Get more information on Bone Graft Market - Request Sample Report

The Bone Graft and Substitutes Market size was valued at USD 3.71 Billion in 2023 and is projected to reach USD 6.74 Billion by 2032, with a growing CAGR of 6.87% over the forecast period 2024-2032.

The Bone Graft and Substitutes Market is booming as surgeons are favouring synthetic substitutes for their safety, compatibility, and ability to promote bone healing. Regulatory approvals for these innovative products are on the rise. Additionally, the growing popularity of minimally invasive surgeries for fractures, facial injuries, and sports injuries is propelling the demand for bone graft alternatives. An aging population with increasing bone issues further fuels market growth. Advancements in medical technology are leading to the development of superior bone graft products, improving surgical outcomes and patient safety. Supportive regulatory frameworks and ongoing efforts to create even better products are paving the way for further market expansion.

Extending pace of road wounds and joint issues

The pace of street wounds is on the ascent. For example, as per the WHO, around 20 to 50 million individuals experience non-lethal wounds, and roughly 1.35 million individuals kick the bucket because of street mishaps consistently. In addition, as per the National Trauma Institute, 2014, the financial weight because of injury cases has expanded to USD 671 billion, including medical care expenses and lost efficiency costs. Bone graft has various applications in fixing wounds and infections. It could be utilized on account of different or complex cracks or those that don't recuperate well after starting treatment. It is likewise utilized for a combination that assists two bones with recuperating in a sick joint. The Combination is most frequently done on the spine.

Improvement of biocompatible produced bone associations

Extended interest in dental bone associations

The Significant expense of the medical procedures

The expense of a bone graft fluctuates generally relying upon the circumstance and the state of the patient. For instance, basic bone uniting for dental purposes utilizing engineered bone will cost anyplace from USD 300 to USD 800 for a solitary embed district. At the point when a patient's bone material is obtained from various pieces of the body for bone graft activity, hospitalization is required, which builds the expense. This type of graft additionally requires the administration of a muscular specialist and an anesthesiologist, bringing about a dental bone graft cost of USD 2,500 to USD 3,500.

Chance and entanglements from bone graft methods

High interest in the muscular consideration area

Thorough and practically identical appraisals of well-being spending in every nation are a critical contribution to well-being strategy and in proper order. They are important to help the accomplishments of public and global wellbeing objectives. On February 20, 2019, the WHO delivered another report on worldwide well-being consumption, as indicated by which the worldwide spending on well-being in low-and center pay nations expanded by 6% and in top-level salary nations by 4%. State-run administrations represent under 40%of essential medical services spending. Many organizations are grafting the area in light of the great market and an open door. Existing players are burning through huge amounts of cash on research and improvement to add cutting-edge innovations to their portfolios and keep up with their piece of the pie.

Risk of Complications

As with any medical procedure, bone graft surgeries using substitutes carry some risks of complications such as infection, rejection, or nerve damage.

Strict regulations imposed by governing bodies like the FDA can lead to lengthy and costly approval processes for new bone graft substitutes

Allografts (donated human bone) currently holding the biggest share. These are popular due to their ability to promote bone growth (osteoconductivity) and provide immediate structure. However, synthetic bone grafts are expected to see the fastest growth. Synthetics offer lower disease transmission risk, better biocompatibility, and are generally more accepted by patients. This segment is further fueled by the rising burden of bone disorders and increasing demand in developed countries.

Spinal fusion procedures currently dominate the bone graft market due to their use in treating spinal conditions common among the growing elderly population. However, dental applications are expected to see the fastest growth. This is driven by the increasing popularity of dental implants and bone regeneration techniques, which rely on bone grafts for successful outcomes.

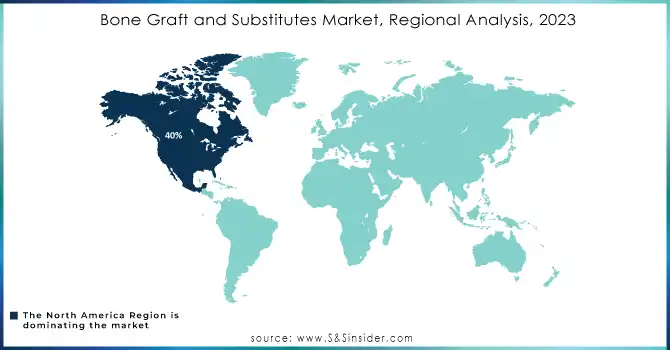

North America overwhelmed the market with more than 40% portion of the worldwide income in 2023. Developing mindfulness connected with the economically available imaginative items, the openness of an advanced medical care structure, and higher medical services use of 16.9% in 2018 is the significant angles adding to the local market development. The market in the U.S. is driving the North American as well as worldwide market by creating the most extreme interest for bone grafts and substitutes on account of the developing number of injury-related wounds as well as instances of muscular infection.

Asia Pacific is assessed to observe rewarding development during the gauge time frame. This development can be ascribed to rising clinical the travel industry and ideal government drives. Then again, tough administrative rules limit the reception in a couple of countries. For example, in South Korea, the item must be supported prior to advertising by the Korean Food and Drug Administration (KFDA). In Australia, the items are directed by the Therapeutic Goods Administration (TGA). The tough administrative viewpoint in Japan confines the passage of unfamiliar players into the country. However, with the most recent endorsement of DBM in Japan in 2019, the allograft market is set to keep worthwhile development in the Asia Pacific over the course of the following 10 years.

Need any customization research on Bone Graft and Substitutes Market - Enquiry Now

The major players are AlloSource, Baxter International Inc., TBF, Johnson & Johnson (DePuy Synthes), Medtronic Plc., Biobank, NuVasive Inc., Stryker Corporation, Xtant Medical Holdings Inc., Smith + Nephew, Zimmer Biomet Holdings Inc., OST Laboratories, Orthofix US LLC, Geistlich Pharma AG and Other Players.

October 2023: Orthofix Medical Inc. launched OsteoCoveTM, a novel FDA-approved synthetic bone graft for various orthopedic and spine surgeries. This innovative product comes in putty and strip forms and boasts exceptional bone-forming properties.

February 2023: NuVasive, Inc. secured FDA approval for their Modulus Cervical interbody implant, further expanding their C360 product line.

June 2022: Medtronic received FDA approval for a ligament-augmenting implant, solidifying their position in the spine surgery market.

March 2022: Zimmer Biomet partnered with Biocomposites to distribute their genex bone graft substitutes.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 3.71 Billion |

| Market Size by 2032 | USD 6.74 Billion |

| CAGR | CAGR of 6.87% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type [Allograft (Demineralized Bone Matrix, Others), Synthetic (Ceramics {HAP, β-TCP, α-TCP, Bi-phasic Calcium Phosphates (BCP), Others}, Composites, Polymers, Bone Morphogenic Proteins)] • By Application [Craniomaxillofacial, Dental, Foot & Ankle, Joint Reconstruction, Long Bone, Spinal Fusion] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | AlloSource, Baxter International Inc., TBF, Johnson & Johnson (DePuy Synthes), Medtronic Plc., Biobank, NuVasive Inc., Stryker Corporation, Xtant Medical Holdings Inc., Smith + Nephew, Zimmer Biomet Holdings Inc., OST Laboratories, Orthofix US LLC, Geistlich Pharma AG |

| Key Drivers | • Extending pace of road wounds and joint issues • Improvement of biocompatible produced bone associations • Extended interest in dental bone associations |

| RESTRAINTS | • The Significant expense of the medical procedures • Chance and entanglements from bone graft methods |

Ans:- The Bone Graft and Substitutes Market was valued at USD 3.71 Billion by 2023.

Ans: The Bone Graft and Substitutes Market is growing at a CAGR of 6.87% over the forecast period 2024-2032.

North America was the greatest revenue contributor in the bone graft and alternatives market.

The forecast period for the Bone Graft and Substitutes Market is 2024 to 2032.

Key Stakeholders Considered in the study: Raw material vendors, Distributors/traders/wholesalers/suppliers, Regulatory authorities, including government agencies and NGO, Commercial research & development (R&D) institutions, Importers and exporters, Government organizations, research organizations, and consulting firms, Trade/Industrial associations, End-use industries are the stake holder of this report.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact Of Russia Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Bone Graft and Substitutes Market Segmentation, By Material Type

9.1 Introduction

9.2 Trend Analysis

9.3 Allograft

9.3.1 Demineralized Bone Matrix

9.3.2 Others

9.4 Synthetic

9.4.1 Ceramics

9.4.1.1 HAP

9.4.1.2 β-TCP

9.4.1.3 α-TCP

9.4.1.4 Bi-phasic Calcium Phosphates (BCP)

9.4.1.5 Others

9.4.2 Composites

9.4.3 Polymers

9.4.4 Bone Morphogenic Proteins (BMP)

10. Bone Graft and Substitutes Market Segmentation, By Application

10.1 Introduction

10.2 Trend Analysis

10.3 Craniomaxillofacial

10.4 Dental

10.5 Foot & Ankle

10.6 Joint Reconstruction

10.7 Long Bone

10.8 Spinal Fusion

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 Trend Analysis

11.2.2 North America Bone Graft and Substitutes Market by Country

11.2.3 North America Bone Graft and Substitutes Market By Material Type

11.2.4 North America Bone Graft and Substitutes Market By Application

11.2.5 USA

11.2.5.1 USA Bone Graft and Substitutes Market By Material Type

11.2.5.2 USA Bone Graft and Substitutes Market By Application

11.2.6 Canada

11.2.6.1 Canada Bone Graft and Substitutes Market By Material Type

11.2.6.2 Canada Bone Graft and Substitutes Market By Application

11.2.7 Mexico

11.2.7.1 Mexico Bone Graft and Substitutes Market By Material Type

11.2.7.2 Mexico Bone Graft and Substitutes Market By Application

11.3 Europe

11.3.1 Trend Analysis

11.3.2 Eastern Europe

11.3.2.1 Eastern Europe Bone Graft and Substitutes Market by Country

11.3.2.2 Eastern Europe Bone Graft and Substitutes Market By Material Type

11.3.2.3 Eastern Europe Bone Graft and Substitutes Market By Application

11.3.2.4 Poland

11.3.2.4.1 Poland Bone Graft and Substitutes Market By Material Type

11.3.2.4.2 Poland Bone Graft and Substitutes Market By Application

11.3.2.5 Romania

11.3.2.5.1 Romania Bone Graft and Substitutes Market By Material Type

11.3.2.5.2 Romania Bone Graft and Substitutes Market By Application

11.3.2.6 Hungary

11.3.2.6.1 Hungary Bone Graft and Substitutes Market By Material Type

11.3.2.6.2 Hungary Bone Graft and Substitutes Market By Application

11.3.2.7 Turkey

11.3.2.7.1 Turkey Bone Graft and Substitutes Market By Material Type

11.3.2.7.2 Turkey Bone Graft and Substitutes Market By Application

11.3.2.8 Rest of Eastern Europe

11.3.2.8.1 Rest of Eastern Europe Bone Graft and Substitutes Market By Material Type

11.3.2.8.2 Rest of Eastern Europe Bone Graft and Substitutes Market By Application

11.3.3 Western Europe

11.3.3.1 Western Europe Bone Graft and Substitutes Market by Country

11.3.3.2 Western Europe Bone Graft and Substitutes Market By Material Type

11.3.3.3 Western Europe Bone Graft and Substitutes Market By Application

11.3.3.4 Germany

11.3.3.4.1 Germany Bone Graft and Substitutes Market By Material Type

11.3.3.4.2 Germany Bone Graft and Substitutes Market By Application

11.3.3.5 France

11.3.3.5.1 France Bone Graft and Substitutes Market By Material Type

11.3.3.5.2 France Bone Graft and Substitutes Market By Application

11.3.3.6 UK

11.3.3.6.1 UK Bone Graft and Substitutes Market By Material Type

11.3.3.6.2 UK Bone Graft and Substitutes Market By Application

11.3.3.7 Italy

11.3.3.7.1 Italy Bone Graft and Substitutes Market By Material Type

11.3.3.7.2 Italy Bone Graft and Substitutes Market By Application

11.3.3.8 Spain

11.3.3.8.1 Spain Bone Graft and Substitutes Market By Material Type

11.3.3.8.2 Spain Bone Graft and Substitutes Market By Application

11.3.3.9 Netherlands

11.3.3.9.1 Netherlands Bone Graft and Substitutes Market By Material Type

11.3.3.9.2 Netherlands Bone Graft and Substitutes Market By Application

11.3.3.10 Switzerland

11.3.3.10.1 Switzerland Bone Graft and Substitutes Market By Material Type

11.3.3.10.2 Switzerland Bone Graft and Substitutes Market By Application

11.3.3.11 Austria

11.3.3.11.1 Austria Bone Graft and Substitutes Market By Material Type

11.3.3.11.2 Austria Bone Graft and Substitutes Market By Application

11.3.3.12 Rest of Western Europe

11.3.3.12.1 Rest of Western Europe Bone Graft and Substitutes Market By Material Type

11.3.2.12.2 Rest of Western Europe Bone Graft and Substitutes Market By Application

11.4 Asia-Pacific

11.4.1 Trend Analysis

11.4.2 Asia Pacific Bone Graft and Substitutes Market by Country

11.4.3 Asia Pacific Bone Graft and Substitutes Market By Material Type

11.4.4 Asia Pacific Bone Graft and Substitutes Market By Application

11.4.5 China

11.4.5.1 China Bone Graft and Substitutes Market By Material Type

11.4.5.2 China Bone Graft and Substitutes Market By Application

11.4.6 India

11.4.6.1 India Bone Graft and Substitutes Market By Material Type

11.4.6.2 India Bone Graft and Substitutes Market By Application

11.4.7 Japan

11.4.7.1 Japan Bone Graft and Substitutes Market By Material Type

11.4.7.2 Japan Bone Graft and Substitutes Market By Application

11.4.8 South Korea

11.4.8.1 South Korea Bone Graft and Substitutes Market By Material Type

11.4.8.2 South Korea Bone Graft and Substitutes Market By Application

11.4.9 Vietnam

11.4.9.1 Vietnam Bone Graft and Substitutes Market By Material Type

11.4.9.2 Vietnam Bone Graft and Substitutes Market By Application

11.4.10 Singapore

11.4.10.1 Singapore Bone Graft and Substitutes Market By Material Type

11.4.10.2 Singapore Bone Graft and Substitutes Market By Application

11.4.11 Australia

11.4.11.1 Australia Bone Graft and Substitutes Market By Material Type

11.4.11.2 Australia Bone Graft and Substitutes Market By Application

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Bone Graft and Substitutes Market By Material Type

11.4.12.2 Rest of Asia-Pacific Bone Graft and Substitutes Market By Application

11.5 Middle East & Africa

11.5.1 Trend Analysis

11.5.2 Middle East

11.5.2.1 Middle East Bone Graft and Substitutes Market by Country

11.5.2.2 Middle East Bone Graft and Substitutes Market By Material Type

11.5.2.3 Middle East Bone Graft and Substitutes Market By Application

11.5.2.4 UAE

11.5.2.4.1 UAE Bone Graft and Substitutes Market By Material Type

11.5.2.4.2 UAE Bone Graft and Substitutes Market By Application

11.5.2.5 Egypt

11.5.2.5.1 Egypt Bone Graft and Substitutes Market By Material Type

11.5.2.5.2 Egypt Bone Graft and Substitutes Market By Application

11.5.2.6 Saudi Arabia

11.5.2.6.1 Saudi Arabia Bone Graft and Substitutes Market By Material Type

11.5.2.6.2 Saudi Arabia Bone Graft and Substitutes Market By Application

11.5.2.7 Qatar

11.5.2.7.1 Qatar Bone Graft and Substitutes Market By Material Type

11.5.2.7.2 Qatar Bone Graft and Substitutes Market By Application

11.5.2.8 Rest of Middle East

11.5.2.8.1 Rest of Middle East Bone Graft and Substitutes Market By Material Type

11.5.2.8.2 Rest of Middle East Bone Graft and Substitutes Market By Application

11.5.3 Africa

11.5.3.1 Africa Bone Graft and Substitutes Market by Country

11.5.3.2 Africa Bone Graft and Substitutes Market By Material Type

11.5.3.3 Africa Bone Graft and Substitutes Market By Application

11.5.2.4 Nigeria

11.5.2.4.1 Nigeria Bone Graft and Substitutes Market By Material Type

11.5.2.4.2 Nigeria Bone Graft and Substitutes Market By Application

11.5.2.5 South Africa

11.5.2.5.1 South Africa Bone Graft and Substitutes Market By Material Type

11.5.2.5.2 South Africa Bone Graft and Substitutes Market By Application

11.5.2.6 Rest of Africa

11.5.2.6.1 Rest of Africa Bone Graft and Substitutes Market By Material Type

11.5.2.6.2 Rest of Africa Bone Graft and Substitutes Market By Application

11.6 Latin America

11.6.1 Trend Analysis

11.6.2 Latin America Bone Graft and Substitutes Market by Country

11.6.3 Latin America Bone Graft and Substitutes Market By Material Type

11.6.4 Latin America Bone Graft and Substitutes Market By Application

11.6.5 Brazil

11.6.5.1 Brazil Bone Graft and Substitutes Market By Material Type

11.6.5.2 Brazil Bone Graft and Substitutes Market By Application

11.6.6 Argentina

11.6.6.1 Argentina Bone Graft and Substitutes Market By Material Type

11.6.6.2 Argentina Bone Graft and Substitutes Market By Application

11.6.7 Colombia

11.6.7.1 Colombia Bone Graft and Substitutes Market By Material Type

11.6.7.2 Colombia Bone Graft and Substitutes Market By Application

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Bone Graft and Substitutes Market By Material Type

11.6.8.2 Rest of Latin America Bone Graft and Substitutes Market By Application

12. Company Profiles

12.1 AlloSource

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 Baxter International Inc.

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 TBF

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 Johnson & Johnson (DePuy Synthesis)

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 Medtronic Plc.

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 Biobank

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 NuVasive Inc.

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 Stryker Corporation

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 Xtant Medical Holdings Inc.

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Smith + Nephew

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

12.10.5 The SNS View

12.11 Zimmer Biomet Holdings Inc.

12.11.1 Company Overview

12.11.2 Financial

12.11.3 Products/ Services Offered

12.11.4 SWOT Analysis

12.11.5 The SNS View

12.12 OST Laboratories

12.12.1 Company Overview

12.12.2 Financial

12.12.3 Products/ Services Offered

12.12.4 SWOT Analysis

12.12.5 The SNS View

13. Competitive Landscape

13.1 Competitive Benchmarking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. USE Cases And Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Material Type

Allograft

Demineralized Bone Matrix

Others

Synthetic

Ceramics

HAP

β-TCP

α-TCP

Bi-phasic Calcium Phosphates (BCP)

Others

Composites

Polymers

Bone Morphogenic Proteins (BMP)

By Application

Craniomaxillofacial

Dental

Foot & Ankle

Joint Reconstruction

Long Bone

Spinal Fusion

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Digital Therapeutics Market size was estimated at USD 6.3 billion in 2023 and is expected to reach USD 50.2 billion by 2032 at a CAGR of 25.9% during the forecast period of 2024-2032.

The Life Science Tools Market size was estimated at USD 158.40 billion in 2023 and is expected to reach USD 407.57 billion by 2032 with a growing CAGR of 11.09% during the forecast period of 2024-2032.

The Antibody Drug Conjugates [ADC] Market was valued at USD 10.28 billion in 2023 and is expected to reach USD 29.10 billion by 2032, growing at a CAGR of 12.29% from 2024-2032.

The Medical Spa Market was valued at USD 18.33 billion in 2023 and is expected to reach USD 61.85 billion by 2032, growing at a CAGR of 14.50% from 2024-2032.

Healthcare Process Mining Software Market was valued at USD 1.15 billion in 2023 and is expected to reach USD 35.66 billion by 2032, growing at a CAGR of 43.29% from 2024-2032.

The Global eClinical Solutions Market, valued at USD 9.82 Billion in 2023, is projected to grow at a 14.02% CAGR, reaching USD 31.90 Billion by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd