AUTOMOTIVE NIGHT VISION SYSTEM MARKET SIZE:

To get more information on Automotive Night Vision System Market - Request Free Sample Report

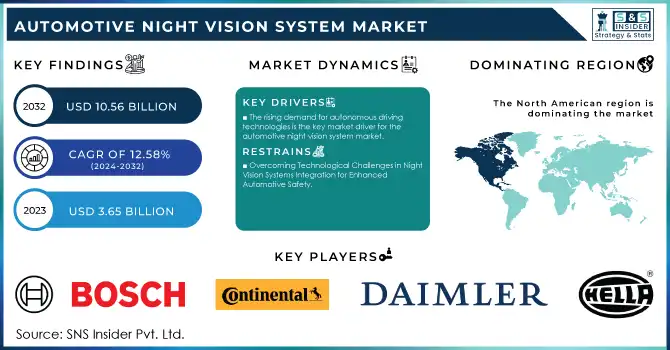

The Automotive Night Vision System Market Size was valued at USD 3.65 Billion in 2023 and is expected to reach USD 10.56 Billion by 2032 and grow at a CAGR of 12.58% over the forecast period 2024-2032.

The automotive night vision system market is growing due to the development of technology and the rise in patron demand for advanced security features. Night vision technology is also helping as vehicle manufacturers continue to improve driver assistance systems for low-light conditions. The use of infrared cameras and several other sensors reveals hazards before the regular headlights show them, giving drivers a better view of the road ahead to see pedestrians, animals, and obstacles on or near the roadway. Such an additional layer of protection is especially attractive to those consumers who consider safety at the top of their list when it comes to vehicle choices.

In 2023, more than 20% of premium and luxury models from brands such as BMW, Audi, and Cadillac offer night vision systems, indicating increasing penetration in the upper portions of the vehicle market. The new systems, which include thermal cameras produce about 90% detection accuracy on pedestrians and animals as far away as 300 meters well beyond the standard headlight range of about 120 meters.

Moreover, increasing knowledge of road safety regulations and the installation of tough safety standards across different markets is further propelling the growth of automotive night vision system market. By making models with elements like night vision integrated into them, automakers stick to the letter of upmarket safety features regulations as well, which are always changing. In addition, the increasing popularity of luxury and high-performance automobiles with advanced technology is also providing an upward push to the market. With consumers looking for not just performance but something that comes built with more safety as well as convenience, the take-up of night vision systems looks set to remain on an upward trend.

In 2023, 90% of new high-end vehicle models in Europe and North America were compliant with the safety regulations incentivizing night vision or advanced driver assistance technologies. According to a 2024 survey, 72% of consumers buying luxury cars were open to paying a premium for advanced safety tech such as night vision.

MARKET DYNAMICS

KEY DRIVERS:

The rising demand for autonomous driving technologies is the key market driver for the automotive night vision system market.

The automotive industry is rapidly pivoting to autonomous vehicles and that trend requires advanced sensing technologies. Night vision systems increase the ability to recognize natural surroundings in any type of lighting environment.

In 2023, around 25% of new autonomous vehicle prototypes included night vision for improved low-light detection. Global automotive firms invested over USD 50 billion in autonomous R&D, focusing on advanced sensing techs like night vision and thermal cameras.

Additionally, 35% of autonomous fleets from companies like Tesla and Waymo tested night vision systems to enhance low-visibility performance. This heightened awareness of the surroundings is crucial for safe navigation, especially when light conditions are poor and traditional lighting may be insufficient. As manufacturers spend billions on R&D to create fully self-driving cars, (integrating night vision systems) is a critical part of the tools that will need to be developed.

Rising consumer safety and accident prevention is another major factor propelling the market growth.

Traffic accidents have been an alarming situation worldwide, and manufacturers are trying to introduce new safety features that can lower the chances of a collision. Night vision systems aid this goal by giving drivers improved visibility so they can make better decisions in life-or-death situations. The result of this safety-conscious trend has been strategic manufacturing measures resulting in the general availability of advanced technologies that have made night vision systems an increasingly popular consumer commodity. In addition, with vehicle safety ratings and consumer awareness of these technologies developing year after year, the pressure for automakers to include night vision on their cars has increased. As a result, this tendency not merely propels the expansion of the night vision system market but also promotes a larger movement toward safer driving spaces in general.

In 2023, more than 1.3 million people were killed on the road, according to a WHO report many of them in low-visibility conditions proving that industry have much room for improvement when it comes to night-time safety.

According to a 2023 survey 68% of drivers sought advanced safety features in vehicles a 15% increase from the previous year. US insurers have been giving as much as 10% discounts on cars with night vision systems since 2024 when nighttime accident claims fell by 20%.

RESTRAIN:

Overcoming Technological Challenges in Night Vision Systems Integration for Enhanced Automotive Safety

The factor that is expected to restrain the growth of the automotive night vision system market over the forecast period is technological limitations related to sensor technologies. Though night vision systems have improved, obstacles remain in creating sensors able to detect and classify objects properly in a wide range of environmental conditions like fog rain, or glare from headlights. Communicating seamlessly between the different components, such as night vision cameras, displays or other driver assistance systems is challenging. There is a lot of time and effort that manufacturers need to put in for effective integration. This considerably delays product development and deployment. An example is BMW, which has been developing and refining its night vision systems so they better integrate with the other advanced driver assistance systems, how well functional integration takes place remains one of the challenges faced.

KEY MARKET SEGMENTS

BY TECHNOLOGY

The Far Infrared technology segment dominated the Automotive Night Vision System Market with a 64% share in 2023 owing to its high-quality ability for thermal imaging and object detection. Whenever it has low-light conditions, the FIR sensors work perfectly as they detect heat signatures from a being, vehicle, or obstacle. This helps drivers to see beyond their headlamp beams, great for safety during night driving. FIR systems have established application reliability and sound functionality, which are primarily responsible for the share of automotive manufacturers adopting FIR technology.

Near Infrared technology is expected to grow at the fastest CAGR from 2024 to 2032. The NIR systems allow for imaging at very high resolution and capture of clear visuals free from ambient reflection interferences. This technology is progressively combined with advanced driver assistance systems and cars, as it improves situational awareness and supplies information to make decisions. Amid warping consumer demand toward safety and automation, NIR tech will be a wave that automakers increasingly surf. In addition, this demand for NIR sensor technology will be supported by its growing consumer preference and continuous technological development in NIR sensors.

BY COMPONENT

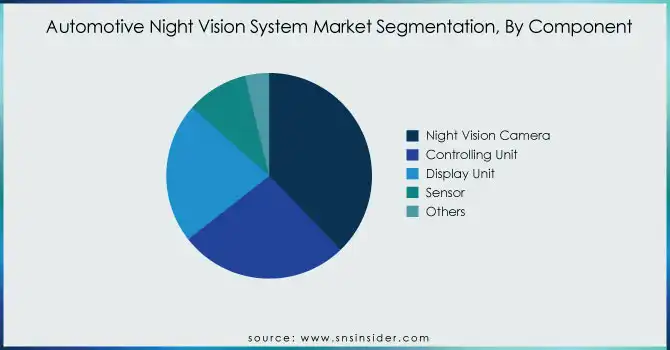

The Night Vision Camera segment held the largest market share of 37% in 2023 due to its crucial advantages in improving driver safety and visibility under low-light conditions. Night vision cameras both thermal and infrared-based allow the driver to be able to see further than their stock headlights would normally allow. Night’s 3D detection of pedestrians, animals, and other obstacles has proven their effectiveness in making them an essential feature in modern vehicles. With increasing consumer awareness regarding such safety technologies, manufacturers are incorporating night vision cameras in their vehicle designs, thus contributing to a substantial market share.

The Display Unit segment will witness the fastest growth at a CAGR from 2024 to 2032 due to display technology advancement and increasing focus towards intuitive human-machine interface. At the same time, as night vision systems become more integrated with other vehicle technologies (e.g., advanced driver assistance systems [ADAS]), high-quality display units will also be required. Modern displays allow you to see more information immediately available, which makes the experience better with clearer visuals and interaction of night vision in an optimal way. In addition, increasing penetration of connected vehicles and implementation of the display via infotainment systems will further increase demand for high-end display units, which is expected to be a main growth driver over the next few years.

BY VEHICLE

The Passenger Vehicles segment dominated with a 73% market share in 2023 because of the steady consumer emphasis on safety & comfort for personal modes of transportation. As passenger vehicles workforces with advanced safety features to protect drivers and passengers alike, such as night vision systems arbitrate appealing options for consumers. The segment that contributed significantly to market share is due to the rising awareness regarding road safety; manufacturers are including night vision into their offerings as a solution for the high demand for visibility and accident prevention.

The Commercial Vehicles segment is estimated to record the fastest growth during the period from 2024 to 2032. This growth is triggered by the safety demand in commercial transport, which typically represents large vehicles driven in rugged environments and at night. Night vision systems improve the visibility for truck and bus drivers along with other commercial vehicle operators thereby minimizing accidents due to less lighting conditions. Furthermore, the increasing regulatory pressure and the need for more effective safety features in commercial transportation are encouraging fleet operators to adopt novel technologies including night vision systems. Since these vehicles are extensively utilized for long-distance travel the commercial sector will continue to be the most significant growth area in this market due to demand for systems enhancing visibility and reducing fatigue.

REGIONAL ANALYSIS

North America led the Automotive Night Vision System Market share accounting for a market share of 31% in 2023, owing to the technologically advanced automotive industry and high safety regulation standards. General Motors, Ford, and Tesla, which have manufacturing operations in the region, are leaders in-vehicle technologies. Night vision systems that improve driver awareness during nighttime driving are included with Cadillac's Super Cruise feature. Additionally, persistent consumer demand for safety has been combined with rising sales of luxury vehicles provided with advanced driver assistance systems (ADAS), hence further complementing the growth of the market in this region.

Asia Pacific region will witness the fastest CAGR during the years 2024-2032 owing to rapid urbanization coupled with high disposable incomes and a developing automotive market. China, India, and other countries are producing and selling so-called motor vehicles akin to hotcakes propelled by a larger middle class and an increased awareness of safety features. Take the night vision for example, we see Chinese manufacturers, NIO and Xpeng embedding this technology into their EVs to beat global brands on the same view of high-end. As night vision systems help improve a driver's vehicle safety and performance, they are increasingly becoming an integral part of autonomous driving technologies being adopted in the Asia Pacific region. These two factors along with the growing demand for safer vehicles across the globe will propel the market growth in the Asia Pacific region during the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key players

Some of the major players in the Automotive Night Vision System Market are:

Bosch (Night Vision Camera, Driver Assistance System)

Continental AG (Night Vision System, Sensor Technology)

Daimler AG (Thermal Imaging System, Driver Assistance)

Ford Motor Company (Night Vision Assistance, Advanced Driver Assistance System)

General Motors (GM) (Night Vision System, Safety Technologies)

Valeo (Thermal Imaging Camera, Night Vision Sensor)

Aisin Seiki Co., Ltd. (Night Vision System, Advanced Lighting Solutions)

Delphi Technologies (Night Vision Systems, Automotive Sensor Solutions)

Hella (Night Vision System, Radar Sensors)

Magna International (Thermal Imaging System, Active Safety Systems)

Nissan Motor Corporation (Night Vision Assistance, Advanced Safety Features)

Toyota Motor Corporation (Night Vision System, Driver Assistance Technologies)

Autoliv (Night Vision System, Advanced Safety Solutions)

ZF Friedrichshafen AG (Night Vision System, Driver Assistance Technology)

Infineon Technologies (Automotive Sensors, Vision Processing Solutions)

Carmudi (Thermal Night Vision Systems, Driver Monitoring Systems)

Samsung Electronics (Automotive Cameras, Night Vision Technology)

Visteon Corporation (Night Vision System, Vehicle Cockpit Electronics)

Pioneer Corporation (Night Vision Display, Automotive Camera Systems)

Stoneridge, Inc. (Night Vision Assistance, Advanced Driver Systems)

Some of the Raw Material Suppliers for Automotive Night Vision System Companies:

3M

DuPont

BASF

Honeywell

SABIC

Covestro

Eastman Chemical Company

Huntsman Corporation

Teijin Limited

Toray Industries

RECENT TRENDS

In September 2024, Veoneer is set to launch the world's first thermal camera designed specifically for Level 4 autonomous vehicles. This groundbreaking technology will utilize multiple high-resolution thermal cameras to improve safety in the mobility-as-a-service sector, marking a significant advancement in autonomous driving systems.

In October 2024, Israeli startup AdaSky is developing an infrared camera to improve night vision for self-driving cars, enhancing navigation in challenging conditions.

In January 2024, InfiRay showcased its Auto AI Night Vision System, the InfiRay NV2, at CES 2024. The NV2 features an infrared thermal imaging unit that captures clear images in total darkness and effectively identifies glare, reflections, and haze in harsh conditions like rain and dust, enhancing night driving safety.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 3.65 Billion |

| Market Size by 2032 | USD 10.56 Billion |

| CAGR | CAGR of 12.58% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Far Infrared (FIR), Near Infrared (NIR)) • By Component (Night Vision Camera, Controlling Unit, Display Unit, Sensor, Others) • By Vehicle (Passenger Vehicles, Commercial Vehicles) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Bosch, Continental AG, Daimler AG, Ford Motor Company, General Motors (GM), Valeo, Aisin Seiki Co., Ltd., Delphi Technologies, Hella, Magna International, Nissan Motor Corporation, Toyota Motor Corporation, Autoliv, ZF Friedrichshafen AG, Infineon Technologies, Carmudi, Samsung Electronics, Visteon Corporation, Pioneer Corporation, Stoneridge, Inc |

| Key Drivers | • Driving the Future Night Vision Systems Revolutionizing Safety in Autonomous Vehicle Technology • Enhancing Road Safety Night Vision Systems Driving Consumer Demand and Reducing Traffic Accidents |

| Restraints | • Overcoming Technological Challenges in Night Vision Systems Integration for Enhanced Automotive Safety |

Ans: The Automotive Night Vision System Market is expected to grow at a CAGR of 12.58% during 2024-2032.

Ans: Automotive Night Vision System Market size was USD 3.65 billion in 2023 and is expected to Reach USD 10.56 billion by 2032.

Ans: The major growth factor in the Automotive Night Vision System Market is the increasing demand for advanced safety features, driven by rising road safety concerns and the push for autonomous driving technologies.

Ans: The Far Infrared (FIR) segment dominated the Automotive Night Vision System Market in 2023.

Ans: North America dominated the Automotive Night Vision System Market in 2023.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Automotive Night Vision System Sales Volume, by Region, (2020-2023)

5.2 Automotive Night Vision System Technology Advancements, by Region, (2020- 2023)

5.3 Automotive Night Vision System Installation and Retrofit Rates, by Region

5.4 Automotive Night Vision System User Experience Metrics, by Region (2023)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Automotive Night Vision System Market Segmentation, by Technology

7.1 Chapter Overview

7.2 Far Infrared (FIR)

7.2.1 Far Infrared (FIR) Market Trends Analysis (2020-2032)

7.2.2 Far Infrared (FIR) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Near Infrared (NIR)

7.3.1 Near Infrared (NIR) Market Trends Analysis (2020-2032)

7.3.2 Near Infrared (NIR) Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Automotive Night Vision System Market Segmentation, by Component

8.1 Chapter Overview

8.2 Night Vision Camera

8.2.1 Night Vision Camera Market Trends Analysis (2020-2032)

8.2.2 Night Vision Camera Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Controlling Unit

8.3.1 Controlling Unit Market Trends Analysis (2020-2032)

8.3.2 Controlling Unit Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Display Unit

8.4.1 Display Unit Market Trends Analysis (2020-2032)

8.4.2 Display Unit Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Sensor

8.5.1 Sensor Unit Market Trends Analysis (2020-2032)

8.5.2 Sensor Unit Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Others

8.6.1 Others Unit Market Trends Analysis (2020-2032)

8.6.2 Others Unit Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Automotive Night Vision System Market Segmentation, by Vehicle

9.1 Chapter Overview

9.2 Passenger Vehicles

9.2.1 Passenger Vehicles Market Trends Analysis (2020-2032)

9.2.2 Passenger Vehicles Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Commercial Vehicles

9.3.1 Commercial Vehicles Market Trends Analysis (2020-2032)

9.3.2 Commercial Vehicles Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Automotive Night Vision System Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.2.4 North America Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.2.5 North America Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.2.6.2 USA Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.2.6.3 USA Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.2.7.2 Canada Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.2.7.3 Canada Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.2.8.2 Mexico Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.2.8.3 Mexico Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Automotive Night Vision System Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.1.6.2 Poland Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.1.6.3 Poland Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.1.7.2 Romania Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.1.7.3 Romania Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Automotive Night Vision System Market Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Automotive Night Vision System Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.4 Western Europe Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.5 Western Europe Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.6.2 Germany Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.6.3 Germany Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.7.2 France Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.7.3 France Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.8.2 UK Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.8.3 UK Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.9.2 Italy Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.9.3 Italy Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.10.2 Spain Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.10.3 Spain Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.13.2 Austria Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.13.3 Austria Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Power Management Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Automotive Night Vision System Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia Pacific Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.4 Asia Pacific Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.5 Asia Pacific Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.6.2 China Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.6.3 China Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.7.2 India Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.7.3 India Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.8.2 Japan Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.8.3 Japan Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.9.2 South Korea Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.9.3 South Korea Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.10.2 Vietnam Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.10.3 Vietnam Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.11.2 Singapore Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.11.3 Singapore Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.12.2 Australia Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.12.3 Australia Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia Pacific Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia Pacific Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Automotive Night Vision System Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.1.4 Middle East Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.1.5 Middle East Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.1.6.2 UAE Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.1.6.3 UAE Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Automotive Night Vision System Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.2.4 Africa Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.2.5 Africa Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Automotive Night Vision System Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.6.4 Latin America Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.6.5 Latin America Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.6.6.2 Brazil Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.6.6.3 Brazil Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.6.7.2 Argentina Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.6.7.3 Argentina Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.6.8.2 Colombia Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.6.8.3 Colombia Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Automotive Night Vision System Market Estimates and Forecasts, by Technology (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Automotive Night Vision System Market Estimates and Forecasts, by Component (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Automotive Night Vision System Market Estimates and Forecasts, by Vehicle (2020-2032) (USD Billion)

11. Company Profiles

11.1 Bosch

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

110.1.4 SWOT Analysis

11.2 Continental AG

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

11.3 Daimler AG

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

11.4 Ford Motor Company

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

11.5 General Motors (GM)

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

11.6 Valeo

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

11.7 Aisin Seiki Co., Ltd.

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

11.8 Delphi Technologies

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

11.9 Hella

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11.10 Magna International

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Technology

Far Infrared (FIR)

Near Infrared (NIR)

By Component

Night Vision Camera

Controlling Unit

Display Unit

Sensor

Others

By Vehicle

Passenger Vehicles

Commercial Vehicles

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Used Car Market Size was valued at USD 1.67 trillion in 2023 and is expected to reach USD 2.70 trillion by 2031 and grow at a CAGR of 6.2% over the forecast period 2024-2031.

The Automotive Operating System Market Size was valued at USD 8.88 Billion in 2023 and is expected to reach USD 21.09 Billion by 2032 and grow at a CAGR of 10.1% over the forecast period 2024-2032.

Electric Commercial Vehicle Market Size was valued at USD 71.51 billion in 2023 and is expected to reach USD 521.92 billion by 2032 and grow at a CAGR of 24.74% over the forecast period 2024-2032.

The Mounted Bearing Market size was valued at USD 1.49 Billion in 2023 and is expected to reach USD 2.38 Billion by 2032, with growing at a CAGR of 5.44% over the forecast period 2024-2032.

The Motor Grader Market size was valued at USD 3.71 Bn in 2023 and is expected to reach USD 5.69 Bn by 2031, with a CAGR of 5.5% over the forecast period of 2024-2031.

The Automotive Fender Market Size was USD 13.01 billion in 2023 and is expected to reach USD 28.07 Bn by 2032, growing at a CAGR of 8.94% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd