Get More Information on Automotive Gear Market - Request Sample Report

The Automotive Gear Market Size is projected to reach USD 52.26 billion by 2032 and grow at an CAGR of 3.2% over 2024-2032. The market was valued at USD 40.05 billion in 2023.

Increased vehicle production, especially conventional and electric vehicles, have been the leading drivers of demand for automotive gears. But this is more than offset by increasing consumer preference for better driving experiences. Automatic transmissions have turned up in increasing numbers, which have trended upward for several years and saw adoption spiking by about 10-12% a year, especially in North America and Europe. Advancements in gear technology, such as dual-clutch transmissions (DCT) and continuously variable transmissions (CVT), to achieve maximum fuel efficiency with better ride quality are enhancing the automotive gear market. Among other contributors are electric vehicles, with estimated growth of around 20-25% gears used in electric powertrains in the next few years, encouraged by growing adoption of EVs. Apart from this, lightweight material gears, such as aluminum and composite gears, have also gathered more demand due to the fact that they help the automobile companies meet tight emission and fuel efficiency standards. Lightweight gears cut vehicle weights up to 15% above, hence increasing overall fuel efficiency. High-performance vehicle consumer demand increased and now forces the need for advanced gear systems with greater control and power delivery.

Automotive gear is growing rapidly mainly due to the increased development of electric vehicles, lightweight materials, and further demands for additional fuel efficiency. The helical gears are gaining popularity since they are very effective at reducing noise, a major quality needed in the electric vehicles. Indeed, the helical gears used in electric vehicle transmissions witnessed a growth of nearly 35% over the last five years because it reduces noise during operations. Another trend is toward lighter aluminum gears for adequate emission control and efficiency in driving. This led to a 28% rise in lightweight gear components' requirement for the last two years.

Drivers:

The fast-growing growth of electric vehicles, and energy efficiency interests from the automotive industry.

Today, the car manufacturers are subjected to increased regulatory pressure that calls for reduction in greenhouse gas emissions. The emphasis put forward by car manufacturers on creating more fuel-efficient vehicles improves advanced and efficient gear demand. Helical gears are very efficient and also contribute to a smoother, quieter operation, making them increasingly prevalent in EVs. Noise reduction is essential for a quieter, more refined driving experience. Another major push is toward lightweight materials: makers are turning to aluminium and other light alloys to develop gears that help reduce a vehicle's weight overall, thus contributing to enhanced fuel efficiency.

Increasing use of ADAS and autonomous vehicles requires higher-precision and durability gears, which also propels manufacturers to use more advanced gear systems such as planetary gears. The increased demands for off-road and AWD vehicles have led to wider usage of bevel gears due to the increased demand by consumers for robust vehicles that can tackle off-road conditions. The growing popularity of automated and electric driving technologies requires better gear power transmission systems.

Restrains:

The complexity of gear systems in modern vehicles has also risen, especially considering the growing popularity of EVs and advanced driver-assistance systems (ADAS).

The advancing nature of automotive technology calls upon the manufacturers to design increasingly intricate gear systems to guarantee vehicle performance, efficiency, and safety. For instance, most electric vehicles come with multi-speed transmissions and higher levels of advanced gearing solutions that are unlike what internal combustion engines would produce. Therefore, it presents a much more advanced engineering precision and innovation in gear design. Most of the EVs would feature components such as regenerative braking and integrated electric motors, which give a unique kind of gearing arrangement.

These technologies require advanced gear systems that can proficiently handle torque and power delivery well, complicating the design. A push toward greater efficiency and better performance necessitates the requirement for manufacturers to ensure gear systems can carry greater stress at various conditions to make this possible. This would potentially lead to more time-consuming testing and development stages to market, possibly extending the time-to-market. Modern gear systems are very complex

By Material

Raw materials used in the manufacture of gears are the main factors driving the car gear market. The market share for metallic gears constitutes around 70%, whereas plastic gears occupy around 30 percent. Metallic gears, which comprise mainly carbon steel, stainless steel, and aluminum alloys, are popular due to their outstanding strength, toughness, and load-bearing capabilities, and thus, more preferred for high-stress applications like, for example, transmission and differential units. On the other hand, plastic gears have been widely used in specific applications due to their light and cost-effective nature. Having been made from various types of materials, including acetal, nylon, and polycarbonate, plastic gears are good for applications that do not carry loads, especially electronic components wherein noise generation cannot be tolerated. The rising demand for electric vehicles also requires more lightweight materials in gear systems and forces the manufacturers to find newer and more innovative solutions to optimize performance while minimizing weight.

By Product Type

The automotive gear market has several varieties of products, though the highest is 35% share, including planetary gears. The bevel gear can be put at 25%, and helical gears at 20%, and both share 10% with non-metallic gears and other kinds. Planetary gears are in high demand for being compact and high torque. This makes them crucial in the automatics and hybrid transmissions. All-wheel systems and differentials have given bevel gears a call, which supports the increasingly popular SUVs and off-road vehicles, through power transmission between shafts in several angles. Helical gears offer smoothness and efficiency while wearing or degrading less as compared to other gear configurations; they are gaining increased importance in conventional as well as electric vehicles to reduce noise and vibration. The last is the non-metallic gear segment, including composite and polymer gears. This latter segment meets specific applications with emphasis on weight reduction and resistance to corrosion, which is especially needed in electric vehicle applications.

By Vehicle Type

Segmentation of the automotive gear market is done mainly between passenger vehicles that comprise 65% of the total market and commercial vehicles, which account for 35%. Demand for efficient and reliable gear systems has been a major growth driver in the passenger vehicle market. In that quest for better efficiency and lower emissions, helical and planetary gears become the norm in most new designs, especially for electric and hybrids. Quite on the other hand, trucks, buses, and vans, on the other hand, are required to have highly strengthened high-performance gear sets, tolerant of extreme applications. As the logistics and transportation business is growing, demand for tough gearing solutions that can carry heavy loads efficiently increases.

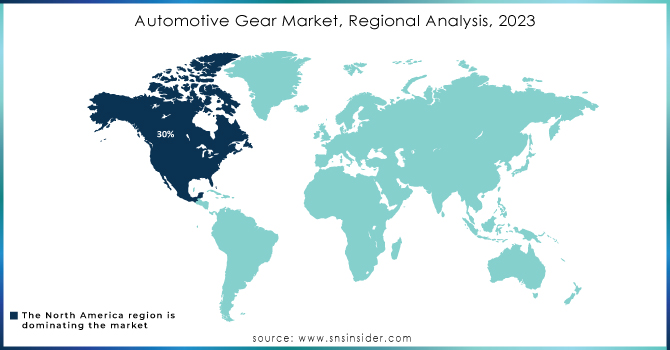

North America dominated the market at about 30% of the overall market share. Here, the dominance of this sector is seen primarily due to the presence of major automotive firms and the significant value granted towards technology. Being the largest automotive market, the United States also serves as a prime hub for innovations related to electric and autonomous vehicles. Increasingly, such vehicles are now bearing high-end gear technologies. Aggressive rules on fuel efficiency and exhaust emissions are driving the high-performance gear system into the market. An elevated logistics and transportation sector is also driving the demand for both passenger and commercial vehicles, which in turn is going to open up this North American automotive gear market. Europe is yet another dominant player in the automotive gear market, with a share of almost 25% in the global market.

The region boasts excellent auto manufacturing and strong research and development activities. For ages, Europe was always in the lead in terms of automotive innovation and remains so till date, in cooperation with Germany, France, and the UK, that are continually developing more advanced transmission system designs and materials which are lighter than the conventional ones. Steps taken in the direction of increasingly advanced electric vehicles and sustainability propitiously motivate the rise in demand for efficient gear systems.

Recent Developments:

ZF Friedrichshafen AG The company, ZF Friedrichshafen AG, has shown significant advancements in developing electric drive systems that combine high-class gear technologies for EVs. In 2023, the company introduced a new modular drive architecture that integrates innovative gear designs to increase efficiency and eliminate noise generation.

BorgWarner Inc. BorgWarner Inc. foresees significant increases in the power shares in the hybrid and electric vehicle market when it unveiled its latest eGearDrive systems. The systems utilize new gear designs that maximize power density and efficiency and allow for a smaller footprint in order to accommodate the compact and lightweight solutions for electric vehicles.

Need Any Customization Research On Automotive Gear Market - Inquiry Now

Some of the major key players are:

ZF Friedrichshafen AG: (Electric Drive Systems, Modular Drive Architecture)

BorgWarner Inc.: (eGearDrive Systems, Turbochargers)

GKN Automotive: (Lightweight Gears, All-Wheel Drive Systems)

Aisin Seiki Co., Ltd.: (Planetary Gear Systems, Automatic Transmissions)

Dana Incorporated: (e-Drive Systems, Driveline Products)

Mahindra & Mahindra: (Electric Vehicle Gears, Manual Transmissions)

Toyota Industries Corporation: (Gear Reduction Units, Automated Transmissions)

Continental AG: (Dual Clutch Transmissions, Electronic Control Units)

Parker Hannifin Corporation: (Hydraulic Gear Pumps, Gear Motors)

Timken Company: (Bearings, Gear Drives)

Rockwell Automation: (Gearboxes, Industrial Gear Motors)

American Axle & Manufacturing, Inc.: (Driveline Systems, Differentials)

Brembo S.p.A.: (Gear-Based Brake Systems, Performance Brake Kits)

Getrag (Magna International): (Manual Transmission Systems, Hybrid Transmission Systems)

Schaeffler AG: (Gear Trains, Clutch Systems)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 52.26 Billion |

| Market Size by 2032 | USD 40.05 Billion |

| CAGR | CAGR of 3.2% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material (Metallic, Plastic) • By Product Type (Planetary, Bevel, Helical, Non-Metallic, Other) • By Vehicle Type (Passenger vehicle, Commercial Vehicle) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ZF Friedrichshafen AG,BorgWarner Inc, Aisin Seiki Co., Ltd., Mahindra & Mahindra, Timken Company, Rockwell Automation, Brembo S.p.A., Getrag and others |

| Key Drivers | • The fast-growing growth of electric vehicles, and energy efficiency interests from the automotive industry. |

| RESTRAINTS | • The complexity of gear systems in modern vehicles has also risen, especially considering the growing popularity of EVs and advanced driver-assistance systems (ADAS). |

Answer: The rise in electric vehicle adoption and the need for lightweight materials to meet emission standards significantly contribute to the demand for automotive gears.

Answer: Advancements in gear technology, including dual-clutch transmissions (DCT) and continuously variable transmissions (CVT), have improved fuel efficiency and ride quality, leading to greater adoption in vehicles.

Answer: The Automotive Gear Market size is projected to reach USD 52.26 billion by 2032 and grow at an CAGR of 3.2% over 2024-2032.

Answer: Manufacturers face challenges related to the increasing complexity of gear systems due to the rise of electric vehicles (EVs) and advanced driver-assistance systems (ADAS).

Answer: North America holds about 30% of the market share due to the presence of major automotive manufacturers and a focus on technology and innovation in electric and autonomous vehicles.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Vehicle Production and Sales Volumes, 2020-2032, by Region

5.2 Emission Standards Compliance, by Region

5.3 Vehicle Service Type Adoption, by Region

5.4 Consumer Preferences, by Region

5.5 Aftermarket Trends (Data on vehicle maintenance, parts, and services)

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Automotive Gear Market Segmentation, By Material Type

7.1 Chapter Overview

7.2 Metallic

7.2.1 Metallic Market Trends Analysis (2020-2032)

7.2.2 Metallic Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.3 Plastic

7.2.3.1 Plastic Market Trends Analysis (2020-2032)

7.2.3.2 Plastic Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Automotive Gear Market Segmentation, by Product Type

8.1 Chapter Overview

8.2 Planetary

8.2.1 Planetary Market Trends Analysis (2020-2032)

8.2.2 Planetary Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Bevel

8.3.1 Bevel Market Trends Analysis (2020-2032)

8.3.2 Bevel Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Helical

8.4.1 Helical Market Trends Analysis (2020-2032)

8.4.2 Helical Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Non-Metallic

8.5.1 Non-Metallic Market Trends Analysis (2020-2032)

8.5.2 Non-Metallic Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Others

8.5.1 Others Market Trends Analysis (2020-2032)

8.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Automotive Gear Market Segmentation, by Vehicle Type

9.1 Chapter Overview

9.2 Passenger Vehicle

9.2.1 Passenger Vehicle Market Trends Analysis (2020-2032)

9.2.2 Passenger Vehicle Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Commercial Vehicle

9.3.1 Commercial Vehicle Market Trends Analysis (2020-2032)

9.3.2 Commercial Vehicle Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Automotive Gear Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.2.4 North America Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.2.5 North America Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.2.6.2 USA Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.2.6.3 USA Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.2.7.2 Canada Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.2.7.3 Canada Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.2.8.2 Mexico Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.2.8.3 Mexico Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Automotive Gear Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.1.6.2 Poland Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.1.6.3 Poland Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.1.7.2 Romania Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.1.7.3 Romania Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Automotive Gear Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.4 Western Europe Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.5 Western Europe Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.6.2 Germany Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.6.3 Germany Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.7.2 France Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.7.3 France Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.8.2 UK Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.8.3 UK Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.9.2 Italy Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.9.3 Italy Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.10.2 Spain Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.10.3 Spain Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.13.2 Austria Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.13.3 Austria Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Automotive Gear Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia Pacific Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.4 Asia Pacific Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.5 Asia Pacific Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.6.2 China Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.6.3 China Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.7.2 India Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.7.3 India Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.8.2 Japan Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.8.3 Japan Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.9.2 South Korea Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.9.3 South Korea Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.10.2 Vietnam Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.10.3 Vietnam Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.11.2 Singapore Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.11.3 Singapore Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.12.2 Australia Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.12.3 Australia Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia Pacific Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia Pacific Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Automotive Gear Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.1.4 Middle East Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.1.5 Middle East Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.1.6.2 UAE Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.1.6.3 UAE Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Automotive Gear Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.2.4 Africa Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.2.5 Africa Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Automotive Gear Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.6.4 Latin America Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.6.5 Latin America Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.6.6.2 Brazil Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.6.6.3 Brazil Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.6.7.2 Argentina Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.6.7.3 Argentina Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.6.8.2 Colombia Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.6.8.3 Colombia Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Automotive Gear Market Estimates and Forecasts, By Material Type (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Automotive Gear Market Estimates and Forecasts, by Product Type (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Automotive Gear Market Estimates and Forecasts, by Vehicle Type (2020-2032) (USD Billion)

11. Company Profiles

11.1 ZF Friedrichshafen AG

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

111.1.4 SWOT Analysis

11.2 BorgWarner Inc.

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 GKN Automotive

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Aisin Seiki Co., Ltd.

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Dana Incorporated

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 Mahindra & Mahindra

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Toyota Industries Corporation

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Continental AG

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Parker Hannifin Corporation

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

12. Competitive Landscape

12.1 Competitive Benchmarking

12.2 Market Share Analysis

12.3 Recent Developments

12.3.1 Industry News

12.3.2 Company News

12.3.3 Mergers & Acquisitions

13. Use Case and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Material

Metallic

Plastic

By Product Type

Planetary

Bevel

Helical

Non-Metallic

other

By Vehicle Type

Passenger vehicle

Commercial vehicle

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Automotive Exterior Smart Lighting Market Size was valued at USD 1.13 billion in 2023 and is expected to reach USD 1.78 billion by 2032 and grow at a CAGR of 5.15% over the forecast period 2024-2032.

The Automotive Sunroof Market Size was valued at USD 7.45 billion in 2023 and is expected to reach USD 19.36 billion by 2032 and grow at a CAGR of 11.2% over the forecast period 2024-2032.

The In-Vehicle Infotainment Market Size was valued at $17.1 billion in 2023 and will reach $39.9 billion by 2031, and grow at a CAGR of 11.2% by 2024-2031

The Automotive Intelligent Door System Market Size was $2.68 billion in 2023 and will reach USD 5.74 billion by 2031 and grow at a CAGR of 10% by 2024-2031

The Tubeless Tire Market size is expected to reach USD 282.90 Bn by 2031, the market was valued at USD 175.5 Bn in 2023 and will grow at a CAGR of 6.15% over the forecast period of 2024-2031.

The Torque Vectoring Market Size was USD 10.5 Billion in 2023. It is expected to grow to USD 28.5 Billion by 2032 and grow at a CAGR of 11.7% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd