Get More Information on Decarbonization Market - Request Sample Report

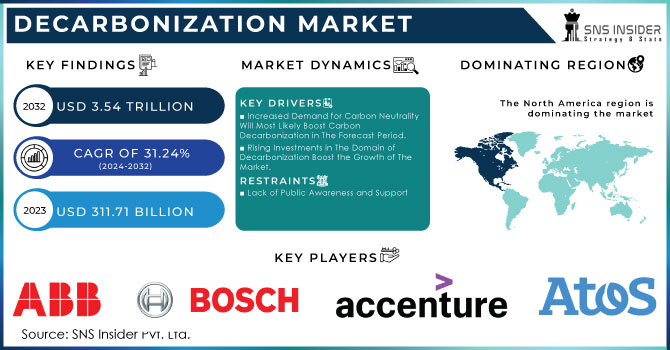

The Decarbonization Market Size was worth USD 311.71 billion in 2023 and is expected to grow to USD 3.54 trillion by 2032, with a CAGR of 31.24% in the forecast period 2024-2032.

The decarbonization market is being transformed by the global charge toward fighting climate change and reaching net-zero emissions. Market dynamics are driven by ambitious government regulations, advancing technology, and rapidly quickening corporate commitments to sustainability. This charge to decarbonization across the board has been driven further and louder since the implementation of policies such as the Green Deal by the European Union and the re-entry of the U.S. into the Paris Agreement. Leading from the front of technology innovations are carbon capture and storage, renewable energies, and electric vehicles—these are scalable solutions to reduce carbon footprints.

Innovators like Tesla pioneered technologies in electric vehicle technology and severely cut emissions in the transportation sector. In contrast, companies like Ørsted, primarily involved with renewable energy, are at the helm of transitioning from fossil fuels to wind and solar power, as can be attested to by their large-scale offshore wind farms. Corporate commitments—such as Microsoft's pledge to be carbon-negative by 2030—show the increasing contribution that private sector commitments can make to shifting markets. In addition, financial institutions are increasingly hard-wiring ESG criteria within investment strategies, acting as yet another driver for the market. Relations between governments, corporations, and financial entities are creating a solid basis for decarbonization. While it still faces challenges—high up-front costs of new technologies and far-reaching infrastructure development—the green technology's economic potential, along with jobs in renewable energies and long-term cost savings through reduced dependency on fossil fuels, buoy the market. The examples, such as the rapid growth of the solar industry in China and the U.S., underscore that there could exist a pathway to scalable and impactful decarbonization. In particular, over the last decade, China's slow transformation from a centrally planned to a more market-based electricity system increased carbon emissions from the power sector by 3 GtCO2 between 2011 and 2019—equivalent to the total emissions of India during this time. Specifically, overset scheduling a decade delayed the timing, adding up to 20% to annual GHG emissions in some provinces. It is further estimated that high-carbon plants over-allocate by at least 30% of electricity generation across every region, including those with the best record on energy savings.

The investment in generation capacity pushed this impact further up the curve at the same time as fuel efficiency improvements reduced the CPO-related emissions by more than 13%. The main conclusions from these findings are the strong economic transitions impact on GHG trajectories and sustainability. Overall, decarbonization markets present a massive growth opportunity at the junction of regulatory support, technological innovation, and growing stakeholder engagement.

KEY DRIVERS:

Increased Demand for Carbon Neutrality Will Most Likely Boost Carbon Decarbonization in The Forecast Period.

The surge in demand for carbon neutrality may occur in the future. Across the world, governments and companies just recently accelerated the targets for achieving net zero; accordingly, forcing innovation and investments into green technologies. As such, the Green Deal of the European Union sets carbon neutrality to be attained in the year 2050—policy and investment change within its member states. Equally, companies like Amazon and Microsoft have committed themselves to carbon Neutrality, hence enhancing technological developments in renewable energy, carbon capture and storage, and electric vehicles. A commitment by the government in China to peak carbon emissions before 2030 and be carbon neutral by 2060 has invited massive investments in renewable energy infrastructure, including expanding solar and wind power projects. Moreover, companies like Tesla are transforming transport by quickening the entry of electric vehicles to supplant an appreciable portion of fossil fuels. In addition, banks as well are working towards mainstreaming ESG criteria in financial investment resolutions, as a way to make more funds available to sustainable projects. This would be further encouraged by the rise of carbon trading markets, exemplified by the European Union Emissions Trading System and China's national carbon market. Examples include actions in the field as Ørsted's remarkable transformation from a mainly fossil fuel-based company to a global leader in offshore wind energy, and companies such as ExxonMobil and Shell implementing projects on CCS. The combined effort that these companies are putting in entropy is a strong trend of decarbonization propelled by global efforts to achieve carbon neutrality and is, therefore, likely to accelerate even more through the forecast period and beyond into a Low-Carbon Future.

Consumer Awareness and Demand for Green Products Fuel the Growth of Decarbonization Market

Consumer awareness and demand for green products are expected to propel growth in the decarbonization market. Consumers are slowly becoming more aware of their ecological footprint and are therefore seeking alternatives, which has recently pushed companies to devise innovative solutions for greener living. This shift is felt in industries such as the automotive sector, where demand for electric vehicles has surged the decarbonization market. Brands such as Tesla and Nissan now report increased sales because the consumer has exchanged a traditional car running on fossil fuels for one with no emissions. In return, retail brands like Patagonia and Unilever are finding that consumer loyalty and market share increase if action is being taken around questions of sustainability and carbon footprint. This demand also coincides on the energy front, whereby utilities start investing heavily in renewable sources: wind, solar, and hydroelectricity. For instance, NextEra, the largest renewable energy company, increased its portfolio multifold to meet demand from the rise in consumer preference toward clean energy. Green building materials and environmentally friendly products are going mainstream in that energy efficiency and sustainability are at the top of both homeowners' and builders' lists. Of late, low-carbon cement and sustainable timber have been born. On the part of food and beverage companies, think Beyond Meat and Oatly, which have been in the media for plant-based products that have less environment-related impact than their traditional meat and dairy counterparts. From the above, it is rather quite clear that there exists a good market by which decarbonization can grow further, driven by consumer demand. A rising consumer preference may drive the decarbonization market even further up to the forecast period, nudging more industries toward being eco-friendly and helping minimize global carbon emissions.

Rising Investments in The Domain of Decarbonization Boost the Growth of The Market.

RESTRAIN:

Lack of Public Awareness and Support

The greatest growth barrier to the decarbonization market is public awareness and support for carbon abatement. Generally, people show some kind of resistance to change from fossil fuels, especially in regions such as parts of the United States, as the impact is mostly related to jobs and economic activity. Misinformation about climate change and green technologies is an important source of friction that lowers the public's acceptance of objectively required policies and measures, including carbon pricing and investments in renewable energy. In many cases, resistance to projects like wind farms and solar installations is coupled with aesthetic concerns or a lack of time-bound understanding of their ecological advantages. Therefore, making the many advantages that decarbonization and sustainable practices offer known to all can help in surmounting these challenges effectively and make a reality the global carbon reduction goals set for 2024 and beyond.

By Service Type

By service, the sustainable transportation services segment dominated the decarbonization market and accounted for a market share of around 48.6% of the total global revenue in the year 2023. Sustainable transport services refer to those options and solutions that mostly consider environmental protection, reducing carbon dioxide emissions, cutting down resource use, and ensuring social and economic welfare. Another definition of sustainability in transportation would be using data and technology for better transportation services, lesser congestion, and more efficient public transit.

By Technology

The renewable energy technologies segment contributed more than 70.1% of the global revenue in 2023 and, by technology, dominated the market. Due to the stringent government regulations regarding emissions, renewable energy plants have increased at a fast rate across regions. With the increased adoption of gas-based and renewable power sources vis-à-vis coal-based power generation, the power scenario of the country has been witnessing a change. Increasing electricity distribution costs, faults in the main grid causing power outages, and incentive programs by the U.S. government most likely will move the end-use towards the setting up of hydropower systems, thereby increasing demand in the renewable energy segment.

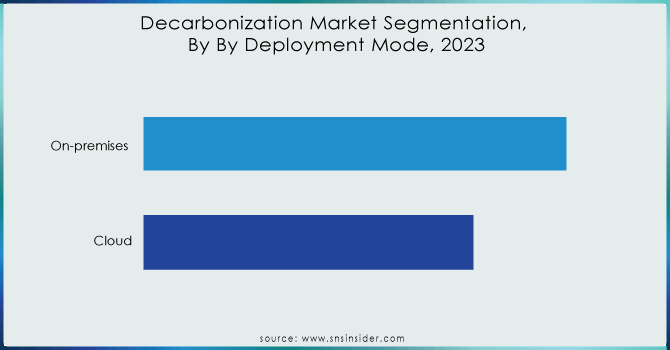

By Deployment Mode

By deployment mode, the on-premises segment held the largest market and generated 55.4% of global revenue in 2023. On-premise deployment in decarbonization refers to the reduction or complete avoidance of carbon emissions from industrial processes, energy production, transport, and buildings to help combat climate change. In-house production from renewable resources, such as solar panels, wind turbines, and even small hydro units, would make these facilities less dependent on fossil fuels and reduce the associated express emissions of power consumption.

Need any customization research on Decarbonization Market - Enquiry Now

By End-use Industry

The energy and utility sector dominated the decarbonization market with a revenue share of about 25% in 2023. Some of the main factors that, together, have been supporting this dominating position include: Energy and utility companies provide leadership to worldwide efforts that are meant toward significantly reducing carbon emissions through regulatory pressures and transformed consumer behaviors related to the choice of cleaner sources of energy. Apart from embracing new technologies such as carbon capture and storage that will help the environment, such firms have invested heavily in projects related to wind and solar farms, among others. Contributed to this has been the fact that this sector's critical role in supplying essential services means that decarbonization efforts within Energy and Utility have immense spillover effects into other sectors.

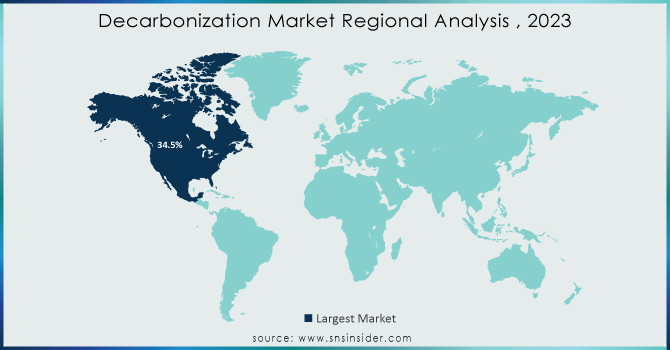

The North American region dominated the decarbonization market accounting for a market share of about 34.5% as a result of increasing climate change concerns from countries like the United States and Canada. Besides, increasing awareness among companies and major companies striving for carbon neutrality drive market growth in the coming years. Furthermore, increasing government interest in clean energy and steps being taken for investment in reducing global warming have been the main reasons for this increased market. For instance, the Department of Energy in the United States announced, on behalf of Biden's Investing America Agenda, that it is going to invest $6 billion in 33 projects across over 20 states to decarbonize energy-intensive industries and reduce GHG emissions in March 2024. Therefore, growing environmental protection awareness and growing investment in all projects in the region are expected to foster the growth of the market over the forecast period.

Moreover, Asia-Pacific held the fastest-growing region in the decarbonization market, with a revenue share of 30.9%. This is backed by ambitious government policies, rapid industrialization, and a growing focus on sustainable development in the region. Countries like China, Japan, and India have scaled up their efforts toward carbon emission reduction across sectors like manufacturing, energy, and transport. For instance, China's commitment to peaking its carbon emissions well before 2030 is accelerating investments in renewable energy and electric vehicles. Similarly, Japan's shifting focus towards hydrogen infrastructure is setting a fine example of regional initiatives towards decarbonization, just like the case of India in terms of its expansion in solar power capacity. This dynamic growth thus places Asia–Pacific at the heart of global comprehensive decarbonization efforts against climate change.

Some of the major players in the Decarbonization Market are ABB Ltd., Accenture, Atos SE, Bosch Thermotechnology, BP plc, Chevron Corporation, Deloitte, Enel S.p.A., General Electric Company (GE), Hitachi, Ltd., IBM, Johnson Controls International plc, Mitsubishi Heavy Industries, Ltd., Orsted A/S, SAP SE, Schneider Electric SE, Siemens AG, Tesla Inc., TotalEnergies SE and Toyota Motor Corporation and other players.

May 2024: The TEC under UNFCCC's Technology Mechanism noted global and regional efforts promoting decarbonization technologies in high-emission industrial sectors, accounting for 34% of global emissions.

February 2024: SECI launched India's largest solar-battery project in Chhattisgarh, combining solar panels and battery storage to store solar energy for peak demand, targeting significant annual CO2 emission reductions.

October 2023: Stargate Hydrogen and NextHeat formed a strategic partnership to develop innovative solutions for decarbonizing the industrial sector. They intend to replace natural gas with green hydrogen for applications such as industrial heating.

May 2023: Envision Digital and Dassault Systèmes have allied to pave the way toward industrial decarbonization by pairing the former's EnOS framework with the latter's 3DEXPERIENCE platform for energizing sustainable energy solutions and virtual twin experiences across industries.

| Report Attributes | Details |

| Market Size in 2023 | US$ 311.71 billion |

| Market Size by 2032 | US$ 3.54 Trillion |

| CAGR | CAGR of 31.24% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service (Carbon Accounting and Reporting, Sustainable Transportation, Waste Reduction, and Circular Economy), • By Technology (Renewable Energy Technologies, Energy Efficiency Solutions, Electric Vehicles (EVs), Carbon Removal Technologies, Carbon Capture and Storage (CCS)) • By Deployment Mode (Cloud, On-premises) • By End-use Industry (Oil & Gas, Energy and Utility, Agriculture, Government, Automotive & Transportation, Aerospace & Defense, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ABB Ltd., Accenture, Atos SE, Bosch Thermotechnology. BP plc, Chevron Corporation, Deloitte, Enel S.p.A., General Electric Company (GE), Hitachi, Ltd., IBM, Johnson Controls International plc, Mitsubishi Heavy Industries, Ltd., Orsted A/S, SAP SE, Schneider Electric SE, Siemens AG, Tesla Inc., TotalEnergies SE, Toyota Motor Corporation |

| Key Drivers | • Increased Demand for Carbon Neutrality Will Most Likely Boost Carbon Decarbonization in The Forecast Period. • Consumer Awareness and Demand for Green Products Fuel the Growth of Decarbonization Market • Rising Investments in The Domain of Decarbonization Boost the Growth of The Market. |

| Restraints | • Lack of Public Awareness and Support |

Ans: The North American region dominated the Decarbonization Market holding the largest market share of about 34.5% during the forecast period.

Ans: Lack of public awareness and support hamper the growth of the market.

Ans: Increased demand for carbon neutrality, consumer awareness, and demand for green products fuel the growth of the decarbonization market and rising investments in the domain of decarbonization are some of the driving factors boosting the growth of the decarbonization market.

Ans: Decarbonization Market size was USD 311.71 billion in 2023 and is expected to reach USD 3.54 trillion by 2032.

Ans: The Decarbonization Market is expected to grow at a CAGR of 31.24%.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Decarbonization Market Segmentation, By Service Type

7.1 Introduction

7.2 Carbon Accounting and Reporting

7.3 Sustainable Transportation

7.4 Waste Reduction and Circular Economy

8. Decarbonization Market Segmentation, By Technology

8.1 Introduction

8.2 Renewable Energy Technologies

8.3 Energy Efficiency Solutions

8.4 Electric Vehicles (EVs)

8.5 Carbon Removal Technologies

8.6 Carbon Capture and Storage (CCS)

9. Decarbonization Market Segmentation, By Deployment Mode

9.1 Introduction

9.2 Cloud

9.3 On-premises

10. Decarbonization Market Segmentation, By End-use Industry

10.1 Introduction

10.2 Oil & Gas

10.3 Energy and Utility

10.4 Agriculture

10.5 Government

10.6 Automotive & Transportation

10.7 Aerospace & Defense

10.8 Manufacturing

10.9 Others

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 Trend Analysis

11.2.2 North America Decarbonization Market by Country

11.2.3 North America Decarbonization Market By Service Type

11.2.4 North America Decarbonization Market By Technology

11.2.5 North America Decarbonization Market By Deployment Mode

11.2.6 North America Decarbonization Market By End-use Industry

11.2.7 USA

11.2.7.1 USA Decarbonization Market By Service Type

11.2.7.2 USA Decarbonization Market By Technology

11.2.7.3 USA Decarbonization Market By Deployment Mode

11.2.7.4 USA Decarbonization Market By End-use Industry

11.2.8 Canada

11.2.8.1 Canada Decarbonization Market By Service Type

11.2.8.2 Canada Decarbonization Market By Technology

11.2.8.3 Canada Decarbonization Market By Deployment Mode

11.2.8.4 Canada Decarbonization Market By End-use Industry

11.2.9 Mexico

11.2.9.1 Mexico Decarbonization Market By Service Type

11.2.9.2 Mexico Decarbonization Market By Technology

11.2.9.3 Mexico Decarbonization Market By Deployment Mode

11.2.9.4 Mexico Decarbonization Market By End-use Industry

11.3 Europe

11.3.1 Trend Analysis

11.3.2 Eastern Europe

11.3.2.1 Eastern Europe Decarbonization Market by Country

11.3.2.2 Eastern Europe Decarbonization Market By Service Type

11.3.2.3 Eastern Europe Decarbonization Market By Technology

11.3.2.4 Eastern Europe Decarbonization Market By Deployment Mode

11.3.2.5 Eastern Europe Decarbonization Market By End-use Industry

11.3.2.6 Poland

11.3.2.6.1 Poland Decarbonization Market By Service Type

11.3.2.6.2 Poland Decarbonization Market By Technology

11.3.2.6.3 Poland Decarbonization Market By Deployment Mode

11.3.2.6.4 Poland Decarbonization Market By End-use Industry

11.3.2.7 Romania

11.3.2.7.1 Romania Decarbonization Market By Service Type

11.3.2.7.2 Romania Decarbonization Market By Technology

11.3.2.7.3 Romania Decarbonization Market By Deployment Mode

11.3.2.7.4 Romania Decarbonization Market By End-use Industry

11.3.2.8 Hungary

11.3.2.8.1 Hungary Decarbonization Market By Service Type

11.3.2.8.2 Hungary Decarbonization Market By Technology

11.3.2.8.3 Hungary Decarbonization Market By Deployment Mode

11.3.2.8.4 Hungary Decarbonization Market By End-use Industry

11.3.2.9 Turkey

11.3.2.9.1 Turkey Decarbonization Market By Service Type

11.3.2.9.2 Turkey Decarbonization Market By Technology

11.3.2.9.3 Turkey Decarbonization Market By Deployment Mode

11.3.2.9.4 Turkey Decarbonization Market By End-use Industry

11.3.2.10 Rest of Eastern Europe

11.3.2.10.1 Rest of Eastern Europe Decarbonization Market By Service Type

11.3.2.10.2 Rest of Eastern Europe Decarbonization Market By Technology

11.3.2.10.3 Rest of Eastern Europe Decarbonization Market By Deployment Mode

11.3.2.10.4 Rest of Eastern Europe Decarbonization Market By End-use Industry

11.3.3 Western Europe

11.3.3.1 Western Europe Decarbonization Market by Country

11.3.3.2 Western Europe Decarbonization Market By Service Type

11.3.3.3 Western Europe Decarbonization Market By Technology

11.3.3.4 Western Europe Decarbonization Market By Deployment Mode

11.3.3.5 Western Europe Decarbonization Market By End-use Industry

11.3.3.6 Germany

11.3.3.6.1 Germany Decarbonization Market By Service Type

11.3.3.6.2 Germany Decarbonization Market By Technology

11.3.3.6.3 Germany Decarbonization Market By Deployment Mode

11.3.3.6.4 Germany Decarbonization Market By End-use Industry

11.3.3.7 France

11.3.3.7.1 France Decarbonization Market By Service Type

11.3.3.7.2 France Decarbonization Market By Technology

11.3.3.7.3 France Decarbonization Market By Deployment Mode

11.3.3.7.4 France Decarbonization Market By End-use Industry

11.3.3.8 UK

11.3.3.8.1 UK Decarbonization Market By Service Type

11.3.3.8.2 UK Decarbonization Market By Technology

11.3.3.8.3 UK Decarbonization Market By Deployment Mode

11.3.3.8.4 UK Decarbonization Market By End-use Industry

11.3.3.9 Italy

11.3.3.9.1 Italy Decarbonization Market By Service Type

11.3.3.9.2 Italy Decarbonization Market By Technology

11.3.3.9.3 Italy Decarbonization Market By Deployment Mode

11.3.3.9.4 Italy Decarbonization Market By End-use Industry

11.3.3.10 Spain

11.3.3.10.1 Spain Decarbonization Market By Service Type

11.3.3.10.2 Spain Decarbonization Market By Technology

11.3.3.10.3 Spain Decarbonization Market By Deployment Mode

11.3.3.10.4 Spain Decarbonization Market By End-use Industry

11.3.3.11 Netherlands

11.3.3.11.1 Netherlands Decarbonization Market By Service Type

11.3.3.11.2 Netherlands Decarbonization Market By Technology

11.3.3.11.3 Netherlands Decarbonization Market By Deployment Mode

11.3.3.11.4 Netherlands Decarbonization Market By End-use Industry

11.3.3.12 Switzerland

11.3.3.12.1 Switzerland Decarbonization Market By Service Type

11.3.3.12.2 Switzerland Decarbonization Market By Technology

11.3.3.12.3 Switzerland Decarbonization Market By Deployment Mode

11.3.3.12.4 Switzerland Decarbonization Market By End-use Industry

11.3.3.13 Austria

11.3.3.13.1 Austria Decarbonization Market By Service Type

11.3.3.13.2 Austria Decarbonization Market By Technology

11.3.3.13.3 Austria Decarbonization Market By Deployment Mode

11.3.3.13.4 Austria Decarbonization Market By End-use Industry

11.3.3.14 Rest of Western Europe

11.3.3.14.1 Rest of Western Europe Decarbonization Market By Service Type

11.3.3.14.2 Rest of Western Europe Decarbonization Market By Technology

11.3.3.14.3 Rest of Western Europe Decarbonization Market By Deployment Mode

11.3.3.14.4 Rest of Western Europe Decarbonization Market By End-use Industry

11.4 Asia-Pacific

11.4.1 Trend Analysis

11.4.2 Asia-Pacific Decarbonization Market by Country

11.4.3 Asia-Pacific Decarbonization Market By Service Type

11.4.4 Asia-Pacific Decarbonization Market By Technology

11.4.5 Asia-Pacific Decarbonization Market By Deployment Mode

11.4.6 Asia-Pacific Decarbonization Market By End-use Industry

11.4.7 China

11.4.7.1 China Decarbonization Market By Service Type

11.4.7.2 China Decarbonization Market By Technology

11.4.7.3 China Decarbonization Market By Deployment Mode

11.4.7.4 China Decarbonization Market By End-use Industry

11.4.8 India

11.4.8.1 India Decarbonization Market By Service Type

11.4.8.2 India Decarbonization Market By Technology

11.4.8.3 India Decarbonization Market By Deployment Mode

11.4.8.4 India Decarbonization Market By End-use Industry

11.4.9 Japan

11.4.9.1 Japan Decarbonization Market By Service Type

11.4.9.2 Japan Decarbonization Market By Technology

11.4.9.3 Japan Decarbonization Market By Deployment Mode

11.4.9.4 Japan Decarbonization Market By End-use Industry

11.4.10 South Korea

11.4.10.1 South Korea Decarbonization Market By Service Type

11.4.10.2 South Korea Decarbonization Market By Technology

11.4.10.3 South Korea Decarbonization Market By Deployment Mode

11.4.10.4 South Korea Decarbonization Market By End-use Industry

11.4.11 Vietnam

11.4.11.1 Vietnam Decarbonization Market By Service Type

11.4.11.2 Vietnam Decarbonization Market By Technology

11.4.11.3 Vietnam Decarbonization Market By Deployment Mode

11.4.11.4 Vietnam Decarbonization Market By End-use Industry

11.4.12 Singapore

11.4.12.1 Singapore Decarbonization Market By Service Type

11.4.12.2 Singapore Decarbonization Market By Technology

11.4.12.3 Singapore Decarbonization Market By Deployment Mode

11.4.12.4 Singapore Decarbonization Market By End-use Industry

11.4.13 Australia

11.4.13.1 Australia Decarbonization Market By Service Type

11.4.13.2 Australia Decarbonization Market By Technology

11.4.13.3 Australia Decarbonization Market By Deployment Mode

11.4.13.4 Australia Decarbonization Market By End-use Industry

11.4.14 Rest of Asia-Pacific

11.4.14.1 Rest of Asia-Pacific Decarbonization Market By Service Type

11.4.14.2 Rest of Asia-Pacific Decarbonization Market By Technology

11.4.14.3 Rest of Asia-Pacific Decarbonization Market By Deployment Mode

11.4.14.4 Rest of Asia-Pacific Decarbonization Market By End-use Industry

11.5 Middle East & Africa

11.5.1 Trend Analysis

11.5.2 Middle East

11.5.2.1 Middle East Decarbonization Market by Country

11.5.2.2 Middle East Decarbonization Market By Service Type

11.5.2.3 Middle East Decarbonization Market By Technology

11.5.2.4 Middle East Decarbonization Market By Deployment Mode

11.5.2.5 Middle East Decarbonization Market By End-use Industry

11.5.2.6 UAE

11.5.2.6.1 UAE Decarbonization Market By Service Type

11.5.2.6.2 UAE Decarbonization Market By Technology

11.5.2.6.3 UAE Decarbonization Market By Deployment Mode

11.5.2.6.4 UAE Decarbonization Market By End-use Industry

11.5.2.7 Egypt

11.5.2.7.1 Egypt Decarbonization Market By Service Type

11.5.2.7.2 Egypt Decarbonization Market By Technology

11.5.2.7.3 Egypt Decarbonization Market By Deployment Mode

11.5.2.7.4 Egypt Decarbonization Market By End-use Industry

11.5.2.8 Saudi Arabia

11.5.2.8.1 Saudi Arabia Decarbonization Market By Service Type

11.5.2.8.2 Saudi Arabia Decarbonization Market By Technology

11.5.2.8.3 Saudi Arabia Decarbonization Market By Deployment Mode

11.5.2.8.4 Saudi Arabia Decarbonization Market By End-use Industry

11.5.2.9 Qatar

11.5.2.9.1 Qatar Decarbonization Market By Service Type

11.5.2.9.2 Qatar Decarbonization Market By Technology

11.5.2.9.3 Qatar Decarbonization Market By Deployment Mode

11.5.2.9.4 Qatar Decarbonization Market By End-use Industry

11.5.2.10 Rest of Middle East

11.5.2.10.1 Rest of Middle East Decarbonization Market By Service Type

11.5.2.10.2 Rest of Middle East Decarbonization Market By Technology

11.5.2.10.3 Rest of Middle East Decarbonization Market By Deployment Mode

11.5.2.10.4 Rest of Middle East Decarbonization Market By End-use Industry

11.5.3 Africa

11.5.3.1 Africa Decarbonization Market by Country

11.5.3.2 Africa Decarbonization Market By Service Type

11.5.3.3 Africa Decarbonization Market By Technology

11.5.3.4 Africa Decarbonization Market By Deployment Mode

11.5.3.5 Africa Decarbonization Market By End-use Industry

11.5.3.6 Nigeria

11.5.3.6.1 Nigeria Decarbonization Market By Service Type

11.5.3.6.2 Nigeria Decarbonization Market By Technology

11.5.3.6.3 Nigeria Decarbonization Market By Deployment Mode

11.5.3.6.4 Nigeria Decarbonization Market By End-use Industry

11.5.3.7 South Africa

11.5.3.7.1 South Africa Decarbonization Market By Service Type

11.5.3.7.2 South Africa Decarbonization Market By Technology

11.5.3.7.3 South Africa Decarbonization Market By Deployment Mode

11.5.3.7.4 South Africa Decarbonization Market By End-use Industry

11.5.3.8 Rest of Africa

11.5.3.8.1 Rest of Africa Decarbonization Market By Service Type

11.5.3.8.2 Rest of Africa Decarbonization Market By Technology

11.5.3.8.3 Rest of Africa Decarbonization Market By Deployment Mode

11.5.3.8.4 Rest of Africa Decarbonization Market By End-use Industry

11.6 Latin America

11.6.1 Trend Analysis

11.6.2 Latin America Decarbonization Market by Country

11.6.3 Latin America Decarbonization Market By Service Type

11.6.4 Latin America Decarbonization Market By Technology

11.6.5 Latin America Decarbonization Market By Deployment Mode

11.6.6 Latin America Decarbonization Market By End-use Industry

11.6.7 Brazil

11.6.7.1 Brazil Decarbonization Market By Service Type

11.6.7.2 Brazil Decarbonization Market By Technology

11.6.7.3 Brazil Decarbonization Market By Deployment Mode

11.6.7.4 Brazil Decarbonization Market By End-use Industry

11.6.8 Argentina

11.6.8.1 Argentina Decarbonization Market By Service Type

11.6.8.2 Argentina Decarbonization Market By Technology

11.6.8.3 Argentina Decarbonization Market By Deployment Mode

11.6.8.4 Argentina Decarbonization Market By End-use Industry

11.6.9 Colombia

11.6.9.1 Colombia Decarbonization Market By Service Type

11.6.9.2 Colombia Decarbonization Market By Technology

11.6.9.3 Colombia Decarbonization Market By Deployment Mode

11.6.9.4 Colombia Decarbonization Market By End-use Industry

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Decarbonization Market By Service Type

11.6.10.2 Rest of Latin America Decarbonization Market By Technology

11.6.10.3 Rest of Latin America Decarbonization Market By Deployment Mode

11.6.10.4 Rest of Latin America Decarbonization Market By End-use Industry

12. Company Profiles

12.1 ABB Ltd.

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 The SNS View

12.2 Accenture

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 The SNS View

12.3 Atos SE

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 The SNS View

12.4 Bosch Thermotechnology

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 The SNS View

12.5 BP plc

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 The SNS View

12.6 Chevron Corporation

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 The SNS View

12.7 Deloitte

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 The SNS View

12.8 Enel S.p.A.

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 The SNS View

12.9 General Electric Company (GE)

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 The SNS View

12.10 Hitachi, Ltd.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 The SNS View

12.11 IBM

12.11.1 Company Overview

12.11.2 Financial

12.11.3 Products/ Services Offered

12.11.4 The SNS View

12.12 Johnson Controls International plc

12.12.1 Company Overview

12.12.2 Financial

12.12.3 Products/ Services Offered

12.12.4 The SNS View

12.13 Mitsubishi Heavy Industries, Ltd.

12.13.1 Company Overview

12.13.2 Financial

12.13.3 Products/ Services Offered

12.13.4 The SNS View

12.14 Orsted A/S

12.14.1 Company Overview

12.14.2 Financial

12.14.3 Products/ Services Offered

12.14.4 The SNS View

12.15 SAP SE

12.15.1 Company Overview

12.15.2 Financial

12.15.3 Products/ Services Offered

12.15.4 The SNS View

12.16 Schneider Electric SE

12.16.1 Company Overview

12.16.2 Financial

12.16.3 Products/ Services Offered

12.16.4 The SNS View

12.17 Siemens AG

12.17.1 Company Overview

12.17.2 Financial

12.17.3 Products/ Services Offered

12.17.4 The SNS View

12.18 Tesla Inc.

12.18.1 Company Overview

12.18.2 Financial

12.18.3 Products/ Services Offered

12.18.4 The SNS View

12.19 TotalEnergies SE

12.19.1 Company Overview

12.19.2 Financial

12.19.3 Products/ Services Offered

12.19.4 The SNS View

12.20 Toyota Motor Corporation

12.20.1 Company Overview

12.20.2 Financial

12.20.3 Products/ Services Offered

12.20.4 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. Use Case and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Service Type

Carbon Accounting and Reporting

Sustainable Transportation

Waste Reduction and Circular Economy

By Technology

Renewable Energy Technologies

Energy Efficiency Solutions

Electric Vehicles (EVs)

Carbon Removal Technologies

Carbon Capture and Storage (CCS)

By Deployment Mode

Cloud

On-premises

By End-use Industry

Oil & Gas

Energy and Utility

Agriculture

Government

Automotive & Transportation

Aerospace & Defense

Manufacturing

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Chondroitin Sulfate Market Size was valued at USD 1.3 Billion in 2023 and is expected to reach USD 1.7 Billion by 2032 and grow at a CAGR of 3.4% over the forecast period 2024-2032.

The Lab-Grown Diamonds Market was valued at USD 26.30 billion in 2023 and is projected to reach USD 60.51 billion by 2032, growing at a CAGR of 9.7% during the forecast period from 2024 to 2032.

The Surfactants Market Size was valued at USD 48.2 billion in 2023 and is expected to reach USD 72.2 billion by 2032 and grow at a CAGR of 4.6% over the forecast period 2024-2032.

The Composite Resin Market Size was USD 24.62 billion in 2023 & is expected to reach USD 41.74 billion by 2032 & grow at a CAGR of 6.04% by 2024-2032.

The Thin Film Material Market size was USD 13.25 billion in 2023 and is expected to Reach USD 18.99 billion by 2031 and grow at a CAGR of 4.6% over the forecast period of 2024-2031.

The Agricultural Textiles Market was valued at USD 15.8 billion in 2023 and will reach USD 24.3 billion by 2032 and grow at a CAGR of 4.9% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd