To get more information on Automotive Stainless Steel Tube Market - Request Free Sample Report

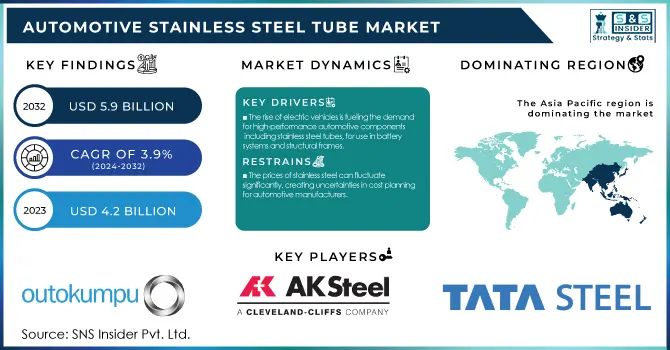

The Automotive Stainless Steel Tube Market Size was valued at USD 4.2 Billion in 2023 and is expected to reach USD 5.9 Billion by 2032, growing at a CAGR of 3.9% over the forecast period 2024-2032.

The automotive stainless steel tube market is driven by increasing demand for lightweight, durable, and corrosion-resistant materials in automotive manufacturing. With governmental regulations across the world becoming stricter in emission norms and demand for fuel-efficient vehicles soaring globally, automotive manufacturers are forced to adopt lighter and performance-improvement materials. The EU CO2 emissions standards, which come into effect this year, require that fleet-wide CO2 emissions from new cars are reduced to 95g/km from the previous target of 130g/km, according to the European Commission. The demand for stainless steel tubes in the automotive sector has received an additional boost from this focus on fuel-efficient vehicles, especially for exhaust systems, fuel lines, and structural applications.

In the U.S., CAFE (Corporate Average Fuel Economy) standards require manufacturers to average 54.5 mpg across their vehicle lineup by 2025, as enforced by the National Highway Traffic Safety Administration (NHTSA). The regulations are encouraging the adoption of lightweight and high-strength materials such as stainless steel tubes, which are ideal for auto parts that need to be both strong and low-weight. Similarly, the Faster Adoption and Manufacturing of Hybrid and Electric Vehicles (FAME) scheme of the Indian government is expected to trigger the growth of electric vehicles, thereby creating further demand for stainless steel tubes. That is, electric vehicles (EVs) and hybrid vehicles use more parts that need corrosion resistance than any conventional vehicle when compared to weight, volume, or use. With automotive companies facing rigorous laws across the globe and consumers wanting tougher, durable, lightweight designs, the demand for stainless steel tubes is only going to increase, experts say. The automotive sector is expected to witness the demand for stainless steel tubes during the forecast period owing to the growing adoption of electric and hybrid vehicles, as well as tightening regulatory measures.

Drivers

Stainless steel tubes are gaining popularity in the automotive industry due to their lightweight and corrosion-resistant properties, helping to reduce vehicle weight and improve fuel efficiency.

The rise of electric vehicles is fueling the demand for high-performance automotive components, including stainless steel tubes, for use in battery systems and structural frames.

Increasing demand for lightweight materials, owing to the rise in the automotive industry's focus on fuel efficiency and sustainability, is one of the key factors boosting this market growth. The preferred models are stainless steel tubes that not only merely reduce the weight of the vehicle but also resist corrosive damage. This further enhances fuel economy by reducing carbon emissions and addressing some of the strictest environmental regulations within many territories. The European Union, for example, has established very high CO2 emissions reduction targets for vehicles manufactured in the region, and the automakers are responding by relying increasingly on lightweight materials such as tubes of stainless steel for exhaust systems and chassis and the like. The two organizations note from an International Energy Agency (IEA) report that lightweight material adoption can cut vehicle weight by up to 15%, which directly enhances fuel economy.

As such the lightweight characteristics of stainless-steel tubes are becoming more valuable in the EV sector as they aid in boosting efficiency and range of the battery. Thermal management is essential for battery systems in EVs, and stainless-steel tubes are used in the cooling circuits, delivering high performance, while remaining lightweight. The drive for lightweight components that enable the adoption of environmentally friendly technologies in the automotive sector will further boost the demand for stainless steel tubes over the forecast period.

Restraints:

The manufacturing process for stainless steel tubes can be expensive, particularly due to the high raw material costs, which may deter some automotive manufacturers from adopting this material.

The prices of stainless steel can fluctuate significantly, creating uncertainties in cost planning for automotive manufacturers

The high cost of production for the manufacturing of stainless-steel tubes is among the key restraints for the automotive stainless steel tube market. Making these tubes can be costly in terms of materials, energy, and advanced manufacturing methods. The base alloy stainless steel is expensive & production involves custom equipment & skilled labour thus resulting in a higher price for the entire process. In addition, high-quality stainless-steel tube manufacturing also includes welding, and seamless tube forming, as well as used for precision shaping which also causes a price overhead to automotive manufacturers. Consequently, these high production costs restrict the penetration of stainless-steel tubes heavily in some price-sensitive segments of the automotive market.

By Product

The welded tube segment dominated the market with a 92% revenue share in 2023, owing to its high application in automotive components, such as exhaust systems, chassis, and fuel lines. Stainless steel tubes have the right tensile strength and corrosion resistance, are cost-effective, and offer versatility making welded stainless-steel tubes often a choice material for automotive manufacturing. This is mainly because they can be made in large numbers at low production costs making them ideal to be used in mass production for the automotive industry.

In addition, the seamless tube segment is anticipated to register a competitive compound annual growth rate (CAGR) throughout the forecast period. The growth is due to rising demand for high-performance and durable automotive components. These have more strength and are suitable for high-temperature applications as compared to seamless stainless-steel tubes, making them an excellent choice for applications such as hydraulic lines, pressure vessels, high-temperature engine components, etc. Additionally, seamless tubes are more reliable than welded tubes in certain high-stress applications, where the integrity of the tube is paramount.

By Application

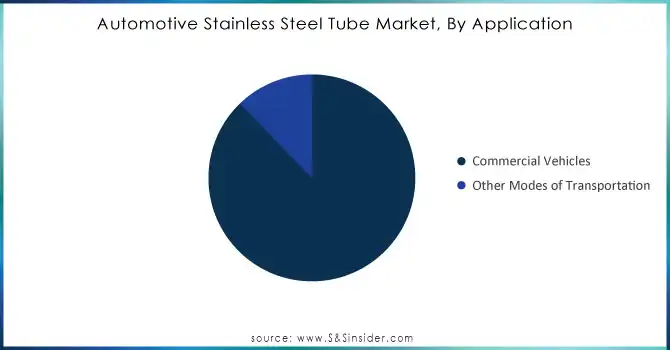

In 2023, the commercial vehicles segment captured the largest revenue share of 51%, attributed to the demand for durable and corrosion-resistant materials in the production of trucks, buses, and other commercial vehicles. Special commercial vehicles usually run in a more severe environment, heavy loads and long-running lines or other materials which need to be good and sufficient to be able to support. Due to its non-corrosive, high strength, and low weight nature, stainless steel tubes are perfectly fit for these applications.

Furthermore, the increasing demand for durable and low-maintenance vehicles in the logistics and transportation industries is anticipated to boost the demand for automotive stainless-steel tubes in commercial vehicles. The demand for commercial vehicles in North America has been increasing steadily, with the U.S. trucking industry alone accounting for more than $700 billion in revenue for the U.S. economy in 2022, according to the U.S. Department of Transportation. Demand for dependable and efficient components, like stainless-steel tubes that convey the durability and performance of the vehicle, increases as the industry grows. In addition, government initiatives for commercial vehicle solutions, including electric trucks and electric buses, are expected to boost the demand for stainless steel tubes in the segment.

Need any customization research on Aviation Crew Management Systems Market - Enquiry Now

In 2023, Asia Pacific held the highest market share of around 51.0% in terms of revenue in the Automotive Stainless Steel Tube Market. This leading position can be attributed to a few essential factors, such as the rapid industrialization of the region, strong automotive manufacturing capabilities, and increasing demand for high-performance automotive components. The automotive vehicle manufacturing industry is being dominated by emerging economies such as Japan, India, South Korea, and China among others, which in turn is fuelling the demand for stainless steel tubes for various automotive critical applications including fuel lines, exhaust systems, and structural components. This boom is mainly due to the massive participation of big players such as Toyota, Hyundai, and Honda in the region. Moreover, government programs such as the 2025 "Made in China 2025" and "FAME" scheme in India to encourage the use of electric vehicles will further propel the demand for high-level materials such as stainless-steel tubes. Further, Asia Pacific has a competitive edge in cost-effective manufacturing and the skilled labour force is steering the automotive stainless steel tube market from the forefront.

North American region is expected to grow at a significant growth rate, due to stringent environmental regulations, efficient fuel vehicles, presence of major automotive manufacturers. In particular, the U.S. has played an important role in the promotion of the market as the CAFE standards of NHTSA have been lobbying for the use of lightweight materials in the form of stainless-steel tubes to prove efficiency in terms of fuel consumption. Additionally, a higher level of electric vehicle (EV) production in the area has fueled the need for long-lasting, corrosion-resistant components driving the market.

Jindal Stainless, in January 2023, also supplied stainless steel for various parts of the Mumbai metro project, including roofs, outer panels, car bodies, and other structural components.

MARCEGAGLIA STEEL S.p.A. purchased a stainless-steel electric furnace plant in Sheffield, U.K. in January 2023. This is the first investment they have made in steel production, completing supply chain integration and offering a more sustainable and competitive product portfolio.

Outokumpu (Outokumpu Stainless Steel Tubes, Duplex Stainless-Steel Tubes)

AK Steel (304 Stainless Steel Tubes, 316 Stainless Steel Tubes)

MARCEGAGLIA STEEL S.p.A. (Stainless Steel Coils, Stainless Steel Sheets)

Tata Steel (Stainless Steel Tubing for Exhaust Systems, High-Temperature Resistant Tubes)

Jindal Stainless (Jindal Stainless Steel Tubes, Stainless Steel Welded Tubes)

Thyssenkrupp (Stainless Steel Seamless Tubes, Stainless Steel Welded Tubes)

SSAB (SSAB Boron Steel Tubes, Advanced High-Strength Steel Tubes)

JFE Steel Corporation (JFE Stainless Tubes, JFE Exhaust Tubes)

Nippon Steel (Seamless Stainless-Steel Tubes, Welded Stainless Steel Tubes)

Sandvik Materials Technology (Sanicro Stainless Steel Tubes, Sanmac Stainless Tubes)

Vallourec (Seamless Tubes for Automotive Applications, Stainless Steel Tubes for Chassis)

ArcelorMittal (Stainless Steel Tubes for Auto Manufacturing, Automotive Exhaust Tubes)

Ford Motor Company

General Motors

Toyota Motor Corporation

Volkswagen Group

BMW AG

Mercedes-Benz (Daimler AG)

Honda Motor Co., Ltd.

Hyundai Motor Company

Nissan Motor Co., Ltd.

Tesla Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 4.2 Billion |

| Market Size by 2032 | USD 5.9 Billion |

| CAGR | CAGR of 3.9% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Welded Tube, Seamless Tube) • By Application (Passenger Cars, Commercial Vehicles, Other Modes of Transportation) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Outokumpu, AK Steel, Tata Steel, ThyssenKrupp, MARCEGAGLIA STEEL S.p.A., SSAB, JFE Steel Corporation, Jindal Stainless, Nippon Steel, Sandvik Materials Technology, Vallourec, ArcelorMittal. |

| Key Drivers | • Stainless steel tubes are gaining popularity in the automotive sector due to their lightweight and corrosion-resistant properties, helping to reduce vehicle weight and improve fuel efficiency. • The rise of electric vehicles is fueling the demand for high-performance automotive components, including stainless steel tubes, for use in battery systems and structural frames. |

| RESTRAINTS | • The manufacturing process for stainless steel tubes can be expensive, particularly due to the high raw material costs, which may deter some automotive manufacturers from adopting this material. |

Ans. The projected market size for the Automotive Stainless Steel Tube Market is USD 5.9 Billion by 2032.

Ans: The Asia Pacific region dominated the Automotive Stainless Steel Tube Market in 2023.

Ans. The CAGR of the Automotive Stainless Steel Tube Market is 3.9% During the forecast period of 2024-2032.

And: The welded tube product segment dominated the Automotive Stainless Steel Tube Market with a 92% share, in 2023.

Ans:

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.2 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Vehicle Production and Sales Volumes, 2020-2032, by Region

5.2 Emission Standards Compliance, by Region

5.3 Vehicle Technology Adoption, by Region

5.4 Consumer Preferences, by Region

5.5 Aftermarket Trends (Data on vehicle maintenance, parts, and services)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Automotive Stainless Steel Tube Market Segmentation, By Product

7.1 Chapter Overview

7.2 Welded Tube

7.2.1 Welded Tube Market Trends Analysis (2020-2032)

7.2.2 Welded Tube Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Seamless Tube

7.3.1 Seamless Tube Market Trends Analysis (2020-2032)

7.3.2 Seamless Tube Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Automotive Stainless Steel Tube Market Segmentation, By Application

8.1 Chapter Overview

8.2 Passenger Cars

8.2.1 Passenger Cars Market Trends Analysis (2020-2032)

8.2.2 Passenger Cars Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Commercial Vehicles

8.3.1 Commercial Vehicles Market Trends Analysis (2020-2032)

8.3.2 Commercial Vehicles Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Other Modes of Transportation

8.4.1 Other Modes of Transportation Market Trends Analysis (2020-2032)

8.4.2 Other Modes of Transportation Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America Automotive Stainless Steel Tube Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.4 North America Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.5.2 USA Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.6.2 Canada Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.7.2 Mexico Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.5.2 Poland Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.6.2 Romania Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.7.2 Hungary Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.1.8 Turkey

9.3.1.8.1 Turkey Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.8.2 Turkey Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.4 Western Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.5.2 Germany Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.6.2 France Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.7.2 UK Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.8.2 Italy Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.9.2 Spain Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.12.2 Austria Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific Automotive Stainless Steel Tube Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia Pacific Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.4 Asia Pacific Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.5.2 China Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.5.2 India Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.5 Japan

9.4.5.1 Japan Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.5.2 Japan Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.6.2 South Korea Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.7.2 Vietnam Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.8.2 Singapore Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.9.2 Australia Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia Pacific Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East Automotive Stainless Steel Tube Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.4 Middle East Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.5.2 UAE Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.6.2 Egypt Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.8.2 Qatar Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa Automotive Stainless Steel Tube Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2.4 Africa Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2.5.2 South Africa Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2.7.2 Rest of Africa Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America Automotive Stainless Steel Tube Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.4 Latin America Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.6.5 Brazil

9.6.5.1 Brazil Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.5.2 Brazil Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.6.2 Argentina Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.7.2 Colombia Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America Automotive Stainless Steel Tube Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America Automotive Stainless Steel Tube Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

10. Company Profiles

10.1 Outokumpu

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

110.1.4 SWOT Analysis

10.2 AK Steel

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Tata Steel

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 ThyssenKrupp

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 MARCEGAGLIA STEEL S.p.A.

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 SSAB

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 JFE Steel Corporation

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Jindal Stainless

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 Nippon Steel

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Sandvik Materials Technology

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Product

Welded Tube

Seamless Tube

By Application

Passenger Cars

Commercial Vehicles

Other Modes of Transportation

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Automotive Operating System Market Size was valued at USD 8.88 Billion in 2023 and is expected to reach USD 21.09 Billion by 2032 and grow at a CAGR of 10.1% over the forecast period 2024-2032.

Automotive Filters Market Size was valued at USD 21.28 billion in 2023 and is expected to reach USD 28.15 billion by 2031 and grow at a CAGR of 3.78% over the forecast period 2024-2031.

The Electric Vehicle Charger Operations and Maintenance Services Market will Hit USD 1990.10 Mn by 2032 with a CAGR of 24.01% by Forecast Period 2024-2032

The Off-Road Vehicles Market Size was valued at USD 22.9 billion in 2023 and will reach to USD 37.07 billion by 2032 and grow at a CAGR of 5.5% by 2024-2032

The Vacuum Truck Market Size was valued at USD 2.0 Billion in 2023 and is expected to reach USD 3.7 Bn by 2032, growing at a CAGR of 7.1% by 2024-2032.

The Fuel Cell Powertrain Market Size was valued at $761.62 million in 2023 & will reach $11958.62 Million by 2031 and grow at a CAGR of 48.2% by 2024-2031

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd