing Process

12.3.3.9.4 UK EV Composites Market By Type

12.3.3.9.5 UK EV Composites Market, By Application

12.3.3.10 Italy

12.3.3.10.1 Italy EV Composites Market By Fiber Type

12.3.3.10.2 Italy EV Composites Market By Resin Type

12.3.3.10.3 Italy EV Composites Market By Manufacturing Process

12.3.3.10.4 Italy EV Composites Market By Type

12.3.3.10.5 Italy EV Composites Market, By Application

12.3.3.11 Spain

12.3.3.11.1 Spain EV Composites Market By Fiber Type

12.3.3.11.2 Spain EV Composites Market By Resin Type

12.3.3.11.3 Spain EV Composites Market By Manufacturing Process

12.3.3.11.4 Spain EV Composites Market By Type

12.3.3.11.5 Spain EV Composites Market, By Application

12.3.3.12 Netherlands

12.3.3.12.1 Netherlands EV Composites Market By Fiber Type

12.3.3.12.2 Netherlands EV Composites Market By Resin Type

12.3.3.12.3 Netherlands EV Composites Market By Manufacturing Process

12.3.3.12.4 Netherlands EV Composites Market By Type

12.3.3.12.5 Netherlands EV Composites Market, By Application

12.3.3.13 Switzerland

12.3.3.13.1 Switzerland EV Composites Market By Fiber Type

12.3.3.13.2 Switzerland EV Composites Market By Resin Type

12.3.3.13.3 Switzerland EV Composites Market By Manufacturing Process

12.3.3.13.4 Switzerland EV Composites Market By Type

12.3.3.13.5 Switzerland EV Composites Market, By Application

12.3.3.14 Austria

12.3.3.14.1 Austria EV Composites Market By Fiber Type

12.3.3.14.2 Austria EV Composites Market By Resin Type

12.3.3.14.3 Austria EV Composites Market By Manufacturing Process

12.3.3.14.4 Austria EV Composites Market By Type

12.3.3.14.5 Austria EV Composites Market, By Application

12.3.3.15 Rest of Western Europe

12.3.3.15.1 Rest of Western Europe EV Composites Market By Fiber Type

12.3.3.15.2 Rest of Western Europe EV Composites Market By Resin Type

12.3.3.15.3 Rest of Western Europe EV Composites Market By Manufacturing Process

12.3.3.15.4 Rest of Western Europe EV Composites Market By Type

12.3.3.15.5 Rest of Western Europe EV Composites Market, By Application

12.4 Asia-Pacific

12.4.1 Trend Analysis

12.4.2 Asia-Pacific EV Composites Market By Country

12.4.3 Asia-Pacific EV Composites Market By Fiber Type

12.4.4 Asia-Pacific EV Composites Market By Resin Type

12.4.5 Asia-Pacific EV Composites Market By Manufacturing Process

12.4.6 Asia-Pacific EV Composites Market By Type

12.4.7 Asia-Pacific EV Composites Market, By Application

12.4.8 China

12.4.8.1 China EV Composites Market By Fiber Type

12.4.8.2 China EV Composites Market By Resin Type

12.4.8.3 China EV Composites Market By Manufacturing Process

12.4.8.4 China EV Composites Market By Type

12.4.8.5 China EV Composites Market, By Application

12.4.9 India

12.4.9.1 India EV Composites Market By Fiber Type

12.4.9.2 India EV Composites Market By Resin Type

12.4.9.3 India EV Composites Market By Manufacturing Process

12.4.9.4 India EV Composites Market By Type

12.4.9.5 India EV Composites Market, By Application

12.4.10 Japan

12.4.10.1 Japan EV Composites Market By Fiber Type

12.4.10.2 Japan EV Composites Market By Resin Type

12.4.10.3 Japan EV Composites Market By Manufacturing Process

12.4.10.4 Japan EV Composites Market By Type

12.4.10.5 Japan EV Composites Market, By Application

12.4.11 South Korea

12.4.11.1 South Korea EV Composites Market By Fiber Type

12.4.11.2 South Korea EV Composites Market By Resin Type

12.4.11.3 South Korea EV Composites Market By Manufacturing Process

12.4.11.4 South Korea EV Composites Market By Type

12.4.11.5 South Korea EV Composites Market, By Application

12.4.12 Vietnam

12.4.12.1 Vietnam EV Composites Market By Fiber Type

12.4.12.2 Vietnam EV Composites Market By Resin Type

12.4.12.3 Vietnam EV Composites Market By Manufacturing Process

12.4.12.4 Vietnam EV Composites Market By Type

12.4.12.5 Vietnam EV Composites Market, By Application

12.4.13 Singapore

12.4.13.1 Singapore EV Composites Market By Fiber Type

12.4.13.2 Singapore EV Composites Market By Resin Type

12.4.13.3 Singapore EV Composites Market By Manufacturing Process

12.4.13.4 Singapore EV Composites Market By Type

12.4.13.5 Singapore EV Composites Market, By Application

12.4.14 Australia

12.4.14.1 Australia EV Composites Market By Fiber Type

12.4.14.2 Australia EV Composites Market By Resin Type

12.4.14.3 Australia EV Composites Market By Manufacturing Process

12.4.14.4 Australia EV Composites Market By Type

12.4.14.5 Australia EV Composites Market, By Application

12.4.15 Rest of Asia-Pacific

12.4.15.1 Rest of Asia-Pacific EV Composites Market By Fiber Type

12.4.15.2 Rest of Asia-Pacific EV Composites Market By Resin Type

12.4.15.3 Rest of Asia-Pacific EV Composites Market By Manufacturing Process

12.4.15.4 Rest of Asia-Pacific EV Composites Market By Type

12.4.15.5 Rest of Asia-Pacific EV Composites Market, By Application

12.5 Middle East & Africa

12.5.1 Trend Analysis

12.5.2 Middle East

12.5.2.1 Middle East EV Composites Market By Country

12.5.2.2 Middle East EV Composites Market By Fiber Type

12.5.2.3 Middle East EV Composites Market By Resin Type

12.5.2.4 Middle East EV Composites Market By Manufacturing Process

12.5.2.5 Middle East EV Composites Market By Type

12.5.2.6 Middle East EV Composites Market, By Application

12.5.2.7 UAE

12.5.2.7.1 UAE EV Composites Market By Fiber Type

12.5.2.7.2 UAE EV Composites Market By Resin Type

12.5.2.7.3 UAE EV Composites Market By Manufacturing Process

12.5.2.7.4 UAE EV Composites Market By Type

12.5.2.7.5 UAE EV Composites Market, By Application

12.5.2.8 Egypt

12.5.2.8.1 Egypt EV Composites Market By Fiber Type

12.5.2.8.2 Egypt EV Composites Market By Resin Type

12.5.2.8.3 Egypt EV Composites Market By Manufacturing Process

12.5.2.8.4 Egypt EV Composites Market By Type

12.5.2.8.5 Egypt EV Composites Market, By Application

12.5.2.9 Saudi Arabia

12.5.2.9.1 Saudi Arabia EV Composites Market By Fiber Type

12.5.2.9.2 Saudi Arabia EV Composites Market By Resin Type

12.5.2.9.3 Saudi Arabia EV Composites Market By Manufacturing Process

12.5.2.9.4 Saudi Arabia EV Composites Market By Type

12.5.2.9.5 Saudi Arabia EV Composites Market, By Application

12.5.2.10 Qatar

12.5.2.10.1 Qatar EV Composites Market By Fiber Type

12.5.2.10.2 Qatar EV Composites Market By Resin Type

12.5.2.10.3 Qatar EV Composites Market By Manufacturing Process

12.5.2.10.4 Qatar EV Composites Market By Type

12.5.2.10.5 Qatar EV Composites Market, By Application

12.5.2.11 Rest of Middle East

12.5.2.11.1 Rest of Middle East EV Composites Market By Fiber Type

12.5.2.11.2 Rest of Middle East EV Composites Market By Resin Type

12.5.2.11.3 Rest of Middle East EV Composites Market By Manufacturing Process

12.5.2.11.4 Rest of Middle East EV Composites Market By Type

12.5.2.11.5 Rest of Middle East EV Composites Market, By Application

12.5.3 Africa

12.5.3.1 Africa EV Composites Market By Country

12.5.3.2 Africa EV Composites Market By Fiber Type

12.5.3.3 Africa EV Composites Market By Resin Type

12.5.3.4 Africa EV Composites Market By Manufacturing Process

12.5.3.5 Africa EV Composites Market By Type

12.5.3.6 Africa EV Composites Market, By Application

12.5.3.7 Nigeria

12.5.3.7.1 Nigeria EV Composites Market By Fiber Type

12.5.3.7.2 Nigeria EV Composites Market By Resin Type

12.5.3.7.3 Nigeria EV Composites Market By Manufacturing Process

12.5.3.7.4 Nigeria EV Composites Market By Type

12.5.3.7.5 Nigeria EV Composites Market, By Application

12.5.3.8 South Africa

12.5.3.8.1 South Africa EV Composites Market By Fiber Type

12.5.3.8.2 South Africa EV Composites Market By Resin Type

12.5.3.8.3 South Africa EV Composites Market By Manufacturing Process

12.5.3.8.4 South Africa EV Composites Market By Type

12.5.3.8.5 South Africa EV Composites Market, By Application

12.5.3.9 Rest of Africa

12.5.3.9.1 Rest of Africa EV Composites Market By Fiber Type

12.5.3.9.2 Rest of Africa EV Composites Market By Resin Type

12.5.3.9.3 Rest of Africa EV Composites Market By Manufacturing Process

12.5.3.9.4 Rest of Africa EV Composites Market By Type

12.5.3.9.5 Rest of Africa EV Composites Market, By Application

12.6 Latin America

12.6.1 Trend Analysis

12.6.2 Latin America EV Composites Market By country

12.6.3 Latin America EV Composites Market By Fiber Type

12.6.4 Latin America EV Composites Market By Resin Type

12.6.5 Latin America EV Composites Market By Manufacturing Process

12.6.6 Latin America EV Composites Market By Type

12.6.7 Latin America EV Composites Market, By Application

12.6.8 Brazil

12.6.8.1 Brazil EV Composites Market By Fiber Type

12.6.8.2 Brazil EV Composites Market By Resin Type

12.6.8.3 Brazil EV Composites Market By Manufacturing Process

12.6.8.4 Brazil EV Composites Market By Type

12.6.8.5 Brazil EV Composites Market, By Application

12.6.9 Argentina

12.6.9.1 Argentina EV Composites Market By Fiber Type

12.6.9.2 Argentina EV Composites Market By Resin Type

12.6.9.3 Argentina EV Composites Market By Manufacturing Process

12.6.9.4 Argentina EV Composites Market By Type

12.6.9.5 Argentina EV Composites Market, By Application

12.6.10 Colombia

12.6.10.1 Colombia EV Composites Market By Fiber Type

12.6.10.2 Colombia EV Composites Market By Resin Type

12.6.10.3 Colombia EV Composites Market By Manufacturing Process

12.6.10.4 Colombia EV Composites Market By Type

12.6.10.5 Colombia EV Composites Market, By Application

12.6.11 Rest of Latin America

12.6.11.1 Rest of Latin America EV Composites Market By Fiber Type

12.6.11.2 Rest of Latin America EV Composites Market By Resin Type

12.6.11.3 Rest of Latin America EV Composites Market By Manufacturing Process

12.6.11.4 Rest of Latin America EV Composites Market By Type

12.6.11.5 Rest of Latin America EV Composites Market, By Application

13. Company Profiles

13.1 Toray Industries

13.1.1 Company Overview

13.1.2 Financial

13.1.3 Products/ Services Offered

13.1.4 The SNS View

13.2 Teijin Limited

13.2.1 Company Overview

13.2.2 Financial

13.2.3 Products/ Services Offered

13.2.4 The SNS View

13.3 Syensqo

13.3.1 Company Overview

13.3.2 Financial

13.3.3 Products/ Services Offered

13.3.4 The SNS View

13.4 Piran Advanced Composites

13.4.1 Company Overview

13.4.2 Financial

13.4.3 Products/ Services Offered

13.4.4 The SNS View

13.5 HRC

13.5.1 Company Overview

13.5.2 Financial

13.5.3 Products/ Services Offered

13.5.4 The SNS View

13.6 Envalior

13.6.1 Company Overview

13.6.2 Financial

13.6.3 Products/ Services Offered

13.6.4 The SNS View

13.7 Exel Composites

13.7.1 Company Overview

13.7.2 Financial

13.7.3 Products/ Services Offered

13.7.4 The SNS View

13.8 Kautex Textron

13.8.1 Company Overview

13.8.2 Financial

13.8.3 Products/ Services Offered

13.8.4 The SNS View

13.9 SGL Carbon

13.9.1 Company Overview

13.9.2 Financial

13.9.3 Products/ Services Offered

13.9.4 The SNS View

13.10 Others

13.10.1 Company Overview

13.10.2 Financial

13.10.3 Products/ Services Offered

13.10.4 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

14.3.1 Industry News

14.3.2 Company News

14.3.3 Mergers & Acquisitions

15. Use Case and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Fiber Type

Glass Fibre

Carbon Fibre

Other Fibres

By Resin Type

Thermoplastics

Thermosets

By Manufacturing Process

Compression Molding

Injection Molding

RTM

By Type

Ultra-Premium

Premium

Non-Premium

By Application

Interior

Exterior

Battery Enclosure

Powertrain & Chassis

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Agricultural Tractors Market Size was valued at USD 95.55 billion in 2023 and is expected to reach USD 175.66 billion by 2032 and grow at a CAGR of 7% over the forecast period 2024-2032.

The Automotive Oil Filter Market size was USD 75.43 Bn in 2023 and is expected to reach USD 106.43 Bn by 2032 and grow at a GAGR of 3.9% by 2024-2032.

The Automotive Horn Systems Market Size was valued at USD 923.17 million in 2023 and is expected to reach USD 1812.64 million by 2031 and grow at a CAGR of 8.8% over the forecast period 2024-2031.

The Automotive Operating System Market Size was valued at USD 8.88 Billion in 2023 and is expected to reach USD 21.09 Billion by 2032 and grow at a CAGR of 10.1% over the forecast period 2024-2032.

The Electric Vehicle Battery Recycling Market Size was valued at USD 8.98 billion in 2023 and is expected to reach USD 57.04 billion by 2031 and grow at a CAGR of 26% over the forecast period 2024-2031.

The Off-highway Electric Vehicle Market Size was valued at USD 2639 million in 2023 and is expected to reach USD 8718.35 million by 2032 and grow at a CAGR of 14.2% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd