Get E-PDF Sample Report on Anti-wear Additives Market - Request Sample Report

The Anti-wear Additives Market size was USD 736.5 million in 2023 and is expected to reach USD 936.1 million by 2032 and grow at a CAGR of 2.7% over the forecast period of 2024-2032.

The automotive industry has become a significant driver of the anti-wear additives market due to the increasing production of vehicles worldwide and the growing focus on meeting stringent emission norms. Today's engines have to contend with performance that creates an environment in which high-performance lubricants are needed to minimize friction. Anti-wear additives are one of the most important components of lubricants, especially highly-loaded automotive applications, as they improve durability and efficiency. Moreover, the regulatory bodies around the world are imposing stringent emission norms, which necessitate the use of cleaner & more effective lubricants to minimize the environmental impact. The focus on vehicle performance and sustainability will maintain demand for quality anti-wear additives in engine oils, transmission fluids, and gear oils, to support the operation and longevity of automotive industry.

In response to environmental concerns, regulatory bodies have introduced rigorous emission standards. For instance, the U.S. Environmental Protection Agency (EPA) finalized new, stringent vehicle emission standards on March 20, 2024, targeting reductions in carbon dioxide and other pollutants for model years 2027 through 2032.

The increasing focus on renewable energy is significantly driving the demand for anti-wear additives as the global energy transition accelerates. High performance lubricants are extensively used in renewable energy systems such as wind turbines, solar power plants, and hydroelectric facilities to enhance the functioning in harsh conditions. Antiwear additives are essential in improving the life and reliability of such lubricants by protecting critical components such as gears and bearings against wear. New renewable energy capacity around the world increased by 9.6% last year, according to the International Renewable Energy Agency (IRENA). The rapid growth of these industries requires modern lubrication solutions to run efficient businesses and to lower maintenance cost perspective of the huge wind turbines and solar installation form, as a termination in their functioning can result in a huge monetary loss. The growing renewable energy sector, fueled by favorable government regulations and sustainability agendas, will likely further drive the use of anti-wear additives, which are critical to the global effort to cleaner energy alternatives.

Drivers

Focus on High-Performance Synthetic Lubricants drives the market growth.

The increasing focus on high-performance synthetic lubricants is one of the primary growth factors for the anti-wear additives market. Due to their better thermal stability (high temperature), low-temperature fluidity, and higher oxidation stability, synthetic lubricants find usage in various industries. They are designed to work under the most extreme challenges of high temperature, load, and cycle use and thus are essential to automotive engines, vessels in aerospace, and other industrial uses. The antiwear additives supplement these lubricants by reducing friction and wear, resulting in a longer service life of mechanical components. This trend towards high-performance lubricants is driving the requirement for quality anti-wear additives which are needed to meet the performance demands of modern machinery.

in June 2023 the Shell Helix HX6 5W-30 and Shell Helix SUV 5W-30 are new high-performance synthetic engine oils that Shell unveiled in response to the changing demands of contemporary automobiles.

Restraint

High cost of advanced additives may hamper the market growth.

One of the biggest growth challenges for the market is the high cost of advanced anti-wear additives. These additives are critical for improving the performance and life span of lubricants and used in various industries such as automotive, aerospace, and industrial manufacturing. These higher end additives frequently require very specific raw materials, highly complex manufacturing processes, and even more R&D all of which can drive costs through the roof. However, in many industries, especially those where costs are sensitive or in emerging markets, the cost of these high-performance additives is prohibitive and many manufacturers choose to go for cheaper alternatives. Such cost-related hindrance may curb the market penetration of advanced anti-wear additives, hence restraining the overall growth of the industry. In addition, insufficient adoption of such additives by small and medium-sized enterprises due to its higher price might also restraining the market growth.

By Type

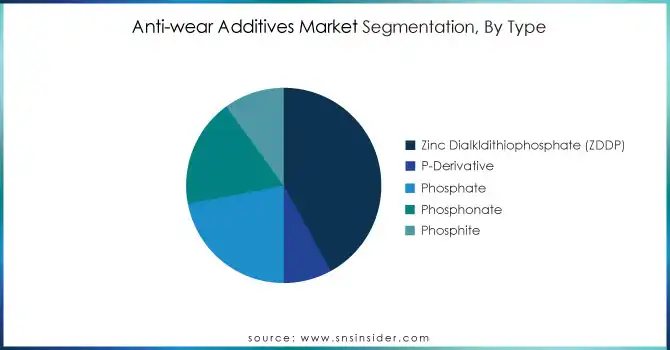

The Zinc Dialkldithiophosphate (ZDDP) segment held the largest market share around 42% in 2023. This is because of its good anti-wear performance, antioxidant performance, and corrosion performance. Over the years, it has been a core ingredient in virtually every automotive engine oil out there, providing a high level of protection for engine wear even elastomers like seal rubbers under extreme conditions such as high temperature and heavy loads. The reason it is the choice of many of the lubricant manufactures because of the effectiveness in increasing the performance and life of the engines. Although there is a growing regulatory pressure to limit the use of ZDDP because of its potential toxicity to the environment, ZDDP remains as a vast majority of the market due to its low cost and ability to perform consistently in many applications. This ubiquitous practice among automotive and industrial applications sustains ZDDP's preeminence in the marketplace, despite the increasing interest in alternative additives such as phosphates and phosphonates for their purported environmental advantage.

By Application

Engine oil held the largest market share around 34% in 2023. This is due to its use in every passenger vehicle and most commercial fleets there is a constant demand for anti-wear additives including Zinc Dialkyldithiophosphate (ZDDP) to prevent engine components from excessive wear. Increasing demand for high-performance engine oils (supplemented with anti-wear additives) persists in the automotive sector, particularly in developing regions which in turn, is expected to bolster growth of the base oil market during the forecast period. Advancements in engine oils have also accelerated from increasing regulatory pressures for enhanced fuel efficiency and lower emissions, which will provide additional catalytic effect for adoption of newer generation anti-wear additives. The established dependency on engine oil for maximized vehicle performance perpetuates its supremacy in the anti-wear additive sector.

North America held the largest market share around 43% in 2023. It is owing to large presence of key verticals such as automotive, aerospace and manufacturing which produce high demand for the advanced lubricants. This area has some of the biggest automotive manufacturers in the world such as General Motors, Ford, and Chrysler which necessitate high-performance engine oils with a high standard of Engine Efficiency and engine durability. Furthermore, aerospace and industrial machinery industries are mature in the U.S. and Canada, both of which use lubricants with anti-wear additives to keep sophisticated instruments running smoothly. In addition to this, the regulatory standards present in North America as well as the standards set by the EPA (Environmental Protection Agency) and some other similar organizations are driving towards the usage of high efficiency and durability of the lubricants which ends up creating a high demand of anti-wear additives. Increasing awareness of the performance and longevity of vehicles, coupled with these factors, further benefits the stronghold North America has on the global anti-wear additives market.

Get Customized Report as Per Your Business Requirement - Request For Customized Report

Key Players

Chemtura Corporation (Durad 620C, Reolube Turbofluid 46XC)

Evonik (ViscoTreat 301, Dynasylan Silanes)

Chevron Oronite (Paratone 855, OLOA 48027)

Vanderbilt Chemicals (VANLUBE 960E, MOLYPAUL 994)

Lubrizol (Lubrizol 7723, Estane 3D TPU M95A)

Infineum (Infineum P5351, Infineum V3000)

Tianhe Chemicals Group (T616, T4208)

Afton Chemical Corporation (HiTEC 1111, HiTEC 5000)

BASF (Keropur 3700, Irganox L57)

Croda International (Priolube 3970, Crodacol C90)

Clariant (AddWorks LXR 568, Licocene PP MA 6452)

Dow Chemical (UCON Fluid AP, Xiameter Silicone Fluids)

ExxonMobil Chemical (SpectraSyn Elite 300, Mobilgard 300)

TotalEnergies (Eolys PowerFlex, HydraSyn)

Shell Global (Gadus S2 V220, Helix Ultra)

Fuchs Petrolub (RENOLIN MR 520, Silkolene Pro Boost)

LANXESS (Additin RC 9800, Durad 220A)

Royal Purple (Max-Tane, Synfilm GT)

Petro-Canada Lubricants (Duron-E SHP 10W-30, Purity FG2)

Idemitsu Kosan (Zeropro 0W-20, Daphne EPI 150)

In October 2022, Azelis finalized the acquisition of Ak-ta? as part of its long-term strategy to expand its portfolio of products and enhance its position in the global lubricant additives market.

In 20 June 2021, EverArc Holdings Limited reached agreement with SK Invictus Holdings S.à. purchase agreement to procure 100% of SK Invictus Intermediate S.à. r.l. to improve business processes and purchasing power.

In July 2022, Gold Eagle Co. acquired Lubrication Specialties Inc. to broaden its product offering and increase its market presence in the lubricant additives market.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 736.5 Million |

| Market Size by 2032 | USD 936.1 Million |

| CAGR | CAGR of 2.7% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Zinc Dialkldithiophosphate (ZDDP), P-Derivative, Phosphate, Phosphonate, Phosphite) • By Application (Engine Oil, Automotive Gear Oil, Automotive Transmission Fluid, Metal working Fluid, Greases, Hydraulic Oil, Others) • By Sales Channel (Merchant, Captive) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Chemtura Corporation, Evonik, Chevron Oronite, Vanderbilt Chemicals, Lubrizol, Infineum, Tianhe Chemicals Group, Afton Chemical Corporation |

| Key Drivers | • Focus on High-Performance Synthetic Lubricants drives the market growth. |

| Restraints | • High cost of advanced additives may hamper the market growth. |

Ans: Manufacturers, Consultant, aftermarket players, association, Research institute, private and universities libraries, suppliers and distributors of the product.

Ans: The COVID-19 has a significant negative effect on the automobile industry, which includes engine oil, automotive gear oil, and automotive transmission fluid. Over the course of 2020 and 2021, a fall in demand for autos and commercial vehicles is anticipated. The COVID-19 pandemic has caused the production of cars in North America to stop in excess of 80%. The scenario is similar in Europe and Asia Pacific. Production has temporarily been halted by businesses like Ford, General Motors, Fiat Chrysler Automobiles, Honda, and Tesla. Even if these businesses start up again once the epidemic passes, the car industry will suffer from economic uncertainty and a drop in customer spending power.

Ans: BRIC countries provide lucrative market prospects are the opportunity for Anti-wear Additives Market.

Ans: Fluctuating crude oil prices are the challenges faced by theAnti-wear Additives Market.

Ans: Anti-wear Additives Market Size was valued at USD 736.5 million in 2023, and expected to reach USD 936.1 million by 2032, and grow at a CAGR of 2.7 % over the forecast period 2024-2032.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 By Production Capacity and Utilization, by Country, By Type, 2023

5.2 Feedstock Prices, by Country, By Type, 2023

5.3 Regulatory Impact, by l Country, By Type, 2023.

5.4 Environmental Metrics: Emissions Data, Waste Management Practices, and Sustainability Initiatives, by Region

5.5 Innovation and R&D, Type, 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new Product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Anti-wear Additives Market Segmentation, by Type

7.1 Chapter Overview

7.2 Zinc Dialkldithiophosphate (ZDDP)

7.2.1 Zinc Dialkldithiophosphate (ZDDP) Market Trends Analysis (2020-2032)

7.2.2 Zinc Dialkldithiophosphate (ZDDP) Market Size Estimates and Forecasts to 2032 (USD Million)

7.3 P-Derivative

7.3.1 P-Derivative Market Trends Analysis (2020-2032)

7.3.2 P-Derivative Market Size Estimates and Forecasts to 2032 (USD Million)

7.4 Phosphate

7.4.1 Phosphate Market Trends Analysis (2020-2032)

7.4.2 Phosphate Market Size Estimates and Forecasts to 2032 (USD Million)

7.5 Phosphonate

7.5.1 Phosphonate Market Trends Analysis (2020-2032)

7.5.2 Phosphonate Market Size Estimates and Forecasts to 2032 (USD Million)

7.6 Phosphite

7.6.1 Phosphite Market Trends Analysis (2020-2032)

7.6.2 Phosphite Market Size Estimates and Forecasts to 2032 (USD Million)

8. Anti-wear Additives Market Segmentation, by Application

8.1 Chapter Overview

8.2 Engine Oil

8.2.1 Engine Oil Market Trends Analysis (2020-2032)

8.2.2 Engine Oil Market Size Estimates and Forecasts to 2032 (USD Million)

8.3 Automotive Gear Oil

8.3.1 Automotive Gear Oil Market Trends Analysis (2020-2032)

8.3.2 Automotive Gear Oil Market Size Estimates and Forecasts to 2032 (USD Million)

8.4 Automotive Transmission Fluid

8.4.1 Automotive Transmission Fluid Market Trends Analysis (2020-2032)

8.4.2 Automotive Transmission Fluid Market Size Estimates and Forecasts to 2032 (USD Million)

8.5 Metalworking Fluid

8.5.1 Metalworking Fluid Market Trends Analysis (2020-2032)

8.5.2 Metalworking Fluid Market Size Estimates and Forecasts to 2032 (USD Million)

8.6 Greases

8.6.1 Greases Market Trends Analysis (2020-2032)

8.6.2 Greases Market Size Estimates and Forecasts to 2032 (USD Million)

8.7 Hydraulic Oil

8.7.1 Hydraulic Oil Fluid Market Trends Analysis (2020-2032)

8.7.2 Hydraulic Oil Market Size Estimates and Forecasts to 2032 (USD Million)

8.8 Others

8.8.1 Others Market Trends Analysis (2020-2032)

8.8.2 Others Market Size Estimates and Forecasts to 2032 (USD Million)

9. Anti-wear Additives Market Segmentation, by Sales Channel

9.1 Chapter Overview

9.2 Merchant

9.2.1 Merchant Market Trends Analysis (2020-2032)

9.2.2 Merchant Market Size Estimates and Forecasts to 2032 (USD Million)

9.3 Captive

9.3.1 Captive Market Trends Analysis (2020-2032)

9.3.2 Captive Market Size Estimates and Forecasts to 2032 (USD Million)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Anti-wear Additives Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.2.3 North America Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.2.4 North America Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.5 North America Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.2.6 USA

10.2.6.1 USA Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.2.6.2 USA Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.6.3 USA Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.2.7 Canada

10.2.7.1 Canada Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.2.7.2 Canada Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.7.3 Canada Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.2.8 Mexico

10.2.8.1 Mexico Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.2.8.2 Mexico Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.2.8.3 Mexico Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Anti-wear Additives Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.1.3 Eastern Europe Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.1.4 Eastern Europe Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.5 Eastern Europe Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.1.6 Poland

10.3.1.6.1 Poland Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.1.6.2 Poland Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.6.3 Poland Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.1.7 Romania

10.3.1.7.1 Romania Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.1.7.2 Romania Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.7.3 Romania Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.1.8.2 Hungary Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.8.3 Hungary Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.1.9.2 Turkey Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.9.3 Turkey Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.1.10.2 Rest of Eastern Europe Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.1.10.3 Rest of Eastern Europe Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Anti-wear Additives Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.3.2.3 Western Europe Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.4 Western Europe Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.5 Western Europe Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.6 Germany

10.3.2.6.1 Germany Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.6.2 Germany Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.6.3 Germany Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.7 France

10.3.2.7.1 France Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.7.2 France Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.7.3 France Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.8 UK

10.3.2.8.1 UK Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.8.2 UK Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.8.3 UK Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.9 Italy

10.3.2.9.1 Italy Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.9.2 Italy Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.9.3 Italy Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.10 Spain

10.3.2.10.1 Spain Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.10.2 Spain Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.10.3 Spain Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.11.2 Netherlands Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.11.3 Netherlands Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.12.2 Switzerland Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.12.3 Switzerland Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.13 Austria

10.3.2.13.1 Austria Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.13.2 Austria Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.13.3 Austria Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.3.2.14.2 Rest of Western Europe Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.3.2.14.3 Rest of Western Europe Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Anti-wear Additives Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.4.3 Asia Pacific Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.4 Asia Pacific Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.5 Asia Pacific Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.6 China

10.4.6.1 China Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.6.2 China Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.6.3 China Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.7 India

10.4.7.1 India Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.7.2 India Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.7.3 India Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.8 Japan

10.4.8.1 Japan Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.8.2 Japan Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.8.3 Japan Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.9 South Korea

10.4.9.1 South Korea Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.9.2 South Korea Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.9.3 South Korea Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.10 Vietnam

10.4.10.1 Vietnam Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.10.2 Vietnam Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.10.3 Vietnam Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.11 Singapore

10.4.11.1 Singapore Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.11.2 Singapore Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.11.3 Singapore Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.12 Australia

10.4.12.1 Australia Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.12.2 Australia Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.12.3 Australia Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.4.13.2 Rest of Asia Pacific Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.4.13.3 Rest of Asia Pacific Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Anti-wear Additives Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.1.3 Middle East Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.1.4 Middle East Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.5 Middle East Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.1.6 UAE

10.5.1.6.1 UAE Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.1.6.2 UAE Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.6.3 UAE Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.1.7.2 Egypt Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.7.3 Egypt Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.1.8.2 Saudi Arabia Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.8.3 Saudi Arabia Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.1.9.2 Qatar Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.9.3 Qatar Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.1.10.2 Rest of Middle East Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.1.10.3 Rest of Middle East Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Anti-wear Additives Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.5.2.3 Africa Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.2.4 Africa Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.5 Africa Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.2.6.2 South Africa Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.6.3 South Africa Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.2.7.2 Nigeria Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.7.3 Nigeria Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.5.2.8.2 Rest of Africa Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.5.2.8.3 Rest of Africa Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Anti-wear Additives Market Estimates and Forecasts, by Country (2020-2032) (USD Million)

10.6.3 Latin America Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.6.4 Latin America Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.5 Latin America Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.6.6 Brazil

10.6.6.1 Brazil Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.6.6.2 Brazil Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.6.3 Brazil Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.6.7 Argentina

10.6.7.1 Argentina Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.6.7.2 Argentina Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.7.3 Argentina Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.6.8 Colombia

10.6.8.1 Colombia Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.6.8.2 Colombia Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.8.3 Colombia Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Anti-wear Additives Market Estimates and Forecasts, by Type (2020-2032) (USD Million)

10.6.9.2 Rest of Latin America Anti-wear Additives Market Estimates and Forecasts, by Application (2020-2032) (USD Million)

10.6.9.3 Rest of Latin America Anti-wear Additives Market Estimates and Forecasts, by Sales Channel (2020-2032) (USD Million)

11. Company Profiles

11.1 Chemtura Corporation

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Product/ Services Offered

11.1.4 SWOT Analysis

11.2 Evonik

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Product/ Services Offered

11.2.4 SWOT Analysis

11.3 Chevron Oronite

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Product/ Services Offered

11.3.4 SWOT Analysis

11.4 Vanderbilt Chemicals

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Product/ Services Offered

11.4.4 SWOT Analysis

11.5 Lubrizol

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Product/ Services Offered

11.5.4 SWOT Analysis

11.6 Infineum

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Product/ Services Offered

11.6.4 SWOT Analysis

11.7 Tianhe Chemicals Group

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Product/ Services Offered

11.7.4 SWOT Analysis

11.8 Afton Chemical Corporation

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Product/ Services Offered

11.8.4 SWOT Analysis

11.9 Petro-Canada Lubricants

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Product/ Services Offered

11.9.4 SWOT Analysis

11.10 ExxonMobil Chemical

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Product/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Type

Zinc Dialkldithiophosphate (ZDDP)

P-Derivative

Phosphate

Phosphonate

Phosphite

By Application

Engine Oil

Automotive Gear Oil

Automotive Transmission Fluid

Metalworking Fluid

Greases

Hydraulic Oil

Others

By Sales Channel

Merchant

Captive

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Propylene Carbonate Market size was USD 396.40 Million in 2023 and is expected to reach USD 672.63 Million by 2032, growing at a CAGR of 6.05% from 2024-2032.

The Wax Emulsion Market was valued at USD 1.95 Billion in 2023 and is expected to reach USD 2.93 Billion by 2032, growing at a CAGR of 4.66% from 2024-2032.

The Isoamyl Acetate Market size was valued at USD 366.8 Million in 2023. It is expected to grow to USD 605.05 Million by 2032 and grow at a CAGR of 5.7% over the forecast period of 2024-2032.

Electric Vehicle Fluids Market Size was valued at USD 1.2 Billion in 2023 and is expected to reach USD 12.6 Billion by 2032 and grow at a CAGR of 29.5% over the forecast period 2024-2032.

LIB Cathode Conductive Auxiliary Agents Market was valued at $ 1.51 Bn in 2023 and is expected to reach $ 7.28 Bn by 2032, at a CAGR of 19.10% from 2024-2032.

The Biofertilizers Market size was valued at USD 2.7 Billion in 2023. It is expected to grow to USD 7.10 Billion by 2032 and grow at a CAGR of 11.4% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd