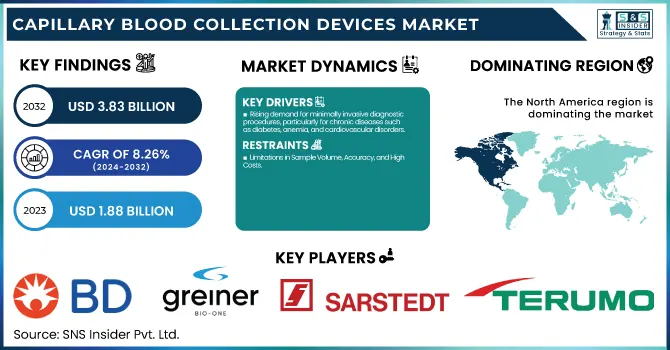

The Capillary Blood Collection Devices Market size was estimated at USD 1.88 Billion in 2023 and is projected to reach USD 3.83 Billion by 2032, growing at a CAGR of 8.26% over the forecast period 2024-2032.

To Get more information on Capillary Blood Collection Devices Market - Request Free Sample Report

This report underscores the rising incidence and prevalence of diseases necessitating capillary blood collection and changing prescription and utilization patterns across regions. The research analyzes changing regulatory and compliance models pivotal in market access and product approvals. The research also discusses technological innovation and advancements, such as automation and improved device precision, that will revolutionize blood collection practices over the next decade. The study also analyzes spending on capillary blood collection from government, commercial, private, and out-of-pocket sources of funds, varying regionally by impacting market forces and growth opportunities.

Drivers

Rising demand for minimally invasive diagnostic procedures, particularly for chronic diseases such as diabetes, anemia, and cardiovascular disorders.

The International Diabetes Federation (IDF) stated that more than 537 million adults worldwide had diabetes in 2023, making it essential to check blood glucose levels regularly. Furthermore, the increasing use of point-of-care (POC) testing and home diagnostics is driving market expansion. The increasing scope of telehealth services and self-monitoring devices, including Abbott's Freestyle Libre and Roche's Accu-Chek, have also driven demand for capillary blood collection devices. Advancements in technology, including automated and pain-free blood collection devices, are enhancing patient compliance, and improving market penetration. Additionally, the growing adoption of capillary blood collection for clinical research and personalized medicine is driving adoption. Regulatory approval for new products, including FDA-cleared Tasso+ blood collection devices, is also aiding market growth. Increasing healthcare consciousness, combined with increased investments in diagnostic technologies, is likely to support long-term growth in the industry.

Restraints

Limitations in Sample Volume, Accuracy, and High Costs

Even with robust growth, some factors hold back the capillary blood collection devices market. One of the main challenges is sample volume constraints, as capillary blood collection tends to provide smaller samples compared to venous blood, which may impact test accuracy. This constraint renders it inappropriate for some diagnostic tests that require larger sample volumes. High sample quality variability, resulting from incorrect collection methods or external contamination, can also influence test results. Most healthcare professionals continue to favor conventional venous blood collection for advanced diagnostic testing, limiting the adoption of capillary blood collection. High costs associated with high-end capillary blood collection instruments, especially automated or digital products, restrict access in resource-constrained settings. Regulatory issues present a substantial limitation since strict compliance demands for blood collection devices are slow to allow new products to come to market. Issues related to blood clotting and hemolysis in microsampling also affect the validity of test results. Additionally, healthcare professionals' ignorance and lack of training in developing markets slow down market acceptance. Overcoming these constraints with innovation, training, and enhanced technology integration is essential for greater acceptance.

Opportunities

The expansion of decentralized diagnostics, rising demand for self-monitoring health devices, and increasing investments in biomarker research present significant opportunities.

The increasing adoption of self-monitoring health devices, particularly in managing chronic conditions like diabetes and cardiovascular diseases, is creating a strong demand for reliable and user-friendly capillary blood collection methods. Additionally, the rise of personalized medicine and biomarker research is boosting the need for microsampling technologies. Companies are focusing on developing automated and pain-free blood collection devices, such as Tasso’s remote blood collection solutions, to enhance patient compliance. Another key opportunity lies in the integration of digital health technologies with capillary blood collection, enabling real-time monitoring and data sharing with healthcare providers. Growing investments in clinical trials and biobanking further drive demand for efficient blood collection methods, supporting research and innovation in diagnostic sciences. Emerging markets also present untapped potential due to improving healthcare access and rising awareness of early disease detection. Furthermore, government initiatives promoting preventive healthcare and advancements in artificial intelligence (AI)-driven diagnostics are expected to revolutionize the sector. Expanding healthcare partnerships and regulatory approvals for innovative devices will further accelerate market growth.

Challenges

Regulatory delays, slow adoption in hospitals, technological limitations in sample preservation, and concerns over data security in digital health integration also restrict market expansion.

One of the main issues is the standardization of microsampling procedures, as differences in collection processes can result in variable outcomes. Maintaining accuracy and reliability between different testing facilities is a top concern. Regulatory barriers are also an issue, as companies have to meet rigorous quality and safety requirements before products can be brought to market. Approval delays can hinder innovation and restrict market penetration. Limited adoption in conventional healthcare facilities is another significant challenge, with venous blood collection remaining the gold standard for the majority of diagnostic procedures in most traditional laboratories and hospitals. Additional evidence and validation are needed before the change to capillary blood collection practices can occur. Technological impediments in the form of enhanced blood stabilizing agents and improved sample preservation are also hindrances to wide usage. Consumer doubt about the validity of at-home testing kits also influences adoption levels. In addition, data security and compatibility issues in digital health integration are challenges that must be overcome to implement real-time diagnosis and remote patient monitoring. Overcoming these, via ongoing research, enhanced regulatory schemes, and industry alliances, will be critical for moving beyond these obstacles and fueling future market expansion.

By Product

Lancets led the capillary blood collection devices market in 2023, with a 32.1% share of the total revenue. The prevalence of lancets in glucose testing, anemia screening, and point-of-care testing helped them lead the market. Their low cost, simplicity, and common use in home care and clinical settings have cemented their position as market leaders.

Conversely, the micro-container tube segment will witness the maximum growth. It is fueled by growing demand for micro-sampling methods in clinical laboratories and hospitals, allowing for minimally invasive blood collection to conduct specialized testing. The growth of this segment is being triggered by the transformation towards sophisticated methods of collection that minimize sample volume requirements.

By Material

Plastic capillary blood collection devices dominated the market with a 41.2% share in 2023. The widespread use of plastic materials is because they are affordable, lightweight, and highly compatible with sterile healthcare conditions. Furthermore, plastic microtubes and containers offer high durability, hence, a high preference in healthcare environments.

Still, the glass segment is growing at the most rapid pace. With a higher chemical resistance and lower threat of contamination, glass micro-containers, and hematocrit tubes are being increasingly adopted. With the growing demand for high-purity blood-gathering products, glass-based products are finding increased acceptance.

By Application

Amongst applications, whole blood testing dominated the market, holding 25.4% of the overall revenue share in 2023. The popularity of this segment is backed by its widespread application in general blood diagnostics such as glucose testing, complete blood count (CBC), and infectious disease diagnosis. Whole blood collection is a core prerequisite for numerous medical and diagnostic tests, allowing it to retain its solid market position.

The plasma/serum protein tests segment will be the fastest-growing. Growth in demand for protein biomarker testing, monitoring of chronic diseases, and complex diagnostic methods is driving this segment. With the increasing traction of personalized medicine and precision diagnostics, the demand for plasma and serum-based testing is rising.

By End Use

Based on end users, clinics and hospitals stood as the prominent segment that comprised 30.3% of the market in 2023. This dominance can be due to the extensive number of diagnostic tests done within hospitals where capillary blood sampling is regularly applied for emergency diagnosis, regular check-ups, and quick patient examinations. The availability of fully-equipped medical facilities adds weight to the control of this segment.

At the same time, the home diagnosis segment is expected to expand at the highest rate. The growing uptake of home testing solutions, prompted by technological innovation in self-monitoring devices and telemedicine services, is driving demand. Growing consumer desire for convenience, along with the spread of home-based diagnostic kits for glucose, cholesterol, and other health indicators, is driving this segment's growth.

In 2023, North America led the capillary blood collection devices market with a market share of 32.2%. The leadership of the region is attributed to the high incidence of chronic conditions like diabetes, cardiovascular diseases, and infectious diseases, which demand regular blood analysis. The advanced healthcare infrastructure, robust reimbursement policies, and developed diagnostic industry further support the large-scale use of capillary blood collection devices. The increasing need for home-use and point-of-care testing, especially in the U.S. and Canada, has further fuelled market expansion.

Europe comes next, helped by rising government healthcare expenditure and an aging population that needs constant blood monitoring. The region also experiences increasing investment in minimally invasive diagnostic devices, which aids in the increase in capillary blood collection practices.

Asia-Pacific is anticipated to be the highest growing market, driven by increasing access to healthcare, growing awareness of early disease detection, and rising instances of diabetes and anemia. China, India, and Japan are experiencing a boost in the demand for capillary blood collection devices with better diagnostic facilities and the aggressive growth of homecare testing.

Get Customized Report as per Your Business Requirement - Enquiry Now

Becton, Dickinson, and Company (BD) – BD Microtainer, BD Microgard Capillary Blood Collection Tubes, BD Lancets

Greiner Bio-One International GmbH – MiniCollect Capillary Blood Collection System

SARSTEDT AG & Co. KG – Safety Lancets, Capillary Blood Collection Tubes

Terumo Medical Corp. – Capiject Safety Lancets, Microvette Capillary Blood Collection Tubes

B. Braun Melsungen AG – Sterican Lancets

Improve Medical – Capillary Blood Collection Tubes, Safety Lancets

Abbott Laboratories – Freestyle Lancets, i-STAT Capillary Blood Collection Tubes

Cardinal Health – Cardinal Health Safety Lancets

Retractable Technologies Inc. – EasyPoint Blood Collection Lancets

Haemonetics Corporation – Safe-T-Vue Capillary Blood Collection Solutions

Medtronic plc – MiniMed Lancets

Radiometer Medical ApS – SafeCrit Capillary Blood Sampling Tubes

Roche Diagnostics – Accu-Chek Softclix Lancets

Siemens Healthineers – Microvette Capillary Blood Collection System

In Feb 2025, Tasso and Arup partnered to enhance blood testing services for clinical research. As part of the collaboration, Arup conducted validation of multiple assays using capillary blood micro samples, supporting the expansion of minimally invasive diagnostics.

In Dec 2024, BD (Becton, Dickinson, and Company) and Babson Diagnostics expanded fingertip blood collection and testing technologies for U.S. healthcare systems, enabling use in urgent care centers, physician offices, and ambulatory care settings to enhance diagnostic accessibility.

In Aug 2024, Vitestro Holding BV received a CE marking for its AI-powered automated blood drawing device, which integrates ultrasound-guided imaging and robotics for precise and secure blood collection. As the first device of its kind to achieve CE certification, it is expected to revolutionize healthcare diagnostics.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.88 billion |

| Market Size by 2032 | USD 3.83 billion |

| CAGR | CAGR of 8.26% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product [Lancets, Micro-container tubes, Micro-hematocrit tubes, Warming devices, Others] • By Material [Plastic, Glass, Stainless steel, Ceramic, Others] • By Application [Whole Blood, Plasma/ serum protein Tests, Comprehensive metabolic panel tests, Liver panel/ liver profile/ liver function tests, Dried blood spot tests] • By End Use [Hospitals and Clinics, Blood Donation Centers, Diagnostic Centers, Home Diagnosis, Pathology Laboratories] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Becton, Dickinson, and Company (BD), Greiner Bio-One International GmbH, SARSTEDT AG & Co. KG, Terumo Medical Corp., B. Braun Melsungen AG, Improve Medical, Abbott Laboratories, Cardinal Health, Retractable Technologies Inc., Haemonetics Corporation, Medtronic plc, Radiometer Medical ApS, Roche Diagnostics, Siemens Healthineers. |

Ans: The Capillary Blood Collection Devices market is anticipated to grow at a CAGR of 8.26% from 2024 to 2032.

Ans: The market is expected to reach USD 3.83 billion by 2032, increasing from USD 1.88 billion in 2023.

Ans: Rising demand for minimally invasive diagnostic procedures, particularly for chronic diseases such as diabetes, anemia, and cardiovascular disorders.

Ans: One of the main challenges is sample volume constraints, as capillary blood collection tends to provide smaller samples compared to venous blood, which may impact test accuracy.

Ans: North America dominated the Capillary Blood Collection Devices market.

Table Of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence of Diseases Requiring Capillary Blood Collection (2023)

5.2 Prescription and Utilization Trends (2023), by Region

5.3 Regulatory and Compliance Trends

5.4 Technological Advancements and Innovations (2023-2032)

5.5 Healthcare Spending on Capillary Blood Collection, by Region (Government, Commercial, Private, Out-of-Pocket), 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and Promotional Activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Capillary Blood Collection Devices Market Segmentation, by Product

7.1 Chapter Overview

7.2 Lancets

7.2.1 Lancets Market Trends Analysis (2020-2032)

7.2.2 Lancets Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Micro-container tubes

7.3.1 Micro-container Tubes Market Trends Analysis (2020-2032)

7.3.2 Micro-container Tubes Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Micro-hematocrit tubes

7.4.1 Micro-hematocrit Tubes Market Trends Analysis (2020-2032)

7.4.2 Micro-hematocrit Tubes Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Warming devices

7.5.1 Warming Devices Market Trends Analysis (2020-2032)

7.5.2 Warming Devices Market Size Estimates and Forecasts to 2032 (USD Billion)

7.6 Others

7.6.1 Others Market Trends Analysis (2020-2032)

7.6.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Capillary Blood Collection Devices Market Segmentation, By Material

8.1 Chapter Overview

8.2 Plastic

8.2.1 Plastic Market Trends Analysis (2020-2032)

8.2.2 Plastic Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Glass

8.3.1 Glass Market Trends Analysis (2020-2032)

8.3.2 Glass Market Size Estimates And Forecasts To 2032 (USD Billion)

8.4 Stainless steel

8.4.1 Stainless Steel Market Trends Analysis (2020-2032)

8.4.2 Stainless Steel Market Size Estimates And Forecasts To 2032 (USD Billion)

8.5 Ceramic

8.5.1 Ceramic Market Trends Analysis (2020-2032)

8.5.2 Ceramic Market Size Estimates And Forecasts To 2032 (USD Billion)

8.6 Others

8.6.1 Others Market Trends Analysis (2020-2032)

8.6.2 Others Market Size Estimates And Forecasts To 2032 (USD Billion)

9. Capillary Blood Collection Devices Market Segmentation, by Application

9.1 Chapter Overview

9.2 Whole Blood

9.2.1 Whole Blood Market Trends Analysis (2020-2032)

9.2.2 Whole Blood Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Plasma/Serum Protein Tests

9.3.1 Plasma/Serum Protein Tests Market Trends Analysis (2020-2032)

9.3.2 Plasma/Serum Protein Tests Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Comprehensive Metabolic Panel Tests

9.4.1 Comprehensive Metabolic Panel Tests Market Trends Analysis (2020-2032)

9.4.2 Comprehensive Metabolic Panel Tests Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Liver Panel/ Liver Profile/ Liver Function Tests

9.5.1 Liver Panel/ Liver Profile/ Liver Function Tests Market Trends Analysis (2020-2032)

9.5.2 Liver Panel/ Liver Profile/ Liver Function Tests Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Dried Blood Spot Tests

9.6.1 Dried Blood Spot Tests Market Trends Analysis (2020-2032)

9.6.2 Dried Blood Spot Tests Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Capillary Blood Collection Devices Market Segmentation, By End Use

10.1 Chapter Overview

10.2 Hospitals and Clinics

10.2.1 Hospitals and Clinics Market Trends Analysis (2020-2032)

10.2.2 Hospitals and Clinics Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Blood Donation Centers

10.3.1 Blood Donation Centers Market Trends Analysis (2020-2032)

10.3.2 Blood Donation Centers Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Diagnostic Centers

10.4.1 Diagnostic Centers Market Trends Analysis (2020-2032)

10.4.2 Diagnostic Centers Market Size Estimates and Forecasts to 2032 (USD Billion)

10.5 Home Diagnosis

10.5.1 Home Diagnosis Market Trends Analysis (2020-2032)

10.5.2 Home Diagnosis Market Size Estimates and Forecasts to 2032 (USD Billion)

10.6 Pathology Laboratories

10.6.1 Pathology Laboratories Market Trends Analysis (2020-2032)

10.6.2 Pathology Laboratories Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America Capillary Blood Collection Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.2.4 North America Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.5 North America Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.6 North America Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.2.7.2 USA Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.7.3 USA Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.7.4 USA Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.2.8.2 Canada Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.8.3 Canada Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.8.4 Canada Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.2.9.2 Mexico Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.2.9.3 Mexico Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.2.9.4 Mexico Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.1.7.2 Poland Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.7.3 Poland Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.7.4 Poland Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.1.8.2 Romania Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.8.3 Romania Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.8.4 Romania Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.1.9.2 Hungary Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.9.3 Hungary Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.9.4 Hungary Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.10 turkey

11.3.1.10.1 Turkey Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.1.10.2 Turkey Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.10.3 Turkey Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.10.4 Turkey Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.4 Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

11.3.2.5 Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Delivery Technology (2020-2032) (USD Billion)

11.3.2.6 Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.7.2 Germany Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.7.3 Germany Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.7.4 Germany Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.8.2 France Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.8.3 France Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.8.4 France Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.9.2 UK Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.9.3 UK Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.9.4 UK Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.10.2 Italy Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.10.3 Italy Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.10.4 Italy Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.11.2 Spain Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.11.3 Spain Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.11.4 Spain Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.14.2 Austria Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.14.3 Austria Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.14.4 Austria Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.4 Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.5 Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.6 Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.7.2 China Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.7.3 China Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.7.4 China Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.8.2 India Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.8.3 India Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.8.4 India Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.9.2 Japan Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.9.3 Japan Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.9.4 Japan Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.10.2 South Korea Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.10.3 South Korea Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.10.4 South Korea Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.11.2 Vietnam Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.11.3 Vietnam Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.11.4 Vietnam Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.12.2 Singapore Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.12.3 Singapore Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.12.4 Singapore Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.13.2 Australia Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.13.3 Australia Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.13.4 Australia Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.1.4 Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.5 Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.6 Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.1.7.2 UAE Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.7.3 UAE Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.7.4 UAE Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.1.8.2 Egypt Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.8.3 Egypt Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.8.4 Egypt Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.1.10.2 Qatar Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.10.3 Qatar Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.10.4 Qatar Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa Capillary Blood Collection Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.2.4 Africa Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.5 Africa Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.6 Africa Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.2.7.2 South Africa Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.7.3 South Africa Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.7.4 South Africa Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.6.4 Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.5 Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.6 Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.6.7.2 Brazil Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.7.3 Brazil Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.7.4 Brazil Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.6.8.2 Argentina Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.8.3 Argentina Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.8.4 Argentina Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.6.9.2 Colombia Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.9.3 Colombia Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.9.4 Colombia Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America Capillary Blood Collection Devices Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

12. Company Profiles

12.1 Becton, Dickinson and Company (BD)

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Product / Services Offered

12.1.4 SWOT Analysis

12.2 Greiner Bio-One International GmbH

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Product / Services Offered

12.2.4 SWOT Analysis

12.3 SARSTEDT AG & Co. KG

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Product / Services Offered

12.3.4 SWOT Analysis

12.4 Terumo Medical Corp.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Product / Services Offered

12.4.4 SWOT Analysis

12.5 B. Braun Melsungen AG

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Product / Services Offered

12.5.4 SWOT Analysis

12.6 Improve Medical

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Product / Services Offered

12.6.4 SWOT Analysis

12.7 Abbott Laboratories

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Product / Services Offered

12.7.4 SWOT Analysis

12.8 Cardinal Health

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Product / Services Offered

12.8.4 SWOT Analysis

12.9 Retractable Technologies Inc.

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Product / Services Offered

12.9.4 SWOT Analysis

12.10 Haemonetics Corporation

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Product / Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Product

Lancets

Micro-container tubes

Micro-hematocrit tubes

Warming devices

Others

By Material

Plastic

Glass

Stainless steel

Ceramic

Others

By Application

Whole Blood

Plasma/ Serum Protein Tests

Comprehensive Metabolic Panel Tests

Liver Panel/ Liver Profile/ Liver Function Tests

Dried Blood Spot Tests

By End Use

Hospitals and Clinics

Blood Donation Centers

Diagnostic Centers

Home Diagnosis

Pathology Laboratories

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Veterinary Vaccine Adjuvants Market size was valued at USD 9.18 billion in 2023 and is estimated to reach USD 15.24 billion by 2032 with a growing CAGR of 5.8% from 2024 to 2032.

The Albumin Market Size was valued at USD 6.15 billion in 2023, and is expected to reach USD 10.5 billion by 2032, and grow at a CAGR of 6.1% over the forecast period 2024-2032.

The Sexual Health Products Market Size was valued at USD 118.83 Billion in 2023, and is expected to reach USD 243.83 Billion by 2032, and grow at a CAGR of 8.71% over the forecast period 2024-2032.

The Bleeding Disorders Treatment Market Size was USD 16.35 Bn in 2023 and is projected to reach USD 35.17 Bn by 2032, growing at 8.91% CAGR.

Transport Chairs Market was valued at USD 1.2 billion in 2023 and is expected to reach USD 2.26 billion by 2032, growing at a CAGR of 7.28% over the forecast period of 2024-2032.

The Personalized Medicine Biomarkers Market to grow from USD 17.26 billion in 2023 to USD 58.39 billion by 2032, at a 14.54% CAGR.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd