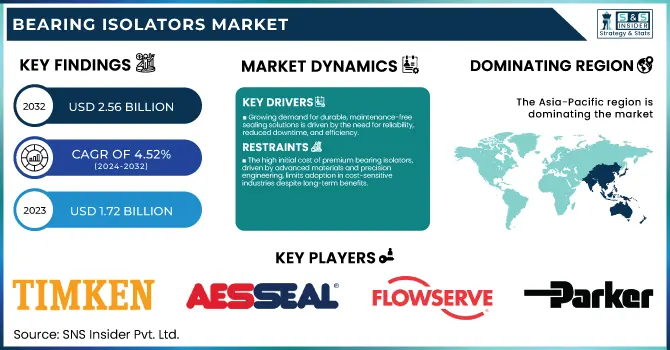

The Bearing Isolators Market was estimated at USD 1.72 billion in 2023 and is expected to reach USD 2.56 billion by 2032, with a growing CAGR of 4.52% over the forecast period 2024-2032. The report on the Bearing Isolators Market offers unique insights into production output trends across regions, highlighting manufacturing utilization rates of key producers. It explores capacity expansions, new production facilities, and supply chain disruptions, emphasizing post-pandemic recovery strategies. Additionally, it covers R&D investments by leading companies, showcasing technological advancements in sealing solutions. A trending addition includes the impact of automation and predictive maintenance adoption, driving demand for advanced bearing protection systems in industrial applications.

To Get more information on Bearing Isolates Market - Request Free Sample Report

Drivers

The rising demand for maintenance-free and long-lasting sealing solutions is driven by the need for enhanced equipment reliability, reduced downtime, and improved operational efficiency across industries.

The growing demand for maintenance-free and long-lasting sealing solutions in industrial applications is driven by the need for enhanced equipment reliability and reduced downtime. Conventional seals quickly wear out due to contact, contaminants, and harsh service conditions, resulting in high maintenance cost due to regular replacements. Unlike traditional seals, which are costly and time-consuming to replace, bearing isolators utilize state-of-the-art non-contact sealing technology to ensure dust, moisture and lubricants stay out of the enclosure, offering a significantly longer finishing life. These solutions are widely adopted across various industries, including manufacturing, oil & gas, and power generation & mining to improve operational efficiency and reduce machine downtime. Moreover, the increasing implementation of predictive maintenance and the integration of Industry 4.0 are also driving the demand for high-performance seals as they help reduce failures and improve the performance of the seals. With organizations targeting both cost-saving and increased equipment reliability, demand for self-lubricating and frictionless sealing technologies is anticipated to continue growth, defining the future of industrial bearing protection solutions.

Restraint

The high initial cost of premium bearing isolators, driven by advanced materials and precision engineering, limits adoption in cost-sensitive industries despite long-term benefits.

Premium bearing isolators offer superior performance, longevity, and maintenance-free operation compared to traditional seals. However, the high upfront investment is still a major obstacle to widespread uptake, particularly in cost-sensitive segments. Seals that rely on a lip like that are cheap, but they also wear out quickly; bearing isolators, however, use advanced materials combined with very precise engineering, making them more costly to install initially. We had to pay up not only because manufacturing is more expensive but also because these designs have to be custom made for particular applications. Although premium isolators greatly decrease long-term maintenance costs and equipment downtime, plenty of firms are still choosing cheaper options because of budgetary constraints or short-term extensions. For small and mid-sized enterprises, the long-term rewards do not always justify the investment, though. With industries prioritizing reliability, it will be essential to develop cost-effective innovations and scalable production techniques to close this pricing gap and create widespread adoption of high-performance bearing isolators.

Opportunities

The growing demand for retrofitting and aftermarket services in the bearing isolators market is driven by the need for cost-effective equipment upgrades, enhanced reliability, and compliance with efficiency standards.

The increasing demand for retrofitting and aftermarket services in the bearing isolators market presents significant growth opportunities. The performance of equipment reliability will drive the demand for these solutions, especially from aging industries that have old machines. Adding bearing isolators to existing systems significantly cuts downtime, maintenance, and oil leakage from lubricants, which is also more economical than replacing equipment. Furthermore, aftermarket services have come into play, involving customized isolator designs and on-site installation assistance for companies that need unique solutions for operational requirements. Particular, upgrading to these systems is a sector investment for manufacturing, oil & gas, and energy to ensure compliance with safety and efficiency regulations. Revolutionising Aftermarket Efforts for Fleet Providers With the advent of predictive maintenance technologies, aftermarket pervaders too have diversified their portfolios with remote monitoring solutions, allowing fleet providers to maintain proactive measures and better performance. Such a rising trend will continue to fuel innovation and market growth in the years to come.

Challenges

Limited awareness, high initial costs, and lack of technical expertise prevent small-scale industries from adopting bearing isolators despite their long-term benefits.

Small-scale industries often face challenges in adopting bearing isolators due to cost constraints and a lack of technical expertise. These businesses often have money to spare, so are reluctant to buy high-performance sealing solutions that are expensive than regular seals. In spite of their contribution to lower maintenance costs and down time, the preliminary expense on bearing isolators can be regarded as high. In addition, most small manufacturers do not have the technical expertise to qualify the performance benefits of bearing isolators, and instead stick with traditional seals. Decision-makers are unaware of the potential for savings through the extended life of equipment and through enhanced efficiency but there is a lack of awareness programs and training to support the need for the concepts. Addressing this hurdle will demand focused educational opportunity, economical initiatives and governmental motivate to create low-cost (SME) for more versatility to adopt advanced bearing protection technologies and improvement in productivity and operational reliability.

By Material

The Metallic segment dominated with a market share of over 66% in 2023, due to its exceptional durability, high load-bearing capacity, and ability to withstand extreme temperatures and harsh environments. Metallic isolators are engineered to provide enhanced durability, corrosion resistance, and load-bearing capabilities, making them a preferred choice for rigorous industrial environments. Metallic bearing isolators play an important role in preventing leakage, contamination and environmental pollution in industries that require an uninterrupted and lossless working environment including oil & gas, manufacturing and power generation sector. The capability of working efficiently at the speed of rotating equipment and prevention from contaminants helps them to be utilized highly. Even further, developments in material coatings and seal technologies are further enhancing the efficiency and longevity of metallic bearing isolators, solidifying their supremacy for industrial applications where reliability and performance are key.

By End-Use

The Oil & Gas segment dominated with a market share of over 34% in 2023, owing to the need for high reliability of equipment, little to no schedule blockage owing to break-down and shielding from severe ecological contaminants. Bearings are used in oil refineries, drilling rigs, and petrochemical plants under extreme conditions-high temperature, moisture, and corrosive substances. These factors increase wear and tear, resulting in expensive maintenance and unplanned shutdowns. Contamination prevention, lubrication retention enhancement, and extended lifespan of rotating equipment are three key operating principle benefits offered by bearing isolators. As a promising bearing protection solution, the industry undergoes frequent tests to offer the most optimal solutions for protecting bearings, providing the highest level of efficacy for preventing damage caused by the loss of bearing fluids. High output isolated bearings oil and gas operations to are producing thousands of times, therefore it is still the most faithful productivity and reduce maintenance costs.

Asia-Pacific region dominated with a market share of over 42% in 2023, due to rapid industrialization, a booming manufacturing sector, and increasing demand across key industries such as automotive, oil & gas, and heavy machinery. The increased economic growth, paired with higher investments in infrastructure and industrial development in the region, contributes by upsurging the adoption rate of bearing isolators for enhancing the efficiency and life of equipment. Emerging production facilities from blue-chip countries like China, India, and Japan is a major contributor to this trend, with emphasis now placed on reducing maintenance costs. Moreover, stricter mandates regarding workplace safety and equipment reliability have been instrumental in industries focusing on high performance sealing solutions. Moreover, the Asia-Pacific market for bearing isolators is further strengthened by the presence of leading manufacturers and suppliers in the region.

North America is emerging as the fastest-growing region in the Bearing Isolators Market, driven by the increasing adoption of advanced sealing technologies to enhance equipment longevity and performance. Aerospace, energy and mining sectors are among those pumping up demand, with a focus on efficiency, reliable use and maintenance cost cutting. This, in addition to stringent environmental regulations that will accelerate the industrial automation market growth. The fast growing is further accelerated by the presence of prominent players and continued technological developments being made in bearing protective methods. Increasing investment in infrastructure, along with a growing focus on predictive maintenance strategies, is also spurring market adoption. All these aspects position North America as the primary growth hotspot in the bearing isolators market over the coming years.

Get Customized Report as per Your Business Requirement - Enquiry Now

Some of the major key players in the Bearing Isolators Market

Timken Company (Labyrinth Bearing Isolators, Magnetic Bearing Isolators)

AESSEAL (Bearing Protection Seals, Non-Contact Bearing Isolators)

Flowserve Corporation (Bearing Protection Systems, Mechanical Seals)

Parker Hannifin Corporation (Composite Bearing Isolators, Rotary Seals)

John Crane (Non-Contact Bearing Isolators, Labyrinth Seals)

Garlock Sealing Technologies (Bearing Isolators, GYLON Seals)

Baldor Electric Company (Custom Bearing Isolators, Motor Protection Seals)

Advanced Sealing International (Metal Bearing Isolators, High-Speed Seals)

Isomag Corporation (Magnetic Bearing Isolators, Containment Seals)

Inpro/Seal (VBXX-D Bearing Isolators, Air Mizer Seals)

SKF (SKF Speedi-Sleeve, Bearing Sealing Solutions)

EagleBurgmann (Labtecta Bearing Isolators, Mechanical Seals)

Saint-Gobain (Omniseal Bearing Isolators, Polymer Sealing Solutions)

Freudenberg Sealing Technologies (Simrit Bearing Isolators, Non-Contact Seals)

SealRyt Corporation (Custom Bearing Isolators, Shaft Seals)

Rexnord Corporation (Bearing Isolator Rings, Contact Seals)

EnPro Industries (Bearing Sealing Solutions, Rotating Equipment Seals)

Waukesha Bearings (Bearing Protection Systems, Hydrodynamic Seals)

Helix Linear Technologies (Precision Bearing Isolators, Rotary Shaft Seals)

Technetics Group (Advanced Bearing Isolators, Metal Sealing Solutions)

Suppliers for (magnetic bearing isolators, offering superior sealing solutions for rotating equipment) on Bearing Isolators Market

Isomag

Superproof Seals Engineering Pvt. Ltd.

Sinoseal Holding Co., Ltd.

Flowserve

M Barnwell Services

Pack Seals Engineering

Actum Sweden AB

S.G. Engineering Works

Vinayak Components

Belt And Bearing House Private Limited

Recent Development

In December 2024: Dover Corporation announced that Waukesha Bearings, a subsidiary within its Fluid Management Segment and a global leader in custom-engineered hydrodynamic and magnetic bearing systems, had acquired Inpro/Seal Company. Inpro/Seal, a leading designer and manufacturer of bearing isolator technologies, is headquartered in Rock Island, Illinois.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 1.72 Billion |

| Market Size by 2032 | USD 2.56 Billion |

| CAGR | CAGR of 4.52% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Metallic, Non-metallic) • By End Use (Oil & Gas, Chemical, Mining, Paper & Pulp, Metal Processing, Manufacturing) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Timken Company, AESSEAL, Flowserve Corporation, Parker Hannifin Corporation, John Crane, Garlock Sealing Technologies, Baldor Electric Company, Advanced Sealing International, Isomag Corporation, Inpro/Seal, SKF, EagleBurgmann, Saint-Gobain, Freudenberg Sealing Technologies, SealRyt Corporation, Rexnord Corporation, EnPro Industries, Waukesha Bearings, Helix Linear Technologies, Technetics Group. |

Ans: The Bearing Isolators Market is expected to grow at a CAGR of 4.52% during 2024-2032.

Ans: The Bearing Isolators Market was USD 1.72 billion in 2023 and is expected to reach USD 2.56 billion by 2032.

Ans: The rising demand for maintenance-free and long-lasting sealing solutions is driven by the need for enhanced equipment reliability, reduced downtime, and improved operational efficiency across industries.

Ans: The “Metallic” segment dominated the Bearing Isolators Market.

Ans: Asia-Pacific dominated the Bearing Isolators Market in 2023

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Production Output, by Region (2020-2023)

5.2 Manufacturing Utilization Rates, by Key Producers (2020-2023)

5.3 Capacity Expansion & New Production Facilities (2020-2023)

5.4 Supply Chain Disruptions & Recovery Trends (2020-2023)

5.5 Investment in R&D, by Leading Companies (2020-2023)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Bearing Isolators Market Segmentation, By Material

7.1 Chapter Overview

7.2 Metallic

7.2.1 Metallic Market Trends Analysis (2020-2032)

7.2.2 Metallic Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Non-metallic

7.3.1 Non-metallic Market Trends Analysis (2020-2032)

7.3.2 Non-metallic Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Bearing Isolators Market Segmentation, By End Use

8.1 Chapter Overview

8.2 Oil & Gas

8.2.1 Oil & Gas Market Trends Analysis (2020-2032)

8.2.2 Oil & Gas Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Chemical

8.3.1 Chemical Market Trends Analysis (2020-2032)

8.3.2 Chemical Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Mining

8.4.1 Mining Market Trends Analysis (2020-2032)

8.4.2 Mining Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Paper & Pulp

8.4.1 Paper & Pulp Market Trends Analysis (2020-2032)

8.4.2 Paper & Pulp Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Metal Processing

8.4.1 Metal Processing Market Trends Analysis (2020-2032)

8.4.2 Metal Processing Market Size Estimates and Forecasts to 2032 (USD Billion)

8.7 Manufacturing

8.4.1Manufacturing Market Trends Analysis (2020-2032)

8.4.2 Manufacturing Market Size Estimates and Forecasts to 2032 (USD Billion)

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Bearing Isolators Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.2.4 North America Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.2.5.2 USA Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.2.6.2 Canada Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.2.7.2 Mexico Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Bearing Isolators Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.1.5.2 Poland Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.1.6.2 Romania Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Bearing Isolators Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.4 Western Europe Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.5.2 Germany Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.6.2 France Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.7.2 UK Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.8.2 Italy Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.9.2 Spain Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.12.2 Austria Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific Bearing Isolators Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia Pacific Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.4 Asia Pacific Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.5.2 China Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.5.2 India Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.5.2 Japan Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.6.2 South Korea Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.2.7.2 Vietnam Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.8.2 Singapore Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.9.2 Australia Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia Pacific Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Bearing Isolators Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.1.4 Middle East Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.1.5.2 UAE Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Bearing Isolators Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.2.4 Africa Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.5.2.7.2 Rest of Africa Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Bearing Isolators Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.6.4 Latin America Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.6.5.2 Brazil Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.6.6.2 Argentina Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.6.7.2 Colombia Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Bearing Isolators Market Estimates and Forecasts, By Material (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Bearing Isolators Market Estimates and Forecasts, By End-Use (2020-2032) (USD Billion)

10. Company Profiles

10.1 Timken Company

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

110.1.4 SWOT Analysis

10.2 AESSEAL

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Flowserve Corporation

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Parker Hannifin Corporation

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 John Crane

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 Garlock Sealing Technologies

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 Baldor Electric Company

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Advanced Sealing International

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Isomag Corporation

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Inpro/Seal

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segmentation

By Material

Metallic

Non-metallic

By End Use

Oil & Gas

Chemical

Mining

Paper & Pulp

Metal Processing

Manufacturing

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Food Processing and Handling Equipment Market size was estimated at USD 108.63 Billion in 2023 and is expected to reach USD 168.79 Billion by 2032 with a growing at a CAGR of 5.02% during the forecast period of 2024-2032.

The Construction Equipment Market Size was estimated at USD 179.37 billion in 2023 and is expected to arrive at USD 345.08 billion by 2032 with a growing CAGR of 7.54% over the forecast period 2024-2032.

Textile Machinery Market was estimated at USD 29.12 billion in 2023 and is expected to reach USD 46.24 billion By 2032 at a CAGR of 5.27% from 2024 to 2032.

The Welding Electrodes Market size was estimated at USD 5.49 billion in 2023 and is expected to reach USD 10.84 billion By 2032 at a CAGR of 7.85% during the forecast period of 2024-2032.

The Safety Valves Market size was estimated at USD 4.86 Billion in 2023 and is expected to reach USD 8.50 Billion by 2032 with a growing CAGR of 6.42% during the forecast period of 2024-2032.

The Arc Welding Torch Market was estimated at USD 2.10 billion in 2023 and is expected to reach USD 3.28 billion by 2032, with a growing CAGR of 5.09% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd