To Get More Information on Drug Delivery Systems Market - Request Sample Report

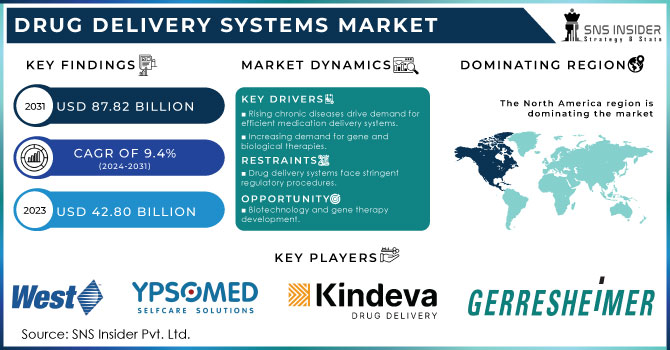

The Drug Delivery Systems Market was valued at USD 42.80 Billion in 2023 and is expected to reach USD 87.82 Billion By 2031 and grow at a CAGR of 9.4% over the forecast period of 2024-2031.

The global market for technologies and systems used to deliver therapeutic medications to predetermined sites or targeted sections of the body is referred to as the Drug Delivery Systems Market. The effectiveness, safety, and ease of drug administration are all optimised by these systems. Drug delivery systems are essential to the pharmaceutical sector because they increase the bioavailability and therapeutic effects of medications, lessen their side effects, and improve patient compliance. These systems can range in complexity and be divided into a number of groups, such as implanted drug delivery systems, transdermal patches, inhalation systems, oral drug delivery systems, injectable drug delivery systems, and others. Due to factors like the rising incidence of chronic diseases, improvements in drug formulation and delivery technologies, and the demand for more focused and individualised therapies, the market for drug delivery systems has seen significant expansion in recent years. This industry has expanded as a result of the expansion of biologics and gene treatments, which frequently need specialised delivery methods. Pharmaceutical firms, producers of medical equipment, and research institutions are major players in the market for drug delivery systems. Liposomes, micelles, nanoparticles, nanocapsules, and implantable devices are just a few of the drug delivery technologies they create and market.

According to the WHO, potentially lethal infections like HIV have been identified in close to 70–71 million people. These innovations have forced medical practitioners to develop efficient drugs and delivery methods. Reputable pharmaceutical and healthcare companies have increased the manufacturing of essential medication delivery technologies to remedy this deficiency.

There is a high demand for efficient medication delivery systems because the prevalence of chronic diseases like cancer, diabetes, cardiovascular diseases, and respiratory disorders is on the rise.

increasing demand for gene and biological therapies.

In the treatment of many diseases, biologics—including monoclonal antibodies, vaccines, and cell therapies—have become increasingly important. To assure the effectiveness of these medicines, specialised drug delivery systems are frequently needed. Advanced delivery techniques are also required by the introduction of gene treatments, which entail introducing genetic material into cells. The market for drug delivery systems is expanding as a result of the growing use of biologics and gene treatments.

Restrain

Drug delivery system research and commercialization are subject to stringent regulatory procedures, which include clinical testing and clearances.

restricted adoption in underdeveloped areas.

Drug delivery systems have become more popular in industrialised areas, but their adoption in less developed areas may be constrained by concerns with infrastructure, a lack of healthcare services, and pricing. These areas might have trouble integrating cutting-edge drug delivery technology, which would restrict market expansion there.

Opportunity

Personalised medicine is becoming more and more of a focus, which presents huge prospects for drug delivery systems.

Biotechnology and gene therapy development.

Specialised drug delivery systems have an opportunity as the use of biologics and gene treatments rises. Targeted delivery of these medicines to particular cells or tissues is frequently necessary. It holds the potential for developing delivery platforms that can effectively distribute gene-editing tools or transport and safeguard sensitive biologics to advance these fields and the market for medication delivery systems.

Challenge

For businesses investing in the development of medicine delivery systems, protecting intellectual property rights is essential.

fragmentation of the market and competition.

The market for medication delivery systems is extremely fragmented, and several companies are vying for market share by creating cutting-edge products. New entrants face difficulties due to incumbent businesses' strong market positions, intellectual property portfolios, and established distribution networks. Market share and profitability can be impacted by fierce competition and the need to differentiate products and technologies.

Due to the Merck Group's small business volume in Russia, Ukraine, Belarus, and the Republic of Moldova, the war in Ukraine has not yet had a substantial impact on its net assets, financial condition, or operating results. Less than 1.5% of the Group's total net sales were produced in the aforementioned nations in both the fiscal years 2021 and 2022. These sales were nearly entirely due to the healthcare industry as well as the life sciences industry in relation to the delivery of healthcare.

Merck doesn't have any subsidiaries of its own in this region, with the exception of Russia. Credit insurance partially covers trade receivables from clients in the Republic of Moldova, Russia, Ukraine, and Belarus. Customers' payment habits in the impacted area are being attentively watched. At the end of 2022, there were no material loss allowances. Local payments within Russia to clients and staff, as well as cross-border payments to and from Russia, have so far been guaranteed without limitation.

Impact of Ongoing Recession

Additional sanctions and accompanying remedies might be implemented in response to the ongoing conflict in Ukraine and any potential future escalation. This poses a risk to economic development, along with other geopolitical crises. Delayed recovery from the COVID-19 outbreak, persistent or increasing supply-side problems, and skyrocketing energy and raw material prices all negatively affect the overall economy and each individual business.

Further increases in inflation rates and central bank interest rates boost the likelihood of a global recession even more. The numerous government support initiatives intended to mitigate the consequences of high energy costs or to build and maintain capacity for the manufacturing of vaccine vials may lower risks, but they may also exacerbate Europe's problems with government debt.

By Device Type

Conventional

Advanced

By Type

Transdermal

Inhalation

Injectable

Others

By Indication

Diabetes

Cardiovascular Disease

COPD

Asthma

By Distribution Channel

Retail Pharmacy

Hospital Pharmacy

Others

North America

USA

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

The Netherlands

Rest of Europe

Asia-Pacific

Japan

South Korea

China

India

Australia

Rest of Asia-Pacific

The Middle East & Africa

Israel

UAE

South Africa

Rest of the Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin America

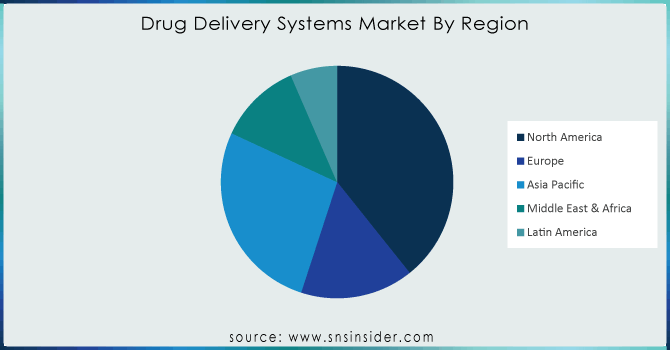

North America: A strong pharmaceutical industry, modern healthcare infrastructure, and favourable reimbursement rules have made North America a prominent market for drug delivery systems. Due to the existence of major market participants, increased R&D efforts, and technical breakthroughs, the industry has grown significantly in the United States in particular.

Asia-Pacific: The market for medication delivery systems is expanding significantly in the Asia-Pacific region. The market is expanding as a result of rapidly expanding economies, rising healthcare spending, and an increase in the prevalence of chronic diseases. With their strong manufacturing capabilities, technical developments, and government initiatives to support healthcare innovation, nations like China, Japan, India, and South Korea are leading the industry.

Do You Need any Customization Research on Drug Delivery Systems Market - Enquire Now

The major players are Gerresheimer AG, BD (Becton, Dickinson and Company), Kindeva Drug Delivery, Baxter, West Pharmaceutical Services Inc., Ypsomed, Medtronic, Nemara, Merck KGaA, E3D Elcam Drug Delivery Devices and others.

Recent Developments

Gerresheimer AG: In 2021, Gerresheimer A. and American Biotech signed a significant agreement to develop a novel pump that will continuously administer medicine to treat uncommon disorders.

Medtronic: In 2020, Medtronic introduced a new product. Real-time CGM data from Guardian Connect was integrated into InPen. The technology provides real-time glucose measurements along with information on insulin dosing.

| Report Attributes | Details |

| Market Size in 2023 | US$ 42.80 Bn |

| Market Size by 2031 | US$ 87.82 Bn |

| CAGR | CAGR of 9.4% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Device Type (Conventional and Advanced) • By Type (Transdermal, Inhalation, Injectable, and Others) • By Indication (Diabetes, Cardiovascular Disease, Multiple Sclerosis, COPD, and Asthma) • By Distribution Channel (Retail Pharmacy, Hospital Pharmacy, and Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Gerresheimer AG, BD (Becton, Dickinson and Company), Kindeva Drug Delivery, Baxter, West Pharmaceutical Services Inc., Ypsomed, Medtronic, Nemara, Merck KGaA, E3D Elcam Drug Delivery Devices |

| Key Drivers | • There is a high demand for efficient medication delivery systems because the prevalence of chronic diseases like cancer, diabetes, cardiovascular diseases, and respiratory disorders is on the rise. • Increasing demand for gene and biological therapies. |

| Market Opportunities | • Personalized medicine is becoming more and more of a focus, which presents huge prospects for drug delivery systems. • Biotechnology and gene therapy development. |

Ans: The Drug Delivery Systems Market size was valued at USD 39.13 Billion in 2022

Ans: The Drug Delivery Systems Market is to grow at 9.2% Over the Forecast Period 2023-2030.

Ans: The drug delivery system market is divided into oral, pulmonary, injectable, ophthalmic, nasal, topical, implantable, and transmucosal drug delivery methods based on the method of administration.

Ans: The Drug Delivery Systems Market is to Hit USD 79.12 Billion by 2030.

Ans: The major key players are Gerresheimer AG, BD (Becton, Dickinson and Company), Kindeva Drug Delivery, Baxter, West Pharmaceutical Services Inc., Ypsomed, Medtronic, Nemara, Merck KGaA, E3D Elcam Drug Delivery Devices and others

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of Ukraine- Russia War

4.2 Impact of Ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Drug Delivery Systems Market Segmentation, By Device Type

8.1 Conventional

8.2 Advanced

9. Drug Delivery Systems Market Segmentation, By Type

9.1 Transdermal

9.2 Inhalation

9.3 Injectable

9.4 Others

10. Drug Delivery Systems Market Segmentation, By Indication Diabetes

10.1 cardiovascular disease

10.2 Multiple Sclerosis

10.3 COPD

10.4 Asthma

11. Drug Delivery Systems Market Segmentation, By Distribution Channel

11.1 Retail Pharmacy

11.2 Hospital Pharmacy

11.3 Others

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 North America Drug Delivery Systems Market by Country

12.2.2 North America Drug Delivery Systems Market by Device Type

12.2.3 North America Drug Delivery Systems Market by Type

12.2.4 North America Drug Delivery Systems Market by Indication

12.2.5 North America Drug Delivery Systems Market by Distribution Channel

12.2.6 USA

12.2.6.1 USA Drug Delivery Systems Market by Device Type

12.2.6.2 USA Drug Delivery Systems Market by Type

12.2.6.3 USA Drug Delivery Systems Market by Indication

12.2.6.4 USA Drug Delivery Systems Market by Distribution Channel

12.2.7 Canada

12.2.7.1 Canada Drug Delivery Systems Market by Device Type

12.2.7.2 Canada Drug Delivery Systems Market by Type

12.2.7.3 Canada Drug Delivery Systems Market by Indication

12.2.7.4 Canada Drug Delivery Systems Market by Distribution Channel

12.2.8 Mexico

12.2.8.1 Mexico Drug Delivery Systems Market by Device Type

12.2.8.2 Mexico Drug Delivery Systems Market by Type

12.2.8.3 Mexico Drug Delivery Systems Market by Indication

12.2.8.4 Mexico Drug Delivery Systems Market by Distribution Channel

12.3 Europe

12.3.1 Europe Drug Delivery Systems Market by Country

12.3.2 Europe Drug Delivery Systems Market by Device Type

12.3.3 Europe Drug Delivery Systems Market by Type

12.3.4 Europe Drug Delivery Systems Market by Indication

12.3.5 Europe Drug Delivery Systems Market by Distribution Channel

12.3.6 Germany

12.3.6.1 Germany Drug Delivery Systems Market by Device Type

12.3.6.2 Germany Drug Delivery Systems Market by Type

12.3.6.3 Germany Drug Delivery Systems Market by Indication

12.3.6.4 Germany Drug Delivery Systems Market by Distribution Channel

12.3.7 UK

12.3.7.1 UK Drug Delivery Systems Market by Device Type

12.3.7.2 UK Drug Delivery Systems Market by Type

12.3.7.3 UK Drug Delivery Systems Market by Indication

12.3.7.4 UK Drug Delivery Systems Market by Distribution Channel

12.3.8 France

12.3.8.1 France Drug Delivery Systems Market by Device Type

12.3.8.2 France Drug Delivery Systems Market by Type

12.3.8.3 France Drug Delivery Systems Market by Indication

12.3.8.4 France Drug Delivery Systems Market by Distribution Channel

12.3.9 Italy

12.3.9.1 Italy Drug Delivery Systems Market by Device Type

12.3.9.2 Italy Drug Delivery Systems Market by Type

12.3.9.3 Italy Drug Delivery Systems Market by Indication

12.3.9.4 Italy Drug Delivery Systems Market by Distribution Channel

12.3.10 Spain

12.3.10.1 Spain Drug Delivery Systems Market by Device Type

12.3.10.2 Spain Drug Delivery Systems Market by Type

12.3.10.3 Spain Drug Delivery Systems Market by Indication

12.3.10.4 Spain Drug Delivery Systems Market by Distribution Channel

12.3.11 The Netherlands

12.3.11.1 Netherlands Drug Delivery Systems Market by Device Type

12.3.11.2 Netherlands Drug Delivery Systems Market by Type

12.3.11.3 Netherlands Drug Delivery Systems Market by Indication

12.3.11.4 Netherlands Drug Delivery Systems Market by Distribution Channel

12.3.12 Rest of Europe

12.3.12.1 Rest of Europe Drug Delivery Systems Market by Device Type

12.3.12.2 Rest of Europe Drug Delivery Systems Market by Type

12.3.12.3 Rest of Europe Drug Delivery Systems Market by Indication

12.3.12.4 Rest of Europe Drug Delivery Systems Market by Distribution Channel

12.4 Asia-Pacific

12.4.1 Asia Pacific Drug Delivery Systems Market by Country

12.4.2 Asia Pacific Drug Delivery Systems Market by Device Type

12.4.2 Asia Pacific Drug Delivery Systems Market by Type

12.4.4 Asia Pacific Drug Delivery Systems Market by Indication

12.4.5 Asia Pacific Drug Delivery Systems Market by Distribution Channel

12.4.6 Japan

12.4.6.1 Japan Drug Delivery Systems Market by Device Type

12.4.6.2 Japan Drug Delivery Systems Market by Type

12.4.6.3 Japan Drug Delivery Systems Market by Indication

12.4.6.4 Japan Drug Delivery Systems Market by Distribution Channel

12.4.7 South Korea

12.4.7.1 South Korea Drug Delivery Systems Market by Device Type

12.4.7.2 South Korea Drug Delivery Systems Market by Type

12.4.7.3 South Korea Drug Delivery Systems Market by Indication

12.4.7.4 South Korea Drug Delivery Systems Market by Distribution Channel

12.4.8 China

12.4.8.1 China Drug Delivery Systems Market by Device Type

12.4.8.2 China Drug Delivery Systems Market by Type

12.4.8.3 China Drug Delivery Systems Market by Indication

12.4.8.4 China Drug Delivery Systems Market by Distribution Channel

12.4.9 India

12.4.9.1 India Drug Delivery Systems Market by Device Type

12.4.9.2 India Drug Delivery Systems Market by Type

12.4.9.3 India Drug Delivery Systems Market by Indication

12.4.9.4 India Drug Delivery Systems Market by Distribution Channel

12.4.11 Australia

12.4.10.1 Australia Drug Delivery Systems Market by Device Type

12.4.10.2 Australia Drug Delivery Systems Market by Type

12.4.10.3 Australia Drug Delivery Systems Market by Indication

12.4.10.4 Australia Drug Delivery Systems Market by Distribution Channel

12.4.11 Rest of Asia-Pacific

12.4.11.1 APAC Drug Delivery Systems Market by Device Type

12.4.11.2 APAC Drug Delivery Systems Market by Type

12.4.11.3 APAC Drug Delivery Systems Market by Indication

12.4.11.4 APAC Drug Delivery Systems Market by Distribution Channel

12.5 The Middle East & Africa

12.5.1 The Middle East & Africa Drug Delivery Systems Market by Country

12.5.2 The Middle East & Africa Drug Delivery Systems Market by Device Type

12.5.3 The Middle East & Africa Drug Delivery Systems Market by Type

12.5.4 The Middle East & Africa Drug Delivery Systems Market by Indication

12.5.5 The Middle East & Africa Drug Delivery Systems Market by Distribution Channel

12.5.6 Israel

12.5.6.1 Israel Drug Delivery Systems Market by Device Type

12.5.6.2 Israel Drug Delivery Systems Market by Type

12.5.6.3 Israel Drug Delivery Systems Market by Indication

12.5.6.4 Israel Drug Delivery Systems Market by Distribution Channel

12.5.7 UAE

12.5.7.1 UAE Drug Delivery Systems Market by Device Type

12.5.7.2 UAE Drug Delivery Systems Market by Type

12.5.7.3 UAE Drug Delivery Systems Market by Indication

12.5.7.4 UAE Drug Delivery Systems Market by Distribution Channel

12.5.8 South Africa

12.5.8.1 South Africa Drug Delivery Systems Market by Device Type

12.5.8.2 South Africa Drug Delivery Systems Market by Type

12.5.8.3 South Africa Drug Delivery Systems Market by Indication

12.5.8.4 South Africa Drug Delivery Systems Market by Distribution Channel

12.5.9 Rest of Middle East & Africa

12.5.9.1 Rest of Middle East & Asia Drug Delivery Systems Market by Device Type

12.5.9.2 Rest of Middle East & Asia Drug Delivery Systems Market by Type

12.5.9.3 Rest of Middle East & Asia Drug Delivery Systems Market by Indication

12.5.9.4 Rest of Middle East & Asia Drug Delivery Systems Market by Distribution Channel

12.6 Latin America

12.6.1 Latin America Drug Delivery Systems Market by Country

12.6.2 Latin America Drug Delivery Systems Market by Device Type

12.6.3 Latin America Drug Delivery Systems Market by Type

12.6.4 Latin America Drug Delivery Systems Market by Indication

12.6.5 Latin America Drug Delivery Systems Market by Distribution Channel

12.6.6 Brazil

12.6.6.1 Brazil Drug Delivery Systems Market by Device Type

12.6.6.2 Brazil Africa Drug Delivery Systems Market by Type

12.6.6.3 Brazil Drug Delivery Systems Market by Indication

12.6.6.4 Brazil Drug Delivery Systems Market by Distribution Channel

12.6.7 Argentina

12.6.7.1 Argentina Drug Delivery Systems Market by Device Type

12.6.7.2 Argentina Drug Delivery Systems Market by Type

12.6.7.3 Argentina Drug Delivery Systems Market by Indication

12.6.7.4 Argentina Drug Delivery Systems Market by Distribution Channel

12.6.8 Rest of Latin America

12.6.8.1 Rest of Latin America Drug Delivery Systems Market by Device Type

12.6.8.2 Rest of Latin America Drug Delivery Systems Market by Type

12.6.8.3 Rest of Latin America Drug Delivery Systems Market by Indication

12.6.8.4 Rest of Latin America Drug Delivery Systems Market by Distribution Channel

13 Company Profile

13.1 Gerresheimer AG

13.1.1 Market Overview

13.1.2 Financials

13.1.3 Product/Services/Offerings

13.1.4 SWOT Analysis

13.1.5 The SNS View

13.2 BD (Becton, Dickinson and Company)

13.2.1 Market Overview

13.2.2 Financials

13.2.3 Product/Services/Offerings

13.2.4 SWOT Analysis

13.2.5 The SNS View

13.3 Kindeva Drug Delivery

13.3.1 Market Overview

13.3.2 Financials

13.3.3 Product/Services/Offerings

13.3.4 SWOT Analysis

13.3.5 The SNS View

13.4 Baxter

13.4.1 Market Overview

13.4.2 Financials

13.4.2 Product/Services/Offerings

13.4.4 SWOT Analysis

13.4.5 The SNS View

13.5 West Pharmaceutical Services Inc

13.5.1 Market Overview

13.5.2 Financials

13.5.3 Product/Services/Offerings

13.5.4 SWOT Analysis

13.5.5 The SNS View

13.6 Ypsome

13.6.1 Market Overview

13.6.2 Financials

13.6.3 Product/Services/Offerings

13.6.4 SWOT Analysis

13.6.5 The SNS View

13.7 Medtronic

13.7.1 Market Overview

13.7.2 Financials

13.7.3 Product/Services/Offerings

13.7.4 SWOT Analysis

13.7.5 The SNS View

13.8 Nemara

13.8.1 Market Overview

13.8.2 Financials

13.8.3 Product/Services/Offerings

13.8.4 SWOT Analysis

13.8.5 The SNS View

13.9 Merck KGaA

13.9.1 Market Overview

13.9.2 Financials

13.9.3 Product/Services/Offerings

13.9.4 SWOT Analysis

13.9.5 The SNS View

13.10 E3D Elcam Drug Delivery Devices

13.10.1 Market Overview

13.10.2 Financials

13.10.3 Product/Services/Offerings

13.10.4 SWOT Analysis

13.10.5 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.2 Recent Developments

15. Use Cases and Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Prosthetic Limbs Market was valued at USD 1.95 billion in 2023, and is expected to reach USD 3.07 billion by 2032, and grow at a CAGR of 5.18% over the forecast period 2024-2032.

The Pharma 4.0 Market was valued at 12.72 Bn in 2023 and is expected to reach 47.17 Bn by 2031, and grow at CAGR of 17.8% by forecast period 2024-2031.

The Veterinary Vaccine Adjuvants Market size was valued at USD 9.18 billion in 2023 and is estimated to reach USD 15.24 billion by 2032 with a growing CAGR of 5.8% from 2024 to 2032.

The HbA1c Testing Devices Market was valued at USD 1.72 billion in 2023, projected to grow to USD 3.18 billion by 2032 at a 7.10% CAGR.

Laboratory Freezers Market Size was valued at USD 4.92 billion in 2023 and is expected to reach USD 7.48 billion by 2032, growing at a CAGR of 4.78% over the forecast period 2024-2032.

The global antibiotics market size was USD 47.23 Billion in 2023 & is expected to reach USD 65.23 billion by 2032 at a CAGR of 3.70%.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd