Artillery Systems Market Report Scope & Overview:

The Artillery Systems Market Size was valued at USD 11.4 billion in 2023 and is expected to reach USD 19.3 billion by 2032 and grow at a CAGR of 6.0% over the forecast period 2024-2032. The market for artillery systems is fragmented, with several global and local firms contributing considerably to market growth via competitive pricing and innovation. BAE Systems PLC, Lockheed Martin Corporation, Hanwha Group, Leonardo SpA, and Nexter Group are some of the leading players in the artillery systems industry. To grow their market share, the firms are primarily focused on improving the capabilities of their artillery systems portfolio. BAE Systems PLC presented a new modular ARCHER Mobile Howitzer at Defence and Security Equipment International (DSEI) in 2020. The new system, according to the manufacturer, has a 21-round auto-loader and onboard ballistic computation, and it can fire up to eight rounds per minute at ranges reaching 40 kilometres with conventional 155 mm ammunition and 60 kilometres with precision-guided missiles. Foreign players are vying with domestic players for multibillion-dollar long-term contracts. Some players have also formed alliances with local businesses in order to broaden their consumer base and exchange technological skills.

To get more information on Artillery Systems Market - Request Free Sample Report

Tensions in Eastern Europe, the Middle East, and the Asia-Pacific region are driving demand for new artillery systems. Demand is also increasing in the United States, which is attempting to address gaps in its ground forces by replacing ageing weapons with modern artillery systems. Furthermore, during the last decade, an increasing emphasis on boosting naval capabilities has resulted in major new orders for frigates, corvettes, aircraft carriers, destroyers, and offshore boats, necessitating the need for new artillery weapons. In 2021, Leonardo and BAE Systems controlled the naval artillery systems market.

The artillery system market is expanding rapidly as a result of an increase in cross-border conflicts. A long-range weapon is an artillery system. Artillery may fire weapons far beyond the range of infantry and tanks. A projectile is aimed and fired by an artillery cannon without relying on a direct line of sight between the target and the artillery gun. As a result, artillery guns employ a variety of systems to track and find targets that are out of their line of sight. Among the several artillery systems are the target acquisition system, communication system, and command and control system. Artillery systems are often utilised in warfare to offer close support fire to suppress and neutralise opposing forces.

Artillery guns are designed to fire explosives at greater distances than small arms and light weapons, providing fire support for armour and infantry troops. The term artillery gun especially refers to self-propelled, towed, and emplaced weapons built for indirect fire and capable of hitting targets at a long distance. Artillery guns might be self-propelled, towed, armoured, or unarmed. However, technical advancements in the 155 mm bullet are expected to stretch the present artillery weapons' ranges between 44 and 62 miles (70-99 km). As a result, the 155 mm artillery fuels market expansion.

MARKET DYNAMICS

DRIVERS:

-

Government defense budgets play a crucial role in determining the procurement and development of artillery systems.

-

Modernization and Upgrades is the driver of the Artillery Systems Market.

Many countries continuously seek to modernize their military equipment, including artillery systems, to maintain a competitive edge in defense capabilities. Upgrading existing artillery platforms with advanced components can be a significant driver.

RESTRAIN:

-

Certain terrain or operational conditions might limit the effective use of artillery systems, reducing their attractiveness in specific scenarios.

-

Ethical and Humanitarian Considerations are the restraint of the Artillery Systems Market.

Concerns about the humanitarian consequences of artillery use, especially in populated areas, might lead to increased scrutiny and calls for more responsible weapon usage.

OPPORTUNITY:

-

Offering comprehensive maintenance, support, and upgrade services for existing artillery systems can be a lucrative opportunity for defense companies.

-

Joint and Network-Centric Operations are an opportunity for the Artillery Systems Market.

Artillery systems that seamlessly integrate with other military assets in joint and network-centric operations offer enhanced capabilities and are in demand.

CHALLENGES:

-

Political tensions and international conflicts can impact arms trade agreements, affecting the potential sales of artillery systems to certain regions.

-

Cost Constraints are the challenges of the Artillery Systems Market.

Developing, manufacturing, and maintaining advanced artillery systems can be expensive, and budget limitations can hinder the acquisition and modernization of these systems.

IMPACT OF RUSSIAN UKRAINE WAR

While Russia has struggled in other areas of the battlefield, artillery has been critical to its ability to keep Ukrainian forces at bay. To overcome hurdles and attain higher efficacy, the Russian armed forces have altered classical artillery practises. Artillery is crucial to the Russian manner of combat; hence Western troops must fully comprehend it. The gunnery issue, which highlights the technical obstacles involved in striking a target using indirect rounds, is the same regardless of country. These difficulties include the precise acquisition and utilisation of meteorological data, which will affect flight route and speed, as well as survey data, which is crucial for determining where the firing cannon is positioned and where it is pointed, as well as accurate target localization.

Many of Russia's weaponry and most experienced crews are believed to have been lost. Russian strikes, on the other hand, are frequently preceded by substantial indirect fire; Russia's ammunition consumption and testimonies from Ukraine both corroborate this viewpoint. Artillery fires are responsible for 70% of Ukraine's casualties. Despite the hurdles, it is obvious that Russian artillery is having a substantial influence on the Ukrainian armed forces and delivering effects using a combination of creative tactics and technology, as well as a reliance on conventional doctrine. In this conflict, the Artillery Systems Market gains profit up to 3.4-4.5%

IMPACT OF ONGOING RECESSION

In the present global crisis, a comparative examination of specific world countries' defence plans must be done within the context of the worldwide crisis that began in 2020. In terms of its unique origins and evolution, the context, the trigger, the consequences, and the anti-crisis programmes devised by countries and international organisations. In terms of its origins, there is a growing consensus that, in the early years of the twentieth century, major international investors operated in an environment of increasing uncertainty about the future evolution of commodity markets such as oil and natural gas, raw materials, and rare minerals.

According to oil market statistics, demand for oil in the United States increased from 22 million barrels per day in early 2020 to about 31 million in 2021-2022, representing a 30% increase in consumption prior to the downward trend caused by the economic crisis. Over the same time, OPEP output climbed by 37%, while non-OPEP production increased by 21%, for a total global production of 106.38 million barrels per day.

KEY MARKET SEGMENTATION

By Caliber

-

Heavy

-

Medium

-

Small

By Range

-

Long

-

Medium

-

Short

By Type

-

Anti-Air

-

Mortar

-

Rocket

-

Howitzer

-

Others

By Component

-

Gun Turret

-

Fire Control System

-

Engine

-

Chassis

-

Others

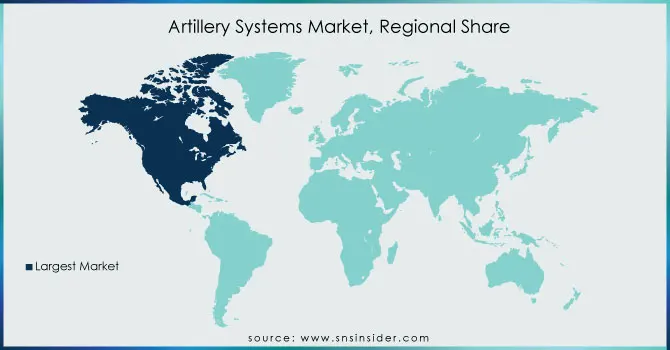

REGIONAL ANALYSIS

North America: North America is expected to retain its dominance in the Artillery Systems market during the projected period. Due to the rising need for better protective solutions in the defence and military sectors, the United States, the world's largest military spender, is occupied with the most contemporary and massive amount of defence equipment, contributing significantly to North America's market growth. Because of the increase in terror attacks, the European Market is now the second-largest share-holding market, after only North America. Market expansion is encouraged in European countries such as the United Kingdom, France, Russia, and Germany.

Asia Pacific: During the projection period, Asia-Pacific is predicted to grow at a rapid pace. The increased tensions among the countries in this area have prompted a fast modernisation of the military forces. China, India, Australia, Japan, and South Korea are all heavily investing in the research, construction, and acquisition of artillery systems.

Need any customization research on Artillery Systems Market - Enquiry Now

REGIONAL COVERAGE:

North America

-

US

-

Canada

-

Mexico

Europe

-

Eastern Europe

-

Poland

-

Romania

-

Hungary

-

Turkey

-

Rest of Eastern Europe

-

-

Western Europe

-

Germany

-

France

-

UK

-

Italy

-

Spain

-

Netherlands

-

Switzerland

-

Austria

-

Rest of Western Europe

-

Asia Pacific

-

China

-

India

-

Japan

-

South Korea

-

Vietnam

-

Singapore

-

Australia

-

Rest of Asia Pacific

Middle East & Africa

-

Middle East

-

UAE

-

Egypt

-

Saudi Arabia

-

Qatar

-

Rest of Middle East

-

-

Africa

-

Nigeria

-

South Africa

-

Rest of Africa

-

Latin America

-

Brazil

-

Argentina

-

Colombia

-

Rest of Latin America

KEY PLAYERS

Some major key players in the Artillery Systems Market are RUAG Group., IMI Systems, General Dynamic, Elbit Systems, Lockheed Martin, Avibras, Denel SOC Ltd, BAE Systems, Hanwha Group, ST Engineering and other players.

RECENT DEVELOPMENTS

In 2021: Australia has agreed to purchase 30 K-9 Thunder self-propelled howitzers from South Korea. The seventh country that bought a howitzer from South Korea is Australia.

In 2021: Rheinmetall received a fresh order from the Netherlands for 155mm illumination and smoke/obscurant artillery munitions. In late 2023, the missiles will be transferred to the Netherlands.

In 2020: The US Army awarded Lockheed Martin a USD 183 million contract to construct and deliver 28 High Mobility Artillery Rocket System launchers and accompanying equipment. The deliveries are scheduled to begin in 2022.

| Report Attributes | Details |

| Market Size in 2023 | US$ 11.4 Bn |

| Market Size by 2032 | US$ 19.3 Bn |

| CAGR | CAGR of 6% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2023-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Caliber (Heavy, Medium, Small) • By Range (Long, Medium, Short) • By Type (Anti-Air, Mortar, Rocket, Howitzer, Others) • By Component (Gun Turret, Fire Control System, Engine, Chassis, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | RUAG Group., IMI Systems, General Dynamic, Elbit Systems, Lockheed Martin, Avibras, Denel SOC Ltd, BAE Systems, Hanwha Group, ST Engineering |

| Key Drivers | • Government defense budgets play a crucial role in determining the procurement and development of artillery systems. • Modernization and Upgrades is the driver of the Artillery Systems Market. |

| Market Restraints | • Certain terrain or operational conditions might limit the effective use of artillery systems, reducing their attractiveness in specific scenarios. • Ethical and Humanitarian Considerations are the restraint of the Artillery Systems Market. |