Autonomous Ships Market Report Scope & Overview:

To get more information on Autonomous Ships Market - Request Free Sample Report

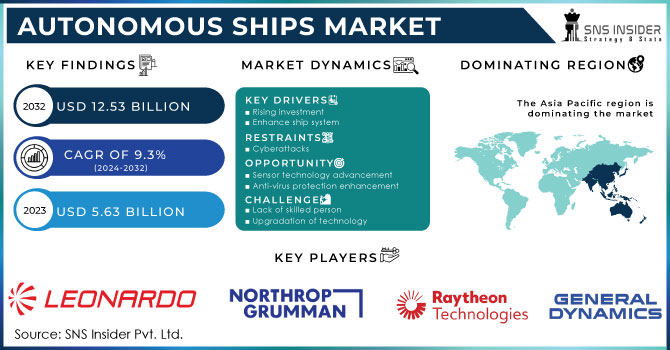

The Autonomous Ships Market Size was valued at USD 5.63 billion in 2023 and is expected to reach USD 12.53 billion by 2032 with a growing CAGR of 9.3% over the forecast period 2024-2032.

An autonomous vessel is an unmanned vessel where all processes are performed automatically with limited human interaction. Many of the activities of private ships are monitored and operated by a coastal person. The control system used by the independent ship is based on many technologies such as radar, sonar, thermal imaging, HD cameras, and LiDAR. Technological advances have increased communication at sea and the development of sensory technology is expected to increase the demand for private vessels. Automatic vessels are controlled and monitored using out-of-board control centers with human intervention. In addition, private vessels have their entire operation controlled by advanced applications, allowing them to make their own decisions and actions.

Private ships gain independence by using technologies found in private cars and autopilots. The sensors provide information with the help of infrared and visual spectrum cameras provided by radar, sonar, lidar, GPS, and AIS, which will be able to provide information for use on the go. Additional data such as weather data and deep-sea navigation and traffic systems from coastal areas help the ship to plan a safe route. The data is then processed by intelligence systems either on the ship itself or on the coast, providing the right route and pattern of decision. However, Automation on ships around the world has increased the risk of cyber threats as these ships follow satellite routes during their voyages.

MARKET DYNAMICS

KEY DRIVERS

-

Rising investment

-

Enhance ship system

RESTRAINTS

-

Cyberattacks

OPPORTUNITIES

-

Sensor technology advancement

-

Anti-virus protection enhancement

CHALLENGES

-

Lack of skilled person

-

Upgradation of technology

IMPACT OF COVID-19

According to the International Chamber of Shipping, maritime vessels make up about 90 percent of all international trade. As a result of the COVID-19 outbreak, cargo and passenger ships around the world have been removed from ports by local authorities, which is why 300,000 merchant sailors have been trapped at sea for months, in addition to their contractual contracts. the ICS and the International Air Transport Association issued a joint declaration calling on governments to take urgent action to make it easier to change flights. ICS estimates that every month about 100,000 sailors reach the end of their employment contract and need to be repatriated. However, many authorities use laws to prevent passersby from passing through their area, either to return home or to join a ship.

COVID-19, however, has led to a number of MASS-related projects being suspended. Yara Birke land was launched in Romania in February 2020 and was expected to arrive at the Vard Breivik shipping port in Norway in May 2020, where control and navigation systems would be installed and tested. As a result of this epidemic and changes in the look of ships around the world, Yara International halted construction. It is expected that the economic impact of COVID-19 will result in further suspension of the private shipping project.

Furthermore, factors such as increased demand for marine freight transportation and ship operational safety fuel market expansion. However, the possibility of exploitation through system hacking and growing network complexity impede industry growth. Furthermore, the trend toward complete automation in the transportation sector, as well as an increase in maritime safety standards, are likely to generate various prospects for market expansion. Major drivers driving market expansion include increased operational safety for ships and quick advances and improvements in the maritime industry. Furthermore, systems with built-in components such as AI, IoT, advanced navigation systems, and others improve ship operation, propelling the autonomous ships industry forward.

The market is divided into two segments based on application: commercial and military. According to the forecast period, the commercial segment of the Global Autonomous Ships Market is predicted to grown at the fastest rising CAGR. The expansion in seaborne trade and tourism around the world is related to the segment's growth. During the forecast period, the military segment is also expected to increase significantly.

The autonomous ships market is divided into three categories: totally autonomous, remotely operated, and partial automation. The increased investment in creating autonomous ships in the European region, particularly in Scandinavian countries, can be ascribed to the expansion of the completely autonomous section of the autonomous ships market.

KEY MARKET SEGMENTATION

By Fuel Type

-

Carbon Neutral Fuels

-

LNG

-

Electric

-

Heavy Fuel Oil

-

Marine Engine Fuel

By Ship Type

-

Commercial

-

Passenger

-

Defense

By Component

-

Hardware

-

Software

By Application

-

Commercial

-

Military

By Type

-

Semi-autonomous

-

Fully-autonomous

-

Remotely autonomous

REGIONAL ANALYSIS

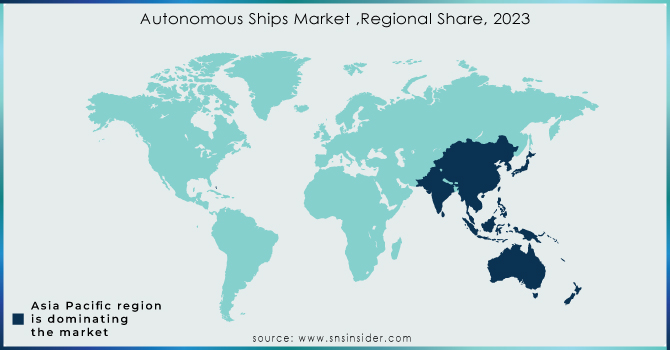

The market for autonomous ships has been researched for North America, Europe, Asia Pacific, and the rest of the world. Asia Pacific is expected to have the greatest share of the global market. Over the years, Asia Pacific has seen fast economic expansion, which has increased maritime trade. This increase in sea trade has resulted in a greater demand for ships to convey manufactured commodities throughout the world. As a result, the demand for autonomous ships in the Asia Pacific region has skyrocketed.

Need any customization research on Autonomous Ships Market - Enquiry Now

REGIONAL COVERAGE:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS

The Major Players are Raytheon Technologies Corporation, General Dynamics Corporation, Northrop Grumman Corporation, Thales, Leonardo Company, BAE Systems, L3Harris Technologies, Inc, Elbit Systems Ltd, and other players

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 5.63 Billion |

| Market Size by 2032 | US$ 12.53 Billion |

| CAGR | CAGR of 9.3% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Fuel Type (Carbon Neutral Fuels, LNG, Electric, and Heavy Fuel Oil/Marine Engine Fuel) • By Ship Type (Commercial, Passenger, and Defense) • By Component (Hardware and Software) • By Application (Commercial, Military) • By Type (Semi-autonomous, Fully-autonomous, and remotely autonomous) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Raytheon Technologies Corporation, General Dynamics Corporation , Northrop Grumman Corporation, Thales, Leonardo Company, BAE Systems, L3Harris Technologies, Inc, Elbit Systems Ltd, and other players. |

| DRIVERS | • Rising investment • Enhance ship system |

| RESTRAINTS | • Cyberattacks |