Get More Information on Cardiac Implant Market - Request Free Sample Report

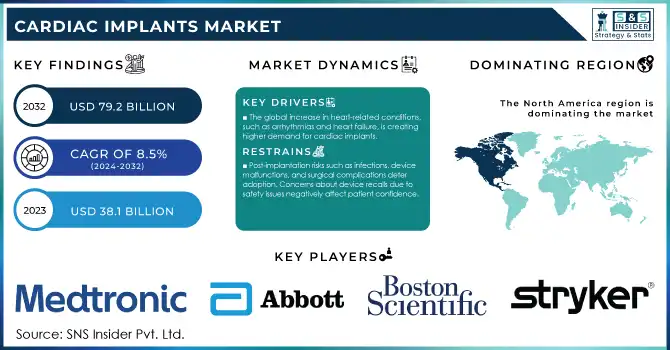

The Cardiac Implants Market Size was valued at USD 38.1 billion in 2023 and is expected to reach USD 79.2 Billion by 2032, growing at a CAGR of 8.5% over the forecast period 2024-2032.

The cardiac implants market is witnessing significant growth, largely due to the increasing prevalence of cardiovascular diseases (CVDs), the most common cause of death in the world. In 2023, cardiovascular diseases (CVDs) were responsible for 32% of all global deaths, or 17.9 million deaths according to the World Health Organization (WHO). Countries worldwide are taking countermeasures by expenditure on healthcare facilities development and planned activities to control CVDs. For instance, in 2023 the US HHS invested USD 10 billion in decreasing large population heart-related deaths via new medical technology offerings such as cardiac implants.

Parallel advancements in minimally invasive procedures and innovations in implantable devices have further enhanced patient outcomes and accessibility. For example, the development of leadless pacemakers and bioresorbable stents is reducing procedural risks and promoting widespread adoption. Public health campaigns in regions like Europe and Asia, supported by government subsidies for critical heart procedures, are also driving demand. This confluence of technological progress and policy support underscores the dynamic growth trajectory of the cardiac implants market.

Drivers

The development of innovative devices such as wireless and leadless pacemakers has improved treatment outcomes and patient convenience, driving market growth.

Increased adoption of advanced cardiac rhythm management devices is enhancing the ability to monitor and manage cardiac conditions effectively.

The global increase in heart-related conditions, such as arrhythmias and heart failure, is creating higher demand for cardiac implants.

The cardiac implant market has seen significant growth due to continuous technological innovations aimed at improving patient outcomes and device functionality. Leadless pacemakers, such as Micra TPS by Medtronic, have transformed pacing therapy by removing leads that can be of concern when it comes to infection. They are also substantially smaller up to one-tenth the size of traditional pacemakers allowing for minimally invasive and less complicated implant procedures. And just as bioabsorbable stents have changed the therapy of coronary interventions. Bioabsorbable stents, work differently from conventional stents, they tend to dissolve over time and thus help in decreasing long-term complications such as opening of artery narrowing again or restenosis. The FDA's approval of innovative devices like Boston Scientific's Synergy Bioabsorbable Polymer Drug-Eluting Stent reflects growing confidence in such technologies.

Furthermore, the usability of wearable and wireless monitoring technologies has improved post-operative care. Bluetooth-connected devices can send information to healthcare providers immediately, which makes it easier to manage chronic diseases. The study showed that detecting arrhythmias early, it proved to reduce the risk of readmission nearly by 15% from hospital to home with wireless cardiac monitoring devices. For example, a 2024 report highlighted over 300 ongoing trials globally focusing on implantable cardioverter defibrillators (ICDs) and leadless pacemakers. Collectively, these innovations are driving broader adoption and improving the quality of life for patients with cardiovascular conditions.

Restraints

The significant upfront and maintenance costs of devices like prosthetic heart valves and implantable cardioverter defibrillators limit their accessibility, especially in low and middle-income countries.

Post-implantation risks such as infections, device malfunctions, and surgical complications deter adoption. Concerns about device recalls due to safety issues negatively affect patient confidence.

The risk of complications and device malfunctions in cardiac implants is one major factor that is restricting the growth of the cardiac implants market. Complications after developing the implant (infections), blood clots, inflammation, etc. are common nuisances that end up with further medical procedures. The stakes are not only patient recovery, but they also dissuade some patients and providers from choosing to treat with implants. In addition to this, if the device malfunctions or the battery fails or the leads get dislodged, device recalls occur. These problems hinder confidence in cardiac implants and also create challenges to manufacturers to ensure the reliability of their products. These issues should be resolved with constant innovation, the most stringent manufacturing quality assurances, and improvements to the pre-and post-implantation care protocols themselves .

By application

The arrhythmias segment dominated the market in 2023 due to the increasing prevalence of conditions like atrial fibrillation. According to the Centers for Disease Control and Prevention (CDC), atrial fibrillation affects around 12.1 million Americans each year. Due to the growing prevalence of arrhythmias along with the increased utilization of pacemakers and implantable cardioverter-defibrillators (ICDs) across the globe. According to the CDC, the foremost cause of arrhythmias leads to more than 454,000 hospitalizations in the U.S. each year, which is further supported by government healthcare policies in countries such as Germany and Japan that offer large subsidies for treatments related to arrhythmias leading to significant growth of this market segment.

On the other hand, the myocardial infarction segment is expected to grow with a high CAGR owing to the higher prevalence of heart attacks along with the new development of implantable defibrillators and stent extracts which are primarily directed towards after-myocardial infarction conditions. Technological advancements including bioresorbable stents, and wearable cardiac monitors are driving the rapid CAGR of the myocardial infarction segment. As an example, the introduction of the "Healthy Heart Program" by the UK National Health Service (NHS) in February 2023 has helped create awareness and improve the uptake of preventive and corrective cardiac implants.

By end user

Hospitals accounted for the largest revenue share in 2023, at 45%. Hospitals have better infrastructure, trained professionals, and complex surgeries hence the preference. As an instance, U.S. Medicare program observed a 22% increase in reimbursement for hospital-associated cardiac implant source systems in 2023.

However cardiology centers are growing at a significant growth rate due to their cost-effectiveness and specialized services. In 2023, the European Society of Cardiology (ESC) reported that in Europe, 30% of cardiac implant procedures were performed at cardiology centers, an increase from 20% in 2020. Government initiatives like the "Cardiac Specialty Program" in India, launched in March 2023, aim to expand the network of dedicated cardiology centers to underserved regions.

By Product

The pacemakers segment dominated the cardiac implants market and held over 39.0% of revenue share in 2023. Pacemakers are in demand due to the increasing burden of bradycardia and heart block conditions. According to historical data from the National Institutes of Health (NIH), more than 1 million pacemakers will be implanted worldwide in 2022, with a projected 8% increase in 2023. Furthermore, the introduction of novel designs of pacemakers coupled with wireless monitoring has proven to improve patient outcomes and further increase the demand in the market.

Likewise, government support has been nothing short of crucial. For example, the implementation of several subsidies targeting the implantation of pacemakers in public hospitals are elements of China's "Healthy China 2030" program which has greatly lifted adoption rates across Asia-Pacific.

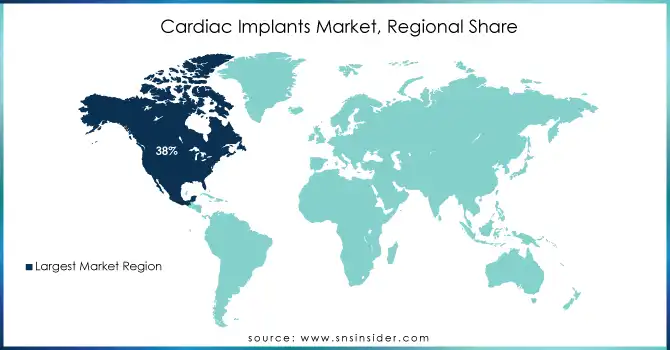

In 2023, North America the region held the largest revenue share of cardiac implants market share 38% in 2023. Factors such as the complicated healthcare system in this region, high USA healthcare expenditure, and supportive government programs such as Medicare and Medicaid are responsible for this. Through generous reimbursements, these programs have been instrumental in expanding access to cardiac implant procedures. As an example, in 2023, the U.S. government spent more than $120 billion to control cardiovascular diseases, which is part of this amount spent on innovative medical devices such as cardiac implants. There is also the continuous research and development of cardiac care expertise for both private and public markets.

Conversely, Asia-Pacific is the fastest-growing region by CAGR, which is attributed to growth in healthcare spending, growing awareness of heart health, and an increased penetration of advanced care Major economies like India and China are working on making cardiac treatments cheaper through government intervention. One good example in this regard is India, where over 50,000 cardiac procedures were performed with the help of the "Ayushman Bharat" scheme in 2023 alone; a national health policy that increased access to life-saving implants for underserved populations. Moreover, the launch of national campaigns such as "Healthy China 2030" has encouraged extensive health reforms across sectors, including government provision of subsidies and incentives to enhance prevention and treatment for the cardiac care market, which has hastened the market growth. Urbanization, a high geriatric population base, and a rise in cardiovascular diseases further boost the demand for cardiac implants in this region, thus being the most important growth driver for the market globally.

Need any customization research on Cardiac Implants Market - Enquiry Now

In January 2024, the U.S. Food and Drug Administration (FDA) approved an additional leadless pacemaker from a new line, part of a public-private collaboration to mitigate complications associated with technologies.

In January 2023, Medtronic introduced the CardioMEMS HF System, a wireless implant designed to remotely monitor heart failure patients by transmitting data directly to their physicians.

Service Providers / Manufacturers:

Medtronic plc (Micra Leadless Pacemaker, CardioMEMS HF System)

Boston Scientific Corporation (WATCHMAN Left Atrial Appendage Closure Device, EMBLEM S-ICD System)

Abbott Laboratories (CardioMEMS HF System, Xience Coronary Stent)

Biotronik SE & Co. KG (Orsiro Coronary Stent System, Rivacor CRT-D)

Stryker Corporation (Trevo ProVue Stent Retriever, Neuroform Atlas Stent System)

Zimmer Biomet Holdings, Inc. (Zimmer Universal Knee, ROSA Robotics)

LivaNova PLC (Perceval Valve, Solo Smart Valve)

Edwards Lifesciences Corporation (SAPIEN Transcatheter Heart Valve, Inspiris Resilia Valve)

Johnson & Johnson (Biosense Webster) (THERMOCOOL SmartTouch SF Catheter, CARTO 3 System)

GE Healthcare (Vivid E95 Ultrasound, CARESCAPE R860 Ventilator)

Key Users

Cleveland Clinic

Mayo Clinic

Johns Hopkins Hospital

Massachusetts General Hospital

Apollo Hospitals (India)

Fortis Healthcare (India)

Mount Sinai Hospital

Stanford Health Care

University of Texas MD Anderson Cancer Center

Karolinska University Hospital (Sweden)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 38.1 Billion |

| Market Size by 2032 | USD 79.2 Billion |

| CAGR | CAGR of 8.5% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Implantable Cardioverter-defibrillators (ICDs), Pacemakers, Coronary Stents, Implantable Heart Rhythm Monitors, Implantable Hemodynamic Monitors, Others) • By Material (Alloys, Biological, Metals, Polymers) • By Application (Arrhythmias, Acute Myocardial Infarction, Myocardial Ischemia, Others) • By End Users (Hospitals, Cardiology Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, Biotronik SE & Co. KG, Stryker Corporation, Zimmer Biomet Holdings, Inc., LivaNova PLC, Edwards Lifesciences Corporation, Johnson & Johnson (Biosense Webster), GE Healthcare. |

| Key Drivers | • The development of innovative devices such as wireless and leadless pacemakers has improved treatment outcomes and patient convenience, driving market growth. • Increased adoption of advanced cardiac rhythm management devices is enhancing the ability to monitor and manage cardiac conditions effectively. |

| Restraints | • The significant upfront and maintenance costs of devices like prosthetic heart valves and implantable cardioverter defibrillators limit their accessibility, especially in low and middle-income countries. |

Ans: The projected market size for the Cardiac Implants Market is USD 79.2 billion by 2032.

Ans: The North American region dominated the Cardiac Implants Market in 2023.

Ans: The CAGR of the Cardiac Implants Market is 8.5% During the forecast period of 2024-2032.

Ans:

The development of innovative devices such as wireless and leadless pacemakers has improved treatment outcomes and patient convenience, driving market growth.

Increased adoption of advanced cardiac rhythm management devices is enhancing the ability to monitor and manage cardiac conditions effectively.

Ans: The pacemakers segment dominated the Cardiac Implants Market in 2023.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023)

5.2 Prescription Trends, (2023), by Region

5.3 Device Volume, by Region (2020-2032)

5.4 Healthcare Spending, by Region, (Government, Commercial, Private, Out-of-Pocket), 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Cardiac Implants Market Segmentation, By Product

7.1 Chapter Overview

7.2 Implantable Cardioverter-defibrillators (ICDs)

7.2.1 Implantable Cardioverter-defibrillators (ICDs) Market Trends Analysis (2020-2032)

7.2.2 Implantable Cardioverter-defibrillators (ICDs) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Pacemakers

7.3.1 Pacemakers Market Trends Analysis (2020-2032)

7.3.2 Pacemakers Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Coronary Stents

7.4.1 Coronary Stents Market Trends Analysis (2020-2032)

7.4.2 Coronary Stents Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Implantable Heart Rhythm Monitors

7.5.1 Implantable Heart Rhythm Monitors Market Trends Analysis (2020-2032)

7.5.2 Implantable Heart Rhythm Monitors Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Implantable Hemodynamic Monitors

7.6.1 Implantable Hemodynamic Monitors Market Trends Analysis (2020-2032)

7.6.2 Implantable Hemodynamic Monitors Market Size Estimates and Forecasts to 2032 (USD Billion)

7.7 Others

7.7.1 Others Market Trends Analysis (2020-2032)

7.7.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Cardiac Implants Market Segmentation, By Material

8.1 Chapter Overview

8.2 Alloys

8.2.1 Alloys Market Trends Analysis (2020-2032)

8.2.2 Alloys Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Biological

8.3.1 Biological Market Trends Analysis (2020-2032)

8.3.2 Biological Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Metals

8.4.1 Metals Market Trends Analysis (2020-2032)

8.4.2 Metals Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Polymers

8.4.1 Polymers Market Trends Analysis (2020-2032)

8.4.2 Polymers Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Cardiac Implants Market Segmentation, By Application

9.1 Chapter Overview

9.2 Arrhythmias

9.2.1 Arrhythmias Market Trends Analysis (2020-2032)

9.2.2 Arrhythmias Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Acute Myocardial Infarction

9.3.1 Acute Myocardial Infarction Market Trends Analysis (2020-2032)

9.3.2 Acute Myocardial Infarction Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Myocardial Ischemia

9.4.1 Myocardial Ischemia Market Trends Analysis (2020-2032)

9.4.2 Myocardial Ischemia Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Others

9.5.1 Others Market Trends Analysis (2020-2032)

9.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Cardiac Implants Market Segmentation, By End Users

10.1 Chapter Overview

10.2 Hospitals

10.2.1 Hospitals Market Trends Analysis (2020-2032)

10.2.2 Hospitals Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Cardiology Centers

10.3.1 Cardiology Centers Market Trends Analysis (2020-2032)

10.3.2 Cardiology Centers Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Others

10.4.1 Others Market Trends Analysis (2020-2032)

10.4.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Cardiac Implants Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.2.4 North America Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.5 North America Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.6 North America Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.2.7.2 USA Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.7.3 USA Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.7.4 USA Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.2.7 Canada

11.2.7.1 Canada Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.2.7.2 Canada Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.7.3 Canada Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.7.3 Canada Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.2.8 Mexico

11.2.8.1 Mexico Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.2.8.2 Mexico Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.8.3 Mexico Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.2.8.3 Mexico Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Cardiac Implants Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.1.6 Poland

11.3.1.6.1 Poland Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.1.6.2 Poland Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.6.3 Poland Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.6.3 Poland Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.1.7 Romania

11.3.1.7.1 Romania Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.1.7.2 Romania Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.7.3 Romania Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.7.3 Romania Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.1.8 Hungary

11.3.1.8.1 Hungary Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.1.8.2 Hungary Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.8.3 Hungary Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.8.3 Hungary Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.1.9 Turkey

11.3.1.9.1 Turkey Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.1.9.2 Turkey Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.9.3 Turkey Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.9.3 Turkey Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Cardiac Implants Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.4 Western Europe Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.5 Western Europe Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.5 Western Europe Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.6 Germany

11.3.2.6.1 Germany Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.6.2 Germany Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.6.3 Germany Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.6.3 Germany Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.7 France

11.3.2.7.1 France Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.7.2 France Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.7.3 France Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.7.3 France Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.8 UK

11.3.2.8.1 UK Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.8.2 UK Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.8.3 UK Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.8.3 UK Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.9 Italy

11.3.2.9.1 Italy Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.9.2 Italy Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.9.3 Italy Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.9.3 Italy Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.11.2 Spain Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.11.3 Spain Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.11.3 Spain Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.11 Netherlands

11.3.2.11.1 Netherlands Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.11.2 Netherlands Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.11.3 Netherlands Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.11.3 Netherlands Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.12 Switzerland

11.3.2.12.1 Switzerland Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.12.2 Switzerland Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.12.3 Switzerland Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.12.3 Switzerland Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.13 Austria

11.3.2.13.1 Austria Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.13.2 Austria Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.13.3 Austria Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.13.3 Austria Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.3.2.14 Rest of Western Europe

11.3.2.14.1 Rest of Western Europe Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.3.2.14.2 Rest of Western Europe Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.14.3 Rest of Western Europe Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.14.3 Rest of Western Europe Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Cardiac Implants Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.4 Asia Pacific Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.5 Asia Pacific Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.5 Asia Pacific Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.6 China

11.4.6.1 China Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.6.2 China Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.6.3 China Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.6.3 China Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.7 India

11.4.7.1 India Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.7.2 India Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.7.3 India Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.7.3 India Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.8 Japan

11.4.8.1 Japan Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.8.2 Japan Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.8.3 Japan Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.8.3 Japan Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.9 South Korea

11.4.9.1 South Korea Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.9.2 South Korea Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.9.3 South Korea Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.9.3 South Korea Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.11.2 Vietnam Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.11.3 Vietnam Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.11.3 Vietnam Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.11 Singapore

11.4.11.1 Singapore Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.11.2 Singapore Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.11.3 Singapore Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.11.3 Singapore Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.12 Australia

11.4.12.1 Australia Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.12.2 Australia Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.12.3 Australia Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.12.3 Australia Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.4.13 Rest of Asia Pacific

11.4.13.1 Rest of Asia Pacific Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.4.13.2 Rest of Asia Pacific Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.13.3 Rest of Asia Pacific Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.4.13.3 Rest of Asia Pacific Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Cardiac Implants Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.1.4 Middle East Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.5 Middle East Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.5 Middle East Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.1.6 UAE

11.5.1.6.1 UAE Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.1.6.2 UAE Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.6.3 UAE Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.6.3 UAE Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.1.7 Egypt

11.5.1.7.1 Egypt Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.1.7.2 Egypt Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.7.3 Egypt Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.7.3 Egypt Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.1.8 Saudi Arabia

11.5.1.8.1 Saudi Arabia Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.1.8.2 Saudi Arabia Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.8.3 Saudi Arabia Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.8.3 Saudi Arabia Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.1.9 Qatar

11.5.1.9.1 Qatar Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.1.9.2 Qatar Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.9.3 Qatar Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.9.3 Qatar Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Cardiac Implants Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.2.4 Africa Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.5 Africa Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.8.3 Africa Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.2.6 South Africa

11.5.2.6.1 South Africa Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.2.6.2 South Africa Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.6.3 South Africa Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.8.3 South Africa Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.2.7 Nigeria

11.5.2.7.1 Nigeria Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.2.7.2 Nigeria Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.7.3 Nigeria Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.5.2.8 Rest of Africa

11.5.2.8.1 Rest of Africa Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.5.2.8.2 Rest of Africa Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.8.3 Rest of Africa Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.5.2.8.3 Rest of Africa Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Cardiac Implants Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.6.4 Latin America Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.5 Latin America Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.5 Latin America Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.6.6 Brazil

11.6.6.1 Brazil Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.6.6.2 Brazil Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.6.3 Brazil Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.6.3 Brazil Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.6.7 Argentina

11.6.7.1 Argentina Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.6.7.2 Argentina Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.7.3 Argentina Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.7.3 Argentina Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.6.8 Colombia

11.6.8.1 Colombia Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.6.8.2 Colombia Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.8.3 Colombia Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.8.3 Colombia Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

11.6.9 Rest of Latin America

11.6.9.1 Rest of Latin America Cardiac Implants Market Estimates and Forecasts, By Product (2020-2032) (USD Billion)

11.6.9.2 Rest of Latin America Cardiac Implants Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.9.3 Rest of Latin America Cardiac Implants Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.6.9.3 Rest of Latin America Cardiac Implants Market Estimates and Forecasts, By End Users (2020-2032) (USD Billion)

12. Company Profiles

12.1 Medtronic plc

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Boston Scientific Corporation

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Abbott Laboratories

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Biotronik SE & Co. KG

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 Stryker Corporation

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Zimmer Biomet Holdings, Inc.

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 LivaNova PLC

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Edwards Lifesciences Corporation

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 Johnson & Johnson (Biosense Webster)

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 GE Healthcare.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Product

Implantable Cardioverter-defibrillators (ICDs)

Pacemakers

Coronary Stents

Implantable Heart Rhythm Monitors

Implantable Hemodynamic Monitors

Others

By Material

Alloys

Biological

Metals

Polymers

By Application

Arrhythmias

Acute Myocardial Infarction

Myocardial Ischemia

Others

By End Users

Hospitals

Cardiology Centers

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Brain Computer Interface Market size was valued at USD 2.23 billion in 2023 and is expected to reach USD 8.36 billion by 2032 and grow at a CAGR of 15.81% over the forecast period of 2024-2032.

Platelet Rich Plasma Market was valued at USD 0.75 billion in 2023 & is expected to reach USD 2.62 billion by 2032, growing at a CAGR of 14.98% from 2024-2032.

The Digital Twins in Healthcare Market size was valued at USD 1.41 billion in 2023, and is expected to reach USD 28.88 billion by 2032, and grow at a CAGR of 40.01% over the forecast period 2024-2032.

The Minimal Residual Disease Testing Market was valued at USD 2.16 billion in 2023 and is expected to reach USD 5.74 billion by 2032, growing at a CAGR of 11.50% over the forecast period of 2024-2032.

The Portable Medical Devices Market Size was USD 63.56 Billion in 2023 and will reach USD 158.22 Billion by 2032 and grow at a CAGR of 10.70% by 2024-2032.

The Healthcare Market Size was valued at USD 21,222.5 Billion in 2023, and is expected to reach USD 44,760.73 Billion by 2032, and grow at a CAGR of 9.07% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd