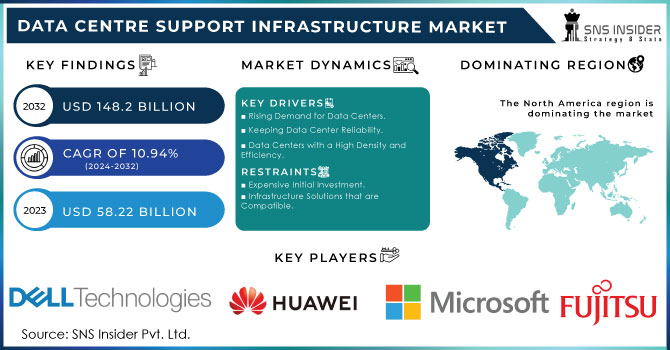

The Data Center Support Infrastructure Market Size was valued at USD 55.98 Billion in 2023 and is expected to reach USD 126.87 Billion by 2032 and grow at a CAGR of 9.6% over the forecast period 2024-2032.

The Data Center Support Infrastructure Market is evolving rapidly, driven by the surging demand for high-performance computing, cloud storage, and increased internet penetration. In addition to conventional metrics, key statistical insights include the average power usage effectiveness (PUE) across facilities, which has improved from 1.67 in 2013 to around 1.55 in recent years, indicating better energy efficiency. Another vital parameter is the uptime reliability rate, with Tier IV data centers offering 99.995% availability, reducing potential annual downtime to just 26.3 minutes. The market also reflects growth in rack density, now averaging over 8kW per rack in enterprise setups, pushing investments in advanced cooling systems. Environmental metrics like carbon footprint per megawatt are also increasingly tracked as sustainability becomes a strategic priority.

Get more information on Data Centre Support Infrastructure Market - Request Sample Report

The U.S. Data Center Support Infrastructure Market size was USD 15.04 billion in 2023 and is expected to reach USD 30.48 billion by 2032, growing at a CAGR of 8.23% over the forecast period of 2024–2032.

The U.S. Data Center Support Infrastructure Market is experiencing steady growth, driven by the increasing demand for reliable, scalable, and energy-efficient data center environments. As digital transformation accelerates across industries, the need for advanced cooling systems, power management solutions, and security infrastructure is on the rise. The adoption of edge computing, AI, and cloud services further fuels the market, prompting continuous infrastructure upgrades. Emphasis on sustainability and operational efficiency is also influencing investment in greener technologies. Additionally, the integration of smart monitoring and DCIM tools is enhancing infrastructure performance and visibility across data center operations.

Key Drivers:

Rising Adoption of Cloud Computing and AI Technologies Drives Growth of the Data Center Support Infrastructure Market

The rapid adoption of cloud computing, big data analytics, and artificial intelligence across industries is significantly driving the demand for robust data center support infrastructure. Enterprises are increasingly relying on digital platforms to manage and store enormous volumes of data, which requires reliable, scalable, and secure data center environments. This surge in digital dependency has fueled investments in support systems such as precision cooling, UPS systems, rack solutions, and intelligent power distribution units. Additionally, hyperscale data centers and colocation facilities are expanding to accommodate the needs of global cloud providers. These developments demand advanced infrastructure capable of ensuring high uptime, energy efficiency, and operational stability. As organizations modernize their IT ecosystems, the need for high-performance support systems continues to escalate. This ongoing transformation is positioning data center support infrastructure as a foundational element in enabling business continuity, high-speed connectivity, and data-driven decision-making across the digital economy.

Restrains:

High Capital and Operational Expenditure Restrains Expansion of the Data Center Support Infrastructure Market

Despite the market’s growth, the high capital investment required for developing and maintaining advanced data center support infrastructure is a significant restraint. Establishing a new data center or upgrading existing infrastructure entails substantial costs, including those for power systems, cooling equipment, physical security, and monitoring tools. Moreover, operational expenditures such as energy consumption, regular maintenance, skilled labor, and compliance with regulatory standards can strain budgets, particularly for small and medium-sized enterprises. These costs may deter potential entrants and slow down expansion plans for existing providers, especially in developing regions.

Additionally, the return on investment for data center infrastructure often unfolds over a longer period, making it less appealing for short-term-focused investors. Financial barriers, combined with the complexity of managing integrated infrastructure systems, pose considerable challenges. As a result, some businesses may opt for cloud services or colocation facilities, reducing direct demand for standalone support infrastructure solutions.

Opportunities:

Rising Emphasis on Sustainability and Energy Efficiency Creates New Opportunities in the Data Center Support Infrastructure Market

Growing environmental awareness and stringent sustainability regulations are creating promising opportunities for innovation in the data center support infrastructure market. Organizations are under increasing pressure to reduce their carbon footprint and adopt eco-friendly practices, making energy-efficient infrastructure a top priority. This trend is driving the development and deployment of green cooling systems, advanced power management tools, and infrastructure components with lower environmental impact. Innovations like liquid cooling, renewable energy integration, and AI-driven energy optimization are being explored to enhance sustainability.

Furthermore, data center operators are investing in modular and prefabricated infrastructure that reduces material waste and speeds up deployment while offering better energy performance. This shift toward greener operations not only supports compliance with environmental standards but also helps reduce operational costs over time. Vendors that offer sustainable, future-ready solutions stand to gain a competitive edge as businesses and governments alike prioritize climate goals and long-term resource efficiency.

Challenge:

Growing Complexity In Managing Multi-Layered Infrastructure Presents A Challenge for the Data Center Support Infrastructure Market

As data centers become more complex and layered with new technologies, managing the associated support infrastructure has become a major challenge. The integration of cloud services, edge computing, IoT devices, and AI-powered operations necessitates highly sophisticated infrastructure that can support varied workloads and real-time data processing. This complexity requires advanced monitoring, predictive maintenance, and seamless coordination across power, cooling, and security systems. However, many organizations lack the internal expertise or tools to effectively manage such a dynamic environment.

Furthermore, legacy infrastructure often cannot scale or adapt to modern requirements, creating compatibility issues and operational inefficiencies. The risk of downtime due to mismanagement, cyber threats, or system overloads becomes increasingly significant as operations scale. These challenges are prompting a demand for smarter infrastructure management platforms and skilled professionals, but talent shortages and integration difficulties remain barriers to efficient infrastructure performance and reliability in the evolving digital landscape.

By Industry Vertical

The BFSI sector holds the largest revenue share in the Data Center Support Infrastructure Market, accounting for 34% in 2023. This dominance is driven by the sector’s critical need for secure, high-performance, and always-available data infrastructure to handle vast volumes of financial transactions, sensitive customer data, and real-time processing requirements. As digital banking and fintech services continue to grow, so does the need for resilient support systems, including advanced cooling, power backup, and monitoring solutions.

Moreover, banks are focusing on data center modernization with edge computing capabilities and DCIM tools to streamline operations. The demand for regulatory compliance, especially regarding data privacy and uptime, further fuels investment in robust support infrastructure, positioning BFSI as a major driver of the market's technological evolution.

The IT & Telecom segment is projected to grow at the highest CAGR of 12.1% in the Data Center Support Infrastructure Market during the forecast period. This rapid growth is propelled by the expansion of 5G networks, increased cloud adoption, and the surge in data traffic driven by mobile and internet-based services. Telecom operators and IT service providers require ultra-low latency and high-availability infrastructure to support real-time applications and continuous connectivity. Recent product developments include the launch of edge-ready modular data center support systems by industry leaders to meet the dynamic needs of telecom operators.

With data centers becoming more distributed, the IT & Telecom sector is prioritizing infrastructure that can support scalable, remote, and software-defined environments. This sector’s embrace of AI, IoT, and hybrid cloud strategies demands resilient support systems, making it a fast-emerging growth area for vendors offering next-generation data center support infrastructure solutions.

By Infrastructure

In 2023, the Power Distribution Systems segment led the Data Center Support Infrastructure Market with a dominant 32% revenue share, reflecting its critical role in ensuring seamless and reliable data center operations. As modern data centers demand uninterrupted power flow to support 24/7 workloads, scalable and intelligent power distribution has become essential. This includes advanced solutions like intelligent power distribution units (PDUs), busway systems, switchgear, and remote power panels that enable real-time energy monitoring, load balancing, and fault detection.

Notable developments include modular power solutions that offer scalability and simplified integration into existing setups, supporting growing rack densities and high-performance computing. With rising energy costs and sustainability mandates, efficient power management is a top priority for operators. Data centers are increasingly adopting renewable energy-compatible and low-loss power distribution systems to reduce operational expenditure and carbon footprint.

By Tier Level

Tier 3 data centers held the largest share of 59% in the Data Center Support Infrastructure Market in 2023, owing to their balance of performance, availability, and cost-efficiency. These facilities offer a minimum of 99.982% uptime and are designed to support concurrent maintenance without service disruption, making them ideal for enterprises seeking reliable infrastructure at a manageable cost.

Recent product innovations include modular power and cooling solutions tailored for Tier 3 standards, enabling faster deployment and lower energy consumption. Several data center providers have upgraded existing Tier 2 facilities to Tier 3, enhancing system redundancy and infrastructure resilience. As digital services scale, businesses increasingly prioritize fault tolerance and availability, making Tier 3 the go-to choice for long-term infrastructure investment.

Tier 4 data centers are projected to grow at the highest CAGR of 10.9% during the forecast period, reflecting an increased demand for ultra-reliable infrastructure in mission-critical applications. These data centers are designed for fault tolerance and offer 99.995% uptime, appealing to industries that require near-zero downtime, such as government, healthcare, and global finance. The market has seen increased activity in launching fully redundant power and cooling systems to meet Tier 4 standards. While cost remains high, the long-term benefits of reliability and operational stability are prompting greater adoption, making Tier 4 a critical growth area in the evolving data center ecosystem.

By Organization Size

Large enterprises dominated the Data Center Support Infrastructure Market with a 79% revenue share in 2023, driven by their extensive IT workloads, global operations, and stringent uptime requirements. These organizations are at the forefront of digital transformation, leveraging AI, big data, and hybrid cloud solutions that necessitate scalable and secure data center environments. To support this, they invest heavily in advanced power and cooling systems, multi-layered security, and real-time infrastructure monitoring. Many large enterprises have rolled out smart DCIM tools to optimize resource usage and reduce energy costs. Companies in sectors such as BFSI, healthcare, and e-commerce are building or upgrading Tier 3 and Tier 4 facilities with support infrastructure capable of handling mission-critical processes.

Small and medium enterprises (SMEs) are expected to grow at the highest CAGR of 11.8% in the Data Center Support Infrastructure Market over the forecast period. As digital transformation becomes accessible to smaller players, SMEs are increasingly adopting cloud computing, SaaS platforms, and data analytics tools. This trend necessitates reliable support infrastructure to ensure system uptime, data security, and scalability. The market has witnessed the introduction of cost-effective, plug-and-play modular systems specifically designed for SMEs, allowing easier and faster deployment. With limited in-house IT resources, SMEs are also leveraging DCIM-as-a-service and outsourced infrastructure management solutions. Several vendors have launched compact UPS units, edge-ready cooling systems, and integrated monitoring tools tailored for small-scale data environments.

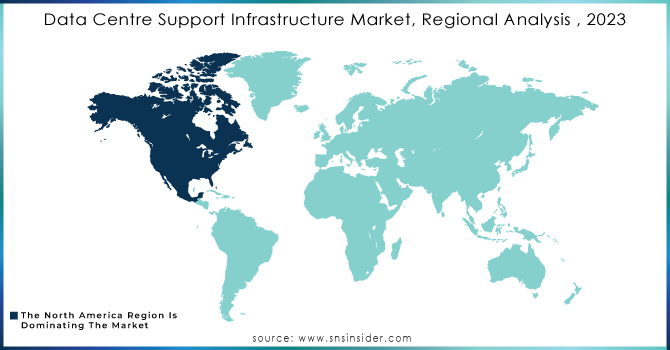

In 2023, North America dominated the Data Center Support Infrastructure Market with an estimated market share of over 38%, driven by its highly developed digital ecosystem, early adoption of advanced technologies, and presence of major cloud and colocation providers. The region is home to tech giants like Amazon Web Services (AWS), Google, Microsoft, and Meta, all of which are heavily investing in hyperscale and edge data centers. These data centers demand sophisticated power, cooling, and monitoring systems, directly fueling the growth of the support infrastructure market.

Additionally, stringent government regulations around data security and energy efficiency have accelerated the adoption of smart infrastructure solutions. For example, Equinix and Digital Realty have expanded their North American footprints with new data center campuses, integrating modular power systems and AI-powered cooling. The high concentration of enterprise IT operations, coupled with continued digital transformation across sectors such as BFSI, healthcare, and retail, reinforces North America’s leadership position in the global market.

In 2023, the Asia Pacific region emerged as the fastest-growing market, projected to expand at an impressive CAGR of around 10.6% during the forecast period. This rapid growth is driven by increased internet penetration, the rise of cloud-native businesses, government-led digital initiatives, and a growing user base demanding faster data access. Countries like China, India, Japan, and Singapore are witnessing a surge in data center development, supported by favorable regulatory policies and strategic investments.

Meanwhile, Singapore, despite space constraints, continues to be a data center hub due to its connectivity advantages and regulatory support for green infrastructure. Local players and global giants are launching modular, energy-efficient, and AI-integrated infrastructure to meet growing demands. The increasing presence of tech startups and expanding 5G networks further amplify the need for scalable and efficient support infrastructure, making the Asia Pacific a key growth engine for the market.

Need any customization on Data Centre Support Infrastructure Market - Enquiry Now

Cisco Systems Inc. (Cisco UCS Servers, Nexus Switches)

Dell Technologies Inc. (Dell PowerEdge Servers, Dell EMC PowerVault Storage)

Fujitsu Ltd. (Fujitsu PRIMERGY Servers, Fujitsu ETERNUS Storage Systems)

Hewlett Packard Enterprise Co. (HPE ProLiant Servers, HPE Nimble Storage)

Lenovo Group Ltd. (Lenovo ThinkSystem Servers, Lenovo TruScale Infrastructure Services)

Microsoft Corp. (Azure Stack HCI, Microsoft System Center)

Vertiv Group Corp. (Liebert UPS Systems, Vertiv SmartRow DCR)

Huawei Investment & Holding Co. Ltd. (Huawei FusionModule Data Center, Huawei OceanStor Storage)

IBM Corp. (IBM FlashSystem Storage, IBM Cloud Infrastructure)

Schneider Electric SE (EcoStruxure IT, Galaxy VX UPS)

Corning (EDGE Data Center Solutions, Corning Pretium EDGE HD)

Leviton (Atlas-X1 Copper Systems, Leviton Opt-X Fiber Enclosures)

Legrand (Nexpand Server Cabinets, Legrand PDUs)

Eaton (Eaton 9PX UPS, Eaton Intelligent Power Manager)

ABB (ABB PowerWave 33 UPS, ABB Data Center Automation)

February 2025: Cisco introduced the N9300 Series Smart Switches, integrating AMD Pensando Data Processing Units (DPUs). These switches aim to enhance data center architectures by embedding services directly into the network, offering improved scalability and adaptability for AI workloads.

December 2024: Dell Technologies celebrated its 40th anniversary by launching the Dell AI Factory, which includes AI PCs and GPU-enabled servers. This initiative has contributed to a 34% increase in Infrastructure Solutions Group revenue in the third quarter of 2024.

August 2023: Fujitsu was recognized as a Visionary in Gartner's Magic Quadrant for Data Center Outsourcing and Hybrid Infrastructure Managed Services. This acknowledgment reflects Fujitsu's strategic approach to Hybrid IT and its commitment to delivering transformative solutions in the data center domain.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 55.98 Billion |

| Market Size by 2032 | US$ 126.87 Billion |

| CAGR | CAGR of 9.6 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Infrastructure (Power Distribution Systems, Network and System Management, Racks and Enclosures, Site and Facility Infrastructure, Security Systems) • By Tier Level (Tier 1, Tier 2, Tier 3, Tier 4) • By Organization Size (Small and Medium Enterprises, Large Enterprises) • By Industry Vertical (BFSI, Retail, IT & Telecom, Healthcare, Energy, Government, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cisco Systems Inc., Dell Technologies Inc., Fujitsu Ltd., Hewlett Packard Enterprise Co., Lenovo Group Ltd., Microsoft Corp., Vertiv Group Corp., Huawei Investment & Holding Co. Ltd., IBM Corp., Schneider Electric SE, Corning, Leviton, Legrand, Eaton, ABB. |

Ans: The Data Center Support Infrastructure Market is expected to grow at a CAGR of 9.6% during 2024-2032.

Ans: The Data Center Support Infrastructure Market size was USD 55.98 billion in 2023 and is expected to reach USD 126.87 billion by 2032.

Ans: The major growth factor of the Data Center Support Infrastructure Market is the rising demand for scalable, energy-efficient, and high-availability infrastructure driven by cloud computing and digital transformation.

Ans: The Power Distribution Systems segment dominated the Data Center Support Infrastructure Market.

Ans: North America dominated the Data Center Support Infrastructure Market in 2023.

Table Of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Uptime and Availability Rates, 2023

5.2 Carbon Emissions & Sustainability Metrics, 2023

5.3 Renewable Energy Usage in Data Centers, 2023

5.4 Cooling Technology Penetration

6. Competitive Landscape

6.1 List of Major Companies By Region

6.2 Market Share Analysis By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Data Center Support Infrastructure Market Segmentation By Infrastructure

7.1 Chapter Overview

7.2 Power Distribution Systems

7.2.1 Power Distribution Systems Market Trends Analysis (2020-2032)

7.2.2 Power Distribution Systems Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Network and System Management

7.3.1 Network and System Management Market Trends Analysis (2020-2032)

7.3.2 Network and System Management Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Racks and Enclosures

7.4.1 Racks and Enclosures Market Trends Analysis (2020-2032)

7.4.2 Racks and Enclosures Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Site and Facility Infrastructure

7.5.1 Site and Facility Infrastructure Market Trends Analysis (2020-2032)

7.5.2 Site and Facility Infrastructure Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Security Systems

7.6.1 Security Systems Market Trends Analysis (2020-2032)

7.6.2 Security Systems Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Data Center Support Infrastructure Market Segmentation By Tier Level

8.1 Chapter Overview

8.2 Tier 1

8.2.1 Tier 1 Market Trends Analysis (2020-2032)

8.2.2 Tier 1 Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Tier 2

8.3.1 Tier 2 Market Trends Analysis (2020-2032)

8.3.2 Tier 2 Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Tier 3

8.4.1 Tier 3 Market Trends Analysis (2020-2032)

8.4.2 Tier 3 Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Tier 4

8.5.1 Tier 4 Market Trends Analysis (2020-2032)

8.5.2 Tier 4 Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Data Center Support Infrastructure Market Segmentation By Organization Size

9.1 Chapter Overview

9.2 Small and medium-sized enterprises

9.2.1 Small and medium-sized enterprises Market Trends Analysis (2020-2032)

9.2.2 Small and medium-sized enterprises Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Large enterprises

9.3.1 Large enterprises Market Trends Analysis (2020-2032)

9.3.2 Large Enterprises Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Data Center Support Infrastructure Market Segmentation By Industry vertical

10.1 Chapter Overview

10.2 Healthcare

10.2.1 Healthcare Market Trends Analysis (2020-2032)

10.2.2 Healthcare Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Retail

10.3.1 Retail Market Trend Analysis (2020-2032)

10.3.2 Retail Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 IT & Telecom

10.4.1 IT & Telecom Market Trends Analysis (2020-2032)

10.4.2 IT & Telecom Market Size Estimates and Forecasts to 2032 (USD Billion)

10.5 Manufacturing

10.5.1 Manufacturing Market Trends Analysis (2020-2032)

10.5.2 Manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

10.7 BFSI

10.7.1 BFSI Market Trends Analysis (2020-2032)

10.7.2 BFSI Market Size Estimates and Forecasts to 2032 (USD Billion)

10.8 Energy

10.8.1 Energy Market Trends Analysis (2020-2032)

10.8.2 Energy Market Size Estimates and Forecasts to 2032 (USD Billion)

10.9 Government

10.9.1 Government Market Trends Analysis (2020-2032)

10.9.2 Government Market Size Estimates and Forecasts to 2032 (USD Billion)

10.10 Others

10.10.1 Others Market Trends Analysis (2020-2032)

10.10.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trend Analysis

11.2.2 North America Data Center Support Infrastructure Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

11.2.3 North America Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.2.4 North America Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.2.5 North America Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.2.6 North America Data Center Support Infrastructure Market Estimates and Forecasts By Industry Vertical (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.2.7.2 USA Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.2.7.3 USA Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.2.7.4 USA Data Center Support Infrastructure Market Estimates and Forecasts By Industry Vertical (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.2.8.2 Canada Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.2.8.3 Canada Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.2.8.4 Canada Data Center Support Infrastructure Market Estimates and Forecasts By Industry Vertical (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.2.9.2 Mexico Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.2.9.3 Mexico Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.2.9.4 Mexico Data Center Support Infrastructure Market Estimates and Forecasts By Industry Vertical (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trend Analysis

11.3.1.2 Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Industry Vertical (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.1.7.2 Poland Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.1.7.3 Poland Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.1.7.4 Poland Data Center Support Infrastructure Market Estimates and Forecasts By Industry Vertical (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.1.8.2 Romania Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.1.8.3 Romania Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.1.8.4 Romania Data Center Support Infrastructure Market Estimates and Forecasts By Industry Vertical (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trend Analysis

11.3.2.2 Western Europe Data Center Support Infrastructure Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.4 Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.5 Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.6 Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.7.2 Germany Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.7.3 Germany Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.7.4 Germany Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.8.2 France Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.8.3 France Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.8.4 France Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.9.2 UK Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.9.3 UK Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.9.4 UK Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.10.2 Italy Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.10.3 Italy Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.10.4 Italy Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.11.2 Spain Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.11.3 Spain Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.11.4 Spain Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.14.2 Austria Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.14.3 Austria Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.14.4 Austria Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trend Analysis

11.4.2 Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.4 Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.5 Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.6 Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.7.2 China Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.7.3 China Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.7.4 China Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.8.2 India Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.8.3 India Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.8.4 India Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.9.2 Japan Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.9.3 Japan Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.9.4 Japan Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.10.2 South Korea Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.10.3 South Korea Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.10.4 South Korea Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.11.2 Vietnam Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.11.3 Vietnam Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.11.4 Vietnam Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.12.2 Singapore Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.12.3 Singapore Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.12.4 Singapore Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.13.2 Australia Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.13.3 Australia Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.13.4 Australia Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trend Analysis

11.5.1.2 Middle East Data Center Support Infrastructure Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.1.4 Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.1.5 Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.1.6 Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.1.7.2 UAE Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.1.7.3 UAE Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.1.7.4 UAE Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trend Analysis

11.5.2.2 Africa Data Center Support Infrastructure Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.2.4 Africa Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.2.5 Africa Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.2.6 Africa Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trend Analysis

11.6.2 Latin America Data Center Support Infrastructure Market Estimates and Forecasts by Country (2020-2032) (USD Billion)

11.6.3 Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.6.4 Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.6.5 Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.6.6 Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.6.7.2 Brazil Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.6.7.3 Brazil Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.6.7.4 Brazil Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.6.8.2 Argentina Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.6.8.3 Argentina Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.6.8.4 Argentina Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.6.9.2 Colombia Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.6.9.3 Colombia Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.6.9.4 Colombia Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Infrastructure (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Tier Level (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Organization Size (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Data Center Support Infrastructure Market Estimates and Forecasts By Industry vertical (2020-2032) (USD Billion)

12. Company Profiles

12.1 Cisco Systems Inc.

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Dell Technologies Inc.

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Fujitsu Ltd.

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Hewlett-Packard Enterprise Co.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Lenovo Group Ltd.

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Microsoft Corp.

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Vertiv Group Corp.

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Huawei Investment & Holding Co. Ltd.

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 IBM Corp.

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Schneider Electric SE

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Infrastructure

Power Distribution Systems

Network and System Management

Racks and Enclosures

Site and Facility Infrastructure

Security Systems

By Tier Level

Tier 1

Tier 2

Tier 3

Tier 4

By Organization size

Small and medium enterprises

Large enterprise

By Industry vertical

BFSI

Retail

IT & Telecom

Healthcare

Energy

Government

Manufacturing

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Business Intelligence (BI) software Market size was valued at USD 35.85 billion in 2023 and will grow to USD 112.4 billion and CAGR of 13.6 % by 2032.

Cloud Infrastructure Services Market size was valued at USD 289.7 Bn in 2023 and is expected to reach USD 784.2 Bn by 2032 and grow at a CAGR of 11.7 % over the forecast period 2024-2032.

Digital signage market size was valued at USD 25.52 Billion in 2023. It is expected to Reach USD 49.48 Billion by 2032 and grow at a CAGR of 7.65% over the forecast period of 2024-2032.

Embedded AI Market was valued at USD 8.79 billion in 2023 and is expected to reach USD 29.07 billion by 2032, growing at a CAGR of 14.28% from 2024-2032.

The Network Telemetry Market Size was valued at USD 420.68 Million in 2023 and is expected to reach USD 1514.99 Million by 2032 and grow at a CAGR of 15.31% over the forecast period 2024-2032.

The Workforce Management Market Size was valued at USD 8.5 Billion in 2023 and will reach USD 19.4 Billion by 2032, growing at a CAGR of 9.6% by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd