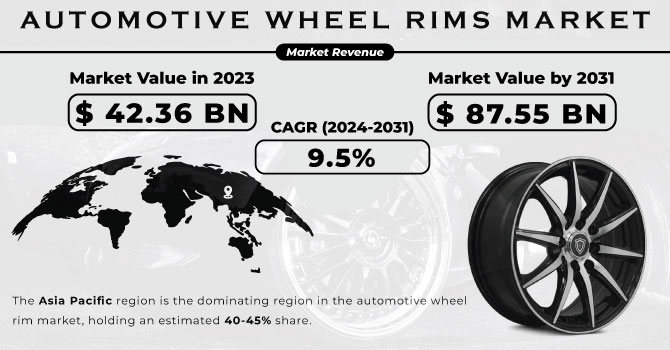

The Automotive Wheel Rims Market Size was valued at USD 42.36 billion in 2023 and is expected to reach USD 87.55 billion by 2031 and grow at a CAGR of 9.5% over the forecast period 2024-2031.

As the demand for high-performance and fuel-efficient vehicles rises, lightweight wheel edges are getting to be dynamically well known. These rims significantly impact driving experience by progressing the power-to-weight proportion, driving to superior ride quality and in general vehicle execution.

Get More Information on Automotive Wheel Rims Market - Request Sample Report

The well-designed rims improve stability and ensure precise rolling, braking, and other basic activities. Beyond performance, wheel rims play a crucial aesthetic role. The different plans and wraps up accessible cater to a wide extend of consumer preferences, further driving market growth. Traditionally, alloys and steel have been the essential materials for rim production. In any case, high-performance vehicles like sports cars are progressively utilizing progressed materials like carbon fibre. Carbon fibre boasts prevalent properties like high tensile strength, thermal and chemical resistance, and remarkable lightweight characteristics, making it a compelling choice for automotive wheel rims.

KEY DRIVERS:

Urbanization and infrastructure development in emerging markets fuel the demand for automobiles and subsequently, automotive wheels.

The rise in urbanization and infrastructure development, especially in developing markets, directly fuels the demand for automobiles and subsequently, automotive wheels. This drift is driven by the extending number of people moving to cities, where car ownership gets to be a more practical and desirable means of personal transportation. Improved infrastructure like roads and highways further encourages car utilization, driving to a rising number of vehicles on the road and a ensuing increase in the demand for automotive wheels.

Lightweight materials, advanced production methods, and innovative designs fuel automotive wheel market expansion.

RESTRAINTS:

Fluctuations in raw material prices impact automotive wheel manufacturing costs.

The automotive wheel market faces a potential issue in the form of fluctuating raw material prices. Steel, aluminium, and carbon fibre which are the essential materials utilized in wheel generation, are subject to market changes. When the costs of these materials rise, it directly influences the manufacturing cost of car wheels. This can lead to increased costs for the final product, influencing customer affordability and possibly influencing generally market demand. Manufacturers may need to adjust their pricing strategies or seek alternative materials to moderate the effect of such cost swings and maintain affordability for their products.

Shifting consumer preferences for EVs, autonomous vehicles, and specific wheel designs necessitate product adaptations by manufacturers.

OPPORTUNITIES:

Manufacturers prioritize advanced facilities, new machinery, and FEA analysis to gain global market recognition.

CHALLENGES:

Developing nations' low adoption, fluctuating material costs, and the need for lightweight, compliant wheels with rising replacements hinder automotive wheel market growth.

The Russia-Ukraine war has severely disrupted the automotive wheel rim market, creating several crisis. The Ukraine is the key supplier of components like wiring harnesses has seen production halts and delays, impacting European and global production. Additionally, Russia, a major source of vital metals like nickel and palladium crucial for wheel production, faces sanctions and export disruptions, leading to significant price hikes. This combined effect is estimated to cut global car production by millions, directly impacting the demand for new wheels. Long-term consequences are likely to include cost inflation as rising raw material and transportation costs translate to higher wheel rim prices, potentially dampening consumer demand. Manufacturers will likely seek alternative suppliers for critical materials, potentially altering the global market landscape. Furthermore, the need for fuel efficiency and emission reduction will likely push manufacturers towards lightweight materials like carbon fibre, despite potential cost challenges.

Economic slowdowns has reduced consumer spending power which leads to a decline in new car purchases, possibly causing a critical drop in demand for new wheel rims, demand for new wheel rims, during such periods. The buyers limit their budgets, driving to postponed non-essential car maintenance like wheel replacements affecting the aftermarket portion and possibly causing a 5-10% decline in sales. Automakers may moreover be constrained to reduce generation or stop operations, specifically affecting the demand for original equipment manufacturer (OEM) wheel rims, possibly leading to a decrease of 15-25% in demand. The long-term impacts incorporate descending weight on costs due to reduced demand, possibly affecting profit margins by 5-10%. Unsold wheel rim inventory can accumulate, driving to potential capacity costs and cash flow issues for producers and wholesalers. Furthermore, weaker players may struggle to survive, possibly driving to market consolidation and reduced competition, possibly resulting in a shift in market share of 5-10% towards larger players.

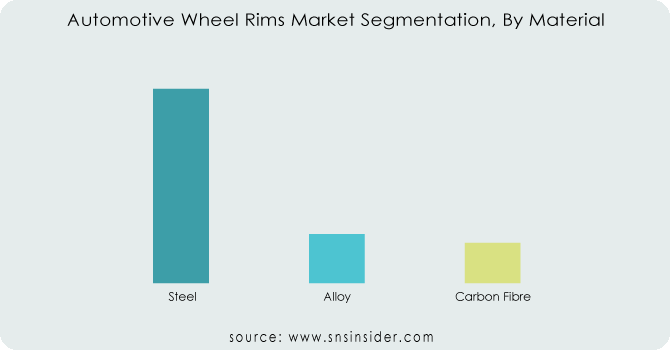

By Material:

Steel

Alloy

Carbon Fibre

Steel is the dominating sub-segment in the Automotive Wheel Rims Market by material, estimated at around 60-70% of market share. Steel is significantly cheaper than alloy or carbon fibre, making it the preferred choice for budget-conscious consumers. Steel rims are known for their strength and ability to withstand heavy loads, making them ideal for commercial vehicles.

Get Customized Report as per your Business Requirement - Request For Customized Report

By Vehicle Type:

Passenger cars

Commercial vehicles

Passenger Cars is the dominating sub-segment in the Automotive Wheel Rims Market by vehicle type, estimated at around 70-80% of market share. Passenger cars significantly outnumber commercial vehicles on the road, leading to higher demand for their wheels. Passenger car owners often prioritize visually appealing and performance-enhancing wheels, driving demand for alloy and carbon fibre options.

By Rim Size:

13”-15”

16”-18”

19”-21”

Above 21”

16”-18” is the dominating sub-segment in the Automotive Wheel Rims Market by rim size, estimated at around 40-50% of market share. This size range provides a wide variety of visually appealing designs. Performance: Offers good handling characteristics without significantly impacting fuel efficiency. Strikes a balance between cost and performance compared to larger sizes.

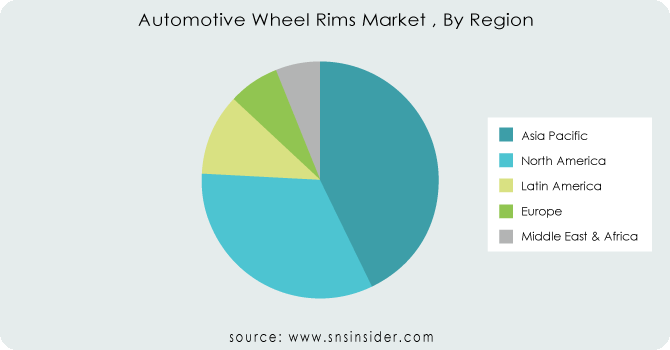

The Asia Pacific region is the dominating region in the automotive wheel rim market, holding an estimated 40-45% share. This dominance stems from a thriving automotive manufacturing hub in countries like China and India, leading to a high demand for wheel rims. The steel wheels dominate due to their affordability and cater to a budget-conscious consumer base, the region is also witnessing a shift towards larger and more visually appealing wheels, potentially leading to increased adoption of alloy and even carbon fibre options in the future. North America is the second highest region in this market holding a share of approximately 30-35%, driven by its well-established automotive industry and a strong aftermarket sector. Consumers here often favour larger wheels, contributing to the demand for alloy and carbon fibre options alongside the prevalent steel rims.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major key players are TSW Alloy Wheels (US), Fuel Offroad Wheels (US), CLN Group, Maxion Wheels Inc. (US), Euromax Wheel (US), VOXX International Corporation (US), Sota Offroad (US), Mobile Hi-Tech Wheels Inc. (US), Status Wheels (TUFF A.T) (US), Wheel Pros Holdings, LLC (US), Topy Industries Limited (Japan) and other key players.

RECENT DEVELOPMENTS:

In Sept., 2022 - Maxion Wheels, the world's top wheel producer, announced the opening of its newest truck steel wheels plant in Turkey, built in partnership with Inci Holding. This marks a significant expansion for the company.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 42.36 Billion |

| Market Size by 2031 | US$ 87.55 Billion |

| CAGR | CAGR of 9.5% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Material (Steel, Alloy, Carbon Fibre) • by Vehicle Type (Passenger cars, Commercial vehicles) • by Rim Size (13”-15”, 16”-18”, 19”-21”, Above 21”), |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America |

| Company Profiles | TSW Alloy Wheels (US), Fuel Offroad Wheels (US), CLN Group, Maxion Wheels Inc. (US), Euromax Wheel (US), VOXX International Corporation (US), Sota Offroad (US), Mobile Hi-Tech Wheels Inc. (US), Status Wheels (TUFF A.T) (US), Wheel Pros Holdings, LLC (US), and Topy Industries Limited (Japan) |

| Key Drivers | •Due to increased vehicle production and the continued trend of vehicle weight reduction. •The need for lightweight wheels to reduce vehicle weight and improve fuel efficiency. |

| RESTRAINTS | •By fluctuating raw material prices in the EV battery production process. •The market is projected to be constrained by a lack of standardization in automobile wheel production methods. |

Ans:- The market size is expected to reach USD 87.55 billion by 2031.

Ans:- Material, Vehicle Type, and Rim Size are the different segments of the market.

Ans:- Yes.

Ans:- Asia pacific region is anticipated to be the primary driver of the market.

Ans:- Raw material vendors, Distributors/traders/wholesalers/suppliers, Regulatory authorities, government agencies and NGOs, Trade/Industrial associations, and End-use industries are the stakeholder of this report.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Automotive Wheel Rims Market Segmentation, By Material

9.1 Introduction

9.2 Trend Analysis

9.3 Steel

9.4 Alloy

9.5 Carbon Fibre

10. Automotive Wheel Rims Market Segmentation, By Vehicle Type

10.1 Introduction

10.2 Trend Analysis

10.3 Passenger cars

10.4 Commercial vehicles

11. Automotive Wheel Rims Market Segmentation, By Rim Size

11.1 Introduction

11.2Trend Analysis

11.3 13”-15”

11.4 16”-18”

11.5 19”-21”

11.6 Above 21”

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 Trend Analysis

12.2.2 North America Automotive Wheel Rims Market Segmentation, By Country

12.2.3 North America Automotive Wheel Rims Market Segmentation, By Material

12.2.4 North America Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.2.5 North America Automotive Wheel Rims Market Segmentation, By Rim Size

12.2.6 USA

12.2.6.1 USA Automotive Wheel Rims Market Segmentation, By Material

12.2.6.2 USA Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.2.6.3 USA Automotive Wheel Rims Market Segmentation, By Rim Size

12.2.7 Canada

12.2.7.1 Canada Automotive Wheel Rims Market Segmentation, By Material

12.2.7.2 Canada Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.2.7.3 Canada Automotive Wheel Rims Market Segmentation, By Rim Size

12.2.8 Mexico

12.2.8.1 Mexico Automotive Wheel Rims Market Segmentation, By Material

12.2.8.2 Mexico Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.2.8.3 Mexico Automotive Wheel Rims Market Segmentation, By Rim Size

12.3 Europe

12.3.1 Trend Analysis

12.3.2 Eastern Europe

12.3.2.1 Eastern Europe Automotive Wheel Rims Market Segmentation, by Country

12.3.2.2 Eastern Europe Automotive Wheel Rims Market Segmentation, By Material

12.3.2.3 Eastern Europe Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.2.4 Eastern Europe Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.2.5 Poland

12.3.2.5.1 Poland Automotive Wheel Rims Market Segmentation, By Material

12.3.2.5.2 Poland Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.2.5.3 Poland Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.2.6 Romania

12.3.2.6.1 Romania Automotive Wheel Rims Market Segmentation, By Material

12.3.2.6.2 Romania Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.2.6.4 Romania Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.2.7 Hungary

12.3.2.7.1 Hungary Automotive Wheel Rims Market Segmentation, By Material

12.3.2.7.2 Hungary Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.2.7.3 Hungary Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.2.8 Turkey

12.3.2.8.1 Turkey Automotive Wheel Rims Market Segmentation, By Material

12.3.2.8.2 Turkey Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.2.8.3 Turkey Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.2.9 Rest of Eastern Europe

12.3.2.9.1 Rest of Eastern Europe Automotive Wheel Rims Market Segmentation, By Material

12.3.2.9.2 Rest of Eastern Europe Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.2.9.3 Rest of Eastern Europe Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3 Western Europe

12.3.3.1 Western Europe Automotive Wheel Rims Market Segmentation, by Country

12.3.3.2 Western Europe Automotive Wheel Rims Market Segmentation, By Material

12.3.3.3 Western Europe Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.4 Western Europe Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.5 Germany

12.3.3.5.1 Germany Automotive Wheel Rims Market Segmentation, By Material

12.3.3.5.2 Germany Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.5.3 Germany Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.6 France

12.3.3.6.1 France Automotive Wheel Rims Market Segmentation, By Material

12.3.3.6.2 France Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.6.3 France Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.7 UK

12.3.3.7.1 UK Automotive Wheel Rims Market Segmentation, By Material

12.3.3.7.2 UK Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.7.3 UK Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.8 Italy

12.3.3.8.1 Italy Automotive Wheel Rims Market Segmentation, By Material

12.3.3.8.2 Italy Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.8.3 Italy Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.9 Spain

12.3.3.9.1 Spain Automotive Wheel Rims Market Segmentation, By Material

12.3.3.9.2 Spain Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.9.3 Spain Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.10 Netherlands

12.3.3.10.1 Netherlands Automotive Wheel Rims Market Segmentation, By Material

12.3.3.10.2 Netherlands Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.10.3 Netherlands Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.11 Switzerland

12.3.3.11.1 Switzerland Automotive Wheel Rims Market Segmentation, By Material

12.3.3.11.2 Switzerland Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.11.3 Switzerland Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.1.12 Austria

12.3.3.12.1 Austria Automotive Wheel Rims Market Segmentation, By Material

12.3.3.12.2 Austria Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.12.3 Austria Automotive Wheel Rims Market Segmentation, By Rim Size

12.3.3.13 Rest of Western Europe

12.3.3.13.1 Rest of Western Europe Automotive Wheel Rims Market Segmentation, By Material

12.3.3.13.2 Rest of Western Europe Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.3.3.13.3 Rest of Western Europe Automotive Wheel Rims Market Segmentation, By Rim Size

12.4 Asia-Pacific

12.4.1 Trend Analysis

12.4.2 Asia-Pacific Automotive Wheel Rims Market Segmentation, by Country

12.4.3 Asia-Pacific Automotive Wheel Rims Market Segmentation, By Material

12.4.4 Asia-Pacific Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.5 Asia-Pacific Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.6 China

12.4.6.1 China Automotive Wheel Rims Market Segmentation, By Material

12.4.6.2 China Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.6.3 China Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.7 India

12.4.7.1 India Automotive Wheel Rims Market Segmentation, By Material

12.4.7.2 India Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.7.3 India Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.8 Japan

12.4.8.1 Japan Automotive Wheel Rims Market Segmentation, By Material

12.4.8.2 Japan Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.8.3 Japan Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.9 South Korea

12.4.9.1 South Korea Automotive Wheel Rims Market Segmentation, By Material

12.4.9.2 South Korea Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.9.3 South Korea Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.10 Vietnam

12.4.10.1 Vietnam Automotive Wheel Rims Market Segmentation, By Material

12.4.10.2 Vietnam Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.10.3 Vietnam Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.11 Singapore

12.4.11.1 Singapore Automotive Wheel Rims Market Segmentation, By Material

12.4.11.2 Singapore Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.11.3 Singapore Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.12 Australia

12.4.12.1 Australia Automotive Wheel Rims Market Segmentation, By Material

12.4.12.2 Australia Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.12.3 Australia Automotive Wheel Rims Market Segmentation, By Rim Size

12.4.13 Rest of Asia-Pacific

12.4.13.1 Rest of Asia-Pacific Automotive Wheel Rims Market Segmentation, By Material

12.4.13.2 Rest of Asia-Pacific Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.4.13.3 Rest of Asia-Pacific Automotive Wheel Rims Market Segmentation, By Rim Size

12.5 Middle East & Africa

12.5.1 Trend Analysis

12.5.2 Middle East

12.5.2.1 Middle East Automotive Wheel Rims Market Segmentation, by Country

12.5.2.2 Middle East Automotive Wheel Rims Market Segmentation, By Material

12.5.2.3 Middle East Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.2.4 Middle East Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.2.5 UAE

12.5.2.5.1 UAE Automotive Wheel Rims Market Segmentation, By Material

12.5.2.5.2 UAE Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.2.5.3 UAE Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.2.6 Egypt

12.5.2.6.1 Egypt Automotive Wheel Rims Market Segmentation, By Material

12.5.2.6.2 Egypt Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.2.6.3 Egypt Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.2.7 Saudi Arabia

12.5.2.7.1 Saudi Arabia Automotive Wheel Rims Market Segmentation, By Material

12.5.2.7.2 Saudi Arabia Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.2.7.3 Saudi Arabia Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.2.8 Qatar

12.5.2.8.1 Qatar Automotive Wheel Rims Market Segmentation, By Material

12.5.2.8.2 Qatar Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.2.8.3 Qatar Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.2.9 Rest of Middle East

12.5.2.9.1 Rest of Middle East Automotive Wheel Rims Market Segmentation, By Material

12.5.2.9.2 Rest of Middle East Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.2.9.3 Rest of Middle East Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.3 Africa

12.5.3.1 Africa Automotive Wheel Rims Market Segmentation, by Country

12.5.3.2 Africa Automotive Wheel Rims Market Segmentation, By Material

12.5.3.3 Africa Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.3.4 Africa Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.3.5 Nigeria

12.5.3.5.1 Nigeria Automotive Wheel Rims Market Segmentation, By Material

12.5.3.5.2 Nigeria Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.3.5.3 Nigeria Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.3.6 South Africa

12.5.3.6.1 South Africa Automotive Wheel Rims Market Segmentation, By Material

12.5.3.6.2 South Africa Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.3.6.3 South Africa Automotive Wheel Rims Market Segmentation, By Rim Size

12.5.3.7 Rest of Africa

12.5.3.7.1 Rest of Africa Automotive Wheel Rims Market Segmentation, By Material

12.5.3.7.2 Rest of Africa Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.5.3.7.3 Rest of Africa Automotive Wheel Rims Market Segmentation, By Rim Size

12.6 Latin America

12.6.1 Trend Analysis

12.6.2 Latin America Automotive Wheel Rims Market Segmentation, by country

12.6.3 Latin America Automotive Wheel Rims Market Segmentation, By Material

12.6.4 Latin America Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.6.5 Latin America Automotive Wheel Rims Market Segmentation, By Rim Size

12.6.6 Brazil

12.6.6.1 Brazil Automotive Wheel Rims Market Segmentation, By Material

12.6.6.2 Brazil Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.6.6.3 Brazil Automotive Wheel Rims Market Segmentation, By Rim Size

12.6.7 Argentina

12.6.7.1 Argentina Automotive Wheel Rims Market Segmentation, By Material

12.6.7.2 Argentina Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.6.7.3 Argentina Automotive Wheel Rims Market Segmentation, By Rim Size

12.6.8 Colombia

12.6.8.1 Colombia Automotive Wheel Rims Market Segmentation, By Material

12.6.8.2 Colombia Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.6.8.3 Colombia Automotive Wheel Rims Market Segmentation, By Rim Size

12.6.9 Rest of Latin America

12.6.9.1 Rest of Latin America Automotive Wheel Rims Market Segmentation, By Material

12.6.9.2 Rest of Latin America Automotive Wheel Rims Market Segmentation, By Vehicle Type

12.6.9.3 Rest of Latin America Automotive Wheel Rims Market Segmentation, By Rim Size

13. Company Profiles

13.1 TSW Alloy Wheels (US)

13.1.1 Company Overview

13.1.2 Financial

13.1.3 Products/ Services Offered

13.1.4 SWOT Analysis

13.1.5 The SNS View

13.2 Fuel Offroad Wheels (US)

13.2.1 Company Overview

13.2.2 Financial

13.2.3 Products/ Services Offered

13.2.4 SWOT Analysis

13.2.5 The SNS View

13.3 CLN Group

13.3.1 Company Overview

13.3.2 Financial

13.3.3 Products/ Services Offered

13.3.4 SWOT Analysis

13.3.5 The SNS View

13.4 Maxion Wheels Inc. (US)

13.4.1 Company Overview

13.4.2 Financial

13.4.3 Products/ Services Offered

13.4.4 SWOT Analysis

13.4.5 The SNS View

13.5 Euromax Wheel (US)

13.5.1 Company Overview

13.5.2 Financial

13.5.3 Products/ Services Offered

13.5.4 SWOT Analysis

13.5.5 The SNS View

13.6 VOXX International Corporation (US)

13.6.1 Company Overview

13.6.2 Financial

13.6.3 Products/ Services Offered

13.6.4 SWOT Analysis

13.6.5 The SNS View

13.7 Sota Offroad (US)

13.7.1 Company Overview

13.7.2 Financial

13.7.3 Products/ Services Offered

13.7.4 SWOT Analysis

13.7.5 The SNS View

13.8 Mobile Hi-Tech Wheels Inc. (US)

13.8.1 Company Overview

13.8.2 Financial

13.8.3 Products/ Services Offered

13.8.4 SWOT Analysis

13.8.5 The SNS View

13.9 Status Wheels (TUFF A.T) (US)

13.9.1 Company Overview

13.9.2 Financial

13.9.3 Products/ Services Offered

13.9.4 SWOT Analysis

13.9.5 The SNS View

13.10 Wheel Pros Holdings, LLC (US)

13.10.1 Company Overview

13.10.2 Financial

13.10.3 Products/ Services Offered

13.10.4 SWOT Analysis

13.10.5 The SNS View

13.11 Topy Industries Limited (Japan)

13.11.1 Company Overview

13.11.2 Financial

13.11.3 Products/ Services Offered

13.11.4 SWOT Analysis

13.11.5 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

14.3.1 Industry News

14.3.2 Company News

14.3.3 Mergers & Acquisitions

15. Use Case and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Tire Machinery Market size was recorded at USD 2.08 Bn in 2023 and is expected to reach USD 2.90 Bn by 2032. And grow at a CAGR of 3.8% over the forecast period of 2024-2032.

The Automotive Rear Seat Infotainment Market, valued at USD 555.1 Billion in 2023, is anticipated to reach USD 1233.87 Billion by 2031 experiencing a compound annual growth rate (CAGR) of 10.5% throughout the forecast period from 2024 to 2031.

The Car Manufacturing Market Size was valued at USD 2.08 Billion in 2023, and is expected to reach USD 10.96 Billion by 2032, and grow at a CAGR of 20.30 % over the forecast period 2024-2032.

The Internal Combustion Engine (ICE) Market demand size was recorded at USD 113 Bn by 2023 and is expected to reach USD 268.8 Bn during 2032, growing at a CAGR of 10.1% over the forecast period 2024-2032.

The Yacht Market Size was valued at USD 9.5 billion in 2023 and is expected to reach USD 14.58 billion by 2031 and grow at a CAGR of 5.5% over the forecast period 2024-2031.

The Automotive Gear Market Size will reach to USD 52.26 billion by 2032 and grow at an CAGR of 3.2% over 2024-2032 & was valued at USD 40.05 billion in 2023.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd