Breast Adenocarcinoma Treatment Market Report Scope & Overview:

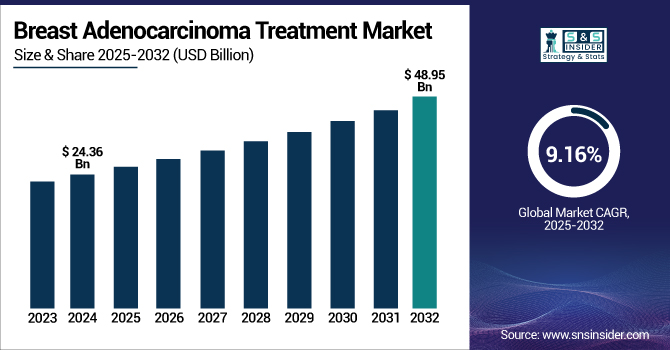

The Breast Adenocarcinoma Treatment Market size was valued at USD 24.36 billion in 2024 and is expected to reach USD 48.95 billion by 2032, growing at a CAGR of 9.16% over the forecast period of 2025-2032.

To Get more information on Breast Adenocarcinoma Treatment Market - Request Free Sample Report

The breast adenocarcinoma treatment market is expanding owing to growing breast cancer prevalence, rising awareness, technological progress in targeted therapies, and increasing access to healthcare. Improved diagnostic equipment and continuous R&D in oncology fuel innovation. Government campaigns and favorable reimbursement policies also promote treatment uptake. The aging population and lifestyle changes also push the demand for effective treatments forward, fueling market growth globally.

For instance, according to the National Cancer Institute, Breast cancer is the leading non-skin cancer in women in the U.S. In 2025, an estimated 59,080 cases of ductal carcinoma in situ (DCIS) and 316,950 cases of invasive breast cancer will occur in women. Of those diagnosed, about 42,170 women, less than one in eight, are expected to die of the disease. For comparison, lung cancer itself is estimated to kill approximately 60,540 American women in the same year. Men account for approximately 1% of both breast cancer diagnoses and deaths from the disease.

The U.S. breast adenocarcinoma treatment market size was valued at USD 8.68 billion in 2024 and is expected to reach USD 16.88 billion by 2032, growing at a CAGR of 8.70% from 2025-2032. The U.S. dominates North America's breast adenocarcinoma treatment market owing to its developed healthcare infrastructure, high rates of incidence, and large number of major pharma players present in the region. Continuing clinical trials and high rates of uptake of emerging therapies also help maintain its leadership position in the market.

Market Dynamics:

Drivers:

-

Advancements in Medical Technology are Driving Market Growth

Technological innovations in the medical field are prominently fueling the breast adenocarcinoma treatment market growth. Advanced diagnostic instruments, such as 3D mammography and genetic testing allow early, accurate diagnosis and individualized treatment planning. Targeted agents and immunotherapy provide better effectiveness with fewer toxicities than traditional chemotherapy. Minimal invasive surgical methods and precision-driven radiation therapies also help in improving patient outcomes and recovery rates. Together, these innovations raise the rates of treatment success and increase access to sophisticated care, increasing the overall market growth and demand globally.

-

Scientists at the National Cancer Institute (NCI) are studying the application of cellular therapies, including CAR T-cell therapy and T-cell transfer therapy, for the treatment of solid tumors, such as breast cancer. One clinical trial is currently evaluating the application of tumor-infiltrating lymphocytes (TILs) in shrinking tumors in women with metastatic breast cancer. In another research, researchers are genetically engineering a patient's T cells in the laboratory to target cancer cells specifically before reinfusing them. This study now enrolls people with solid tumors, such as breast cancer.

-

Targeted Therapy for Breast Cancer is Propelling the Market Expansion

Targeted therapy is fueling breast cancer market expansion through more accurate treatment options that target specific molecules implicated in cancer cell proliferation. Unlike conventional chemotherapy, targeted therapies, such as HER2 inhibitors or PI3K blockers, target the molecular mechanisms that drive cancer development, enhancing treatment effectiveness and minimizing side effects. As additional targeted therapies are brought to the market and approved, their use to treat more subtypes of breast cancer is increasing, driving market demand.

-

According NIC, Trastuzumab deruxtecan (Enhertu), an antibody-drug conjugate, was initially approved to treat HER2-positive breast cancer. The monoclonal antibody trastuzumab (Herceptin) binds to tumor cells that have HER2 on their surface and delivers the chemotherapy drug deruxtecan to these cells.

Restraints:

-

Limited Access in Low-Income Regions for Breast Cancer Adenocarcinoma Therapy Hinders Market Expansion

Breast cancer continues to be one of the principal health challenges globally, as the most common malignancy in females. It affects an estimated 2.1 million new women each year and represents 24.2% of all new female cancer cases. It is responsible for 15% of cancer deaths in women and occurs for one of every four malignancies in females. Early-onset breast cancer, diagnosed in women under the age of 50, is usually more aggressive and with a worse prognosis. Late-onset breast cancer, diagnosed in women over 70 years old, is less aggressive. The lifetime risk of developing breast cancer depends on country and ethnicity due to varying exposure to risk factors.

Segmentation Analysis:

By Treatment Product

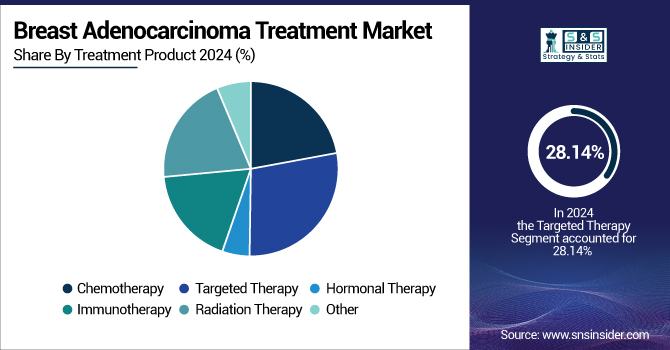

In 2024, the targeted therapy segment dominated the breast adenocarcinoma treatment market share with 28.14%, as it is precision-driven and increasingly used in clinical practice. In contrast to conventional chemotherapy, targeted therapies target specific molecular pathways that drive cancer growth, for instance, HER2 or PI3K mutations. Widely embraced therapies, such as trastuzumab, pertuzumab, and CDK4/6 inhibitors (palbociclib), have had successful development in improving progression-free survival and overall survival rates, particularly in hormone receptor-positive and HER2-positive subsets. Increasing adoption of companion diagnostics and genomic profiling further facilitated the dominance of this segment by allowing more patients to receive individualized and effective therapies.

The immunotherapy segment is expected to grow at the fastest over the forecast period, with 10.13% CAGR through the potential for transformation of treatment scenarios for highly aggressive and therapy-refractory breast adenocarcinomas, including TNBC. Contrary to traditional therapies, the immunotherapies turn the patient's immune system itself to identify and destroy cancerous cells, resulting in long-lasting outcomes. The approval and ongoing studies of immune checkpoint inhibitors and cell-based treatments (CAR T-cell and TIL therapies) have created considerable optimism. With ongoing research and approval of new indications, the immunotherapy segment should see accelerated adoption, most notably for patients with few therapeutic choices.

By End-Use

In 2024, the hospitals segment dominated with a 64.21% breast adenocarcinoma treatment market share in terms of end-use, due to the thorough infrastructure of hospitals for cancer diagnosis, treatment, and post-treatment. Hospitals have sophisticated imaging systems, pathology laboratories, operating theaters, and multidisciplinary teams that facilitate proper management of complex cases of breast cancer. They are also the principal locations for chemotherapy, radiation, and surgical intervention provision. Besides, hospitals tend to be the first source of treatment upon diagnosis and also commonly provide patient care throughout the treatment, especially in cases that include hospital stay or intensive care.

The specialty clinics segment will be showing the fastest growth throughout the forecast period. This expansion is driven by the increased trend toward treatment outside of an inpatient setting, technological advancements in minimally invasive treatments, and the increased demand for individualized, convenient, and low-cost cancer treatment. Specialty clinics focus exclusively on oncology or breast health so that a more individualized and patient-centric experience can be achieved. Specialty clinics are increasingly charged with the administration of targeted therapies and follow-up care. With improved access, decreasing waiting times, and growing association with diagnostic labs and pharmaceutical companies, specialty clinics are emerging as a feasible substitute for hospital-based care, particularly for early-stage or non-malignant patients.

Regional Analysis:

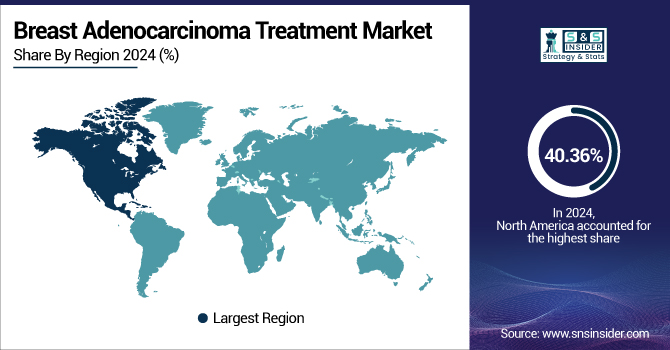

North America dominated the breast adenocarcinoma treatment market with a 40.36% market share in 2024, driven by its sophisticated healthcare infrastructure, strong awareness levels, and heavy investments in cancer treatment and research. The region has the privileges of early screening campaigns, extensive use of target therapies and immunotherapies, and the dominance of major pharmaceutical companies. According to the NCBI, in the U.S., breast cancer is the second leading cause of death in women. The U.S., particularly, possesses strong regulatory systems, positive reimbursement policies, and exposure to novel clinical trials, which all induce early diagnosis and timely treatment.

The Asia Pacific region is anticipated to register the fastest growth over the forecast period with 9.83% CAGR due to the increasing healthcare spending, rising incidence of breast cancer, and increased access to sophisticated treatment centers. Growing awareness campaigns and government-funded screening programs are helping in the detection of the disease at an early stage. Moreover, the area is witnessing rapid economic growth, which is fueling expanded healthcare infrastructure and rising adoption of advanced therapies, particularly in economies such as China, India, and Japan. The growing focus of multinationals from the pharmaceutical sector on emerging markets, coupled with the availability of affordable treatment options, also serves to enhance the rapid market expansion in the Asia Pacific.

The U.K. leads the European breast adenocarcinoma treatment market because of its strong healthcare infrastructure, high R&D spending, and fast take-up of innovative therapies. Academic institutions and major pharma drive innovation, and the NHS facilitates widespread availability of advanced treatments. With increasing emphasis on personalized medicine and biologics, the U.K. continues to raise standards in breast cancer treatment, and hence it is a leader in Breast cancer adenocarcinoma therapy.

The Middle East & Africa are witnessing enormous growth in the breast adenocarcinoma treatment market, attributed to increasing cases of cancer, enhanced healthcare facilities, and enhanced uptake of the latest therapies. Enhancing public awareness, government funding, and increasing incorporation of major drug companies are impelling early diagnostics and access to novel treatments, positioning the region as a most prominent emerging contender in cancer therapy.

The breast adenocarcinoma treatment market in Latin America is expanding with increased breast cancer incidence, better healthcare facilities, and greater use of newer therapies such as targeted therapies and immunotherapies. Government efforts and increased awareness are driving earlier detection and access to care, and thereby fuelling growth in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Market Players:

The leading players in the market include F. Hoffmann-La Roche Ltd., Novartis AG, Pfizer Inc., AstraZeneca PLC, Eli Lilly and Company, Merck & Co., Inc., Bristol-Myers Squibb Company, Sanofi S.A., AbbVie Inc., Johnson & Johnson, Kyowa Kirin, and other players.

Recent Developments:

-

January 2025 – The U.S. Food and Drug Administration (FDA) approved Datroway (datopotamab deruxtecan or Dato-DXd) for the treatment of unresectable or metastatic hormone receptor (HR)-positive, HER2-negative breast cancer in adult patients who have received prior endocrine-based therapy and chemotherapy. The approval followed encouraging results from the TROPION-Breast01 Phase III trial.

-

October 2024 – Roche was granted FDA approval for Itovebi (inavolisib) in combination with palbociclib (Ibrance) and fulvestrant to treat adults with endocrine-resistant, PIK3CA-mutated, HR-positive, HER2-negative locally advanced or metastatic breast cancer. The PIK3CA mutation, found in approximately 40% of HR-positive metastatic breast cancers, was detected by an FDA-approved test.

-

September 2024 – Novartis announced FDA approval of Kisqali (ribociclib) with an aromatase inhibitor (AI) for adjuvant treatment of patients with HR+/HER2- stage II and III early breast cancer (EBC) at high risk of recurrence, including node-negative.

-

February 2024 – Arvinas, Inc. and Pfizer Inc. announced that their investigational treatment vepdegestrant (ARV-471) was granted FDA Fast Track designation. Vepdegestrant is an oral first-in-class PROteolysis Targeting Chimera (PROTAC) ER degrader for the treatment of adults with ER+/HER2- locally advanced or metastatic breast cancer who have previously received endocrine-based therapy.

-

November 2024 – Eli Lilly and Company made announcements of new Phase 3 EMBER-3 trial data of imlunestrant, a once-daily oral selective estrogen receptor degrader (SERD). The trial assesses imunestrant alone as well as when used with Verzenio (abemaciclib) as a treatment option in patients with ER+/HER2- previously been treated with endocrine therapy breast cancer.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 24.36 Billion |

| Market Size by 2032 | USD 48.95 Billion |

| CAGR | CAGR of 9.16% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Treatment Product (Chemotherapy, Targeted Therapy, Hormonal Therapy, Immunotherapy, Radiation Therapy, Other) • By End Use (Hospitals, Specialty Clinics, Other) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | F. Hoffmann-La Roche Ltd., Novartis AG, Pfizer Inc., AstraZeneca PLC, Eli Lilly and Company, Merck & Co., Inc., Bristol-Myers Squibb Company, Sanofi S.A., AbbVie Inc., Johnson & Johnson, and other players. |