To Get More Information on Brain Tumor Drugs Market - Request Sample Report

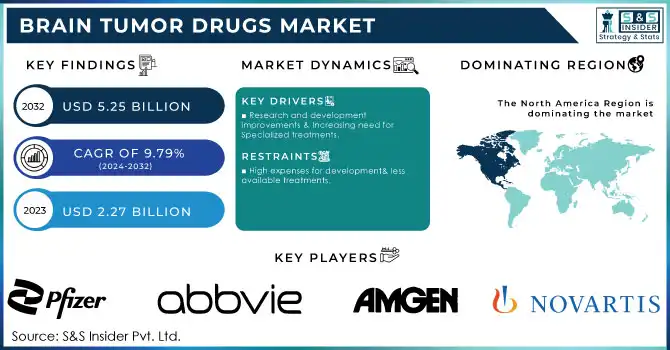

The Brain Tumor Drugs Market size was estimated at USD 2.27 billion in 2023 and is expected to reach USD 5.25 billion by 2032 at a CAGR of 9.79% during the forecast period of 2024-2032. This report provides a review of trends in brain tumor incidence and mortality rates, and how these contribute to an increasing demand for effective treatment options. The report has also discussed drug approval trends and pipeline development, which points out promising new therapies that shape the future of brain tumor treatment. It also looks into the expenditure on brain tumor treatment by different sources, such as healthcare institutions, government funding, and private insurance. The study also explores how changing consumer preferences for targeted therapies and emerging treatment solutions affect market dynamics.

Drivers

Technological advancements in diagnostics, drug delivery, and research investments are driving growth in the brain tumor drug market.

Advances in imaging diagnostics, including MRI and CT scans, have also meant earlier diagnosis and accuracy in the diagnosis of brain tumors, which further leads to a better treatment outcome using targeted therapy. Developments in drug delivery systems, for example, nanoparticles and other advanced techniques to deliver drugs to the tumor site, ensure that drugs are metabolized at sites appropriately. Another major impetus is the rising global incidence of brain tumors, particularly with aging populations. Governments and private organizations are spending heavily on research, which accelerates the discovery of new therapies. All these factors, combined with an increased focus on personalized medicine, are driving the growth of the market.

Restraints

Factors such as the blood-brain barrier, tumor heterogeneity, drug resistance, and high treatment costs hinder the market growth

A significant challenge is the blood-brain barrier, which does not allow many drugs to penetrate tumor sites. In addition, the heterogeneity of brain tumors, with each tumor acting differently, poses a problem for universal treatment approaches. Another issue is drug resistance, where the tumor evolves and becomes less responsive to therapy. Further, the high cost of developing, manufacturing, and administering brain tumor drugs limits accessibility, especially in regions with fewer healthcare resources, making it difficult for many patients to access potentially life-saving treatments.

Opportunities

Advancements in Precision Medicine, Targeted Therapies, and Immunotherapy are the major opportunities in the brain tumor drugs market

The brain tumor drug market is full of potential innovation and expansion. Precision medicine offers a promising treatment for each individual with his unique genetic makeup that promises more effectiveness. Targeted therapies hold great promise in various kinds of brain tumors with very minimal side effects compared to more common side effects of general chemotherapy and radiation. Immunotherapy, including the use of immune checkpoint inhibitors and CAR-T cell therapy, is becoming an exciting option for patients with advanced or aggressive brain tumors. The collaboration between biotech companies, pharmaceutical firms, and academic institutions provides the foundation for breakthrough research, driving the development of new treatment options. Another way is increasing healthcare access in emerging markets and also expanding the access of these new innovative treatments to a larger number of patients in such markets.

Challenges

The brain tumor drug market faces challenges including the high cost of treatment, tumor complexity, and insufficient research funding.

The lengthy approval process for newly discovered brain tumor drugs creates major delays in treatment for patients in the hope of a life-saving medicine. Besides this, inherent characteristics of the tumors pose multiple problems, among them the tumor's resistance to specific therapies, as well as their inaccessibility due to the location inside the brain. These problems are compounded by the limited funding of research, particularly for rare brain tumor types. This makes the development of novel and more effective treatments difficult to achieve. Further, the absence of universally accepted treatment protocols means that physicians must often rely on trial-and-error methods, with suboptimal outcomes for the patient. Such factors together contribute to major impediments in developing better options for the treatment of brain tumors and improving patient care.

By Therapy

Chemotherapy dominated the market share in the brain tumor drugs with a 36.4 % share of market in 2023 and is considered effective in various types of brain tumors. Chemotherapy targets fast-dividing cells, which characterize cancerous growth, and it has been at the core of cancer treatment for decades. Its wide availability, established protocols, and high clinical experience make its treatment of brain tumors the most dominant treatment. Chemotherapy is most effective for sensitive tumor types that respond well to systemic treatment. It poses side effects, and its efficacy is limited in some tumor types.

The immunotherapy segment is likely to gain momentum during the forecast period. This shift is mainly prompted by advances in the knowledge of the immune system and how to harness it against brain tumors. The increasing appreciation for immunotherapies such as immune checkpoint inhibitors, CAR-T cell therapies, and monoclonal antibodies can specifically target brain tumors, causing less harm than chemotherapy, the most commonly used traditional therapy. Another aspect driving the need for immunotherapy is the increase in precision medicine that tailors treatment to a particular patient according to their genetic makeup.

By Indication

The glioma segment accounted for the highest share of 38.9% in the brain tumor drug market in 2023, as it is more common and hard to treat. Gliomas are one of the most aggressive and common forms of brain tumors, and their complex biology is a significant challenge in treating them. This high demand for efficient therapies has spurred extensive research in targeted therapies, immunotherapy, and chemotherapy. Glioma encompasses the following tumor types, including glioblastomas, which are known to be particularly challenging and with a very poor prognosis, even with aggressive treatment. As such, more emphasis has been placed on novel therapies that improve patient outcomes. The large patient population suffering from gliomas remains a significant market driver.

The meningioma segment is expected to have a substantial compound annual growth rate (CAGR) over the forecast period. Meningiomas are generally benign, slowly growing tumors originating from the meninges, which cover the brain and spinal cord. Because of their benign nature, meningiomas are often more treatable than gliomas, creating a larger patient pool for therapeutic intervention. These tumors are more frequently diagnosed due to advancements in imaging techniques, leading to increased treatment demand. The growth in this segment is because of the increasing knowledge of the treatment options for meningiomas, such as surgical resection, radiation therapy, and targeted drug therapies.

By Distribution Channel

In 2023, hospital pharmacy segment was capturing a 63.2% share of brain tumor drugs market. Hospital pharmacies have the right kind of infrastructure and expertise to administer the complex treatment process, often consisting of chemotherapy and immunotherapy or other advanced drugs. Hospitals also offer integrated care such as surgery and radiation therapy that are an integral part of holistic brain tumor treatment plans.

Retail and online pharmacies are expected to grow significantly over the forecast period. The growing demand for home care by patients and the telemedicine phenomenon also increase growth as it helps patients receive prescriptions through these methods. Patients have a higher chance of visiting retail or online pharmacies since these entities provide easier access to drugs for them, besides giving them an affordable option. With this shift in preference toward more accessible and affordable options, especially for maintenance therapies that are more routine or for less aggressive tumor types, this segment will expand.

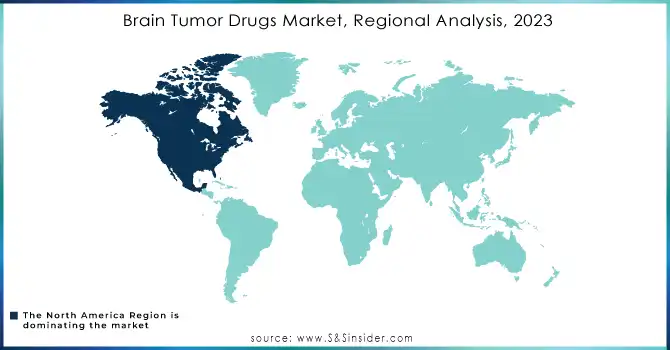

North America dominated the brain tumor drug market with a 44.1% share in 2023 due to robust healthcare infrastructure, high research and development investment, and a high rate of brain tumor diagnosis. In particular, the U.S. is leading the pack in the availability of advanced treatment options such as targeted therapies, chemotherapy, and immunotherapy. This region is further supported by high government funding for cancer research and the presence of key pharmaceutical players, thus increasing the availability and development of innovative therapies. Patients in North America also have more access to clinical trials, further driving market growth.

On the other hand, the Asia Pacific region is likely to see the fastest growth in the forecast period. The reasons for this include increased accessibility to healthcare services, increased awareness about brain tumor treatments, and an improvement in the healthcare infrastructure in countries like China, Japan, and India. The rise in the prevalence of brain tumors due to reasons such as demographic and lifestyle factors has led to the demand for better treatment alternatives. Medical technology and pharmaceutical advancements also are coming up in the region, and they are creating innovative therapies. There is also an extension of healthcare coverage and the effort of governments toward improving the reach of cancer drugs, so the Asia-Pacific market is seen to have promising growth and this is the hub for future investments.

Do You Need any Customization Research on Brain Tumor Drugs Market - Enquire Now

F. Hoffmann-La Roche Ltd – Avastin (Bevacizumab)

Novartis AG – Kymriah (Tisagenlecleucel)

Merck & Co. Inc. – Keytruda (Pembrolizumab)

Pfizer Inc. – Ibrance (Palbociclib)

Amneal Pharmaceuticals LLC – Temozolomide

Amgen Inc. – AMG 595 (Investigational)

NextSource Pharmaceuticals, LLC – Gleostine (Lomustine)

Emcure Pharmaceuticals – Temozolomide

AstraZeneca plc – Selumetinib

Johnson & Johnson Inc. – JNJ-64619178 (Investigational)

Y-mAbs Therapeutics, Inc. – Omburtamab

Shimadzu Corporation – Research & Diagnostic Solutions

Bristol-Myers Squibb – Opdivo (Nivolumab)

Bayer AG – Stivarga (Regorafenib)

Dr. Reddy's Laboratories Ltd – Temozolomide

In July 2024, The FDA approved vorasidenib for treating IDH-mutant low-grade glioma, a breakthrough based on a genetic discovery at the Johns Hopkins Kimmel Cancer Center. This targeted therapy inhibits the mutated IDH gene, slowing tumor growth and advancing brain cancer treatment.

In May 2024, Tovorafenib received approval for select pediatric patients with low-grade glioma, marking a significant advancement in targeted brain tumor treatments. This approval enhances treatment options and improves outcomes for children with this condition.

| Report Attributes | Details |

|---|---|

|

Market Size in 2023 |

USD 2.27 Billion |

|

Market Size by 2032 |

USD 5.25 Billion |

|

CAGR |

CAGR of 9.79 % From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Therapy [Targeted Therapy, Chemotherapy, Immunotherapy, Others] |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

F. Hoffmann-La Roche Ltd, Novartis AG, Merck & Co. Inc., Pfizer Inc., Amneal Pharmaceuticals LLC, Amgen Inc., NextSource Pharmaceuticals, LLC, Emcure Pharmaceuticals, AstraZeneca plc, Johnson & Johnson Inc., Y-mAbs Therapeutics, Inc., Shimadzu Corporation, Bristol-Myers Squibb, Bayer AG, Dr. Reddy's Laboratories Ltd. |

Ans: North America held the dominant position in the global Brain Tumor Drugs market.

Ans: The brain tumor drug market faces challenges including the high cost of treatment, tumor complexity, and insufficient research funding, all of which limit accessibility, particularly in developing countries.

Ans: Technological advancements in diagnostics, drug delivery, and research investments are driving growth in the brain tumor drug market.

Ans: The Brain Tumor Drugs market is projected to reach a value of USD 5.25 billion by 2032, up from USD 2.27 billion in 2023.

Ans: The Brain Tumor Drugs market is expected to grow at a compound annual growth rate (CAGR) of 9.79% during the forecast period.

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research & Academic Institutes Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research & Academic Institutes Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Mortality Rates of Brain Tumors (2023)

5.2 Drug Approval Trends and Pipeline Insights (2020-2032)

5.3 Expenditure on Brain Tumor Treatment, by Source (2023)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and Promotional Activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new Product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Brain Tumor Drugs Market Segmentation, by Therapy

7.1 Chapter Overview

7.2 Targeted Therapy

7.2.1 Targeted Therapy Market Trends Analysis (2020-2032)

7.2.2 Targeted Therapy Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Chemotherapy

7.3.1 Chemotherapy Market Trends Analysis (2020-2032)

7.3.2 Chemotherapy Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Immunotherapy

7.4.1 Immunotherapy Market Trends Analysis (2020-2032)

7.4.2 Immunotherapy Market Size Estimates and Forecasts to 2032 (USD Billion)

7.5 Others

7.5.1 Others Market Trends Analysis (2020-2032)

7.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Brain Tumor Drugs Market Segmentation, by Indication

8.1 Chapter Overview

8.2 Pituitary

8.2.1 Pituitary Market Trends Analysis (2020-2032)

8.2.2 Pituitary Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Meningioma

8.3.1 Meningioma Market Trends Analysis (2020-2032)

8.3.2 Meningioma Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Glioma

8.4.1 Glioma Market Trends Analysis (2020-2032)

8.4.2 Glioma Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Others

8.5.1 Others Market Trends Analysis (2020-2032)

8.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Brain Tumor Drugs Market Segmentation, by Distribution Channel

9.1 Chapter Overview

9.2 Hospital Pharmacy

9.2.1 Hospital Pharmacy Market Trends Analysis (2020-2032)

9.2.2 Hospital Pharmacy Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Retail & Online Pharmacy

9.3.1 Retail & Online Pharmacy Market Trends Analysis (2020-2032)

9.3.2 Retail & Online Pharmacy Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Brain Tumor Drugs Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.2.4 North America Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.2.5 North America Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.2.6.2 USA Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.2.6.3 USA Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.2.7.2 Canada Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.2.7.3 Canada Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.2.8.2 Mexico Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.2.8.3 Mexico Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Brain Tumor Drugs Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.1.6.2 Poland Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.1.6.3 Poland Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.1.7.2 Romania Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.1.7.3 Romania Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.9 turkey

10.3.1.9.1 Turkey Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Brain Tumor Drugs Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.4 Western Europe Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.5 Western Europe Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.6.2 Germany Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.6.3 Germany Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.7.2 France Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.7.3 France Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.8.2 UK Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.8.3 UK Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.9.2 Italy Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.9.3 Italy Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.10.2 Spain Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.10.3 Spain Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.13.2 Austria Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.13.3 Austria Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Brain Tumor Drugs Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia Pacific Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.4 Asia Pacific Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.5 Asia Pacific Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.6.2 China Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.6.3 China Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.7.2 India Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.7.3 India Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.8.2 Japan Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.8.3 Japan Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.9.2 South Korea Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.9.3 South Korea Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.10.2 Vietnam Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.10.3 Vietnam Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.11.2 Singapore Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.11.3 Singapore Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.12.2 Australia Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.12.3 Australia Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia Pacific Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia Pacific Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Brain Tumor Drugs Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.1.4 Middle East Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.1.5 Middle East Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.1.6.2 UAE Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.1.6.3 UAE Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Brain Tumor Drugs Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.2.4 Africa Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.2.5 Africa Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Brain Tumor Drugs Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.6.4 Latin America Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.6.5 Latin America Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.6.6.2 Brazil Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.6.6.3 Brazil Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.6.7.2 Argentina Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.6.7.3 Argentina Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.6.8.2 Colombia Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.6.8.3 Colombia Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Brain Tumor Drugs Market Estimates and Forecasts, by Therapy (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Brain Tumor Drugs Market Estimates and Forecasts, by Indication (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Brain Tumor Drugs Market Estimates and Forecasts, by Distribution Channel (2020-2032) (USD Billion)

11. Company Profiles

11.1 F. Hoffmann-La Roche Ltd

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Product / Services Offered

11.1.4 SWOT Analysis

11.2 Novartis AG

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Product / Services Offered

11.2.4 SWOT Analysis

11.3 Merck & Co. Inc.

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Product / Services Offered

11.3.4 SWOT Analysis

11.4 Amneal Pharmaceuticals LLC

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Product / Services Offered

11.4.4 SWOT Analysis

11.5 Pfizer Inc.

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Product / Services Offered

11.5.4 SWOT Analysis

11.6 Amgen Inc.

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Product / Services Offered

11.6.4 SWOT Analysis

11.7 NextSource Pharmaceuticals, LLC

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Product / Services Offered

11.7.4 SWOT Analysis

11.8 Emcure Pharmaceuticals

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Product / Services Offered

11.8.4 SWOT Analysis

11.9 Johnson & Johnson Inc.

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Product / Services Offered

11.9.4 SWOT Analysis

11.10 AstraZeneca plc

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Product / Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Therapy

Targeted Therapy

Chemotherapy

Immunotherapy

Others

By Indication

Pituitary

Meningioma

Glioma

Others

By Distribution Channel

Hospital Pharmacy

Retail & Online Pharmacy

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization to meet the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five

The Cancer biomarkers market Size was valued at USD 22 billion in 2023, and is expected to reach USD 58.12 billion by 2032, and grow at a CAGR of 11.4% over the forecast period 2024-2032.

The Urology Devices Market valued at USD 34.08 Billion in 2023, projected to hit USD 64.46 Billion by 2032, growing at a 7.35% CAGR from 2024–2032.

The Medical Clothing Market, valued at USD 110 Billion in 2023, The Medical Clothing Market valued USD 85.95 Billion in 2023 and anticipated to reach USD 163.84 billion by 2032 with compound annual growth rate 7.45% over the forecast period 2024-2032.

The Atrial Fibrillation Devices Market was valued at USD 10.30 billion in 2023 and is expected to reach USD 30.47 billion by 2032, growing at a CAGR of 12.85% from 2024-2032.

The Albumin Market Size was valued at USD 6.15 billion in 2023, and is expected to reach USD 10.5 billion by 2032, and grow at a CAGR of 6.1% over the forecast period 2024-2032.

The Antiperspirants and Deodorants Market Size was valued at USD 62,889 million in 2023 and is expected to reach USD 81,920.89 million by 2031, and grow at a CAGR of 3.36% over the forecast period 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd