Coating Additives Market Report Scope & Overview:

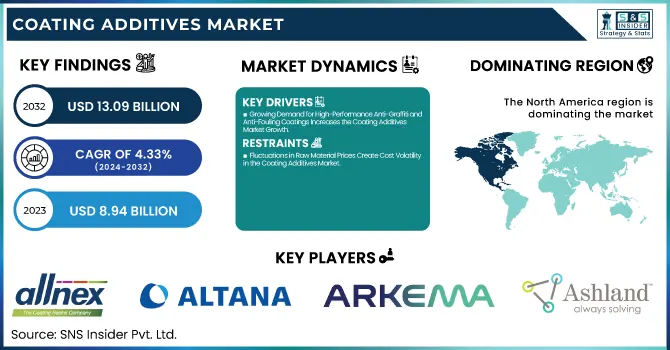

The Coating Additives Market Size was valued at USD 8.94 Billion in 2023 and is expected to reach USD 13.09 Billion by 2032, growing at a CAGR of 4.33% over the forecast period of 2024-2032.

To Get more information on Coating Additives Market - Request Free Sample Report

The Coating Additives Market is evolving with increasing investments in high-performance and eco-friendly solutions. Investment & funding trends reveal a shift toward sustainable innovations, while raw material pricing trends indicate fluctuating costs of acrylics, urethanes, and fluoropolymers, affecting profitability. Market dynamics are further shaped by economic indicators, including GDP growth, inflation, and trade policies influencing demand across key industries. A focused R&D spending analysis uncovers advancements in VOC-free and bio-based additives, driving product innovation. Additionally, the industry faces growing regulatory pressures, as highlighted in the environmental impact assessment, emphasizing sustainability and compliance with global standards. Our report offers a comprehensive analysis of these critical factors, shaping the future of coating additives.

Coating Additives Market Dynamics

Drivers

-

Growing Demand for High-Performance Anti-Graffiti and Anti-Fouling Coatings Increases the Coating Additives Market Growth

The increasing need for anti-graffiti and anti-fouling coatings in urban infrastructure, transportation, and marine applications is driving the coating additives market. Graffiti removal and biofouling pose significant maintenance challenges, leading to substantial cleaning costs and surface damage. Advanced coating additives that enhance resistance to graffiti, marine fouling, and chemical exposure are gaining traction among manufacturers. In the marine industry, anti-fouling coatings prevent the accumulation of barnacles and algae, thereby improving fuel efficiency and reducing maintenance expenses for ships and offshore structures. Similarly, municipalities and commercial property owners are adopting anti-graffiti coatings to minimize damage to public infrastructure and buildings. The demand for specialized additives that offer self-cleaning, hydrophobic, and oleophobic properties is rising, as they enable coatings to repel contaminants effectively. As urbanization and maritime trade expand globally, the need for durable, low-maintenance protective coatings will continue driving innovation in the coating additives market.

Restraints

-

Fluctuations in Raw Material Prices Create Cost Volatility in the Coating Additives Market

The coating additives market is heavily influenced by the fluctuation in raw material prices, creating cost volatility for manufacturers. The production of coating additives depends on key raw materials such as acrylics, silicones, fluoropolymers, and urethanes, which are derived from petroleum-based feedstocks. Any disruption in crude oil supply, geopolitical tensions, or trade restrictions directly impacts the pricing of these raw materials. Additionally, the industry faces challenges due to supply chain constraints and rising transportation costs, further escalating production expenses. The unpredictability in raw material availability makes it difficult for manufacturers to maintain stable pricing, often forcing them to either absorb costs or pass them on to consumers. The competitive nature of the market makes it challenging for companies to retain customers while dealing with unpredictable price surges. Unless alternative bio-based or recycled raw materials gain prominence, coating additive manufacturers will continue facing cost volatility issues.

Opportunities

-

Integration of Nanotechnology in Coating Additives Drives Innovation and Market Expansion

The integration of nanotechnology in coating additives is unlocking new possibilities for the coating additives market, driving performance enhancements and novel applications. Nanoparticle-based additives, including nano-silica, nano-alumina, and carbon nanotubes, significantly improve coating properties such as scratch resistance, UV protection, and anti-microbial functionalities. Industries such as healthcare, electronics, and automotive are increasingly adopting nano-enhanced coatings to meet high-performance standards. Moreover, self-healing and self-cleaning coatings powered by nanotechnology are gaining traction, reducing maintenance costs and improving durability. The rising investments in nanomaterials research and development create a promising landscape for manufacturers to introduce cutting-edge solutions tailored for diverse industrial applications. As demand for multi-functional coatings rises, nanotechnology-based coating additives will shape the future of the market.

Challenge

-

Intense Market Competition and Price Wars Limit Profitability in the Coating Additives Market

The coating additives market faces fierce competition, with numerous global and regional players striving for market dominance. The presence of multiple manufacturers results in aggressive pricing strategies, forcing companies to reduce profit margins to maintain competitiveness. Large corporations with extensive research capabilities and strong distribution networks hold an advantage, making it difficult for smaller players to gain significant market share. Additionally, customer demands for cost-effective yet high-performance additives add pressure on manufacturers to innovate while keeping prices competitive. The constant need to balance cost-efficiency, quality, and compliance creates a challenging business environment. To sustain profitability, companies must focus on differentiation strategies, investing in customized solutions and sustainable formulations to stand out in a crowded marketplace.

Coating Additives Market Segmental Analysis

By Product

Acrylic-based coating additives dominated the coating additives market in 2023, securing a 38.5% market share due to their excellent durability, adhesion, and resistance to weathering and UV radiation. These additives are widely used in architectural coatings, automotive finishes, industrial applications, and protective coatings, offering high-performance characteristics such as gloss retention, flexibility, and resistance to yellowing. The demand for low-VOC and water-based coatings has further fueled the growth of acrylic-based additives, as they are more compatible with environmentally friendly formulations. Organizations like the American Coatings Association (ACA) have highlighted the rising shift towards acrylic-based coatings due to their lower environmental footprint. Moreover, government initiatives such as the EU’s REACH regulations and the U.S. EPA’s VOC reduction policies have encouraged industries to transition towards waterborne acrylic-based coatings over solvent-based alternatives. Major players like BASF, Dow, and Arkema are actively investing in research and development to enhance the performance, sustainability, and cost-effectiveness of acrylic-based coating additives, further strengthening their dominance in the market.

By Formulation

Waterborne formulations dominated the coating additives market in 2023, holding a 55.7% market share, driven by growing environmental concerns, stringent regulations, and increasing consumer preference for low-VOC coatings. These formulations offer reduced toxicity, low odor, and compliance with sustainability goals, making them the preferred choice for architectural, industrial, and automotive coatings. Government regulations, such as the EPA’s Clean Air Act, China's VOC emission standards, and the European Union’s REACH regulations, have significantly impacted the market, forcing manufacturers to shift towards waterborne solutions. According to the European Coatings Council (CEPE), there has been a rapid adoption of water-based coatings across the construction and furniture industries, owing to their low environmental impact and superior performance. Additionally, technological advancements in resin and polymer chemistry have improved the performance of waterborne coatings, allowing them to match the durability and effectiveness of solvent-based alternatives. Companies like PPG Industries, Sherwin-Williams, and AkzoNobel are expanding their waterborne coating portfolios, investing in next-generation additives that enhance drying time, adhesion, and durability, ensuring continued growth in this segment.

By Application

The rheology modification segment emerged as the dominant application in the coating additives market, holding a 32.8% market share in 2023, primarily due to the growing need for enhanced viscosity control, stability, and application performance. Rheology modifiers are essential in coatings formulation, as they help in controlling flow behavior, preventing sagging, improving levelling, and optimizing film formation. These additives are widely used in architectural coatings, industrial coatings, and automotive paints, where precise viscosity control is required for uniform application, durability, and improved aesthetics. According to reports by the American Coatings Association (ACA), advancements in rheology modifier technology are enabling manufacturers to develop coatings with improved workability, anti-settling properties, and resistance to environmental fluctuations. Furthermore, government infrastructure projects and initiatives promoting high-performance coatings are accelerating the demand for rheology modification additives. Companies like Evonik, Lubrizol, and Clariant are heavily investing in advanced rheology modifiers tailored for waterborne, solvent-based, and high-solid coatings, ensuring better formulation stability and application efficiency across diverse industries.

By End-Use Industry

The architectural segment dominated the coating additives market in 2023, accounting for a 45.2% market share, fueled by rapid urbanization, infrastructure development, and stringent environmental regulations. The growing demand for durable, weather-resistant, and eco-friendly coatings in residential and commercial buildings has significantly contributed to this segment's dominance. Reports from the U.S. Green Building Council (USGBC) and European Construction Industry Federation (FIEC) highlight the increasing emphasis on energy-efficient and sustainable building materials, driving the demand for high-performance architectural coatings. Additionally, government initiatives promoting green construction, such as LEED certification standards and smart city projects, have further accelerated market growth. Leading manufacturers such as Asian Paints, AkzoNobel, and Nippon Paints are focusing on developing low-VOC, antimicrobial, and heat-reflective coatings to meet evolving regulatory and consumer demands. The shift towards smart coatings with self-cleaning, anti-microbial, and energy-saving properties is also reshaping the architectural coatings landscape, ensuring continued growth in this segment.

Coating Additives Market Regional Outlook

North America dominated the coating additives market in 2023 with a 33.4% market share, driven by strict environmental regulations, technological advancements, and strong demand across multiple industries. The United States was the largest contributor, backed by Environmental Protection Agency (EPA) mandates that promote the use of low-VOC and waterborne coatings, pushing manufacturers to develop eco-friendly and high-performance coating additives. The construction sector, valued at over $1.8 trillion, played a crucial role in increasing demand for architectural coatings, particularly in commercial and residential real estate. Additionally, the automotive industry, contributing over 3% to the U.S. GDP, saw a surge in demand for high-performance coatings, particularly for electric vehicles (EVs), where thermal management coatings and anti-corrosion additives are essential. Major coating manufacturers like Sherwin-Williams, Axalta, and PPG Industries have been expanding their production capacities and R&D investments to align with sustainability goals.

Canada followed closely, driven by the growing demand for protective coatings in its flourishing wood and furniture industry, where bio-based and anti-microbial additives are gaining traction. The country’s expanding oil and gas sector also contributed to the demand for corrosion-resistant coatings. Mexico, on the other hand, saw substantial growth due to its booming automotive manufacturing industry, where OEMs are investing in advanced coating technologies to enhance vehicle durability and fuel efficiency. With major players setting up production hubs in North America and increasing investments in next-generation coating additives, the region remains a global leader in the coating additives market.

Moreover, Asia Pacific is anticipated to be the fastest-growing region in the coating additives market, with a significant growth rate primarily driven by rapid urbanization, large-scale infrastructure projects, and increasing automotive production. China dominated the regional market, supported by government initiatives promoting green coatings and increasing investments in waterborne and high-solid formulations. According to the China National Coatings Industry Association (CNCIA), the push for low-VOC and solvent-free coatings has accelerated, prompting leading manufacturers to invest in next-generation coating additives. China’s Belt and Road Initiative (BRI) is further driving demand for protective and architectural coatings, ensuring strong growth in the coating additives sector.

India ranked as the second-largest contributor, with demand fueled by government infrastructure projects, urban housing initiatives, and the rapid expansion of the industrial sector. According to the Indian Paint Association (IPA), the Indian coatings industry is expected to grow at a double-digit rate, with manufacturers like Asian Paints and Berger Paints investing in R&D for sustainable additives. Japan and South Korea are at the forefront of innovation, particularly in automotive and marine coatings, where self-healing and anti-fouling additives are gaining traction. Leading companies like Nippon Paint and Kansai Paint are increasing R&D spending to develop coatings with enhanced durability and environmental benefits. The fast-paced industrial expansion across Asia Pacific, along with an increasing focus on sustainable and high-performance coatings, continues to drive significant demand for coating additives, making it the fastest-growing region in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Allnex GmbH (ADDITOL XL 480, CYMEL 385, MODAFLOW 2100)

-

ALTANA AG (BYK) (BYK-333, BYK-024, CERAFLOUR 996)

-

Arkema (CRAYVALLAC SLX, ORGASOL 2002 D, FLOW-AD® FX 109)

-

Ashland Inc. (NATROSOL 250, AQUAFLOW NLS 200, DREWPLUS L-3500)

-

BASF SE (DISPEX Ultra PX 4290, FOAMSTAR SI 2290, EFKA PX 4350)

-

Cabot Corporation (CAB-O-SIL TS-720, EMPEROR 1800, STERLING R)

-

Clariant AG (CERIDUST 1060, HOSTAVIN 3206, DISPERBYK 190)

-

Daikin Industries Ltd. (ZONYL 9364, POLYFLON PTFE-311, NEOSOL UF-5100)

-

Dow Inc. (DOWSIL 52 Additive, PARALOID B-82, ECOSURF EH-9)

-

Eastman Chemical Company (CAB-381-0.5, SOLUS 2100, TCH3A)

-

Elementis PLC (BENTONE SD-1, RHEOLATE 150, DAPRO W-77)

-

Evonik Industries AG (TEGO Dispers 685, AEROSIL R 974, SURFYNOL 104)

-

ICL Advanced Additives (FYROL PCF, BUDIT 380, PHOS-CHEK 745)

-

Kamin LLC (KAOPOLITE 1104, KAMIN 2000C, KAMIN HG90)

-

King Industries, Inc. (K-KAT 6212, NACURE 3525, K-FLEX XM-332)

-

Lubrizol Corporation (SOLSPERSE 27000, CARBOWAX PEG 6000, LANCOWAX PP-136)

-

Momentive Performance Materials Inc. (COATOSIL MP 200, SILWET L-77, SILQUEST A-1100)

-

MÜNZING Corporation (AGITAN 282, CERETAN MXF 9510, EDAPLAN 490)

-

Nouryon (BERMOCOLL EBS 481 FQ, SURFYNOL DF 75, EXPANCEL 920 DU)

-

Solvay (RHODOLINE 643, FLUOROLINK AD1700, ALGOHIT C40)

Recent Developments

-

March 2025: Evonik Coating Additives and Nippon Paint China collaborated to develop eco-friendly coatings, integrating Evonik’s advanced additives to enhance sustainability and performance.

-

March 2025: Evonik introduced TEGO Foamex 8420, a siloxane-based defoamer designed for waterborne inks and varnishes, ensuring long-term effectiveness and compliance with food contact regulations.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 8.94 Billion |

| Market Size by 2032 | USD 13.09 Billion |

| CAGR | CAGR of 4.33% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product (Acrylic-based, Urethane, Metallic, Fluoropolymer, Others) •By Formulation (Waterborne, Solvent-based, Others) •By Application (Rheology Modification, Biocides Impact Modification, Anti-Foaming, Wetting & Dispersion, Others) •By End Use Industry (Automotive, Architectural, Industrial, Wood & Furniture, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF SE, Dow Inc., Evonik Industries AG, ALTANA AG, Nouryon, Arkema, Clariant AG, Ashland Inc., Eastman Chemical Company, Allnex GmbH and other key players |