Enterprise LLM Market Report Scope & Overview:

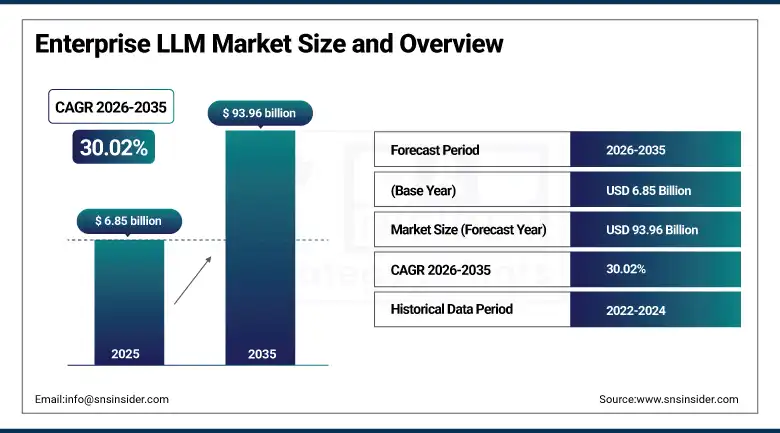

The Enterprise LLM Market was valued at USD 6.85 Billion in 2025 and is expected to reach USD 93.96 Billion by 2035, growing at a CAGR of 30.02% from 2026–2035.

The global enterprise LLM market is entering its most commercially consequential growth phase as organisations across every industry sector transition from AI experimentation toward production deployment of large language model capabilities. Enterprise LLMs are purpose-deployed AI systems built on foundation models including GPT-4o, Claude 3.5, Gemini 1.5, and Llama that are fine-tuned, retrieval-augmented, and governed for specific business applications whose production quality, security, compliance, and reliability requirements substantially exceed consumer AI deployment standards. The market’s commercial momentum is reinforced by the competitive urgency that AI adoption creates, as enterprises that successfully deploy LLM capabilities gain measurable productivity and quality advantages.

Microsoft Azure OpenAI Foundry launched in 2025 to provide enterprise-grade access to OpenAI models with reasoning models, multimodal LLMs, and secure deployment for business applications across the Azure cloud ecosystem. The launch consolidated Microsoft’s position as the enterprise LLM market’s most commercially significant infrastructure provider by integrating foundation model access, security governance, compliance tooling, and application development infrastructure within a unified enterprise AI platform that reduces deployment complexity for organisations at every stage of LLM adoption maturity.

Market Size and Forecast

-

Market Size in 2026E: USD 8.91 Billion

-

Market Size by 2035: USD 93.96 Billion

-

CAGR: 30.02% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Enterprise LLM Market - Request Free Sample Report

Enterprise LLM Market Trends

-

Rising adoption of retrieval-augmented generation (RAG) architectures is enabling enterprise LLMs to generate responses grounded in proprietary knowledge bases.

-

Growing investment in domain-specific fine-tuned LLMs for legal, healthcare, financial services, and engineering applications is creating differentiated enterprise AI solutions.

-

Increasing enterprise LLM governance investments, including output monitoring, bias detection, audit trails, and human oversight, are strengthening AI accountability.

-

Rising adoption of multimodal LLMs capable of processing text, images, audio, and structured data is expanding enterprise automation opportunities.

-

Expanding open-source LLM ecosystems through models such as Llama, Mistral, and community-developed derivatives is increasing deployment flexibility.

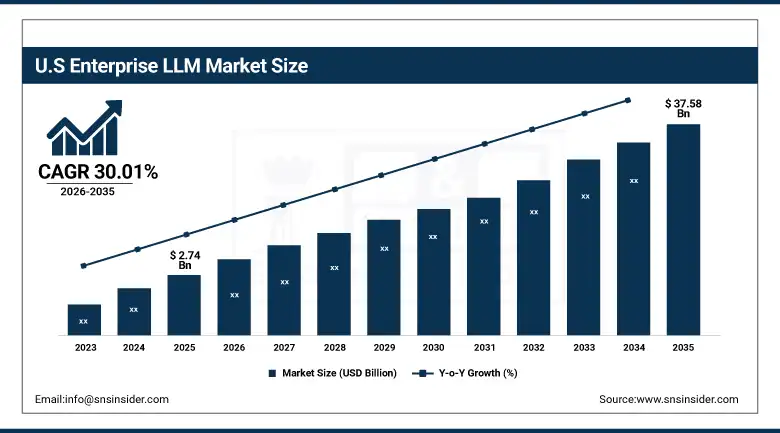

U.S. Enterprise LLM Market Outlook

The U.S. Enterprise LLM Market was valued at approximately USD 2.74 Billion in 2025 and is expected to reach approximately USD 37.58 Billion by 2035, growing at a CAGR of approximately 30.01%.

The United States is the world’s largest enterprise LLM market, driven by the extraordinary concentration of AI technology companies, the most commercially advanced enterprise AI adoption culture, and the headquarters presence of the world’s leading LLM foundation model providers. American enterprises across financial services, healthcare, technology, and professional services are deploying LLMs for legal document analysis, clinical documentation, code generation, customer service automation, and financial report synthesis at production scale that validates the commercial model for enterprise-wide LLM investment.

Amazon Web Services launched Amazon Nova, a family of foundation models on Amazon Bedrock in 2024, optimised for enterprise tasks including document analysis, video understanding, and agent workflows, at competitive price points that improve the cost economics of high-volume enterprise LLM deployment.

Enterprise LLM Market Segment Analysis

-

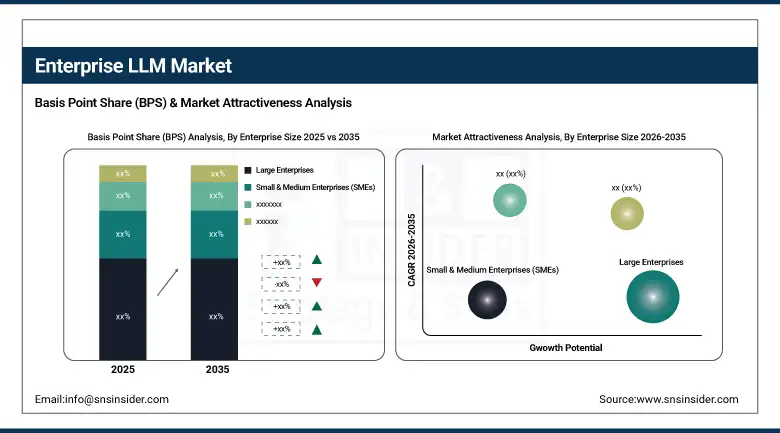

By Enterprise Size, the Large Enterprises segment dominated the Enterprise LLM Market with approximately 64.00% share in 2025, while the Small & Medium Enterprises segment is the fastest growing with a CAGR of 36.80% during the forecast period.

-

By Component, the Software segment dominated the Enterprise LLM Market with approximately 71.50% share in 2025, while the Services segment is the fastest growing with a CAGR of 38.20% during the forecast period.

-

By Deployment Mode, the Cloud-Based segment dominated the Enterprise LLM Market with approximately 68.40% share in 2025, while the Hybrid Deployment segment is the fastest growing with a CAGR of 39.10% during the forecast period.

-

By Industry Vertical, the IT & Telecom segment dominated the Enterprise LLM Market with approximately 24.60% share in 2025, while the Healthcare segment is the fastest growing with a CAGR of 40.30% during the forecast period.

By Enterprise Size, large enterprises dominate, SMEs grow fastest

Large enterprises retained the dominant enterprise size position with approximately 64% of the enterprise LLM market in 2025. Their commercial primacy reflects the structural advantages that organisational scale provides for LLM deployment success: large data assets that enable effective fine-tuning and RAG system development, dedicated AI engineering teams that can manage deployment complexity, procurement budgets that can absorb foundation model API costs at production volume, and the operational scale that creates measurable financial return from each percentage point of productivity improvement that LLM deployment delivers across thousands of employees. Large enterprise LLM programmes also generate the case study evidence and implementation reference architecture that sustain continued investment and expand deployment scope across successive business function adoption waves.

SMEs are the fastest-growing enterprise size segment because the commercial accessibility of enterprise LLM capabilities is improving rapidly through the development of simplified deployment platforms, pre-built industry-specific applications, and subscription pricing models whose per-month cost structure aligns with SME budget management preferences.

By Industry Vertical, IT & telecom dominates, healthcare grows fastest

IT and Telecom retained the dominant industry vertical position in the enterprise LLM market in 2025. The sector’s leadership reflects the perfect alignment between LLM capabilities and IT operations’ most time-consuming activities. Code generation, code review, documentation creation, incident analysis, runbook automation, and customer support scripting are each high-volume repetitive tasks that LLM automation addresses with measurable quality and productivity improvement. IT organisations’ above-average tolerance for AI tool adoption risk, whose mitigation strategies their technical expertise enables, and their direct access to the productivity measurement infrastructure.

Healthcare is the fastest-growing industry vertical in the enterprise LLM market because the sector’s combination of extraordinary administrative burden, clinical documentation time consumption, and the availability of validated AI clinical documentation solutions is creating the most commercially certain near-term LLM ROI calculation of any enterprise sector.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Enterprise LLM Market Insights

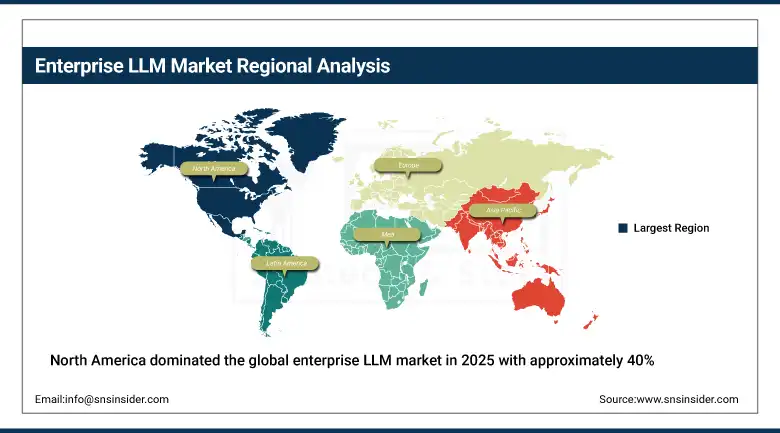

North America dominated the global enterprise LLM market in 2025 with approximately 40% of global revenues, with the United States accounting for approximately 87.4% of North American revenues. The region’s market leadership is grounded in the extraordinary concentration of AI foundation model companies, enterprise software vendors, and cloud infrastructure providers whose combined ecosystem defines the global enterprise LLM commercial standard.

Canada contributes approximately 12.6% of North American revenues through its sophisticated enterprise technology market, active AI research ecosystem anchored by the Vector Institute and Mila, and the progressive enterprise AI adoption across financial services, telecommunications, and healthcare organisations whose LLM investment is accelerating in alignment with the federal government’s Pan-Canadian AI Strategy commercialisation agenda.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Enterprise LLM Market Insights

Europe is a commercially significant enterprise LLM market where the EU AI Act’s governance framework for high-risk AI systems, GDPR’s data processing requirements, and the enterprise technology sector’s sophisticated adoption of AI productivity tools collectively create a structured commercial environment whose compliance-conscious procurement adds governance and explainability requirements that enterprise LLM platforms must satisfy for European adoption.

Germany accounts for approximately 22.3% of European revenues through its concentration of global industrial enterprises whose manufacturing, logistics, and finance operations are generating above-average LLM investment in supply chain automation, predictive maintenance, and financial compliance applications.

The United Kingdom and France are significant secondary European enterprise LLM markets where financial services sector compliance automation, healthcare NHS digital transformation investment, and the active AI startup ecosystems of London and Paris are creating structured commercial demand.

Asia Pacific Enterprise LLM Market Insights

Asia Pacific is the fastest-growing regional enterprise LLM market at a CAGR of approximately 32.17%, driven by China’s government-backed enterprise AI investment programme, India’s technology services sector’s rapid LLM adoption for service delivery automation, Japan’s manufacturing sector’s autonomous process optimisation investment, and Southeast Asia’s rapidly digitalising financial services and retail sectors.

China accounts for approximately 44.8% of Asia Pacific revenues through government-sponsored enterprise AI adoption programmes, domestic LLM providers including Baidu, Alibaba, and Huawei whose enterprise models serve Chinese corporate deployments, and the extraordinary pace of enterprise digital transformation investment that characterises the country’s commercial modernisation agenda.

India represents the most commercially significant emerging enterprise LLM opportunity within Asia Pacific, as the country’s vast technology services sector is simultaneously deploying LLMs to improve service delivery efficiency and developing LLM implementation capability that creates a globally competitive enterprise AI services industry.

MEA & Latin America Enterprise LLM Market Insights

The Middle East and Africa and Latin America are growing enterprise LLM markets where government digital transformation investment, expanding cloud infrastructure, and the commercial adoption of AI productivity platforms by financial services and technology companies are creating structured demand.

UAE leads MEA revenues at approximately 38.4% of the regional total through Dubai’s Smart City AI programme, the DIFC financial sector’s active AI adoption, and the UAE government’s explicit national AI strategy whose enterprise adoption targets create institutional motivation for LLM deployment across public and private sector organisations.

Brazil leads Latin American revenues at approximately 44.2% of the regional total through its large financial services sector’s active AI investment, growing technology enterprise adoption of AI productivity platforms, and the commercial presence of global enterprise software vendors whose Brazilian operations are deploying LLM capabilities through established enterprise customer relationships.

Market Dynamics

Growth Drivers: AI competitive urgency compelling enterprise investment and foundation model capability advancement continuously expanding automatable task range

The commercial competitive urgency created by AI adoption is the enterprise LLM market’s most powerful growth driver because it transforms AI investment from a discretionary productivity improvement into a competitive necessity whose deferral creates compounding disadvantage relative to AI-adopting competitors. Enterprises that successfully deploy LLMs for code generation, customer service, document processing, and operational automation are achieving productivity advantages whose financial impact is progressively visible in quarterly earnings performance, creating board-level investment pressure that sustains enterprise AI programme funding through economic cycle variation. This competitive urgency creates a self-reinforcing adoption cycle whose commercial momentum accelerates as reference case evidence accumulates.

Foundation model capability advancement is simultaneously expanding the range of enterprise tasks that LLMs can reliably complete without human supervision, creating new deployment opportunities with each model generation release. The transition from GPT-4 to GPT-4o, the introduction of reasoning models like o1 and o3, and the multimodal capability expansion of Claude 3.5 and Gemini 1.5 Ultra collectively demonstrate capability trajectories whose business application implications sustain investment interest among enterprise technology leaders whose evaluation of LLM deployment ROI improves with each model generation.

Restraints: AI hallucination and reliability concerns limiting deployment in high-stakes decision-making and data privacy and IP protection concerns in cloud-based model inference

LLM hallucination, where models generate plausible-sounding but factually incorrect outputs with apparent confidence, represents the most commercially significant reliability concern for enterprise deployment in high-stakes applications where factual accuracy is professionally and legally consequential. Legal, medical, financial, and regulatory compliance applications whose professional standard of care requires accurate information cannot tolerate the hallucination frequency of current LLM architectures without the human review overhead that RAG, confidence scoring, and citation verification systems are progressively improving but have not yet eliminated to the reliability threshold that fully autonomous deployment requires.

Data privacy and intellectual property protection concerns in cloud-based LLM inference create procurement hesitation among regulated enterprises whose customer data, proprietary business information, and confidential communications cannot be processed through third-party model inference endpoints without the contractual, technical, and regulatory safeguards that each hyperscaler’s enterprise LLM platform provides with varying degrees of verifiability. Regulated industries including financial services, healthcare, and government are progressively resolving these concerns through private deployment and secure processing agreements, but the compliance review timeline adds adoption delay that extends commercial realisation of latent LLM deployment demand.

Opportunities: Domain-specific fine-tuned model market creating premium AI product differentiation and agentic LLM workflow automation creating productivity leverage beyond single-task deployment

Domain-specific enterprise LLMs represent the most commercially differentiated product development direction in the market, as fine-tuned or RAG-augmented models whose performance quality in specific professional domains substantially exceeds general-purpose alternatives create premium pricing opportunities whose value is directly validated by the productivity and quality improvement that specialised models deliver relative to generic alternatives. Legal AI platforms whose document analysis accuracy reflects deep legal precedent training, medical documentation systems whose clinical terminology precision reflects healthcare-specific fine-tuning, and financial analysis tools whose regulatory knowledge is current and domain-accurate each represent commercially defensible market positions that general-purpose model providers cannot easily replicate without the domain-specific training investment that specialist providers are making.

Agentic LLM workflow automation represents the market’s most transformative near-term commercial evolution as the transition from single-task LLM assistance toward autonomous multi-step workflow execution creates qualitatively different productivity leverage whose commercial value proposition encompasses entire business process automation rather than individual task efficiency. Each successfully automated end-to-end business process creates a recurring cost reduction whose compounding financial impact over years of deployment substantially exceeds the initial investment, creating enterprise budget cases whose long-term ROI is commercially compelling for processes whose current labour cost constitutes significant operational expense.

Recent Developments:

-

2025: Microsoft Azure OpenAI Foundry launched in 2025 to provide enterprise-grade access to OpenAI models including reasoning models and multimodal LLMs within secure, compliant Azure infrastructure, consolidating Microsoft’s position as the enterprise LLM market’s most commercially significant infrastructure provider with over 31% global market share across enterprise AI deployment.

-

2024: Amazon Web Services launched Amazon Nova, a family of foundation models on Amazon Bedrock in 2024, optimised for enterprise tasks including document analysis, video understanding, and agent workflows, providing enterprise customers with AWS-native model choices at competitive price points that improve high-volume enterprise LLM deployment economics within the Bedrock platform.

-

2025: Google launched production-ready Gemini 2.5 AI models including Pro, Flash, and Flash-Lite in June 2025, targeting enterprise applications with enhanced reasoning, multimodal understanding, and scalable performance. The launch enables mission-critical enterprise workflows at varied performance-cost trade-offs, with major companies already deploying these models, signalling Google’s commercial push to compete for enterprise LLM market share against OpenAI and Microsoft.

Enterprise LLM Market Key Players

-

Microsoft

-

OpenAI

-

Google

-

Amazon Web Services

-

Anthropic

-

Meta AI

-

IBM

-

Mistral AI

-

Cohere

-

AI21 Labs

-

Salesforce

-

Oracle

-

SAP

-

Baidu

-

Huawei Technologies

-

Databricks

-

Nvidia

-

Palantir Technologies

-

Workday

-

ServiceNow

Enterprise LLM Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.85 Billion |

| Market Size by 2035 | USD 93.96 Billion |

| CAGR | CAGR of 30.02% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Enterprise Size (Large Enterprises, and Small & Medium Enterprises) • by Component (Software, Hardware, and Services) • by Deployment Mode (Cloud-Based, On-Premises, and Hybrid) • by Industry Vertical (IT & Telecom, BFSI, Healthcare, Retail & E-Commerce, Manufacturing, Government, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Microsoft, OpenAI, Google, Amazon Web Services, Anthropic, Meta AI, IBM, Mistral AI, Cohere, AI21 Labs, Salesforce, Oracle, SAP, Baidu, Huawei Technologies, Databricks, Nvidia, Palantir Technologies, Workday, ServiceNow |

Get in Touch