Get more information on Care Management Solutions Market - Request Sample Report

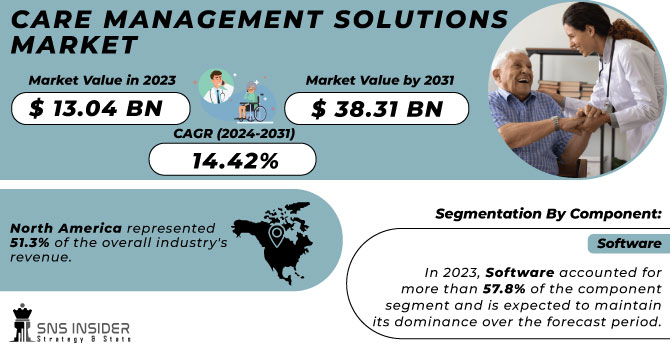

The Care Management Solutions Market Size was valued at USD 13.9 Billion in 2023 and is expected to reach USD 43.3 Billion by 2032, growing at a CAGR of 13.2% over the forecast period 2024-2032.

The care management solutions market report offers a comprehensive analysis of key statistics and emerging trends, as well as data-driven industry growth and transformation. The report notes adoption rates, stressing that care management solutions are becoming more widely used by healthcare providers, payers, and ACOs. It further delves into HIPPA and GDPR compliance as well as changing value-based care models and regulatory compliance and certifications. The report provides a global analysis of healthcare expenditure on care management solutions by healthcare government, healthcare insurers and private healthcare providers. Assessments of the potential promise of future trends such as care coordination enabled by AI and automation, the use of predictive analytics, and progress toward interoperability are summarized. Furthermore, user demographics and role-based utilization 2023 are explored, offering insights into physician, insurer, and patient engagement, aiding stakeholders in strategic planning and market positioning.

Market Dynamics

Drivers

Favorable government initiatives and regulations promoting patient-centric care are driving the growth of care management solutions among the end users.

Government initiative and regulations focusing on patient centric care is driving the adoption of a care management solution. The "Martha's Rule" implemented in the UK in 2024 allows patients and their families to insist upon an urgent review of their treatment by specialist teams. There have been 573 emergency medicine requests since it was introduced, 286 of which led to a critical care staff review and 57 of which has seen an escalation-to-care decision that could reduce mortality

Additionally, the establishment of 160 Community Diagnostic Centres (CDCs) across England has expedited access to essential tests like X-rays and scans. Around 87% of patients reported satisfaction in these centers, proving them to be effective in providing timely and patient-centered services. These initiatives are prime examples of how these government policies are making healthcare delivery more patient-centric and in turn leading to a much faster adoption of patient engagement and PT care management solutions. The philosophy behind integrated people-centered health services is to organize the health system around people rather than around diseases, an idea the World Health Organization (WHO) is advocating worldwide. This approach promotes equitable access to appropriate high-quality health services and seeks to ensure that care is coordinated across the continuum of care and that it is person-centered.

Restraint:

Interoperability issues between different healthcare systems can hinder the effectiveness of care management solutions, leading to fragmented care.

However, interoperability challenges still remain and keep hindering the overall effectiveness of care management solutions. Among U.S. hospitals in 2024, the Office of the National Coordinator for Health Information Technology (ONC) reported that only 55% were able to electronically discover, send, receive and incorporate information from other providers about a patient. This can result in missing patient records and possible medical mistakes. Moreover, the lack of standard data formats and communication protocols also compounds these problems preventing seamless data exchange between the various health IT systems. This lack of standardization hinders efficient care coordination and can result in suboptimal patient outcomes. Meeting these interoperability challenges is essential to increasing the utility of care management tools and patient care.

Opportunity:

The integration of artificial intelligence and machine learning into care management solutions presents vast opportunities for enhancing efficiency and personalization in patient care.

Integrating artificial intelligence (AI) and machine learning (ML) into care management solutions can create opportunities for better patient care with more accurate diagnoses, tailored treatment plans, and proper resource allocation. Machine learning algorithms have proven to be better than humans in interpreting the images that are used to detect certain medical conditions, including cancers and heart disease at an early stage. For example, the UK National Health Service (NHS) is about to begin the largest trial in the world of AI in breast cancer diagnosis, using around 700,000 mammograms. The goal of this trial is to evaluate how effectively AI can identify breast cancer, which may aid in speeding up diagnosis and ensure radiologists make the most of their time.

AI and ML process huge amounts of patient data to customize treatment plans in individualized care. Cera, a healthcare startup from the UK, uses AI to improve outcomes and reduce the risk of further deterioration for older people that does not require hospitalization and falls of those older people. Cera, which employs 10,000 staff to deliver 2 million appointments a month, claims to save the NHS £1 million a day by using machine learning to proactively manage patients. AI also improves patient engagement and monitoring. For instance, PainChek uses AI to analyze small alterations in facial expressions, allowing caregivers to determine the pain score for non-verbal patients, especially those with dementia. This tech will help to provide timely pain management interventions, improving the comfort and quality of provided care to the patient. This represents a significant opportunity for progressing healthcare delivery, as care management solutions incorporating AI and ML can enable patient care that is more efficient, personalized, and proactive, respectively.

Challenge:

Data security and privacy concerns are significant challenges, as care management solutions handle sensitive patient information, necessitating robust cybersecurity measures.

The rise of cyberattacks in the healthcare sector has prompted strict regulatory proposals. The U.S. Senate in 2024 proposed legislation requiring the Department of Health and Human Services to adopt new cybersecurity practices, including greater reliance on multifactor authentication and regular auditing. The decision came after large-scale attacks hit entities such as Ascension Health Alliance and Cedars-Sinai Medical Center, disrupting operations. Smaller healthcare providers, in particular, have limited resources to respond to these evolving security demands. Data transfer is hampered by fragmented healthcare systems. According to a new report from the Office of the National Coordinator for Health Information Technology, published in May 2024, only 55% of U.S. hospitals are able to electronically search, send, receive, and integrate patient information from outside providers. This fragmentation causes incomplete patient records and creates the potential for medical error. Moreover, heterogeneous data standards between different Electronic Health Record (EHR) systems make it harder to share patient-level data, and this leads to misinterpretation and latency effects in patient care. Addressing these challenges is crucial for the effective implementation of care management solutions, ensuring both the security of patient data and the seamless integration of healthcare information across platforms.

Segment analysis

By Component

In 2023, the software segment held the largest revenue share of 56% in the market. The dominance of this segment is owing to the enterprises shifting toward electronic health records (EHRs) and rising demand for an integrated healthcare IT solution. 96% of all non-federal acute care hospitals have adopted certified EHR technology in 2023, according to the Office of the National Coordinator for Health Information Technology (ONC). In addition, software segment dominance is attributed to the ease in care coordination, patient engagement, and clinical decision-making.

According to the U.S. Department of Health and Human Services, providers using comprehensive care management software experienced a 15% reduction in hospital readmissions and a 20% increase in patient satisfaction scores over 2022. Also, in 2023, National Institutes of Health (NIH) funded a few research project assignments to total funding of over USD 100 million towards developing novel care management software approaches to improve chronic disease management using technology. Such investments highlight the government's resolve towards improving the healthcare delivery mechanism using software.

By Mode of Delivery

Web-based solutions dominated the market in 2023 and accounted for the largest revenue share of 38%. That leadership position is substantially the result of web-based platforms being flexible, available, and inexpensive. A national preparedness strategy, opened 2022, stated that in 2022, health care organizations using web-based care management solutions had lower administrative costs by 25% and had 30% more efficient care coordination from the U.S. Multimedia Audio with a Background.

In 2023, the National Institute of Standards and Technology (NIST) released guidelines for secure web-based healthcare applications to further the advancement of these types of solutions throughout the healthcare enterprise. The FCC also set aside USD 250 million in 2023 for broadband expansion in rural areas to make such web-based healthcare more widely available. The low cost of deployment and reduced initial investment, along with government-backed support for technology solutions have played a major role in the stalled acceptance & growth of web-based solutions in the care management market, coupled with increasing trends of remote patient monitoring.

By Application

In 2023, the Disease Management segment accounted for significant share of revenue. The increase in the number of chronic diseases and the associated demand for effective long-term care solutions is the primary reason for this position. The U.S. Department of Health and Human Services created "Healthy People 2030" which clarifies disease management plays an intrinsic role in addressing population health. In 2023, the National Institutes of Health (NIH) budgeted USD 1.5 billion for research into new methods of managing disease, encompassing the creation of predictive analytics utilizing AI for chronic diseases. Moreover, the Agency for Healthcare Research and Quality (AHRQ) stated that the implementation of comprehensive evidence-based disease management programs by healthcare providers resulted in a 20% reduction in emergency department visits and a 15% reduction in hospitalizations among patients with chronic conditions in 2022. These statistics highlight the critical role of disease management applications in modern healthcare delivery and explain their significant market share.

By End Use

In 2023, healthcare providers have dominated the market with a 55% revenue share. The reason for this dominance is that hospitals, clinics and healthcare facilities, in general, are increasingly adopting integrated care models and moving towards value-based care. According to the Centers for Medicare & Medicaid Services (CMS), reported that 61% of healthcare providers participated in value-based care programs in 2022, compared with 54% in 2021. Thus, the increasing requirement for care management solutions by healthcare providers is stemming from this trend. According to the U.S. Department of Health and Human Services in 2023, hospitals implementing advanced Care management solutions experienced a 12% lower cost across the healthcare continuum and a 18% increase in overall patient outcomes. Furthermore, ONC announced that 89% of healthcare providers utilized care coordination and patient engagement tools in care management solutions. Such statistics highlight the need for care management solutions to improve healthcare delivery which helps to compute the larger share of the market accounted for by healthcare providers.

Need any customization research on Care Management Solutions Market - Enquire Now

Regional Analysis

In 2023, North America held a leading position in the care management solutions market with a market share of 45%. The position of leadership is due to an extensive healthcare infrastructure, high adoption of digital health technologies, and supportive government initiatives in the region. The largest market share within the region was held by the United States, due to new software development, and improved awareness about care management solutions. Accordingly, the increasing implementation of patient care solutions for cost containment and quality improvement continues to drive the market over the coming years. The underlying reasons for this growth are positive consumer attitudes towards telehealth, regulatory reforms to better reimburse these services, and the growing burden of chronic diseases. Regional key players such as Allscripts Healthcare Solutions, Inc. & Cognizant are constantly innovating and expanding their portfolios.

Asia-Pacific will register the highest CAGR over the forecast period. This growth is driven by rising health spending, rising awareness of digital health solutions, and government initiatives to enhance the accessibility of healthcare services in countries like China and India. The growth rate for healthcare spending across the Asia-Pacific region also, as projected by the World Health Organization (WHO), is much faster than that of other regions, an annual 7.5% up to the year 2025, thereby continuing to create high potential for care management solution providers.

Key Players

Key Service Providers/Manufacturers

Philips Healthcare (Philips Engage, Wellcentive)

Cerner Corporation (HealtheIntent, Population Health Management)

Allscripts Healthcare Solutions (Care Director, FollowMyHealth)

Epic Systems Corporation (Healthy Planet, MyChart Care Companion)

IBM Watson Health (Phytel Outreach, IBM Micromedex)

Salesforce Health Cloud (Health Cloud, Einstein Analytics for Healthcare)

Optum (UnitedHealth Group) (Optum Care Coordination, Optum One)

Medecision (Aerial, Risk Management)

eClinicalWorks (CCMR, Healow)

Health Catalyst (Care Management Suite, Population Health Analytics)

Key Users

UnitedHealth Group

Humana Inc.

Anthem, Inc. (Elevance Health)

Cigna Corporation

Kaiser Permanente

CVS Health (Aetna)

Mayo Clinic

Cleveland Clinic

Ascension Health

Blue Cross Blue Shield Association

Recent Developments in the Care Management Solutions Market

In Marc 2024, The U.S. Department of Health and Human Services announced a USD ss500 million initiative to expand the uptake of AI-based care management solutions at rural healthcare facilities to ensure that under-served areas get access to quality care.

In February 2024 HealthSnap, a vendor of Chronic Care Management and Remote Patient Monitoring solutions, announced USD 25 million in Series B funding, notably continuing to showcase the valuable place of investment in the sector.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 13.9 Billion |

| Market Size by 2032 | USD 43.3 Billion |

| CAGR | CAGR of 13.2% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Application (Disease Management, Case Management, Utilization Management, Others) • By Mode of Delivery (Web-based, Cloud-based, On-premise) • By End Use (Healthcare Providers, Healthcare Payers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Philips Healthcare, Cerner Corporation, Allscripts Healthcare Solutions, Epic Systems Corporation, IBM Watson Health, Salesforce Health Cloud, Optum (UnitedHealth Group), Medecision, eClinicalWorks, Health Catalyst |

Ans. The projected market size for the Care Management Solutions Market is USD 42.3 Million by 2032.

Ans: The North American region dominated the Care Management Solutions Market in 2023.

Ans. The CAGR of the Care Management Solutions Market is 13.2% During the forecast period of 2024-2032.

Ans: The major key players in the market are Philips Healthcare, Cerner Corporation, Allscripts Healthcare Solutions, Epic Systems Corporation, IBM Watson Health, Salesforce Health Cloud, Optum (UnitedHealth Group), Medecision, eClinicalWorks, Health Catalyst, and others in the final report.

Ans: The Software segment dominated the Care Management Solutions Market.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Adoption Rates (2023-2024)

5.2 Regulatory Compliance & Certifications (2023-2024)

5.3 Healthcare Spending on Care Management Solutions (2023)

5.4 AI & Automation Integration Trends (2023-2024)

5.5 User Demographics & Role-Based Utilization (2023)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Care Management Solutions Market Segmentation, By Component

7.1 Chapter Overview

7.2 Software

7.2.1 Software Market Trends Analysis (2020-2032)

7.2.2 Software Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Services

7.3.1 Services Market Trends Analysis (2020-2032)

7.3.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Care Management Solutions Market Segmentation, By Application

8.1 Chapter Overview

8.2 Disease Management

8.2.1 Disease Management Market Trends Analysis (2020-2032)

8.2.2 Disease Management Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Case Management

8.3.1 Case Management Market Trends Analysis (2020-2032)

8.3.2 Case Management Market Size Estimates and Forecasts to 2032 (USD Billion)

8.2 Utilization Management

8.2.1 Utilization Management Market Trends Analysis (2020-2032)

8.2.2 Utilization Management Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Others

8.3.1 Others Market Trends Analysis (2020-2032)

8.3.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Care Management Solutions Market Segmentation, By Mode of Delivery

9.1 Chapter Overview

9.2 Web-based

9.2.1 Web-based Market Trends Analysis (2020-2032)

9.2.2 Web-based Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 On-Premise

9.3.1 On-Premise Market Trends Analysis (2020-2032)

9.3.2 On-Premise Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Cloud Based

9.4.1 Cloud Based Market Trends Analysis (2020-2032)

9.4.2 Cloud Based Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Care Management Solutions Market Segmentation, By End Use

10.1 Chapter Overview

10.2 Healthcare Providers

10.2.1 Healthcare Providers Market Trends Analysis (2020-2032)

10.2.2 Healthcare Providers Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Healthcare Payers

10.3.1 Healthcare Payers Market Trends Analysis (2020-2032)

10.3.2 Healthcare Payers Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Others

10.4.1 Others Market Trends Analysis (2020-2032)

10.4.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Care Management Solutions Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.4 North America Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.5 North America Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.2.6 North America Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.7.2 USA Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.7.3 USA Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.2.7.4 USA Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.7 Canada

11.2.7.1 Canada Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.7.2 Canada Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.7.3 Canada Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.2.7.3 Canada Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.8 Mexico

11.2.8.1 Mexico Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.2.8.2 Mexico Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.8.3 Mexico Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.2.8.3 Mexico Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Care Management Solutions Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.6 Poland

11.3.1.6.1 Poland Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.6.2 Poland Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.6.3 Poland Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.1.6.3 Poland Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.7 Romania

11.3.1.7.1 Romania Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.7.2 Romania Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.7.3 Romania Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.1.7.3 Romania Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.8 Hungary

11.3.1.8.1 Hungary Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.8.2 Hungary Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.8.3 Hungary Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.1.8.3 Hungary Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.9 Turkey

11.3.1.9.1 Turkey Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.9.2 Turkey Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.9.3 Turkey Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.1.9.3 Turkey Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Care Management Solutions Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.4 Western Europe Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.5 Western Europe Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.5 Western Europe Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.6 Germany

11.3.2.6.1 Germany Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.6.2 Germany Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.6.3 Germany Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.6.3 Germany Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.7 France

11.3.2.7.1 France Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.7.2 France Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.7.3 France Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.7.3 France Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.8 UK

11.3.2.8.1 UK Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.8.2 UK Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.8.3 UK Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.8.3 UK Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.9 Italy

11.3.2.9.1 Italy Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.9.2 Italy Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.9.3 Italy Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.9.3 Italy Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.11.2 Spain Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.11.3 Spain Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.11.3 Spain Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.11 Netherlands

11.3.2.11.1 Netherlands Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.11.2 Netherlands Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.11.3 Netherlands Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.11.3 Netherlands Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.12 Switzerland

11.3.2.12.1 Switzerland Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.12.2 Switzerland Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.12.3 Switzerland Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.12.3 Switzerland Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.13 Austria

11.3.2.13.1 Austria Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.13.2 Austria Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.13.3 Austria Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.13.3 Austria Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.14 Rest of Western Europe

11.3.2.14.1 Rest of Western Europe Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.3.2.14.2 Rest of Western Europe Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.14.3 Rest of Western Europe Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.3.2.14.3 Rest of Western Europe Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Care Management Solutions Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.4 Asia Pacific Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.5 Asia Pacific Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.5 Asia Pacific Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.6 China

11.4.6.1 China Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.6.2 China Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.6.3 China Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.6.3 China Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.7 India

11.4.7.1 India Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.7.2 India Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.7.3 India Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.7.3 India Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.8 Japan

11.4.8.1 Japan Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.8.2 Japan Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.8.3 Japan Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.8.3 Japan Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.9 South Korea

11.4.9.1 South Korea Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.9.2 South Korea Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.9.3 South Korea Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.9.3 South Korea Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.11.2 Vietnam Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.11.3 Vietnam Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.11.3 Vietnam Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.11 Singapore

11.4.11.1 Singapore Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.11.2 Singapore Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.11.3 Singapore Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.11.3 Singapore Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.12 Australia

11.4.12.1 Australia Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.12.2 Australia Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.12.3 Australia Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.12.3 Australia Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.13 Rest of Asia Pacific

11.4.13.1 Rest of Asia Pacific Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.4.13.2 Rest of Asia Pacific Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.13.3 Rest of Asia Pacific Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.4.13.3 Rest of Asia Pacific Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Care Management Solutions Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.4 Middle East Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.5 Middle East Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.1.5 Middle East Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.6 UAE

11.5.1.6.1 UAE Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.6.2 UAE Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.6.3 UAE Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.1.6.3 UAE Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.7 Egypt

11.5.1.7.1 Egypt Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.7.2 Egypt Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.7.3 Egypt Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.1.7.3 Egypt Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.8 Saudi Arabia

11.5.1.8.1 Saudi Arabia Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.8.2 Saudi Arabia Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.8.3 Saudi Arabia Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.1.8.3 Saudi Arabia Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.9 Qatar

11.5.1.9.1 Qatar Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.9.2 Qatar Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.9.3 Qatar Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.1.9.3 Qatar Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Care Management Solutions Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.4 Africa Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.5 Africa Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.2.8.3 Africa Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.6 South Africa

11.5.2.6.1 South Africa Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.6.2 South Africa Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.6.3 South Africa Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.2.8.3 South Africa Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.7 Nigeria

11.5.2.7.1 Nigeria Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.7.2 Nigeria Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.7.3 Nigeria Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.8 Rest of Africa

11.5.2.8.1 Rest of Africa Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.5.2.8.2 Rest of Africa Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.8.3 Rest of Africa Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.5.2.8.3 Rest of Africa Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Care Management Solutions Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.4 Latin America Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.5 Latin America Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.6.5 Latin America Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.6 Brazil

11.6.6.1 Brazil Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.6.2 Brazil Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.6.3 Brazil Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.6.6.3 Brazil Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.7 Argentina

11.6.7.1 Argentina Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.7.2 Argentina Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.7.3 Argentina Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.6.7.3 Argentina Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.8 Colombia

11.6.8.1 Colombia Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.8.2 Colombia Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.8.3 Colombia Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.6.8.3 Colombia Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.9 Rest of Latin America

11.6.9.1 Rest of Latin America Care Management Solutions Market Estimates and Forecasts, By Component (2020-2032) (USD Billion)

11.6.9.2 Rest of Latin America Care Management Solutions Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.9.3 Rest of Latin America Care Management Solutions Market Estimates and Forecasts, By Mode of Delivery (2020-2032) (USD Billion)

11.6.9.3 Rest of Latin America Care Management Solutions Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

12. Company Profiles

12.1 Philips Healthcare

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Cerner Corporation

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Allscripts Healthcare Solutions

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Epic Systems Corporation

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 IBM Watson Health

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Salesforce Health Cloud

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Optum (UnitedHealth Group)

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Medecision

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 eClinicalWorks

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Health Catalyst.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Component

Software

Services

By Application

Disease Management

Case Management

Utilization Management

Others

By Mode of Delivery

Web-based

Cloud-based

On-premise

By End Use

Healthcare Providers

Healthcare Payers

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Cellular Health Screening Market, valued at USD 3.18 billion in 2023, is projected to reach USD 7.85 billion by 2032, growing at a CAGR of 10.60% by 2032

The 3D ultrasound market size was valued at USD 3.66 Billion in 2023 and is predicted to reach USD 7.79 Billion by 2032 expanding at a CAGR of 8.77% during the forecast period of 2024-2032.

The Electronic Medical Record (EMR) Systems Market size was valued at USD 29.0 billion in 2023 and is projected to reach over USD 42.6 billion by 2032, with a growing CAGR of 4.2% during the forecast period 2024-2032.

The Wearable Cardiac Devices Market size was USD 3.72 billion in 2023, projected to reach USD 25.71 billion by 2032, at a CAGR of 24.0% from 2024-2032.

Emergency Department Information System Market was valued at USD 1 billion in 2023 and is expected to reach USD 3.40 billion by 2032, at a CAGR of 14.60%.

The Infusion Pump Rental Market Size was valued at USD 379.65 Million in 2023, and is expected to reach USD 567.32 Million by 2032, and grow at a CAGR of 5.03%.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd