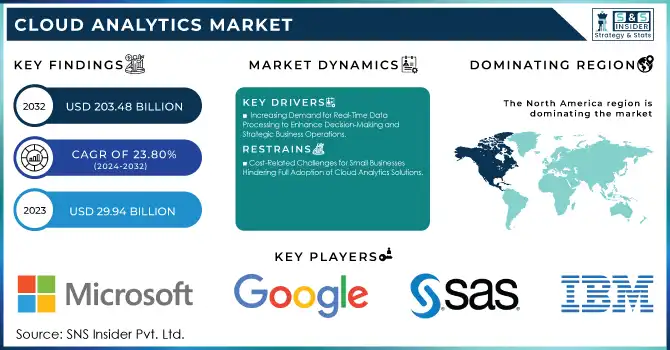

The Cloud Analytics Market was valued at USD 29.94 billion in 2023 and is expected to reach USD 203.48 billion by 2032, growing at a CAGR of 23.80% from 2024-2032.

To get more information on Cloud Analytics Market - Request Free Sample Report

The cloud analytics sector is witnessing significant expansion because of the extensive integration of cloud technologies across various sectors, as companies aim to enhance their operations and cut expenses. Studies show that employees utilize about 36 cloud services each day, while the typical enterprise depends on 1,295 cloud services, and 92% of companies have embraced a multicloud strategy. The movement towards cloud adoption is primarily motivated by the demand for scalability, flexibility, and the capability to process extensive data sets effectively. As organizations progressively acknowledge the importance of data-informed insights, cloud analytics has emerged as a vital resource for obtaining real-time intelligence, facilitating better decision-making. In September 2024, HEAVY.AI collaborated with Vultr to improve big data analytics by utilizing Vultr's powerful GPU cloud infrastructure, thereby further evolving the cloud analytics environment.

The need for cloud analytics is further heightened by its capacity to deliver real-time actionable insights, essential for sectors like healthcare, finance, and retail. These industries depend significantly on data to enhance customer interactions, optimize processes, and boost efficiency, thereby accelerating the broad uptake of cloud-based analytics tools. Additionally, cloud analytics alleviates the responsibility of managing costly on-site infrastructure, rendering it a more attainable option for small and medium-sized businesses aiming to leverage big data's potential without facing substantial initial expenses. Consequently, the scalability and affordability of cloud platforms position them as a perfect option for companies of various sizes to remain flexible and competitive in a constantly changing market.

Looking to the future, the potential for growth in cloud analytics is substantial, mainly fueled by progress in AI, machine learning, and automation, which will facilitate enhanced data processing and predictive analytics. In 2024, Qlik introduced the Qlik Talend Cloud, a fresh data integration and management platform that utilizes its latest acquisitions. This platform incorporates AI for data governance, quality, and transformation, and features a generative AI assistant for leveraging unstructured data. These advancements in technology will enable companies to discover more profound insights, resulting in wiser, data-driven decisions. Moreover, as worries regarding data privacy and security grow, the demand for cloud analytics solutions equipped with strong encryption and compliance functionalities will generate new market prospects.

Cloud Analytics Market Dynamics

Drivers

Increasing Demand for Real-Time Data Processing to Enhance Decision-Making and Strategic Business Operations

The increasing demand for real-time analytics is driving the uptake of cloud-based analytics solutions. As companies encounter a continuously growing amount of data, the capability to process and analyze information in real time has become crucial for maintaining competitiveness. Immediate insights allow organizations to make swift, data-informed decisions, adjust to market fluctuations, and enhance operational efficiency. Cloud platforms, offering scalability and processing capabilities, enable swift data ingestion, helping businesses monitor crucial metrics and respond quickly to new trends. This is especially crucial in industries such as retail, finance, and healthcare, where timely decisions can greatly influence results. Cloud analytics facilitates the smooth integration of different data sources, offering a complete perspective on performance and allowing for proactive management, thus serving as an essential tool for strategic business functions.

Rising Shift Toward Cloud Environments Boosting the Need for Scalable, Flexible, and Cost-Effective Analytics Solutions

As more businesses transition to cloud computing, there is a growing demand for cloud-based analytics tools that offer enhanced scalability, flexibility, and cost-efficiency. Cloud environments allow organizations to scale their infrastructure as needed, adapting to fluctuating data demands without the limitations of on-premise systems. This flexibility enables companies to handle diverse workloads and expand analytics capabilities with minimal investment in physical hardware. Additionally, the cost-effectiveness of cloud solutions, with their pay-as-you-go models, reduces the burden of large upfront costs while providing access to advanced analytics features. These advantages are driving businesses across industries to integrate cloud-based analytics platforms to manage their increasing data needs and optimize their operations. The shift to cloud infrastructure is thus reshaping how organizations approach data analytics, fostering innovation and efficiency in decision-making processes.

Restraints

Cost-Related Challenges for Small Businesses Hindering Full Adoption of Cloud Analytics Solutions

Although cloud analytics solutions offer significant cost benefits, small businesses may still experience concerns about the ongoing subscription costs, particularly as their data processing needs grow. As businesses scale, the amount of data they need to analyze and store increases, which can result in higher service fees and usage charges. These escalating costs may strain small business budgets, especially for companies that operate with limited resources or have fluctuating data requirements. The uncertainty around future expenses, coupled with the need to balance these costs against potential returns on investment, can deter small businesses from fully adopting cloud analytics solutions. Furthermore, small enterprises may lack the technical expertise to optimize cloud platforms for cost-efficiency, making them more vulnerable to unexpected charges as their data needs evolve. As such, managing cloud analytics costs remains a significant barrier for many smaller organizations.

Concerns Over Data Security and Privacy Impacting the Widespread Adoption of Cloud Analytics Solutions

Many organizations remain cautious about storing sensitive data on the cloud due to significant concerns about security and privacy. Fears of data breaches, unauthorized access, or loss of critical business information pose a major barrier to the adoption of cloud analytics solutions. The potential for hackers to exploit vulnerabilities in cloud platforms and the risk of mishandling or theft of data have made businesses wary, particularly in sectors like finance, healthcare, and government. Additionally, companies are often concerned about compliance with strict data protection regulations such as GDPR and HIPAA, which require stringent safeguards for sensitive information. These security and privacy risks can create reluctance among organizations to fully transition to cloud-based analytics platforms, especially when considering the potential reputational damage and financial loss resulting from a security breach. As a result, addressing these concerns is crucial to fostering broader market acceptance.

By Component

In 2023, the Solution segment dominated the Cloud Analytics Market with a significant revenue share of approximately 73%. This dominance can be attributed to the increasing reliance of businesses on cloud-based software solutions for real-time data analysis, predictive insights, and operational efficiency. As companies adopt cloud infrastructure to manage large data volumes, the demand for advanced analytics solutions that offer scalability, flexibility, and cost-effectiveness continues to rise, solidifying the solution segment’s lead in the market.

The Services segment is expected to grow at the fastest CAGR of 25.91% from 2024 to 2032. This rapid growth is driven by the increasing need for organizations to access specialized consulting, implementation, and support services to maximize the potential of cloud analytics platforms. As businesses face complex migration processes and require ongoing maintenance, the demand for expert services that ensure smooth integration, customization, and optimization of cloud analytics tools is fueling this rapid expansion in the services segment.

By Deployment

In 2023, the Public Cloud segment led the Cloud Analytics Market with the largest revenue share of approximately 48%. This dominance is primarily due to the increasing adoption of cost-effective, scalable, and flexible cloud solutions by organizations of all sizes. Public cloud platforms offer businesses the ability to access advanced analytics tools without the need for extensive infrastructure investments, making them an attractive option for companies seeking rapid data processing and storage capabilities at competitive prices.

The Hybrid Cloud segment is projected to grow at the fastest CAGR of 25.92% from 2024 to 2032. This growth is fueled by organizations seeking to balance the flexibility of public cloud services with the control and security provided by private cloud environments. The hybrid approach allows businesses to retain sensitive data on private clouds while utilizing the public cloud for less-critical operations, offering a tailored solution that addresses both security concerns and the need for scalable analytics capabilities.

By Industry Vertical

In 2023, the Banking, Financial Services, and Insurance segment dominated the Cloud Analytics Market with the highest revenue share of approximately 28%. This dominance is driven by the sector’s need for data-driven insights to enhance decision-making, manage risks, and comply with ever-evolving regulations. With large volumes of transaction and customer data to analyze, BFSI organizations are increasingly adopting cloud analytics solutions to improve operational efficiency, deliver personalized services, and gain a competitive edge in a fast-paced market.

The Healthcare and Life Sciences segment is expected to grow at the fastest CAGR of 27.32% from 2024 to 2032. The rapid expansion in this segment is fueled by the growing demand for data analytics to enhance patient care, streamline operations, and comply with strict healthcare regulations. Cloud analytics enables healthcare providers to process vast amounts of patient data in real-time, supporting predictive analytics for better diagnosis, treatment planning, and resource management, ultimately accelerating growth in the sector.

Regional Analysis

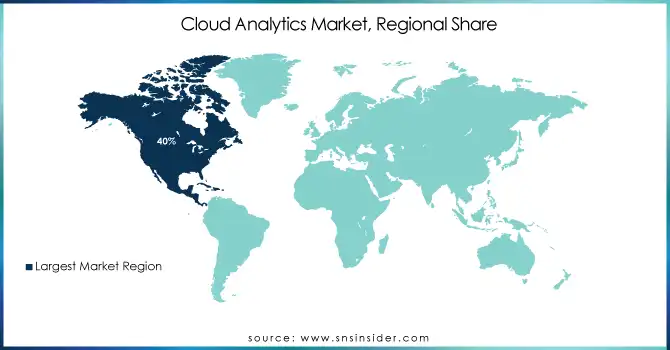

In 2023, North America dominated the Cloud Analytics Market with the largest revenue share of approximately 40%. This dominance can be attributed to the region’s early adoption of cloud technologies, the presence of major cloud service providers, and a highly developed infrastructure. The robust demand for advanced analytics solutions across industries such as BFSI, healthcare, and retail further fueled market growth, with businesses seeking innovative tools to drive operational efficiency, enhance customer experiences, and support data-driven decision-making.

Asia Pacific is projected to grow at the fastest CAGR of 25.53% from 2024 to 2032. This rapid growth is driven by the region’s accelerating digital transformation, particularly in countries like China, India, and Japan. As businesses in Asia Pacific increasingly embrace cloud technologies to improve operational agility, optimize costs, and harness the potential of big data, the demand for cloud analytics solutions continues to rise. Additionally, government initiatives promoting smart cities, e-commerce, and healthcare innovation further contribute to the region's dynamic market expansion.

Get Customized Report as per Your Business Requirement - Enquiry Now

IBM (Watson Analytics, IBM Cognos Analytics)

SAS Institute (SAS Visual Analytics, SAS Viya)

Oracle (Oracle Analytics Cloud, Oracle Autonomous Database)

Google (Google Analytics 360, Looker)

Microsoft (Power BI, Azure Synapse Analytics)

Teradata (Teradata Vantage, Teradata Cloud)

Salesforce (Tableau, Salesforce Analytics Cloud)

AWS (Amazon QuickSight, AWS Redshift)

NetApp (Cloud Insights, NetApp ONTAP)

Qlik (Qlik Sense, QlikView)

Sisense (Sisense for Cloud Data Teams, Sisense for Cloud Analytics)

SAP (SAP BusinessObjects, SAP Analytics Cloud)

Atos (Atos Analytics, Atos Digital Transformation)

Altair (Altair Smart Learning Analytics, Altair Data Analytics)

Microstrategy (MicroStrategy Cloud, MicroStrategy Analytics)

Tibco Software (TIBCO Spotfire, TIBCO Jaspersoft)

Hexaware Technologies (Hexaware Data Analytics, Hexaware Cloud Services)

Zoho (Zoho Analytics, Zoho Business Intelligence)

Rackspace Technology (Rackspace Analytics, Rackspace Data Cloud)

Splunk (Splunk Cloud, Splunk Enterprise)

Cloudera (Cloudera Data Platform, Cloudera Altus)

Domo (Domo Business Cloud, Domo Data Science)

Hewlett Packard Enterprise (HPE Ezmeral, HPE GreenLake)

Incorta (Incorta Analytics, Incorta Cloud Analytics)

Tellius (Tellius Analytics, Tellius Business Intelligence)

Rapyder (Rapyder Cloud Analytics, Rapyder Data Analytics)

Recent Developments:

In June 2024, Telefónica Tech and IBM announced a collaboration to advance AI, analytics, and data management solutions for businesses. The partnership focuses on deploying an open hybrid cloud platform, SHARK.X, and aims to accelerate digital transformation through AI-driven initiatives, including generative AI and data governance, primarily in Spain.

In September 2024, SAS highlighted the challenge of balancing cloud computing and AI innovation with sustainability goals. As AI technologies, including generative AI, become more energy-intensive, organizations are urged to optimize their data usage and infrastructure to reduce carbon emissions while advancing digital capabilities.

In September 2024, Oracle introduced the Intelligent Data Lake as part of its Data Intelligence Platform. This new feature integrates AI, cloud, and data analytics, enabling organizations to manage and analyze structured and unstructured data more effectively.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 29.94 Billion |

| Market Size by 2032 | USD 203.48 Billion |

| CAGR | CAGR of 23.80% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Organization Size (Large Enterprises, Small & Medium-Sized Enterprises) • By Deployment (Public Cloud, Private Cloud, Hybrid Cloud) • By Industry Vertical (BFSI, IT & Telecommunication, Manufacturing, Healthcare & Life Sciences, Government, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IBM, SAS Institute, Oracle, Google, Microsoft, Teradata, Salesforce, AWS, NetApp, Qlik, Sisense, SAP, Atos, Altair, Microstrategy, Tibco Software, Hexaware Technologies, Zoho, Rackspace Technology, Splunk, Cloudera, Domo, Hewlett Packard Enterprise, Incorta, Tellius, Rapyder. |

| Key Drivers | • Increasing Demand for Real-Time Data Processing to Enhance Decision-Making and Strategic Business Operations • Rising Shift Toward Cloud Environments Boosting the Need for Scalable, Flexible, and Cost-Effective Analytics Solutions |

| RESTRAINTS | • Cost-Related Challenges for Small Businesses Hindering Full Adoption of Cloud Analytics Solutions • Concerns Over Data Security and Privacy Impacting the Widespread Adoption of Cloud Analytics Solutions |

Cloud Analytics Market was valued at USD 29.94 billion in 2023 and is expected to reach USD 203.48 billion by 2032, growing at a CAGR of 23.80% from 2024-2032.

Ans: The Cloud Analytics Market is expected to grow at a CAGR of 23.80% from 2024-2032.

Ans: The Solution segment dominated the market with a 73% revenue share in 2023.

Ans: The Public Cloud segment led the market with a 48% revenue share in 2023.

Ans: North America dominated the market with a 40% revenue share in 2023.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates of Emerging Technologies

5.2 Network Infrastructure Expansion, by Region

5.3 Cybersecurity Incidents, by Region (2020-2023)

5.4 Cloud Services Usage, by Region

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Cloud Analytics Market Segmentation, By Component

7.1 Chapter Overview

7.2 Solutions

7.2.1 Solutions Market Trends Analysis (2020-2032)

7.2.2 Solutions Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Services

7.3.1 Services Market Trends Analysis (2020-2032)

7.3.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Cloud Analytics Market Segmentation, By Organization Size

8.1 Chapter Overview

8.2 Large Enterprises

8.2.1 Large Enterprises Market Trends Analysis (2020-2032)

8.2.2 Large Enterprises Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Small & Medium-Sized Enterprises

8.3.1 Small & Medium-Sized Enterprises Market Trends Analysis (2020-2032)

8.3.2 Small & Medium-Sized Enterprises Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Cloud Analytics Market Segmentation, By Deployment

9.1 Chapter Overview

9.2 Public Cloud

9.2.1 Public Cloud Market Trends Analysis (2020-2032)

9.2.2 Public Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Private Cloud

9.3.1 Private Cloud Market Trends Analysis (2020-2032)

9.3.2 Private Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Hybrid Cloud

9.4.1 Hybrid Cloud Market Trends Analysis (2020-2032)

9.4.2 Hybrid Cloud Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Cloud Analytics Market Segmentation, By Industry Vertical

10.1 Chapter Overview

10.2 Banking, Financial Services and Insurance

10.2.1 Banking, Financial Services and Insurance Market Trends Analysis (2020-2032)

10.2.2 Banking, Financial Services and Insurance Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 IT and Telecommunications

10.3.1 IT and Telecommunications Market Trends Analysis (2020-2032)

10.3.2 IT and Telecommunications Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Retail and Consumer Goods

10.4.1 Retail and Consumer Goods Market Trends Analysis (2020-2032)

10.4.2 Retail and Consumer Goods Market Size Estimates and Forecasts to 2032 (USD Billion)

10.5 Healthcare and Life Sciences

10.5.1 Healthcare and Life Sciences Market Trends Analysis (2020-2032)

10.5.2 Healthcare and Life Sciences Market Size Estimates and Forecasts to 2032 (USD Billion)

10.6 Manufacturing

10.6.1 Manufacturing Market Trends Analysis (2020-2032)

10.6.2 Manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

10.7 Research & Education

10.7.1 Research & Education Market Trends Analysis (2020-2032)

10.7.2 Research & Education Market Size Estimates and Forecasts to 2032 (USD Billion)

10.8 Others

10.8.1 Others Market Trends Analysis (2020-2032)

10.8.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Cloud Analytics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.4 North America Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.2.5 North America Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.6 North America Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.7.2 USA Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.2.7.3 USA Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.7.4 USA Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.8.2 Canada Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.2.8.3 Canada Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.8.4 Canada Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.9.2 Mexico Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.2.9.3 Mexico Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.2.9.4 Mexico Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Cloud Analytics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.7.2 Poland Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.7.3 Poland Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.7.4 Poland Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.8.2 Romania Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.8.3 Romania Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.8.4 Romania Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.10 Turkey

11.3.1.10.1 Turkey Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Cloud Analytics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.4 Western Europe Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.5 Western Europe Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.6 Western Europe Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.7.2 Germany Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.7.3 Germany Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.7.4 Germany Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.8.2 France Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.8.3 France Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.8.4 France Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.9.2 UK Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.9.3 UK Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.9.4 UK Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.10.2 Italy Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.10.3 Italy Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.10.4 Italy Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.11.2 Spain Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.11.3 Spain Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.11.4 Spain Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.14.2 Austria Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.14.3 Austria Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.14.4 Austria Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Cloud Analytics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.4 Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.5 Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.6 Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.7.2 China Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.7.3 China Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.7.4 China Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.8.2 India Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.8.3 India Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.8.4 India Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.9.2 Japan Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.9.3 Japan Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.9.4 Japan Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.10.2 South Korea Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.10.3 South Korea Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.10.4 South Korea Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.11.2 Vietnam Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.11.3 Vietnam Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.11.4 Vietnam Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.12.2 Singapore Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.12.3 Singapore Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.12.4 Singapore Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.13.2 Australia Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.13.3 Australia Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.13.4 Australia Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Cloud Analytics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.4 Middle East Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.5 Middle East Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.6 Middle East Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.7.2 UAE Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.7.3 UAE Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.7.4 UAE Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Cloud Analytics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.4 Africa Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2.5 Africa Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.6 Africa Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Cloud Analytics Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.4 Latin America Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.5 Latin America Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.6 Latin America Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.7.2 Brazil Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.7.3 Brazil Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.7.4 Brazil Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.8.2 Argentina Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.8.3 Argentina Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.8.4 Argentina Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.9.2 Colombia Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.9.3 Colombia Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.9.4 Colombia Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Cloud Analytics Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Cloud Analytics Market Estimates and Forecasts, By Organization Size (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Cloud Analytics Market Estimates and Forecasts, By Deployment (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Cloud Analytics Market Estimates and Forecasts, By Industry Vertical (2020-2032) (USD Billion)

12. Company Profiles

12.1 IBM

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 SAS Institute

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Oracle

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Google

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Microsoft

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Teradata

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Salesforce

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 AWS

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 NetApp

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Qlik

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Component

Solutions

Services

By Organization Size

Large Enterprises

Small & Medium-Sized Enterprises

By Deployment

Public Cloud

Private Cloud

Hybrid Cloud

By Industry Vertical

BFSI

IT & Telecommunication

Manufacturing

Healthcare & life sciences

Government

Energy & Utilities

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Human Resource Management Software Market Size was USD 29.77 Billion in 2023 & will reach $78.84 Bn by 2032 & grow at a CAGR of 11.43% by 2024-2032.

The Wearable AI Market was valued at USD 29.0 billion in 2023 and is expected to reach USD 276.0 billion by 2032, growing at a CAGR of 28.44% from 2024-2032.

The Streaming Analytics Market size was valued at USD 22.97 Billion in 2023 and is expected to reach USD 231.35 Billion by 2032, and grow at a CAGR of 29.26 % over the forecast period 2024-2032.

Mobile Satellite Services Market was valued at USD 5.61 billion in 2023 and is expected to reach USD 10.22 billion by 2032, growing at a CAGR of 6.92% from 2024-2032

The Digital Payment Infrastructure Market was worth USD XX billion in 2023 and is predicted to be worth USD XX billion by 2032, growing at a CAGR of XX by 2032.

The Virtual Reality in Healthcare Market Size was USD 3.20 billion in 2023 and will reach USD 46.40 Bn by 2032, growing at a CAGR of 33.30% from 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd