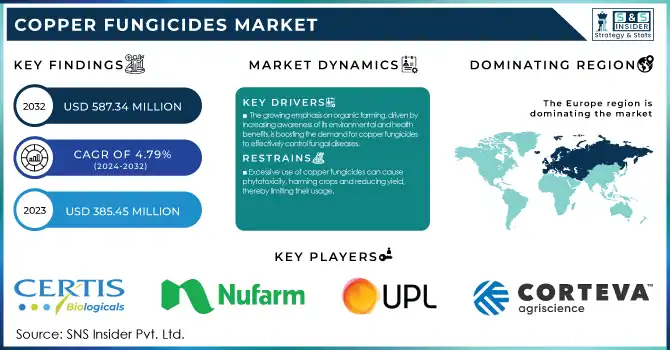

The Copper Fungicides Market size was valued at USD 385.45 million in 2023. It is expected to grow to USD 587.34 million by 2032 and grow at a CAGR of 4.79% over the forecast period of 2024-2032.

Get E-PDF Sample Report on Copper Fungicides Market - Request Sample Report

The Copper Fungicides Market is witnessing significant growth, driven by increasing demand for sustainable agricultural practices and the rising prevalence of fungal diseases in crops. Copper fungicides are widely used in the agricultural industry to control a broad spectrum of fungal and bacterial diseases in fruits, vegetables, grains, and ornamental plants. Their effectiveness, combined with their ability to enhance plant health and yield, makes them an indispensable tool for farmers globally. One of the key trends in the market is the growing adoption of organic farming. With consumers increasingly prioritizing chemical-free and sustainably produced food, organic-certified copper fungicides are gaining traction. Additionally, advancements in formulation technologies, such as the development of nanoparticle-based copper fungicides, are improving efficacy while reducing environmental impact. Another trend is the rise in integrated pest management (IPM) programs, which promote the judicious use of copper fungicides alongside other biological and mechanical methods to minimize residue levels and resistance risks.

The market is also being bolstered by government support and subsidies for agricultural inputs, particularly in developing regions, to improve food security and crop resilience. Furthermore, the increasing awareness about crop protection in regions susceptible to climatic fluctuations, such as Asia-Pacific and Latin America, is driving demand. According to research, global agricultural land under copper fungicide application has increased by over 15% in the last five years, highlighting the growing reliance on these products. Copper-based solutions account for approximately 25% of all fungicides used in fruit cultivation, emphasizing their importance in high-value crops. Leading companies are also investing in R&D to create environmentally friendly formulations that comply with stringent regulatory standards, ensuring continued market growth.

DRIVERS

The rising demand for organic farming practices is a significant growth driver for the copper fungicides market. With increasing awareness among farmers and consumers about the environmental and health benefits of organic agriculture, there has been a notable shift towards sustainable farming practices. Copper fungicides, widely accepted in organic farming, play a vital role in controlling fungal diseases such as downy mildew and leaf spots, thereby ensuring crop health and productivity. This demand is further bolstered by the growing emphasis on reducing synthetic chemical usage in agriculture due to their adverse effects on human health and the environment.

Key market trends include advancements in formulation technologies, such as nanoparticle-based copper fungicides and slow-release formulations, which improve efficacy while minimizing environmental impact. Additionally, regulatory support for organic farming in regions like Europe and North America has amplified the adoption of copper fungicides. Emerging economies, where agriculture remains a primary industry, are also witnessing increasing usage as farmers adopt organic practices to meet global export standards.

RESTRAINT

Excessive application of copper fungicides can cause phytotoxicity, a condition where high levels of copper negatively impact plants. This often manifests as leaf discoloration, wilting, or stunted growth, ultimately reducing crop quality and yield. While copper fungicides are effective in controlling fungal diseases, improper dosage or frequent usage can harm sensitive crops, making farmers cautious about their application. The risk of phytotoxicity is particularly high in humid or wet conditions, where copper residue may accumulate on plant surfaces. This limitation not only affects their effectiveness but also deters widespread adoption, especially among farmers unfamiliar with precise application techniques. As a result, balancing efficacy with safety becomes a critical challenge for users. Manufacturers are addressing this concern by developing advanced formulations with controlled release mechanisms, but the issue remains a significant restraint in the adoption of copper fungicides across the agricultural sector.

By Product

Copper Oxychloride segment dominated with the market share over 30% in 2023. This product is highly valued for its broad-spectrum fungicidal properties, making it effective against a range of fungal diseases that affect crops, particularly in agriculture. Its reliability, affordability, and versatility have led to its widespread adoption by farmers globally. Copper Oxychloride is especially favored for controlling fungal issues in fruits, vegetables, and ornamental plants. Its long history of use and proven efficacy in preventing crop damage contribute significantly to its dominant position in the market.

By Application

Fruit & Vegetables segment dominated with the market share over 40% in 2023. This is primarily due to the essential role copper fungicides play in protecting fruit and vegetable crops from a wide range of fungal diseases, which can significantly impact yield and quality. The increasing global demand for high-quality produce and the need to maintain crop health in diverse environmental conditions have driven widespread adoption of copper-based fungicides. Their effectiveness, affordability, and regulatory acceptance contribute to their extensive use in both conventional and organic farming, making this segment the leading one in the market.

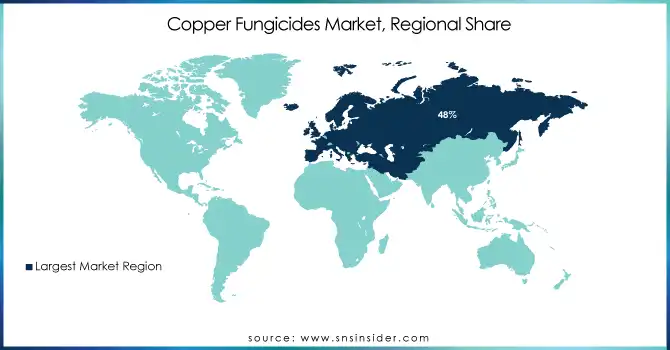

Europe region dominated with the market share over 48% in 2023, due to its well-established and highly productive agricultural sector. The region benefits from advanced farming techniques, which require effective crop protection solutions. Copper fungicides are widely used to manage plant diseases in a variety of crops, contributing to higher agricultural yields. The presence of key market players in Europe also strengthens its position, as these companies have developed and commercialized copper-based fungicides that adhere to strict regulatory standards. Furthermore, European governments support the use of copper fungicides as part of integrated pest management programs, promoting sustainable agriculture practices. The European Union’s regulatory framework ensures that copper-based products are used responsibly, balancing environmental concerns with the need for crop protection.

The Asia-Pacific region is experiencing the fastest growth in the copper fungicides market, primarily driven by the rising demand for crop protection solutions. Modern farming practices are increasingly being adopted, particularly in countries like China and India, where agricultural activities are expanding rapidly. This growth is further fueled by the need for effective pest and disease management to ensure higher crop yields. Additionally, the region's industrialization and increasing awareness of sustainable agricultural practices are boosting the usage of copper fungicides.

Get Customized Report as per your Business Requirement - Request For Customized Report

Some of the major key players of the Copper Fungicides Market

Suppliers for (Advanced crop protection and seed technology) on Copper Fungicides Market

14 November 2024: Corteva Agriscience Launches Two New Preemergence Soybean Herbicides for 2025, Corteva Agriscience introduces Kyber Pro and Sonic Boom herbicides, designed to offer multiple modes of action and extended residual activity. These products will help soybean growers combat resistant weeds like waterhemp and Palmer amaranth, ensuring optimal growth and yield potential.

In March 2023: Corteva Agriscience revealed the commercial launch of Adavel Active, an innovative fungicide that has recently been granted product registrations in Australia, Canada, and South Korea. Adavel Active is notable for its unique mode of action, offering protection against a wide range of diseases that can have a major impact on crop yields.

19 March 2024: Certis Biologicals acquired the Howler and Theia fungicides from AgBiome, enhancing its portfolio of biological pest control solutions. These products provide effective and sustainable options for high-value crops, further complementing Certis' current range of biofungicides.

| Report Attributes | Details |

| Market Size in 2023 | USD 385.45 million |

| Market Size by 2032 | USD 587.34 million |

| CAGR | CAGR of 4.79% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Chemistry (Copper Hydroxide, Copper Oxychloride, Copper Sulphate, Cuprous Oxide, and Others) • By Application (Fruits & Vegetables, Oilseeds & Pulses, Cereals & Grains, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Corteva, UPL Ltd. India, Nufarm, Certis USA LLC, Albaugh LLC, Bayer AG, Isagro S.p.A., ADAMA, Quimetal, Cosaco, Cinkarna Celje d.d., Nordox AS, FMC Corporation, BASF SE, Sumitomo Chemical, Syngenta AG, American Vanguard Corporation, Gowan Company, Limin Chemical Co. Ltd., Sharda Cropchem Limited. |

| Key Drivers | • The growing emphasis on organic farming, driven by increasing awareness of its environmental and health benefits, is boosting the demand for copper fungicides to effectively control fungal diseases. |

| RESTRAINTS | • Excessive use of copper fungicides can cause phytotoxicity, harming crops and reducing yield, thereby limiting their usage. |

Ans: Europe dominated the Copper Fungicides Market in 2023

Ans: The “Copper Oxychloride” segment dominated the Copper Fungicides Market.

Ans: The growing emphasis on organic farming, driven by increasing awareness of its environmental and health benefits, is boosting the demand for copper fungicides to effectively control fungal diseases.

Ans: The Copper Fungicides Market was USD 385.45 million in 2023 and is expected to Reach USD 587.34 million by 2032.

Ans: The Copper Fungicides Market is expected to grow at a CAGR of 4.79% during 2024-2032.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Consumption Volume

5.2 Product Demand Trends

5.3 Import & Export Data

5.4 Adoption Rate

5.5 Regulatory Impact

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Copper Fungicides Market Segmentation, By Product

7.1 Chapter Overview

7.1 Copper Oxychloride

7.1.1 Copper Oxychloride Market Trends Analysis (2020-2032)

7.1.2 Copper Oxychloride Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2 Copper Hydroxide

7.2.1 Copper Hydroxide Market Trends Analysis (2020-2032)

7.2.2 Copper Hydroxide Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Cuprous Oxide

7.3.1 Cuprous Oxide Market Trends Analysis (2020-2032)

7.3.2 Cuprous Oxide Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Copper Sulfate

7.4.1 Copper Sulfate Market Trends Analysis (2020-2032)

7.4.2 Copper Sulfate Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Other Products

7.5.1 Other Products Market Trends Analysis (2020-2032)

7.5.2 Other Products Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Copper Fungicides Market Segmentation, By Application

8.1 Chapter Overview

8.2 Fruit & Vegetables

8.2.1 Fruit & Vegetables Market Trends Analysis (2020-2032)

8.2.2 Fruit & Vegetables Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Cereals & Grains

8.3.1 Cereals & Grains Market Trends Analysis (2020-2032)

8.3.2 Cereals & Grains Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Pulses & Oilseed

8.4.1 Pulses & Oilseed Market Trends Analysis (2020-2032)

8.4.2 Pulses & Oilseed Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Other Applications

8.5.1 Other Applications Market Trends Analysis (2020-2032)

8.5.2 Other Applications Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Copper Fungicides Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.4 North America Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.5.2 USA Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.6.2 Canada Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.7.2 Mexico Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Copper Fungicides Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.5.2 Poland Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.6.2 Romania Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Copper Fungicides Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.4 Western Europe Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.5.2 Germany Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.6.2 France Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.7.2 UK Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.8.2 Italy Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.9.2 Spain Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.12.2 Austria Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4 Asia-Pacific

9.4.1 Trends Analysis

9.4.2 Asia-Pacific Copper Fungicides Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia-Pacific Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.4 Asia-Pacific Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.5.2 China Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.5.2 India Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.5.2 Japan Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.6.2 South Korea Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.2.7.2 Vietnam Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.8.2 Singapore Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.9.2 Australia Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.4.10 Rest of Asia-Pacific

9.4.10.1 Rest of Asia-Pacific Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia-Pacific Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Copper Fungicides Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.4 Middle East Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.5.2 UAE Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Copper Fungicides Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.2.4 Africa Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Copper Fungicides Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.4 Latin America Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.5.2 Brazil Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.6.2 Argentina Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.7.2 Colombia Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Copper Fungicides Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Copper Fungicides Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11. Company Profiles

11.1 Corteva

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 UPL Ltd.

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Nufarm

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Certis USA LLC

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Albaugh LLC

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 Bayer AG

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Isagro S.p.A.

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 ADAMA

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Quimetal

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Cosaco

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Product

Copper Oxychloride

Copper Hydroxide

Cuprous Oxide

Copper Sulfate

Other Products

By Application

Fruit & Vegetables

Cereals & Grains

Pulses & Oilseed

Other Applications

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The UV Curable Resins & Formulated Products Market Size was USD 5.5 billion in 2023 & will reach to $12.8 Bn by 2032 & grow at a CAGR of 9.9% by 2024-2032.

The Aromatherapy Market Size was valued at USD 7.19 Billion in 2023 and is expected to reach USD 14.55 Bn by 2032, growing at a CAGR of 18.18% over the forecast period of 2024-2032.

The Flexible Foam Market was valued at USD 45.52 Billion in 2023 and is expected to reach USD 71.75 Billion by 2032, growing at a CAGR of 5.19% from 2024-2032.

The Semiconductor Gases Market size was USD 10.38 billion in 2023 and is expected to Reach USD 19.72 billion by 2032, at a CAGR of 7.39% from 2024-2032.

The Biopolymers Market Size was valued at USD 17.5 billion in 2023 and is expected to reach USD 47.4 billion by 2032 and grow at a CAGR of 11.7% 2024-2032.

The Fly Ash Market size was USD 13.42 Billion in 2023 and is expected to reach USD 23.30 Billion by 2032, growing at a CAGR of 5.67% from 2024 to 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd