Get more information on ATM Market - Request Sample Report

The ATM Market was valued at USD 23.86 Billion in 2023 and is expected to reach USD 34.23 Billion by 2032, growing at a CAGR of 4.11% over the forecast period 2024-2032.

A big driver of growth is the growing worldwide demand for cash access and self-service banking solutions, especially in underbanked areas. The growing idea of financial inclusion assumes ATMs as a critical part of this provision of accessibility to banking services in a cheap and fast manner. AMR Group stated that rising demand for higher technology features, such as biometric authentication, currency recycling, and availability of multi-functional services have driven the adoption of the smart ATM. This innovation strengthens security, saves money on operational expenses for banks, and expands the range of services, making ATMs more appealing to financial institutions and users alike. More than 10,000 ATMs around the world now include biometric functionality as of 2023, including 2,000 ATMs in India to boost financial inclusion. By 2022, the global installed base for cash recycling ATMs had risen to 1.4 million, up from 1 million in 2021, with 25% of U.S. ATMs now outfitted with this capability. More than 50,000 ATMs now provide multi-functional services including bill payments, mobile top-ups, and check deposits instead of a simple cash withdrawal.

The increasing automation of the banking sector is another reason. ATMs provide a great way to handle at least routine transactions with little human intervention, which is a big cost saver for banks, which are under constant pressure to increase the operational efficiency of their branches. This increase further augments the viability of ATMs that can open and allow people to take out digital currencies and digital accounts with increased digital banking and e-wallet usage. Furthermore, there is a rapid growth of the ATM networks in emerging markets, in particular, Asia-Pacific and Africa the banking penetration is rising along with a growing middle-class population. All of the aforementioned factors augur well for the growth of the ATM market in the coming years.

It is estimated that more than 3 million ATMs will be rolled out globally, having undergone considerable automation to minimize human involvement and operational costs by 2024. For instance, more than 80% of ATMs in the U.S. sort cash in addition to recycling and facilitating digital transactions. Africa's ATM network is expanding by 10% each year as institutions work to enhance financial accessibility in unbanked areas. Aside from this, there are 40,000 cryptocurrency ATMs in the world, 35,000 of which are in the U.S., indicating a growing demand for cash out in the form of digital currencies.

KEY DRIVERS:

The expanding need for contactless and secure payment options is a major factor contributing to growth in the ATM market. With the growing apprehensions surrounding the reliability and security of financial transactions both on consumer and enterprise segments alike ATMs are increasingly being upgraded with contactless payment functionalities. This includes access to cash withdrawals via mobile or tap-and-go card functionality. COVID-19 created serious worries around close interactions, requiring urgent demand for touch-free solutions. As a result, ATM manufacturers and banks are responding by upgrading old machines for contactless enablement which allows a much smoother and safer way to withdraw money. The rise of features in ATMs like Near Field Communication (NFC) or QR code readers is expected to rise, it will provide an easy, faster, and safer way for users to get their cash without inserting any physical card into the ATM. Globally, 50% of ATMs will be ready for contactless by 2024 with 40,000 ATMs in the U.S. being upgraded for tap-and-go card functionality. In 2024 alone, expect 35% more ATMs to integrate QR code transactions. On top of that, 200,000 cardless ATMs are expected to be in use throughout the globe by using a mobile app or other device to access cash machines without needing to use a physical card.

The growth in demand for integrated digital banking solutions is the other key driver. As digital banking has proliferated, banks are increasingly recasting the ATM as a form of omnichannel banking strategy. Smart ATMs aim to continue addressing the space between physical banking and digital banking; enabling customers to make types of transactions like transfers between banks, pay bills, and make checks. These machines are evolving into an extension of digital platforms, providing new digital services with advanced features, thus improving customer experience. This has led the banks to deploy these advanced ATMs as a part of their digital transformation strategies where they meet the customers online and offline. Such a trend is spurring investments and innovations in the ATM market paving the way for its omnipresence in the banking infrastructure. More than 300,000 smart ATMs worldwide are projected to be available by 2024, providing bill payment and transfer services. 55% of banking customers in U.S. prefer mobile apps to manage their accounts and billions of people around the globe, 2 billion to be precise uses mobile banking. On top of that, 40% of ATMs are linked with mobile apps, features such as cardless ATM withdrawals, and mobile check deposits.

RESTRAIN:

Growing threats regarding fraud and security are one of the major challenges faced in the ATM market. With the increased integration of ATMs into digital banking and new technology, they are also increasingly exposed to cyberattacks and deception. Criminals employ methods such as skimming, card trapping, and malware to obtain customer data and money. This threat can only supplement the need for ATM financial institutions; regular upgrades and the practice of consumers watching ensuring ATM security itself. Another difficulty comes from the regional safety regulation that differs from one country to another. Given that financial institutions have to deal with an ever-evolving regulatory landscape, spanning AML laws and data privacy rules, they have to do a delicate balancing act to stay in compliance with the letter of the law while providing customers and regulators with seamless access to financial services. The mix of country and domain ATM requirements can create challenges for ATM rollout and machine management. Such differences in legal systems can also delay the advancement of good markets and lead to the need to have extra resources to battle for compliance management something that is seen predominantly in developing markets.

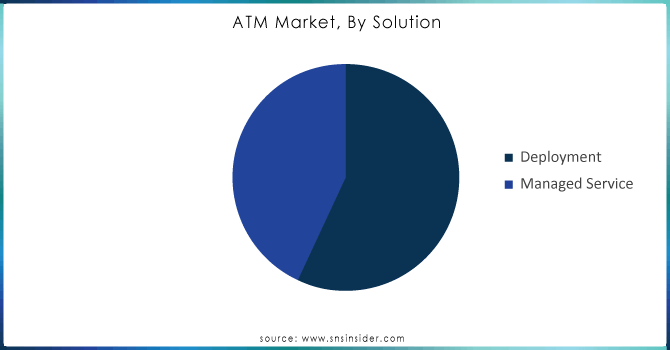

BY SOLUTION

The deployment segment held the largest ATM market with a share of 52.7% in 2023, and it is evaluated to grow at the highest CAGR from 2024 to 2032 owing to, one is the growing ATM networks in emerging markets. Geographically, demand for more ATMs to reach un-banked populations scales as financial inclusion initiatives grow across Asia-Pacific, Latin America, and Africa. Investment from banks and financial institutions is expanding access to convenient and accessible banking services through them, in turn, fueling demand for the new ATM deployments. In addition, the latest digital transformation in the banking sector is instigating demand for smart ATMs which offer ease over simple cash withdrawal functionalities. Smart ATMs support multi-function services (cash recycling, bill, and coin deposit, bill payments, cash deposits, and withdrawal, passbook printing) and various biometric authentication, which increase the number of times advanced machines are deployed for the day. Due to the role these innovative ATMs play in forming some of the core aspects for all financial institutions that are especially crucial in a competitive environment such as increasing customer experience and minimizing operational costs. Therefore, the segment of deployment will sustain its steady growth and will increase at a significant pace in the upcoming years.

BY TYPE

The Conventional/Bank ATM segment captured a market share of 54.7% in 2023 and this can be attributed to the widespread presence that these ATMs have along with their importance in traditional banking services. Such ATMs have been historically known as a trusted means for carrying credit/debit-related operations that solely include cash withdrawals, balance checks, fund transfers, etc. Their persona and omnipresence in urban and rural regions combined with the familiarity and reliability of paper as a medium explains why paper is still widely used by most users, especially in countries where digital banking is yet to mature. These ATMs are still kept alive by financial institutions, often serving a significant customer base, particularly older demographics and those with a lower tendency to embrace digital banking solutions.

Smart ATMs are expected to record the highest CAGR between 2024 and 2032, due to the growing technical demand for advanced features and multi-functional capabilities. They include smarter services such as cash recycling, biometric authentication, integration with mobile and online banking platforms, etc. They serve growing trends and tech-savvy consumers, while also aligning with banks' digital transformation strategies, a seamless merge of the physical and digital bank. Global demand for Smart ATMs is anticipated to increase due to their growing usage and the need among financial institutions to diminish branch operations and offer better experiences to customers, particularly in developed economies and cities worldwide.

Do you need any custom research/data on ATM Market - Enquiry Now

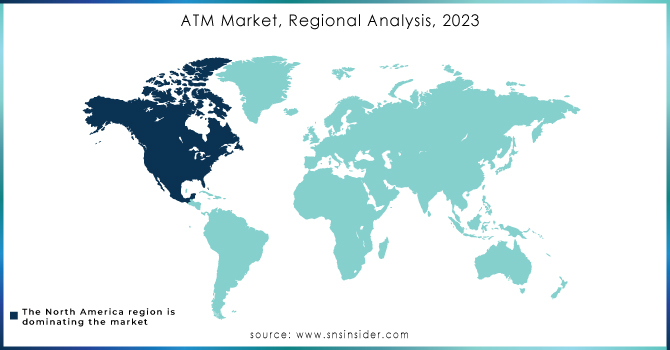

REGIONAL ANALYSIS

North America holds the largest ATM market share of 30.7% in 2023, which is due to its highly developed financial ecosystem combined with developed countries, and high adoption of advanced banking technologies. The area is home to one of the highest per capita ATM densities in the world in part enabled by a stable regulatory climate and strong consumer banking behavior. Banks across the US and Canada (Bank of America, RBC (Royal Bank of Canada)) have been focused on increasing customer convenience with value added features in ATMs. Cardless ATM withdrawal methods through a phone app or NFC technology, are already a reality, providing the user with an extra layer of security and access. North America, the developed nations will inspire more development in the vertical since it is the repository of research and development on financial technologies and would witness the introduction of features such as real time account updates and sophisticated measures to prevent fraudulent access in the ATM column. Such trends only solidify the region's position as the global leader in ATM.

Asia-Pacific is anticipated to register the highest CAGR during the forecast period, owing to rapid economic growth, urbanization, and the growing initiatives for financial inclusion. Countries like India, China, and Indonesia are heavily investing in increasing ATM coverage, thanks to well-structured government backing and financial institutions. For example, India has encouraged ATM installations in rural areas through the PMJDY program, thus bringing financial services to millions of unbanked people. China has already seen the likes of regular and enhanced Smart ATMs from banks such as ICBC and China Construction Bank, focusing on multifunctional capabilities like cash recycling; opening accounts, and biometric-enabled capabilities. Additionally, trends such as the region's increasing adoption of mobile payments and QR code-based cash withdrawals are changing the way consumers use ATMs, well in line with Asia-Pacific's drive towards a cash-lite digital economy. Combined, these factors make this region an important source of innovation and growth for the ATM market.

Key players

Some of the major players in the ATM Market are:

Diebold Nixdorf (Opteva Series, ActivEdge Card Reader)

NCR Corporation (SelfServ ATMs, Interactive Teller Machines)

Triton Systems of Delaware LLC (RL2000, FT5000)

Hitachi Channel Solutions Corp (Cash Recycling ATMs, Card Readers)

Hyosung TNS Inc. (Halo II, 2700 CE)

GRG Banking Equipment Co. Ltd. (H68N Series, P2800L)

Fujitsu Frontech Ltd. (Series 8000 ATMs, PalmSecure Vein Authentication)

Euronet Worldwide Inc. (REN Self-Service ATM, iCash ATMs)

OKI Electric Industry Co. Ltd. (ATM-Recycler G7, ATM-Recycler G8)

Glory Ltd. (RG Series ATMs, TellerInfinity)

Hantle USA (1700W, T4000)

Genmega Inc. (G2500, GT3000)

Nautilus Hyosung America Inc. (MX8800, MX5600)

Wincor Nixdorf AG (ProCash Series, Cineo Series)

Sigma ATM (Monimax 5000CE, Monimax 5100T)

Shenzhen Zhongji Technology Co. Ltd. (ZJ6000, ZJ8000)

KingTeller Technology Co. Ltd. (KT ATM-7000, KT ATM-8000)

Hitachi-Omron Terminal Solutions Corp. (HT-2845-V, HT-2845-S)

Keba AG (KePlus D10, KePlus D6)

Euronet India (Euronet ATMs, REN ATMs)

Some of the Raw Material Suppliers for ATM companies:

ATM Polymers

Shenzhen Mufeng Paper Limited

ATM Trafilerie

KUNSHANG INTERNATIONAL CO., LTD.

Hebei Luobin Trading Co., Ltd.

Advance Traffic Markings

Sailing Paper

Asia Manufacturer

ATM Recyclingsystems

Global Sources

RECENT TRENDS

In December 2024, Diebold Nixdorf becomes the first to deploy Microsoft® Windows 11® on live ATMs, enhancing security and user experience in banking technology.

In October 2024, NCR Corporation introduced advanced ATMs equipped with facial recognition technology and self-service capabilities, enhancing security and streamlining user transactions.

In September, Hitachi introduces India's first Android-powered ATM, enabling seamless UPI-based withdrawals and deposits, revolutionizing digital banking services.

| Report Attributes | Details |

| Market Size in 2023 | USD 23.86 Billion |

| Market Size by 2032 | USD 34.23 Billion |

| CAGR | CAGR of 4.11% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2022-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Deployment, Managed Service) • By Type (Conventional/Bank ATMs, Brown ATMs, White ATMs, Cash Dispenser ATM, Smart ATMs) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Diebold Nixdorf, NCR Corporation, Triton Systems of Delaware LLC, Hitachi Channel Solutions Corp, Hyosung TNS Inc., GRG Banking Equipment Co. Ltd., Fujitsu Frontech Ltd., Euronet Worldwide Inc., OKI Electric Industry Co. Ltd., Glory Ltd., Hantle USA, Genmega Inc., Nautilus Hyosung America Inc., Wincor Nixdorf AG, Sigma ATM, Shenzhen Zhongji Technology Co. Ltd., KingTeller Technology Co. Ltd., Hitachi-Omron Terminal Solutions Corp. |

| Key Drivers | • Surge in Contactless ATM Adoption and Mobile Integration Revolutionizing the Future of Banking Services • Digital Banking Revolution Drives Growth in Smart ATMs and Enhances Customer Experience Globally |

| Market Challenges | • Rising Cybersecurity Threats and Regulatory Challenges Hampering Growth of the ATM Market Globally |

Ans: North America dominated the ATM Market in 2023.

Ans: The Deployment segment dominated the Industrial battery market in 2023.

Ans: The major growth factor of the ATM market is the increasing demand for advanced, multi-functional ATMs offering enhanced services like cash recycling, biometric authentication, and digital banking integration.

Ans: ATM Market size was USD 23.86 Billion in 2023 and is expected to Reach USD 34.23 Billion by 2032.

Ans: The ATM Market is expected to grow at a CAGR of 4.11% during 2024-2032.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 ATM Utilization Rate (2023)

5.2 ATM Cash Withdrawal and Deposit Ratio (2023)

5.3 ATM Downtime and Service Availability

5.4 ATM Security Incident Rates

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. ATM Market Segmentation, By Solution

7.1 Chapter Overview

7.2 Deployment

7.2.1 Deployment Market Trends Analysis (2020-2032)

7.2.2 Deployment Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Managed Service

7.3.1 Managed Service Market Trends Analysis (2020-2032)

7.3.2 Managed Service Market Size Estimates and Forecasts to 2032 (USD Billion)

8. ATM Market Segmentation, By Type

8.1 Chapter Overview

8.2 Conventional/Bank ATMs

8.2.1 Conventional/Bank ATMs Market Trends Analysis (2020-2032)

8.2.2 Conventional/Bank ATMs Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Brown ATMs

8.3.1 Brown ATMs Market Trends Analysis (2020-2032)

8.3.2 Brown ATMs Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 White ATMs

8.4.1 White ATMs Market Trends Analysis (2020-2032)

8.4.2 White ATMs Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 Cash Dispenser ATM

8.5.1 Cash Dispenser ATM Market Trends Analysis (2020-2032)

8.5.2 Cash Dispenser ATM Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 Smart ATMs

8.6.1 Smart ATMs Market Trends Analysis (2020-2032)

8.6.2 Smart ATMs Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Regional Analysis

9.1 Chapter Overview

9.2 North America

9.2.1 Trends Analysis

9.2.2 North America ATM Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.2.3 North America ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.2.4 North America ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.5 USA

9.2.5.1 USA ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.2.5.2 USA ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.6 Canada

9.2.6.1 Canada ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.2.6.2 Canada ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.2.7 Mexico

9.2.7.1 Mexico ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.2.7.2 Mexico ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3 Europe

9.3.1 Eastern Europe

9.3.1.1 Trends Analysis

9.3.1.2 Eastern Europe ATM Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.1.3 Eastern Europe ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.1.4 Eastern Europe ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.5 Poland

9.3.1.5.1 Poland ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.1.5.2 Poland ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.6 Romania

9.3.1.6.1 Romania ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.1.6.2 Romania ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.7 Hungary

9.3.1.7.1 Hungary ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.1.7.2 Hungary ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.8 turkey

9.3.1.8.1 Turkey ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.1.8.2 Turkey ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.1.9 Rest of Eastern Europe

9.3.1.9.1 Rest of Eastern Europe ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.1.9.2 Rest of Eastern Europe ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2 Western Europe

9.3.2.1 Trends Analysis

9.3.2.2 Western Europe ATM Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.3.2.3 Western Europe ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.4 Western Europe ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.5 Germany

9.3.2.5.1 Germany ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.5.2 Germany ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.6 France

9.3.2.6.1 France ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.6.2 France ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.7 UK

9.3.2.7.1 UK ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.7.2 UK ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.8 Italy

9.3.2.8.1 Italy ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.8.2 Italy ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.9 Spain

9.3.2.9.1 Spain ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.9.2 Spain ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.10 Netherlands

9.3.2.10.1 Netherlands ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.10.2 Netherlands ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.11 Switzerland

9.3.2.11.1 Switzerland ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.11.2 Switzerland ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.12 Austria

9.3.2.12.1 Austria ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.12.2 Austria ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.3.2.13 Rest of Western Europe

9.3.2.13.1 Rest of Western Europe ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.3.2.13.2 Rest of Western Europe ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4 Asia Pacific

9.4.1 Trends Analysis

9.4.2 Asia Pacific ATM Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.4.3 Asia Pacific ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.4 Asia Pacific ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.5 China

9.4.5.1 China ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.5.2 China ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.6 India

9.4.5.1 India ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.5.2 India ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.5 japan

9.4.5.1 Japan ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.5.2 Japan ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.6 South Korea

9.4.6.1 South Korea ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.6.2 South Korea ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.7 Vietnam

9.4.7.1 Vietnam ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.2.7.2 Vietnam ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.8 Singapore

9.4.8.1 Singapore ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.8.2 Singapore ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.9 Australia

9.4.9.1 Australia ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.9.2 Australia ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.4.10 Rest of Asia Pacific

9.4.10.1 Rest of Asia Pacific ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.4.10.2 Rest of Asia Pacific ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5 Middle East and Africa

9.5.1 Middle East

9.5.1.1 Trends Analysis

9.5.1.2 Middle East ATM Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.1.3 Middle East ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.1.4 Middle East ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.5 UAE

9.5.1.5.1 UAE ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.1.5.2 UAE ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.6 Egypt

9.5.1.6.1 Egypt ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.1.6.2 Egypt ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.7 Saudi Arabia

9.5.1.7.1 Saudi Arabia ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.1.7.2 Saudi Arabia ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.8 Qatar

9.5.1.8.1 Qatar ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.1.8.2 Qatar ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.1.9 Rest of Middle East

9.5.1.9.1 Rest of Middle East ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.1.9.2 Rest of Middle East ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2 Africa

9.5.2.1 Trends Analysis

9.5.2.2 Africa ATM Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.5.2.3 Africa ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.2.4 Africa ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2.5 South Africa

9.5.2.5.1 South Africa ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.2.5.2 South Africa ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2.6 Nigeria

9.5.2.6.1 Nigeria ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.2.6.2 Nigeria ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.5.2.7 Rest of Africa

9.5.2.7.1 Rest of Africa ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.5.2.7.2 Rest of Africa ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6 Latin America

9.6.1 Trends Analysis

9.6.2 Latin America ATM Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

9.6.3 Latin America ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.6.4 Latin America ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.5 brazil

9.6.5.1 Brazil ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.6.5.2 Brazil ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.6 Argentina

9.6.6.1 Argentina ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.6.6.2 Argentina ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.7 Colombia

9.6.7.1 Colombia ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.6.7.2 Colombia ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

9.6.8 Rest of Latin America

9.6.8.1 Rest of Latin America ATM Market Estimates and Forecasts, By Solution (2020-2032) (USD Billion)

9.6.8.2 Rest of Latin America ATM Market Estimates and Forecasts, By Type (2020-2032) (USD Billion)

10. Company Profiles

10.1 Diebold Nixdorf

10.1.1 Company Overview

10.1.2 Financial

10.1.3 Products/ Services Offered

10.1.4 SWOT Analysis

10.2 NCR Corporation

10.2.1 Company Overview

10.2.2 Financial

10.2.3 Products/ Services Offered

10.2.4 SWOT Analysis

10.3 Triton Systems of Delaware LLC

10.3.1 Company Overview

10.3.2 Financial

10.3.3 Products/ Services Offered

10.3.4 SWOT Analysis

10.4 Hitachi Channel Solutions Corp.

10.4.1 Company Overview

10.4.2 Financial

10.4.3 Products/ Services Offered

10.4.4 SWOT Analysis

10.5 Hyosung TNS Inc

10.5.1 Company Overview

10.5.2 Financial

10.5.3 Products/ Services Offered

10.5.4 SWOT Analysis

10.6 GRG Banking Equipment Co. Ltd

10.6.1 Company Overview

10.6.2 Financial

10.6.3 Products/ Services Offered

10.6.4 SWOT Analysis

10.7 Fujitsu Frontech Ltd

10.7.1 Company Overview

10.7.2 Financial

10.7.3 Products/ Services Offered

10.7.4 SWOT Analysis

10.8 Euronet Worldwide Inc.

10.8.1 Company Overview

10.8.2 Financial

10.8.3 Products/ Services Offered

10.8.4 SWOT Analysis

10.9 OKI Electric Industry Co. Ltd.

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

10.10 Glory Ltd.

10.9.1 Company Overview

10.9.2 Financial

10.9.3 Products/ Services Offered

10.9.4 SWOT Analysis

11. Use Cases and Best Practices

12. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Solution

Deployment

Managed Service

By Type

Conventional/Bank ATMs

Brown ATMs

White ATMs

Cash Dispenser ATM

Smart ATMs

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Deep Learning Market was valued at USD 72.31 billion in 2023 and is expected to reach USD 858.69 billion by 2032, growing at a CAGR of 31.69% by 2032.

Gigabit Passive Optical Network Market was valued at USD 6.7 Billion in 2023 and will reach USD 12.9 Million by 2032, growing at a CAGR of 7.49% by 2032.

The Fleet Management Software Market Size was valued at USD 28.80 billion in 2023 and is expected to reach USD 93.17 Billion by 2032 and grow at a CAGR of 14.70% over the forecast period 2024-2032.

The Roaming Tariff Market was valued at USD 77.5 Billion in 2023 and is expected to reach USD 140.3 Billion by 2032, growing at a CAGR of 6.83% by 2032.

The Artificial Intelligence in Manufacturing Market was valued at USD 3.4 billion in 2023 and is expected to reach USD 103.3 billion by 2032, growing at a CAGR of 46.08% from 2024-2032.

Attack Surface Management Market was valued at USD 858.97 million in 2023 and is expected to reach USD 8247.40 million by 2032, growing at a CAGR of 28.60% from 2024-2032

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd