Blister Packaging Market Key Insights:

Get more Information on Blister Packaging Market - Request Sample Report

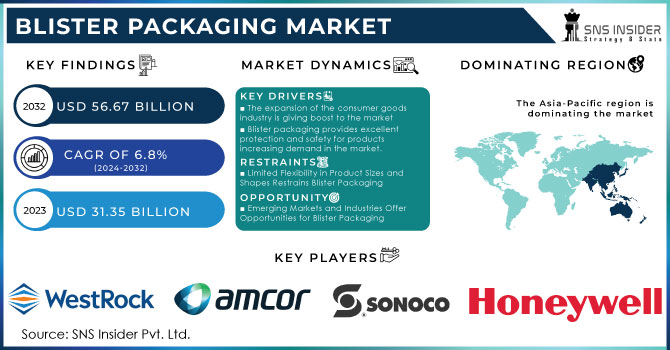

The Blister Packaging Market size was valued at USD 31.35 billion in 2023 and is expected to Reach USD 56.67 billion by 2032 and grow at a CAGR of 6.8% over the forecast period of 2024-2032.

The plastic, aluminum, paper and paperboard segments of the global blister packaging equipment market are also studied for demand and supply. The plastic segment is anticipated to take the largest share out of these three. The packaging used for blister packs is made of PVC (polyvinyl chloride). Blister packaging is the type of packaging that is used the most. Blister packs are typically made from PVC sheets with a thickness of about 0.3 mm. Blister packs are made robust, attractive, and durable using PVC sheets, which also make them difficult to bend. For instance, it was estimated that approximately 57,000 thousand tons of PVC (polyvinyl chloride) were consumed worldwide. Therefore, over the course of the forecast period, such factors are expected to fuel market growth.

This market expansion is attributed to the rising demand from healthcare end-use industries for the tamper-evident packaging designs offered by blister packaging solutions and their high visibility attributes.

This packaging option is frequently used for tamper-evident packaging because it gives products a sealed and obvious container, enabling customers to determine whether the product has been opened or tampered with. This kind of packaging also makes it challenging to substitute the product with fakes or other harmful materials without rupturing the seal, giving customers an extra layer of security.

Furthermore, improvements in packaging design, such as child-resistant packaging configurations, the focus on the use of recyclable materials, and the introduction of smart blister packaging solutions to provide information about the product and monitor its usage, are driving demand for blister packaging.

MARKET DYNAMICS

KEY DRIVERS:

-

The expansion of the consumer goods industry is giving boost to the market

Demand for blister packaging is significantly fueled by the growth of the consumer goods industry, which includes industries like pharmaceuticals, organic food and beverage, and cosmetics. Due to population growth, urbanization, and shifting consumer lifestyles, there is a growing demand for effective and efficient packaging options like blister packs.

-

Blister packaging provides excellent protection and safety for products increasing demand in the market.

RESTRAIN:

-

Limited ability to accommodate different product sizes and shapes is major restrain for blister packaging

The rigid nature of the packaging format may not be appropriate for products that need special shapes, a wide range of dimensions, or larger sizes. The use of blister packaging may be constrained by this restriction in some markets and product lines.

-

The cost of blister packaging materials and equipment can be relatively higher when compared to traditional methods of packaging. This can damage the growth of market.

OPPORTUNITY:

-

The blister packaging market presents opportunities in emerging markets and industries.

The e-commerce industry's explosive growth fuels demand for packaging solutions that are both safe and attractive to the eye. Additionally, sectors like electronics, cosmetics, and food are increasingly using blister packaging for their goods, providing new market opportunities for blister packaging producers.

-

Increased Demand for Pharmaceutical Packaging is major opportunity for the growth of market.

CHALLENGES:

-

The blister packaging industry needs to follow various regulations and standards which can be challenging

It can be difficult and time-consuming to comply with laws pertaining to product safety, labeling, child-resistant packaging, and serialization. The standards for packaging must be met, so manufacturers must keep up with regulatory requirements.

IMPACT OF RUSSIA-UKRAINE WAR

Russia's and Ukraine's ongoing conflict decreased exports of plastics to nations including resin, plastics machinery, plastics molds, and plastic goods. Exports of plastics to Russia fell from $100.1 million to $37.8 million, a 61.4% decrease, and exports to Ukraine fell from $20.3 million to $9.4 million, a 50.4% decline. So far, 2022 has been the last year for Russia and Ukraine to receive any exports of plastic machinery or molds.

Ukraine the major exporter of machinery required for production was affected because of war and trade restrictions. Due to the war, there are now trade restrictions, embargoes, and tariffs between the two nations. These actions have had an impact on the import and export of blister packaging products and materials, obstructing trade and preventing market expansion. Additionally, the geopolitical unrest has made it challenging for companies to forge and maintain dependable business relationships, which has resulted in uncertainty and a decline in cross-border investments.

IMPACT OF ONGOING RECESSION

Market participants may experience losses in 2023 as a result of a significant currency translation gap, which will be followed by declining revenues, narrowing profit margins, and cost pressure on supply chain and logistics.

Beginning in the final quarter of 2022, reducing inflation has been given top priority by all major economies, with 2023 to follow. The economy is skewed, governments are raising interest rates to rein in spending and inflation, oil and gas prices are skyrocketing, inflation is high, and geopolitical issues, affecting the growth of blister packaging market.

Blister packaging demand is declining as a result of businesses cutting back on production and investments during the recession. To cut costs, businesses may decide to postpone or cancel the introduction of new products, reduce production volumes, or optimize their packaging procedures. These actions also help to reduce the market's demand for blister packaging.

KEY MARKET SEGMENTATION

By Raw Material

-

Aluminium

-

Paper & Paperboards

-

Others

By Product Type

-

Carded

-

Clamshell

By Technology

-

Cold Forming

-

Thermoforming Technology

By End Use

-

Healthcare

-

Food

-

Industrial Goods

-

Consumer Goods

-

Pharmaceuticals

-

Medical Devices

REGIONAL ANALYSIS

Asia Pacific region dominated the market of blister packaging with a market share of 55 % in 2023 and will continue to dominate the market during the forecast period. The growth of blister packaging in this region is due to the availability of raw materials in the region required for production such as aluminum and PVC. China in 2020, produced more than 37 million tons and dominated the market which was later followed by India and Canada.

Blister packaging in Asia Pacific regions such as India and China is dominating because of contract manufacturing.

The blister packaging market is expanding in North America. This is due to the region's advanced and well-established end-user industries, like the pharmaceutical and healthcare sectors. The highest CAGR is anticipated for Asia-Pacific during the forecast period, on the other hand. This is brought on by escalating urbanization, industrialization, and increased use of practical packaging options. Numerous end-user verticals, like the packaging industry, are growing and expanding in this region, which will lead to more prosperous and rewarding market growth opportunities.

Get Customized Report as per Your Business Requirement - Enquiry Now

REGIONAL COVERAGE

North America

-

USA

-

Canada

-

Mexico

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

Asia-Pacific

-

Japan

-

South Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of the Middle East & Africa

Latin America

-

Brazil

-

Argentina

-

Rest of Latin American

Key Players

Some major key players in the Blister packaging market are WestRock Company, Constantia Flexibles, Blisterpack Inc, Honeywell International Inc, Amcor plc, Abhinav Enterprises, SteriPack Group, Sonoco Products Company, ACG, WINPAK LTD and other players.

RECENT DEVELOPMENTS

-

Shawpak, The new Shawpak Rigid Blister Machine has been introduced by the UK-based Shawpak medical packaging machinery company.

-

SUDPACK, For the pharmaceutical, medical device, and life science industries, SÜDPACK has unveiled a new recyclable mono-polypropylene blister packaging solution.

-

MAX Solutions, New packaging from MAX Solutions has been unveiled as a possible environmentally friendly replacement for plastic blister packs. The brand-new packaging, known as MAX Ecoblister, combines the paper recyclable qualities of a fiber top card and a PaperFoam tray without sacrificing the tray's compostability.

| Report Attributes | Details |

| Market Size in 2023 | US$ 31.35 Bn |

| Market Size by 2032 | US$ 56.67 Bn |

| CAGR | CAGR of 6.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Raw Material (Plastic Films, Aluminium, Paper & Paperboards, Others) • by Product Type (Carded, Clamshell) • by Technology (Cold Forming, Thermoforming Technology) • by End Use (Healthcare, Food, Industrial Goods, Consumer Goods, Pharmaceuticals, Medical Devices) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | WestRock Company, Constantia Flexibles, Blisterpack Inc, Honeywell International Inc, Amcor plc, Abhinav Enterprises, SteriPack Group, Sonoco Products Company, ACG, WINPAK LTD and other players. |

| Key Drivers | • The expansion of the consumer goods industry is giving boost to the market |

| Market Opportunities | • The blister packaging market presents opportunities in emerging markets and industries. |