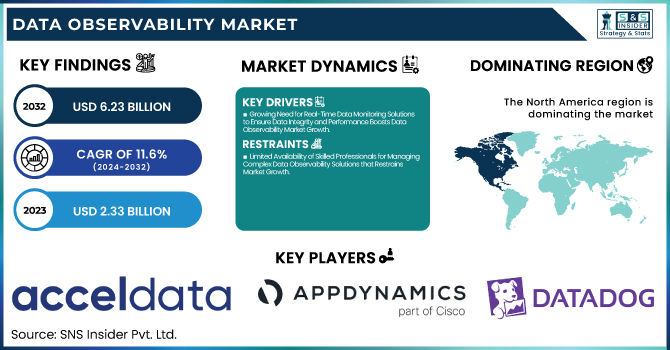

The Data Observability Market Size was valued at USD 2.33 Billion in 2023 and is expected to reach USD 6.23 Billion by 2032 and grow at a CAGR of 11.6% over the forecast period 2024-2032.

To Get more information on Data Observability Market - Request Free Sample Report

The market is a rapidly evolving segment within the broader data management and analytics industry, driven by the increasing reliance on data for decision-making across various sectors. It enables businesses to monitor, track, and ensure the health of their data systems, providing insights into data quality, availability, and performance. As the volume, variety, and velocity of data continue to surge, the need for robust monitoring tools that can handle complex data environments becomes crucial. The market’s expansion is further fueled by the rising demand for automated solutions that improve operational efficiency and reduce manual efforts.

The U.S. Data Observability Market size was USD 0.71 billion in 2023 and is expected to reach USD 1.71 billion by 2032, growing at a CAGR of 10.43% over the forecast period of 2024-2032.

The U.S. Data Observability Market is experiencing significant growth as organizations increasingly prioritize data monitoring and quality management. With the rising complexity of data systems and the need for real-time insights, businesses across various industries are adopting advanced observability solutions. These tools help ensure data integrity, improve performance, and enhance decision-making capabilities. As data-driven strategies continue to evolve, the demand for comprehensive data observability solutions in the U.S. is expected to grow, supporting the market's expansion in the coming years.

Key Drivers:

Growing Need for Real-Time Data Monitoring Solutions to Ensure Data Integrity and Performance Boosts Data Observability Market Growth

The growing need for real-time data monitoring is a key driver of the data observability market’s growth. As organizations increasingly rely on data for decision-making, they require real-time insights into the health, availability, and performance of their data systems. Real-time monitoring enables businesses to detect and resolve issues promptly, minimizing downtime and ensuring smooth operations. This need is particularly important in sectors such as finance, healthcare, and e-commerce, where even a minor data failure can have significant consequences.

Moreover, with the rising complexities of data environments, organizations are looking for solutions that provide automated, end-to-end monitoring capabilities. As the volume and diversity of data continue to increase, the demand for effective and efficient real-time data monitoring solutions is expected to rise, fueling market expansion. With advancements in AI and machine learning technologies, these observability tools are becoming more predictive, further boosting the growth of the market.

Restrain:

Limited Availability of Skilled Professionals for Managing Complex Data Observability Solutions that Restrains Market Growth

Data observability solutions are often complex, requiring specialized expertise to implement, maintain, and optimize. Organizations face challenges in finding talent with the right skill set to manage these tools effectively. This talent shortage hampers the widespread adoption of observability solutions, particularly among small and medium-sized enterprises (SMEs) that may not have the resources to hire and retain highly skilled professionals. The demand for expertise in areas such as machine learning, AI, and cloud computing, which are critical components of modern data observability tools, only exacerbates the issue.

The complexity of integrating these solutions into existing IT infrastructures also adds to the challenge, further delaying deployment and adoption. While the industry is actively working on simplifying these tools, the skills gap remains a significant barrier. Without sufficient expertise to optimize these solutions, organizations risk not fully capitalizing on the potential benefits of data observability, leading to slower market adoption in certain regions and industries.

Opportunity:

Integration of AI and Machine Learning Technologies Presents Significant Opportunity for Advancing Data Observability Capabilities

The integration of AI and machine learning technologies into data observability tools presents a tremendous opportunity for the market. As organizations continue to generate vast amounts of data, it becomes increasingly difficult to monitor, manage, and ensure the quality of this data without advanced technologies. AI and machine learning can automate anomaly detection, identify patterns, and predict potential data issues before they occur, significantly improving the efficiency of observability solutions.

Moreover, AI-driven observability tools can continuously learn from data patterns, improving their accuracy and adaptability over time. As industries such as finance, healthcare, and retail adopt these advanced technologies, the demand for AI-powered data observability solutions is expected to rise, presenting substantial growth opportunities for vendors. Furthermore, these tools can help organizations enhance data security, optimize performance, and improve compliance with regulatory standards, making them an invaluable asset in today’s data-driven world.

Challenges:

Data Privacy and Security Concerns Present Significant Challenges in Adopting Data Observability Solutions

As organizations implement observability tools to monitor and analyze their data, they expose sensitive and proprietary information to potential risks. Given that observability tools often need access to vast amounts of data across multiple platforms, ensuring that this data is protected from breaches, unauthorized access, and cyberattacks is a major challenge. Many businesses are concerned about how observability solutions can maintain the confidentiality and security of their data, especially when using third-party vendors or cloud-based platforms.

Additionally, the regulatory landscape surrounding data privacy is becoming more stringent, with frameworks like GDPR and CCPA requiring organizations to meet specific compliance standards. Ensuring that observability tools are compliant with these regulations while providing real-time insights can be a delicate balancing act. As organizations increasingly prioritize data security, the challenge lies in finding observability solutions that can offer effective monitoring without compromising data privacy. Addressing these concerns will be critical for the continued growth and adoption of data observability solutions across industries.

By Component

In 2023, the Solution segment of the data observability market accounted for the largest revenue share, standing at 62%. This is primarily due to the increased demand for end-to-end monitoring solutions that ensure the health and reliability of data systems. Several companies have introduced innovative product developments in this area. For instance, companies like Datadog and Splunk have launched new observability tools focused on improving data monitoring capabilities across cloud environments. Their solutions use machine learning to automatically detect and resolve data issues, driving the demand for such tools. The growth of digital transformation initiatives across various sectors has fueled the widespread adoption of these solutions.

The Services segment within the data observability market is anticipated to grow at the highest CAGR of 12.5% during the forecast period. The demand for implementation, consulting, and managed services is rising as businesses seek expert guidance to adopt data observability tools. Leading firms like IBM and Accenture are launching tailored services to help organizations transition to observability-driven data management systems.

Additionally, managed services are gaining traction due to the increasing complexity of data environments. Outsourcing data observability to experts allows organizations to focus on core business operations while experts handle the data monitoring, troubleshooting, and analytics. As the market for data observability services grows, these offerings will become essential for businesses that need to maintain high data quality standards.

By Deployment

The Public Cloud deployment segment is the dominant force in the data observability market in 2023, commanding the largest revenue share. Public cloud services like AWS, Microsoft Azure, and Google Cloud provide the scalability and flexibility needed for data observability solutions. Their adoption enables businesses to scale their data monitoring capabilities according to demand without the need for extensive on-premise infrastructure. These cloud platforms also offer integrated AI and machine learning tools to enhance observability functionalities. With growing digitalization, organizations are increasingly adopting public cloud solutions for their data analytics and management needs, driving the demand for cloud-based observability tools.

The Private Cloud segment is expected to grow at the highest CAGR during the forecast period in the data observability market. Organizations concerned about data privacy and control are shifting toward private cloud solutions for their observability needs. This segment allows businesses to maintain the dedicated infrastructure that is secure and compliant with data governance regulations. Companies such as Oracle and IBM have introduced private cloud solutions that offer enhanced data observability features tailored to the needs of enterprises in regulated industries like finance and healthcare. As businesses increasingly prioritize security and regulatory compliance, the private cloud segment is set to gain substantial traction, providing growth opportunities for both software vendors and service providers in the market.

By End-Use

The BFSI sector holds the largest share of the data observability market, representing 32% of total revenue in 2023. This sector has increasingly adopted data observability solutions to improve data quality, reduce fraud, and enhance regulatory compliance. Financial institutions like JPMorgan and Bank of America are leveraging advanced data observability tools to ensure the health of their vast data ecosystems, which include sensitive customer information. With the growing complexity of financial transactions and regulatory requirements, data observability plays a critical role in maintaining high levels of data integrity. As more organizations in the BFSI sector prioritize data-driven decision-making, the demand for observability solutions is expected to rise, further solidifying this sector's dominant position in the market.

The IT & Telecom segment is anticipated to grow at the highest CAGR of 12.6% within the forecast period in the data observability market. With the rise of digital transformation and increased data traffic, the IT & telecom sectors are heavily investing in observability tools to ensure optimal data performance. Leading companies like Cisco and Ericsson are enhancing their data observability offerings to improve the performance of networks and infrastructure. These tools help manage the high volumes of data generated by telecommunications networks, ensuring uptime and service continuity. As the demand for faster and more reliable data services grows, the IT & telecom segment will continue to lead in terms of growth rate, creating significant opportunities for service providers in the data observability space.

North America was the dominant region in the data observability market in 2023, with an estimated market share of over 43%. The region's dominance is driven by the high adoption of advanced technologies and the presence of key players like Splunk, Datadog, and New Relic. These companies have introduced cutting-edge solutions that help businesses improve data monitoring and troubleshooting. Additionally, the strong regulatory framework in the U.S. and Canada, particularly around data privacy and security, has accelerated the adoption of observability solutions. The increasing focus on cloud-based data solutions and AI-driven technologies further strengthens North America's position as the leading region in the market.

Asia Pacific is the fastest-growing region in the data observability market, with a projected CAGR of 12.9% during the forecast period. The rapid digitalization in countries like China, India, and Japan is a significant driver of this growth. As businesses in these regions undergo digital transformation, the need for data observability solutions to ensure data quality, availability, and performance becomes critical. The rise of e-commerce, fintech, and cloud computing in the region has led to a surge in demand for observability tools that can manage complex data systems. With increasing investments in AI and machine learning technologies, the Asia Pacific market is poised for exponential growth, creating ample opportunities for vendors to expand their presence.

Get Customized Report as per Your Business Requirement - Enquiry Now

Acceldata (Acceldata Platform, Acceldata Data Observability)

AppDynamics (AppDynamics Performance Monitoring, AppDynamics Business iQ)

Datadog (Datadog Log Management, Datadog Cloud Security Platform)

Dynatrace LLC (Dynatrace Smart Cloud Monitoring, Dynatrace AI-Powered Observability)

Hound Technology, Inc. (Hound Platform, Hound Data Solutions)

International Business Machines Corporation (IBM) (IBM Watson Studio, IBM Observability Platform)

Microsoft (Microsoft Azure Monitor, Microsoft Power BI)

Monte Carlo (Monte Carlo Data Observability, Monte Carlo Data Quality Management)

New Relic, Inc. (New Relic One, New Relic Infrastructure Monitoring)

Splunk Inc. (Splunk Enterprise, Splunk Observability Cloud)

In March 2024, AppDynamics enhanced its platform's observability capabilities by integrating advanced AI-driven insights, allowing organizations to proactively identify issues across their entire tech stack. This integration enables quicker resolution of data issues, ensuring better business continuity

In 2024, Dynatrace launched a next-gen version of its observability platform, incorporating deeper AI and machine learning features for better root cause analysis. This upgrade is set to optimize data flows, allowing enterprises to predict and fix issues before they impact business operations

In October 2023, Acceldata reported significant growth, achieving 150% year-over-year revenue growth and expanding its customer base with major Fortune 500 clients. The company also raised an additional USD 10 million in Series C funding, bringing the total to over USD 100 million. This momentum is supporting its product innovation and market expansion.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 2.33 Billion |

| Market Size by 2032 | US$ 6.23 Billion |

| CAGR | CAGR of 11.6 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (Public Cloud, Private Cloud) • By End Use (BFSI, IT & Telecom, Government & Public Sector, Energy & Utility, Manufacturing, Healthcare & Life Sciences, Retail & Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Acceldata, AppDynamics, Datadog, Dynatrace LLC, Hound Technology, Inc., International Business Machines Corporation (IBM), Microsoft, Monte Carlo, New Relic, Inc., Splunk Inc. |

Ans: The Data Observability Market is expected to grow at a CAGR of 11.6% during 2024-2032.

Ans: The Data Observability Market size was USD 2.33 billion in 2023 and is expected to reach USD 6.23 billion by 2032.

Ans: The major growth factor of the Data Observability Market is the increasing need for real-time monitoring and management of complex data systems to ensure data quality and performance.

Ans: The Public Cloud segment dominated the Data Observability Market.

Ans: North America dominated the Data Observability Market in 2023.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trend Reporting

5.1 Investment and Funding Trend

5.2 Customer Satisfaction and Retention Rates

5.3 Regulatory Compliance and Adoption

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Data Observability Market Segmentation, By Component

7.1 Chapter Overview

7.2 Solutions

7.2.1 Solutions Market Trend Analysis (2020-2032)

7.2.2 Solutions Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Services

7.3.1 Services Market Trend Analysis (2020-2032)

7.3.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Data Observability Market Segmentation, By Deployment

8.1 Chapter Overview

8.2 Public Cloud

8.2.1 Public Cloud Market Trend Analysis (2020-2032)

8.2.2 Public Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Private Cloud

8.3.1 Private Cloud Market Trend Analysis (2020-2032)

8.3.2 Private Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Data Observability Market Segmentation, By End-Use

9.1 Chapter Overview

9.2 BFSI

9.2.1 BFSI Market Trend Analysis (2020-2032)

9.2.2 BFSI Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 IT & Telecom

9.3.1 IT & Telecom Market Trend Analysis (2020-2032)

9.3.2 IT & Telecom Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Government & Public Sector

9.4.1 Government & Public Sector Market Trend Analysis (2020-2032)

9.4.2 Government & Public Sector Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Energy & Utility

9.5.1 Energy & Utility Market Trend Analysis (2020-2032)

9.5.2 Energy & Utility Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Manufacturing

9.6.1 Manufacturing Market Trend Analysis (2020-2032)

9.6.2 Manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

9.7 Healthcare & Life Science

9.7.1 Healthcare & Life Science Market Trend Analysis (2020-2032)

9.7.2 Healthcare & Life Science Market Size Estimates and Forecasts to 2032 (USD Billion)

9.8 Retail & Consumer Goods

9.8.1 Retail & Consumer Goods Market Trend Analysis (2020-2032)

9.8.2 Retail & Consumer Goods Market Size Estimates and Forecasts to 2032 (USD Billion)

9.9 Others

9.9.1 Others Market Trend Analysis (2020-2032)

9.9.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trend Analysis

10.2.2 North America Data Observability Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

10.2.3 North America Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.2.4 North America Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.2.5 North America Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.2.6.2 USA Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.2.6.3 USA Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.2.7.2 Canada Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.2.7.3 Canada Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.2.8.2 Mexico Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.2.8.3 Mexico Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trend Analysis

10.3.1.2 Eastern Europe Data Observability Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.1.6.2 Poland Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.1.6.3 Poland Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.1.7.2 Romania Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.1.7.3 Romania Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trend Analysis

10.3.2.2 Western Europe Data Observability Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.4 Western Europe Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.5 Western Europe Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.6.2 Germany Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.6.3 Germany Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.7.2 France Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.7.3 France Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.8.2 UK Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.8.3 UK Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.9.2 Italy Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.9.3 Italy Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.10.2 Spain Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.10.3 Spain Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.13.2 Austria Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.13.3 Austria Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trend Analysis

10.4.2 Asia Pacific Data Observability Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

10.4.3 Asia Pacific Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.4 Asia Pacific Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.5 Asia Pacific Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.6.2 China Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.6.3 China Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.7.2 India Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.7.3 India Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.8.2 Japan Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.8.3 Japan Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.9.2 South Korea Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.9.3 South Korea Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.10.2 Vietnam Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.10.3 Vietnam Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.11.2 Singapore Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.11.3 Singapore Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.12.2 Australia Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.12.3 Australia Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia Pacific Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia Pacific Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trend Analysis

10.5.1.2 Middle East Data Observability Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.1.4 Middle East Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.1.5 Middle East Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.1.6.2 UAE Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.1.6.3 UAE Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trend Analysis

10.5.2.2 Africa Data Observability Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.2.4 Africa Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.2.5 Africa Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trend Analysis

10.6.2 Latin America Data Observability Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

10.6.3 Latin America Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.6.4 Latin America Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.6.5 Latin America Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.6.6.2 Brazil Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.6.6.3 Brazil Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.6.7.2 Argentina Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.6.7.3 Argentina Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.6.8.2 Colombia Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.6.8.3 Colombia Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Data Observability Market Estimates and Forecasts By Component (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Data Observability Market Estimates and Forecasts By Deployment (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Data Observability Market Estimates and Forecasts By End-Use (2020-2032) (USD Billion)

11. Company Profiles

11.1 Acceldata

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 AppDynamics

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Datadog

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Dynatrace LLC.

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Hound Technology, Inc.

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 International Business Machines Corporation

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Microsoft

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Monte Carlo

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 New Relic, Inc.

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Splunk Inc.

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Component

Solutions

Services

By Deployment

Public Cloud

Private Cloud

By End-use

BFSI

IT & Telecom

Government & Public Sector

Energy & Utility

Manufacturing

Healthcare & Life Science

Retail & Consumer Goods

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

Cloud Infrastructure Services Market size was valued at USD 289.7 Bn in 2023 and is expected to reach USD 784.2 Bn by 2032 and grow at a CAGR of 11.7 % over the forecast period 2024-2032.

The Metaverse in Gaming Market Size was valued at USD 21.6 billion in 2023 and will reach USD 390.6 Billion by 2032, growing at a CAGR of 37.92% by 2032.

The Game Engines Market is anticipated to be worth USD 2.80 billion in 2023 and is expected to reach USD 11.69 billion by 2032, growing at a CAGR of 17.2% over the forecast period 2024-2032.

The Green IT Services Market was valued at USD 18.8 Billion in 2023 and is expected to reach USD 69.4 Billion by 2032, growing at a CAGR of 15.65% from 2024-2032.

POS Security Market was valued at USD 4.55 billion in 2023 and is expected to reach USD 9.99 billion by 2032, growing at a CAGR of 9.16% from 2024-2032.

The Cloud Microservices Market Size was valued at USD 1.71 billion in 2023 and is expected to reach USD 9.77 billion by 2032 and grow at a CAGR of 21.4% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd