Digital Transformation Market Size & Overview:

Get more information on Digital Transformation Market - Request Sample Report

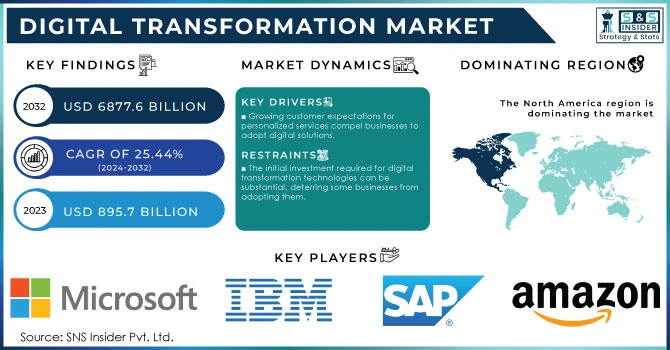

Digital Transformation Market was valued at USD 895.7 Billion in 2023 and is expected to reach USD 6877.6 Billion by 2032 and grow at a CAGR of 25.44% from 2024-2032.

The digital transformation market is experiencing significant growth as organizations worldwide seek to modernize their operations and enhance customer experiences through technology. Companies are increasingly adopting digital tools and solutions to optimize processes, enhance data analytics, and foster innovation. For instance, according to a survey, 93% of executives prioritize digital adoption within their organizations, with 66% acknowledging that the pandemic has accelerated their digital transformation initiatives. Several key factors are driving the growth of the digital transformation market, such as the rising demand for superior customer experiences, the need for operational efficiency, and the growing volume of data generated by businesses. As customer expectations evolve, companies are leveraging digital technologies like artificial intelligence (AI), machine learning (ML), and cloud computing to provide personalized experiences. A recent study indicated that 70% of customers expect businesses to understand their unique needs and preferences, leading to increased investment in analytics and customer relationship management (CRM) systems.

Moreover, the global shift toward remote work has underscored the importance of effective digital collaboration tools. Organizations are increasingly implementing cloud-based solutions to facilitate seamless communication and project management among remote teams. According to a report, 74% of CFOs plan to maintain some form of remote work permanently, highlighting the necessity for digital infrastructure that supports flexible work environments. The expansion of e-commerce also plays a crucial role in driving digital transformation, Companies are investing in e-commerce platforms and digital payment solutions to meet the growing consumer demand for convenient and secure shopping experiences.

In conclusion, the digital transformation market is rapidly evolving due to heightened customer expectations, the pursuit of operational efficiency, and the transition to remote work. Organizations that effectively utilize digital technologies will improve their competitiveness and adaptability in an increasingly digital landscape.

Digital Transformation Market Dynamics

Drivers

-

Growing customer expectations for personalized services compel businesses to adopt digital solutions.

-

Companies are compelled to adopt digital technologies to maintain competitiveness and meet industry standards.

-

The rising demand for online shopping pushes businesses to invest in e-commerce platforms and digital payment solutions.

The rise of online shopping significantly impacts the Digital Transformation Market, driving businesses to invest in e-commerce platforms and digital payment solutions. As consumer preferences shift towards digital shopping experiences, companies recognize the necessity to adapt to this trend to remain competitive. This transformation is fueled by factors such as convenience, speed, and the availability of a vast array of products online. Companies are increasingly investing in sophisticated e-commerce solutions that enable seamless user experiences, from product browsing to secure transactions. Features like personalized recommendations, customer reviews, and easy navigation are essential for attracting and retaining customers in a competitive market. Additionally, the growth of digital payment solutions complements the rise of online shopping. Consumers demand secure, efficient, and flexible payment options, including mobile wallets and buy-now-pay-later services. Companies are integrating these payment solutions into their e-commerce platforms to enhance the checkout experience and reduce cart abandonment rates. moreover, businesses are leveraging data analytics to understand consumer behavior and preferences better. By analyzing purchasing patterns, companies can optimize their product offerings, tailor marketing strategies, and improve customer service. The integration of technologies such as artificial intelligence (AI) and machine learning (ML) enables personalized shopping experiences, enhancing customer satisfaction and loyalty.

In conclusion, the increasing demand for online shopping is a key driver of the Digital Transformation Market, prompting businesses to invest in e-commerce platforms and digital payment solutions. By embracing these changes, companies can effectively meet consumer expectations and thrive in the evolving digital landscape.

|

Aspect |

Role of Online Shopping |

|---|---|

|

Consumer Preferences |

Increased demand for convenience and variety in shopping. |

|

Technology Integration |

Drives adoption of advanced technologies for seamless experiences. |

|

Payment Solutions |

Promotes development of secure and efficient payment methods. |

|

Customer Engagement |

Enhances interaction through reviews, ratings, and feedback. |

Restraints

-

The initial investment required for digital transformation technologies can be substantial, deterring some businesses from adopting them.

-

A lack of skilled personnel to manage and implement digital technologies can impede transformation efforts.

-

As more businesses undergo digital transformation, standing out becomes increasingly difficult, leading to potential competitive disadvantages.

As businesses increasingly embrace digital transformation, the landscape becomes more competitive and crowded, making it challenging for individual companies to differentiate themselves. This saturation of digital initiatives can lead to a scenario where many organizations offer similar services, products, and customer experiences, ultimately resulting in potential competitive disadvantages. In a rapidly evolving market, organizations that fail to innovate and set themselves apart risk losing customers to competitors who effectively leverage digital tools. While digital transformation is crucial for modern operations, the uniformity of digital solutions can make it difficult for businesses to create unique value propositions. For instance, many companies adopt similar e-commerce platforms, customer relationship management (CRM) systems, and marketing automation tools, leading to homogeneity in offerings. Moreover, as more companies invest in data analytics, artificial intelligence (AI), and personalized marketing strategies, distinguishing one’s brand becomes increasingly complex. The overabundance of digital content and marketing messages can lead to consumer fatigue, causing potential customers to overlook individual brands.

Additionally, the cost of keeping up with the latest digital trends can be high. Organizations must continuously innovate to stay relevant, requiring ongoing investment in new technologies and employee training. Those unable to keep pace with technological advancements may fall behind their competitors, struggling to catch up in a fast-moving environment. To mitigate these competitive disadvantages, businesses must focus on building strong brand identities and unique customer experiences. This can be achieved through innovative product offerings, exceptional customer service, and leveraging advanced technologies in ways that resonate with target audiences. Companies that adopt a customer-centric approach, continuously gather feedback and adapt their strategies accordingly will have a better chance of standing out in the crowded digital marketplace.

In summary, as digital transformation becomes more prevalent, the challenge of differentiation intensifies, pushing companies to innovate continuously and refine their value propositions to avoid competitive disadvantages.

Digital Transformation Market Segment Analysis

By Solution

In 2023, the big data and analytics segment dominated the market, securing a significant revenue share of 35.7%. This growth is primarily driven by the ability of analytical solutions to support a wide array of applications across different industries, along with the increasing demand from businesses to extract valuable insights from large data sets. These solutions help industries enhance operational efficiency, improve yield, and minimize equipment downtime. By effectively utilizing these tools, companies can gain a better understanding of consumer purchasing behaviors and achieve more accurate sales forecasts.

The social media segment is anticipated to see the highest CAGR during the forecast period. This growth is fueled by a shift among end-user enterprises toward leveraging social media to broaden their audience reach and enhance brand visibility. Businesses are increasingly using social media for sales promotions, marketing their products and services, managing public relations, and launching new offerings. Additionally, organizations are tapping into social media to gain essential market insights. The rising competition, evolving consumer demands, and technological advancements are driving companies to operate with greater agility and creativity, thereby supporting the growth of this segment.

By Service

In 2023, the professional services segment dominated the market and accounted for the largest revenue share of 74.8% in the market. This notable share is largely due to the rising demand for professional services, including managed and consulting services, across various sectors. Organizations aiming to digitalize their operations increasingly require expert assistance to tackle challenges such as vendor selection and cultural transformation. The market is anticipated to expand as professional service providers help end-user organizations effectively deploy and utilize the necessary resources.

The implementation and integration service segment is expected to achieve the highest CAGR during the forecast period. This growth is fueled by end-user organizations' preference for implementation service providers to ensure the smooth deployment of digital solutions. Furthermore, the intricate nature of implementing and integrating digital transformation solutions highlights the need for adequate support in aligning these solutions with existing frameworks, thereby bolstering the growth of this segment.

By End-Use

In 2023, the BFSI segment dominated the market and represented over 29.7% revenue share. This achievement is largely due to banks and financial institutions prioritizing the enhancement of customer experiences to strengthen their brand identity and expand their customer base. The increased focus on improving customer retention and offering seamless technical support is driving the growth of this segment. Additionally, the rise in remote work has greatly contributed to the expansion of the BFSI industry.

The healthcare segment is expected to experience a remarkable CAGR during the forecast period. This growth is driven by the digital transformation of healthcare, which yields positive results in marketing and sales while providing a comprehensive view of each patient. As a consequence, leading market players are emphasizing the enhancement of their solutions through the integration of advanced technologies like machine learning (ML), artificial intelligence (AI), and big data. Furthermore, digitalization in healthcare empowers organizations to offer contextual and predictive solutions to their customers.

Regional Analysis

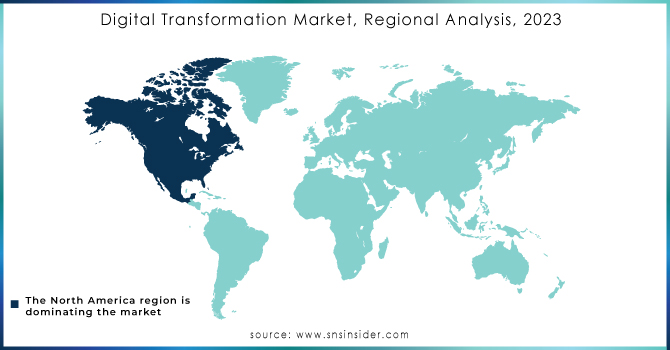

In 2023, North America solidified its position as the market leader with a revenue share of 43.5%. This dominance is primarily attributed to the extensive adoption of various online payment methods and the rapid integration of cloud computing technologies. Additionally, the rising consumer preference for digital media to post reviews and share experiences is driving brands and businesses to adopt digital transformation solutions and create customer-centric business models. Companies in the U.S. and Canada are making substantial investments, allocating budgets for marketing and digital channels that align with current industry trends.

The Asia Pacific digital transformation market is expected to significant CAGR during the forecast period, driven by the increasing uptake of digital transformation solutions among SMEs. The growing use of AI-driven advanced analytics tools to provide personalized services for both B2B and B2C consumers is a key factor propelling this growth. A significant number of smartphone users in the Asia Pacific region are actively engaging with social media on their devices, creating significant opportunities for digital transformation solutions.

Within the Asia Pacific, China captured a market share of 25.4% in the digital transformation space. Organizations in China are increasingly utilizing big data across various business processes, while government initiatives promoting workplace digitization are encouraging enterprises to implement electronic document management (EDM) solutions.

Need any customization research/data on Digital Transformation Market - Enquiry Now

Key Players

The major key players with their products are

-

Microsoft - Microsoft Azure

-

IBM - IBM Watson

-

Salesforce - Salesforce Customer 360

-

Oracle - Oracle Cloud Infrastructure

-

SAP - SAP S/4HANA

-

Google - Google Cloud Platform

-

Amazon Web Services (AWS) - AWS Lambda

-

Cisco - Cisco Meraki

-

Accenture - myConcerto

-

Deloitte - Deloitte Digital

-

Infosys - Infosys Digital Services

-

Capgemini - Capgemini Cloud Services

-

Wipro - Wipro HOLMES

-

HCL Technologies - HCL Digital Transformation Services

-

Adobe - Adobe Experience Cloud

-

TCS (Tata Consultancy Services) - TCS BaNCS

-

ServiceNow - ServiceNow ITSM

-

Atos - Atos Digital Transformation Solutions

-

Zebra Technologies - Zebra's SmartVision

-

Pega - Pega Customer Decision Hub

Recent developments

In January 2024, Google LLC collaborated with Worldline to enhance its digital transformation efforts and streamline operations. Worldline plans to leverage Google’s cloud-based technologies to improve digital payment services for customers throughout Europe.

In January 2024, Microsoft entered into a 10-year partnership with Vodafone aimed at enhancing customer experience services through Microsoft’s generative AI technologies. Together, they will develop financial and digital services targeted at SMEs in Africa and Europe.

| Report Attributes | Details |

| Market Size in 2023 | USD 895.7 Billion |

| Market Size by 2032 | USD 6877.6 Billion |

| CAGR | CAGR of 25.44% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Big Data & Analytics, Artificial Intelligence (AI), Cyber Security, Cloud Computing, Mobility, Social Media, Others) • By Service (Professional Services, Implementation & Integration) • By Deployment (Hosted, On-premise) • By Enterprise size (Large Enterprise, Small & Medium Enterprise) • By End-Use (BFSI, Government, Healthcare, IT & Telecom, Manufacturing, Retail, Others) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | IBM Corporation, Salesforce, Inc, Microsoft Corporation, Apple, Inc, SAP SE, Adobe, Yash Technologies, Alibaba, Amazon.com, Inc, Cisco Systems, Inc |

| Key Drivers | •Growing customer expectations for personalized services compel businesses to adopt digital solutions. •Companies are compelled to adopt digital technologies to maintain competitiveness and meet industry standards. •The rising demand for online shopping pushes businesses to invest in e-commerce platforms and digital payment solutions. |

| Market Restraints | •The initial investment required for digital transformation technologies can be substantial, deterring some businesses from adopting them. •A lack of skilled personnel to manage and implement digital technologies can impede transformation efforts. •As more businesses undergo digital transformation, standing out becomes increasingly difficult, leading to potential competitive disadvantages. |