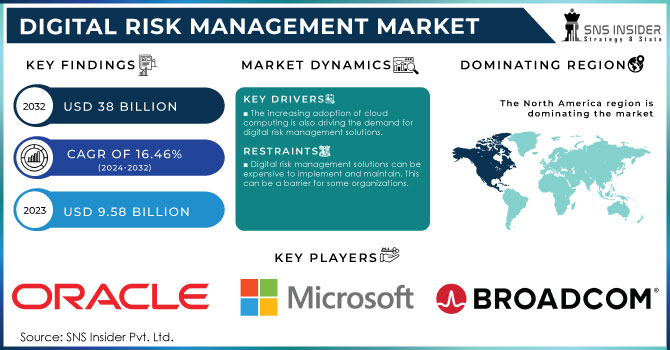

Digital Risk Management Market was valued at USD 9.82 billion in 2023 and is expected to reach USD 34.68 billion by 2032, growing at a CAGR of 15.12% from 2024-2032.

To Get More Information on Digital Risk Management Market - Request Sample Report

The Digital Risk Management market is witnessing rapid growth due to the increased reliance on digital technologies like cloud computing and the Internet of Things, which have made organizations more vulnerable to a wide range of risks. This growing digital infrastructure has led to a rise in cybersecurity threats, regulatory compliance challenges, and data privacy concerns. In 2023 alone, there were 2,365 cyberattacks, affecting 343,338,964 victims, marking a 72% increase in data breaches since 2021, which held the previous record. As a result, businesses are investing in advanced DRM solutions to mitigate these risks effectively. Nearly 75% of organizations now report having an incident response plan, with 63% regularly testing it, reflecting the heightened urgency for reliable risk management tools, particularly in sectors like finance and healthcare.

As digital transformation reshapes industries, the demand for DRM solutions is growing. Businesses recognize the need to address operational, financial, and reputational risks in their digital strategies. The evolving nature of cybersecurity threats has made proactive risk management essential. In 2023, 80% of consumers expressed concern about personal data protection, prompting businesses to prioritize cybersecurity. This is especially evident in sectors like retail, where consumer data protection is a priority. As companies focus on risk mitigation, the emphasis is on implementing comprehensive risk frameworks, including compliance with evolving regulations. For example, in June 2024, Broadcom's Symantec solutions achieved IRAP certification, meeting Australian government standards for securing sensitive data and critical infrastructure, further underscoring the need for robust risk management strategies.

Looking forward, the future of the Digital Risk Management market is filled with significant opportunities. The rise of technologies like artificial intelligence and machine learning is set to revolutionize how organizations predict, assess, and mitigate digital risks. 80% of organizations identify AI as an emerging risk while adopting the technology themselves. These advancements will allow for faster, more efficient responses to emerging threats, enabling businesses to be more proactive in risk management. Additionally, the expansion of IoT and cloud services is expected to create new vulnerabilities, increasing the demand for sophisticated DRM solutions. For example, in August 2024, Qualys expanded its TruRisk platform with Qualys TotalAI, targeting security and compliance challenges related to generative AI and large language models. This evolution will drive future growth in the DRM market.

Drivers

Escalating Cybersecurity Threats Push Demand for Advanced Digital Risk Management Solutions

The digital landscape is witnessing a surge in cybersecurity threats, with cyberattacks becoming more frequent and sophisticated. High-profile incidents such as ransomware attacks and massive data breaches are highlighting the vulnerabilities of organizations across sectors. This growing threat landscape has driven the demand for advanced Digital Risk Management solutions to proactively identify, assess, and mitigate risks. As cybercriminals continuously evolve their tactics, traditional security measures often fall short, necessitating more sophisticated DRM tools that can monitor potential threats in real-time, detect anomalies, and respond swiftly. Organizations are increasingly focusing on strengthening their cybersecurity frameworks, ensuring they have the right technology in place to protect sensitive data, preserve their reputation, and maintain business continuity. The rise in these security challenges is therefore a critical driver of the expanding DRM market.

Growing Recognition of Non-Traditional Risks Fuels Demand for Innovative Digital Risk Management Solutions

Organizations are increasingly aware of a broader spectrum of risks beyond traditional cybersecurity concerns. Emerging risks such as third-party vulnerabilities, supply chain disruptions, and reputational damage have become critical focus areas. These non-traditional risks can have significant financial and operational impacts, underscoring the need for more comprehensive Digital Risk Management strategies. As businesses increasingly rely on external partners, the potential for exposure through third-party vendors or partners has risen, necessitating enhanced monitoring and mitigation processes. Additionally, supply chain disruptions whether due to cyber incidents, geopolitical issues, or natural disasters highlight the need for DRM solutions that can identify and address these complex, interdependent risks. As organizations shift their focus to managing these emerging threats, the demand for advanced DRM solutions continues to grow, driving market expansion

Restraints

High Implementation Costs Limit Digital Risk Management Adoption for Smaller Enterprises

The high upfront investment required for advanced Digital Risk Management solutions presents a significant challenge for smaller enterprises. Implementing DRM systems involves substantial costs, including the purchase of specialized software, hardware, and the hiring or training of skilled personnel. For small and medium-sized enterprises, these expenses can be prohibitively high, making it difficult for them to justify such investments. SMEs often face budget constraints and may prioritize other areas of their business over cybersecurity, leaving them more vulnerable to emerging risks. This financial barrier not only hinders the adoption of DRM technologies but also limits the ability of smaller businesses to stay competitive in a rapidly digitalizing world. As a result, the high cost of implementation remains a key obstacle for many organizations in the DRM market.

Integration Challenges Delay the Adoption of Digital Risk Management Solutions

Integrating Digital Risk Management solutions with existing IT infrastructure, business processes, and legacy systems can be a complex and time-consuming process, deterring many organizations from adopting new technologies. Companies with established systems and workflows may face significant technical hurdles when trying to incorporate DRM tools, especially if the systems are outdated or incompatible with modern solutions. This integration complexity can lead to disruptions in daily operations, additional costs, and longer implementation timelines. Furthermore, the need for specialized technical expertise to manage the integration process adds to the resource burden. As a result, organizations may delay or avoid adopting DRM solutions altogether, fearing the potential operational challenges and costs associated with integration. These difficulties in aligning DRM solutions with existing business environments contribute to slower market adoption.

By Component

The Software segment dominated the Digital Risk Management market in 2023, with the highest revenue share of about 60%. This dominance is primarily due to the increasing need for advanced software solutions to address evolving cyber threats and regulatory requirements. Organizations are investing heavily in DRM software to enhance their cybersecurity infrastructure, automate risk assessments, and streamline compliance processes. The growing complexity of digital landscapes and the rise of sophisticated cyberattacks further amplify the demand for these software solutions, solidifying their market leadership.

The Services segment is expected to grow at the fastest CAGR of about 16.45% from 2024 to 2032, driven by the increasing need for personalized, expert-driven support in digital risk management. As businesses prioritize risk mitigation strategies, they require ongoing consultation, monitoring, and incident response services to effectively manage their digital risks. The shift toward cloud computing, along with the growing complexity of digital ecosystems, has accelerated the demand for specialized services, positioning the Services segment for rapid growth in the coming years.

By Organization Size

The Large Enterprise segment dominated the Digital Risk Management market in 2023, holding the highest revenue share of about 68%. This dominance is driven by the substantial budgets and resources that large enterprises allocate toward robust risk management strategies. These organizations face a broad range of complex risks, from cybersecurity threats to regulatory compliance, and therefore invest heavily in advanced DRM solutions. Additionally, large enterprises often require scalable, comprehensive risk management frameworks to protect vast amounts of sensitive data, which further drives their market leadership.

The Small and Medium-Sized Enterprise segment is expected to grow at the fastest CAGR of about 16.94% from 2024 to 2032. This growth is attributed to the increasing recognition among SMEs of the critical need to protect digital assets against evolving threats. As cyberattacks become more prevalent and regulations more stringent, SMEs are increasingly adopting affordable, scalable DRM solutions to safeguard their operations. The rise of cloud-based risk management platforms, which offer cost-effective, flexible options, is also fueling the rapid adoption of DRM solutions in this segment.

By Industry Vertical

The BFSI segment dominated the Digital Risk Management market in 2023, capturing the highest revenue share of about 32%. This dominance can be attributed to the critical need for safeguarding sensitive financial data and ensuring compliance with stringent regulations such as GDPR and PCI-DSS. The BFSI sector is a prime target for cyberattacks, including data breaches and financial fraud, prompting significant investment in advanced DRM solutions to mitigate these risks and protect customer trust.

The Healthcare segment is expected to grow at the fastest CAGR of 18.93% from 2024 to 2032, driven by the increasing need to protect patient data and comply with healthcare-specific regulations such as HIPAA. As the sector adopts digital transformation technologies, including electronic health recordsand telemedicine, the risk of cyber threats intensifies. Healthcare organizations are prioritizing digital risk management to protect sensitive patient information from cybercriminals and ensure the security of critical health data, fueling the sector's rapid growth in DRM adoption.

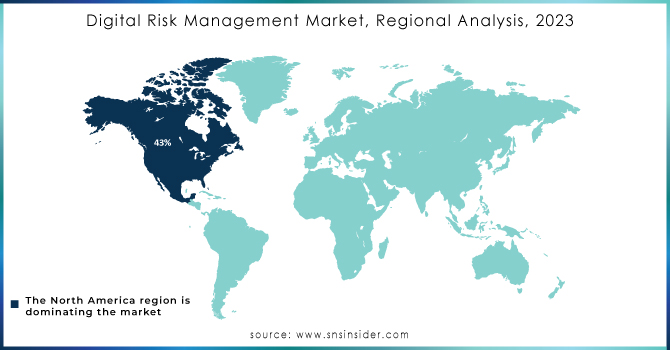

The North America segment dominated the Digital Risk Management market in 2023, securing the highest revenue share of about 39%. This leadership is largely due to the region's well-established digital infrastructure, high adoption of advanced technologies, and strong regulatory frameworks. North American companies, particularly in sectors like BFSI and healthcare, are investing heavily in DRM solutions to address growing cybersecurity risks and comply with stringent data protection regulations. The increasing frequency of cyberattacks and the region's emphasis on data privacy further solidify North America's position as the dominant player in the DRM market.

The Asia Pacific segment is expected to grow at the fastest CAGR of about 16.96% from 2024 to 2032, driven by the rapid digital transformation across emerging economies and the increasing awareness of cybersecurity risks. As organizations in countries like China, India, and Japan accelerate their adoption of digital technologies, the need for effective DRM solutions becomes more critical. With the rise of e-commerce, cloud computing, and mobile applications, the region is witnessing a surge in cyber threats, prompting a swift adoption of DRM solutions to protect digital assets and ensure compliance with evolving regulations. This combination of digital growth and heightened risk awareness is fueling the region's fast-paced market expansion.

Do You Need any Customization Research on Digital Risk Management Market - Enquire Now

IBM Corporation (IBM OpenPages, IBM Security QRadar)

Oracle Corporation (Oracle Risk Management Cloud, Oracle Governance, Risk, and Compliance)

SAP (SAP Business Integrity Screening, SAP Risk Management)

SAS Institute Inc. (SAS Risk Management for Banking, SAS Fraud Management)

Broadcom (Symantec Endpoint Protection, Symantec Data Loss Prevention)

NAVEX Global Inc (NAVEX EthicsPoint, NAVEX Risk & Compliance Management)

LogicManager Inc. (LogicManager Risk Management, LogicManager Incident Management)

Metric Stream (MetricStream GRC Platform, MetricStream Third-Party Risk Management)

Rapid7 (InsightVM, InsightIDR)

Microsoft Corporation (Microsoft Compliance Manager, Microsoft Defender for Identity)

ServiceNow Inc. (ServiceNow GRC, ServiceNow Security Incident Response)

Rsam (Rsam GRC Platform, Rsam Third-Party Risk Management)

Proofpoint Inc. (Proofpoint Email Protection, Proofpoint Cloud App Security Broker)

RSA Security LLC (RSA Archer GRC, RSA SecurID)

Optiv Security Inc. (Optiv Cybersecurity, Optiv Managed Security Services)

Qualys Inc. (Qualys Vulnerability Management, Qualys Policy Compliance)

OneTrust (OneTrust GRC, OneTrust Privacy Management)

Riskonnect Inc. (Riskonnect Risk Management, Riskonnect Incident Management)

ZeroFox Holdings Inc. (ZeroFox Social Media Risk Protection, ZeroFox External Threat Intelligence)

SecurityScorecard (SecurityScorecard Enterprise, SecurityScorecard Risk Assessment)

Archer Technologies LLC (Archer GRC Platform, Archer IT Risk Management)

Galvanize (Galvanize HighBond, Galvanize Governance, Risk, and Compliance)

LogicGate Inc. (LogicGate GRC Platform, LogicGate Third-Party Risk Management)

Resolver Inc. (Resolver Risk Management, Resolver Incident Management)

BitSight (BitSight Security Ratings, BitSight for Third-Party Risk)

Hyperproof Inc. (Hyperproof Compliance Management, Hyperproof Risk Management)

Oracle launched new cloud services in October 2024 aimed at enhancing profitability and risk management for banks. The suite includes tools for asset liability management, cash flow analysis, and profitability management, leveraging AI to improve financial insights and decision-making.

In July 2024, Datricks and SAP Signavio introduced a proactive risk management solution leveraging AI-powered risk mining. This collaboration helps organizations detect, prevent, and mitigate risks by analyzing financial data, streamlining audits, and enhancing business processes.

At VMware Explore 2024 in Barcelona, Broadcom announced innovations to accelerate IT modernization. These include advancements in VMware Cloud Foundation for private cloud transformation, AI-powered networking with VeloRAIN for edge workloads, and enhanced security solutions like VMware vDefend for better threat defense.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 9.82 Billion |

| Market Size by 2032 | USD 34.68 Billion |

| CAGR | CAGR of 15.12% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Deployment (Cloud, On-premise) • By Organization Size (Large Enterprise, Small and Medium-Sized Enterprise) • By Industry Vertical (BFSI, IT & Telecom, Healthcare, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IBM Corporation, Oracle Corporation, SAP, SAS Institute Inc., Broadcom, NAVEX Global Inc., LogicManager Inc., MetricStream, Rapid7, Microsoft Corporation, ServiceNow Inc., Rsam, Proofpoint Inc., RSA Security LLC, Optiv Security Inc., Qualys Inc., OneTrust, Riskonnect Inc., ZeroFox Holdings Inc., SecurityScorecard, Archer Technologies LLC, Galvanize, LogicGate Inc., Resolver Inc., BitSight, Hyperproof Inc. |

| Key Drivers | • Escalating Cybersecurity Threats Push Demand for Advanced Digital Risk Management Solutions • Growing Recognition of Non-Traditional Risks Fuels Demand for Innovative Digital Risk Management Solutions |

| RESTRAINTS | • High Implementation Costs Limit Digital Risk Management Adoption for Smaller Enterprises • Integration Challenges Delay the Adoption of Digital Risk Management Solutions |

Ans. The Compound Annual Growth rate for Digital Risk Management Market over the forecast period is 16.5 %.

Ans. USD 28.1 Billion is the Company's projected Digital Risk Management Market size by 2030.

Ans. Digital risk management refers to how a company assesses, monitors, and treats those risks that arise from digital transformation. It focuses on the threats and risks to an organization's data and the IT systems that process it.

Ans. Digital risk is created by the new technologies that a company adopts to help accelerate its digital transformation. A digital risk management program usually encompasses the risks associated with these technology categories: third-party organizations, mobile, big data, the Internet of Things, cloud computing, and social media.

Ans. Digital risk management is critical to business management because it helps organizations protect their data and IT systems from cyber threats and other risks associated with digital transformation. It also assists in demonstrating compliance with numerous data security mandates and industry standards.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates of Emerging Technologies

5.2 Network Infrastructure Expansion, by Region

5.3 Cybersecurity Incidents, by Region (2020-2023)

5.4 Cloud Services Usage, by Region

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Digital Risk Management Market Segmentation, By Component

7.1 Chapter Overview

7.2 Software

7.2.1 Software Market Trends Analysis (2020-2032)

7.2.2 Software Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Services

7.3.1 Services Market Trends Analysis (2020-2032)

7.3.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Digital Risk Management Market Segmentation, By Deployment

8.1 Chapter Overview

8.2 Cloud

8.2.1 Cloud Market Trends Analysis (2020-2032)

8.2.2 Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 On-premise

8.3.1 On-premise Market Trends Analysis (2020-2032)

8.3.2 On-premise Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Digital Risk Management Market Segmentation, By Industry Vertical

9.1 Chapter Overview

9.2 BFSI

9.2.1 BFSI Market Trends Analysis (2020-2032)

9.2.2 BFSI Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 IT & Telecom

9.3.1 IT & Telecom Market Trends Analysis (2020-2032)

9.3.2 IT & Telecom Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Healthcare

9.4.1 Healthcare Market Trends Analysis (2020-2032)

9.4.2 Healthcare Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Retail

9.5.1 Retail Market Trends Analysis (2020-2032)

9.5.2 Retail Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Manufacturing

9.6.1 Manufacturing Market Trends Analysis (2020-2032)

9.6.2 Manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Others

9.6.1 Others Market Trends Analysis (2020-2032)

9.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Digital Risk Management Market Segmentation, By Organization Size

10.1 Chapter Overview

10.2 Large Enterprise

10.2.1 Large Enterprise Market Trends Analysis (2020-2032)

10.2.2 Large Enterprise Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Small and Medium Size Enterprise

10.3.1 Small and Medium Size Enterprise Market Trends Analysis (2020-2032)

10.3.2 Small and Medium Size Enterprise Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Digital Risk Management Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.4 North America Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.5 North America Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.6 North America Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.7.2 USA Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.7.3 USA Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.7.4 USA Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.8.2 Canada Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.8.3 Canada Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.8.4 Canada Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.9.2 Mexico Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.9.3 Mexico Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.9.4 Mexico Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Digital Risk Management Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.7.2 Poland Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.7.3 Poland Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.7.4 Poland Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.8.2 Romania Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.8.3 Romania Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.8.4 Romania Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Digital Risk Management Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.4 Western Europe Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.5 Western Europe Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.6 Western Europe Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.7.2 Germany Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.7.3 Germany Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.7.4 Germany Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.8.2 France Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.8.3 France Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.8.4 France Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.9.2 UK Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.9.3 UK Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.9.4 UK Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.10.2 Italy Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.10.3 Italy Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.10.4 Italy Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.11.2 Spain Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.11.3 Spain Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.11.4 Spain Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.14.2 Austria Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.14.3 Austria Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.14.4 Austria Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Digital Risk Management Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.4 Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.5 Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.6 Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.7.2 China Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.7.3 China Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.7.4 China Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.8.2 India Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.8.3 India Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.8.4 India Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.9.2 Japan Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.9.3 Japan Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.9.4 Japan Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.10.2 South Korea Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.10.3 South Korea Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.10.4 South Korea Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.11.2 Vietnam Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.11.3 Vietnam Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.11.4 Vietnam Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.12.2 Singapore Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.12.3 Singapore Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.12.4 Singapore Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.13.2 Australia Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.13.3 Australia Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.13.4 Australia Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Digital Risk Management Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.4 Middle East Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.5 Middle East Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.6 Middle East Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.7.2 UAE Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.7.3 UAE Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.7.4 UAE Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Digital Risk Management Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.4 Africa Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.5 Africa Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.6 Africa Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Digital Risk Management Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.4 Latin America Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.5 Latin America Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.6 Latin America Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.7.2 Brazil Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.7.3 Brazil Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.7.4 Brazil Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.8.2 Argentina Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.8.3 Argentina Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.8.4 Argentina Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.9.2 Colombia Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.9.3 Colombia Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.9.4 Colombia Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Digital Risk Management Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Digital Risk Management Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Digital Risk Management Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Digital Risk Management Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

12. Company Profiles

12.1 IBM Corporation

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Oracle Corporation

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 SAP

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 SAS Institute Inc.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Broadcom

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 NAVEX Global Inc.

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 LogicManager Inc.

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 MetricStream

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Rapid7

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Microsoft Corporation

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Component

Software

Services

By Deployment

Cloud

On-premise

By Organization Size

Large Enterprise

Small and Medium Size Enterprise

By Industry Vertical

BFSI

IT

Telecom

Healthcare

Retail

Manufacturing

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Connected Infrastructure Market was valued at XX Bn in 2023 and will reach XX Bn in 2032, growing at a compound annual growth rate of XX % by to 2032.

The IoT-based Asset Tracking and Monitoring Market was valued at USD 4.5 billion in 2023 and will reach USD 13.1 billion and CAGR of 12.69% by 2032.

The Microserver Market size was valued at USD 30.04 billion in 2023 and is expected to grow to USD 108.94 billion by 2031 and grow at a CAGR of 15.39% over the forecast period of 2024-2031.

The Video Surveillance Market Size was valued at USD 60.1 Billion in 2023 and will reach USD 149.5 Billion by 2032, growing at a CAGR of 10.67% by 2032.

Carbon Footprint Management Market Size was valued at USD 10.68 Billion in 2023 and is expected to reach USD 31.02 Billion by 2032 and grow at a CAGR of 12.60 % over the forecast period 2024-2032.

Content Delivery Network Market was valued at USD 21.5 billion in 2023 and is expected to grow to USD 85.6 billion by 2032, at a CAGR of 16.6% over 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd