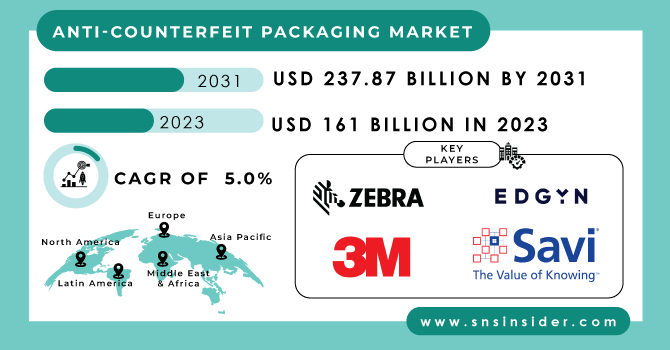

The Anti-counterfeit Packaging Market size was USD 161 billion in 2023 and is expected to reach USD 237.87 billion by 2031 and grow at a CAGR of 5 % over the forecast period of 2024-2031.

The Anti-counterfeit packaging market refers to the industry involved in packaging products to prevent the counterfeiting of branded products. Many products in the market are copies or replicas of branded products. Anti-counterfeit packaging is one of the best ways to overcome this. Anti-counterfeit packaging solution helps customer to identify between branded products and counterfeit goods.

Get More Information on Anti-Counterfeit Packaging Market - Request Sample Report

There has been a rise in Anti-counterfeit packaging globally due to consumer awareness about the risk of counterfeit goods. Counterfeit goods can damage the brand image and risk public health, and financial losses can occur.

Technological advancements in this market have brought unique solutions to differentiate between counterfeit and branded goods. Holograms, QR Codes, and Unique Serial Numbers are some of the tools used in the Anti-counterfeit packaging market.

The demand for the Anti-counterfeit packaging market is likely to grow because of the steps taken by the government and many industries to fight against the counterfeiting of goods.

KEY DRIVERS:

Increase in counterfeit activities globally

Various industries including pharmaceuticals, electronics, and many luxurious goods are facing counterfeiting activities worldwide. Many companies are adopting anti-counterfeit packaging to protect themselves from counterfeiting as it may harm their brand image and reputation. The government and industries are together working on counterfeiting activities, which also boosts the anti-counterfeit market. The overall packaging industry is very large, so demand in the anti-counterfeit market is also increasing. Standard packaging does not give the ultimate solution to the counterfeiting of goods, this can only be done using anti-counterfeit technology such as holograms, RFID, and QR codes.

Growth of the E-Commerce Packaging industry.

Brand image protection

RESTRAIN:

High investment in technological advancement & increasing cost of production

The use of anti-counterfeit packaging increases the overall production cost of the final good, which ultimately affects the consumers. This will increase the demand for counterfeit goods. For industries to overall the counterfeit market technological advancement needs to be done and increasing investment in technology will increase the cost of production. This will lead to financial losses for the company.

Even after the use of holograms and barcodes to safeguard the product, still, counterfeit products can be seen, and this is slowing down the overall growth of the anti-counterfeit packaging market.

Customer awareness and education

OPPORTUNITY:

Agricultural Sector, Pharmaceuticals industry, food and beverages

This sector faces counterfeiting of goods at a high level. Many farmers get seeds for fake crops, this damages the brand image of reputed companies. Also, in the pharmaceuticals and food industry, counterfeit goods are seen with the brand name of a reputed company.

So, there is an increasing opportunity for anticounterfeit packaging to overcome counterfeiting activities in this industry.

Growth opportunities in the Emerging economies of India and China.

CHALLENGES:

Increasing consumer awareness and education

In countries such as India, where literacy level is low as compared to other developed countries, there is a need for consumer awareness about counterfeit goods. Counterfeit goods are much cheaper than the original goods, consumers are attracted to these goods. Creating consumer awareness and educating them is a bigger challenge for the anticounterfeit packaging industries.

Reducing the high cost of investment in technology

The war between the two countries affected the global economy, prices of goods increased, inflation increased and it affected the Anti-counterfeit packaging market and affected the industries in regions of Russia. The global supply chain was disrupted and prices of raw materials were fluctuating leading to the volatility of the overall market.

Covid 19 has affected the Anti-counterfeit packaging market to a large extent. The government-imposed restrictions on the movement of people and the supply chain was affected, due to which a shortage of raw materials was there which is necessary for production. Demand for FMCG products also decreased as people were not ready to buy packed goods due to fear of the spread of coronavirus.

On the other side, companies focused on the development of technology to overcome counterfeiting activities keeping in mind the safety of customers from covid 19 spread.

There was both direct and indirect impact of covid 19 on the anti-counterfeit packaging market. During covid, there was a need for personal protective equipment in the market. It became difficult to recognize the trusted products and the replicas. Due to supply chain disruption, there was a delay in the production and delivery of Anti-counterfeit packaging technologies and raw materials. There was also a need for the development of new technology and methods to safeguard public from the counterfeit goods. This affected the overall profitability of companies and the overall anti-counterfeit packaging market.

By Packaging Format:

Bottle & Jars

Blisters

Trays

Vials & Ampoules

Pouches & Sachets

Others

By Technology:

RFID

Forensic Makers

Mass Encoding

Holograms

Tampers Evidence

Others

By End Use:

Automotive

Pharmaceuticals

Personal Care

Luxury Goods

Food & Beverage

Electrical & Electronics

Others

REGIONAL ANALYSIS

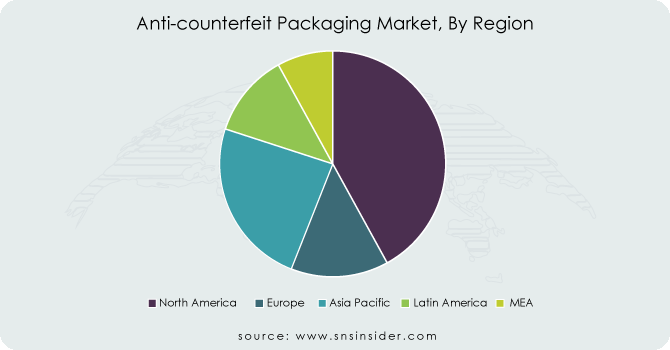

North America Region is holding the highest market share followed by Asia Pacific Region and Europe. Strict regulations against counterfeiting activities have increased the market share for the North American region.

In China and India market for anti-counterfeit packaging market will rise as they both are emerging economies, giving more exposure to growth as markets in developed countries matured.

Asia Pacific region is likely to show high CAGR growth during our forecast period of 2024-2031. This is likely to happen because of increasing consumer awareness about the disadvantages of counterfeit goods.

Get Customized Report as per Your Business Requirement - Request For Customized Report

REGIONAL COVERAGE:

North America

USA

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

The Netherlands

Rest of Europe

Asia-Pacific

Japan

South Korea

China

India

Australia

Rest of Asia-Pacific

The Middle East & Africa

Israel

UAE

South Africa

Rest of the Middle East & Africa

Latin America

Brazil

Argentina

Rest of Latin American

According to news of October 2022, the government has planned to launch Track and Trace mechanism. The top 300 selling drugs will print QR codes on their primary packaging.

The news in April 2023 of Amazon launching an Anti-counterfeiting exchange to identify and track counterfeiters.

In 2022, Amazon removed around more than 5 million counterfeit items from its supply chain.

Key players List-

Major players in the Anti-counterfeit packaging market are Zebra Technologies Corporation, 3M Company, SAVI Technology, EDGYN, Authentix Inc, Applied DNA Science, CCL Industries, Micro Tag Temed Ltd, Advance Track & Trace, DuPont, and other players.

| Report Attributes | Details |

| Market Size in 2023 | US$ 161 Bn |

| Market Size by 2031 | US$ 237.87 Bn |

| CAGR | CAGR of 14.3 % From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Packaging Format (Bottle & Jars, Blisters, Trays, Vials & Ampoules, Pouches & Sachets, Others) • By Technology (RFID, Forensic Makers, Mass Encoding, Holograms, Tampers Evidence, Others) • By End Use (Automotive, Pharmaceuticals, Personal Care, Luxury Goods, Food & Beverage, Electrical & Electronics, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Zebra Technologies Corporation, 3M Company, SAVI Technology, EDGYN, Authentix Inc, Applied DNA Science, CCL Industries, Micro Tag Temed Ltd, Advance Track & Trace, DuPont |

| Key Drivers | • Increase in counterfeit activities globally |

| Market Opportunities | • Agricultural Sector, Pharmaceuticals industry, food, and beverages |

Ans: The Anti-counterfeit Packaging Market is expected to grow at a CAGR of 5% over the forecast period of 2024-2031.

Ans: The Anti-counterfeit Packaging Market size was USD 161 billion in 2023 and is expected to reach USD 237.87 billion by 2031.

Ans: Some of the major key players in the Anti-counterfeit packaging market are 3M Company, SAVI Technology, Authentix Inc, Zebra Technologies Corporation, Applied DNA Science, CCL Industries, Micro Tag Temed Ltd, EDGYN, Advance Track & Trace, and DuPont.

Ans: Increase in counterfeit activities globally is a major key driver for this market as many counterfeiting activities are happening globally.

Ans: North America Region is holding the highest market share followed by Asia Pacific Region and Europe.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Anti-counterfeit Packaging Market Segmentation, By Packaging Format

9.1 Introduction

9.2 Trend Analysis

9.3 Bottle & Jars

9.4 Blisters

9.5 Trays

9.6 Vials & Ampoules

9.7 Pouches & Sachets

9.8 Others

10. Anti-counterfeit Packaging Market Segmentation, By Technology

10.1 Introduction

10.2 Trend Analysis

10.3 RFID

10.4 Forensic Makers

10.5 Mass Encoding

10.6 Holograms

10.7 Tampers Evidence

10.8 Others

11. Anti-counterfeit Packaging Market Segmentation, By End Use

11.1 Introduction

11.2 Trend Analysis

11.3 Automotive

11.4 Pharmaceuticals

11.5 Personal Care

11.6 Luxury Goods

11.7 Food & Beverage

11.8 Electrical & Electronics

11.9 Others

12. Regional Analysis

12.1 Introduction

12.2 North America

12.2.1 Trend Analysis

12.2.2 North America Anti-counterfeit Packaging Market by Country

12.2.3 North America Anti-counterfeit Packaging Market By Packaging Format

12.2.4 North America Anti-counterfeit Packaging Market By Technology

12.2.5 North America Anti-counterfeit Packaging Market By End Use

12.2.6 USA

12.2.6.1 USA Anti-counterfeit Packaging Market By Packaging Format

12.2.6.2 USA Anti-counterfeit Packaging Market By Technology

12.2.6.3 USA Anti-counterfeit Packaging Market By End Use

12.2.7 Canada

12.2.7.1 Canada Anti-counterfeit Packaging Market By Packaging Format

12.2.7.2 Canada Anti-counterfeit Packaging Market By Technology

12.2.7.3 Canada Anti-counterfeit Packaging Market By End Use

12.2.8 Mexico

12.2.8.1 Mexico Anti-counterfeit Packaging Market By Packaging Format

12.2.8.2 Mexico Anti-counterfeit Packaging Market By Technology

12.2.8.3 Mexico Anti-counterfeit Packaging Market By End Use

12.3 Europe

12.3.1 Trend Analysis

12.3.2 Eastern Europe

12.3.2.1 Eastern Europe Anti-counterfeit Packaging Market by Country

12.3.2.2 Eastern Europe Anti-counterfeit Packaging Market By Packaging Format

12.3.2.3 Eastern Europe Anti-counterfeit Packaging Market By Technology

12.3.2.4 Eastern Europe Anti-counterfeit Packaging Market By End Use

12.3.2.5 Poland

12.3.2.5.1 Poland Anti-counterfeit Packaging Market By Packaging Format

12.3.2.5.2 Poland Anti-counterfeit Packaging Market By Technology

12.3.2.5.3 Poland Anti-counterfeit Packaging Market By End Use

12.3.2.6 Romania

12.3.2.6.1 Romania Anti-counterfeit Packaging Market By Packaging Format

12.3.2.6.2 Romania Anti-counterfeit Packaging Market By Technology

12.3.2.6.4 Romania Anti-counterfeit Packaging Market By End Use

12.3.2.7 Hungary

12.3.2.7.1 Hungary Anti-counterfeit Packaging Market By Packaging Format

12.3.2.7.2 Hungary Anti-counterfeit Packaging Market By Technology

12.3.2.7.3 Hungary Anti-counterfeit Packaging Market By End Use

12.3.2.8 Turkey

12.3.2.8.1 Turkey Anti-counterfeit Packaging Market By Packaging Format

12.3.2.8.2 Turkey Anti-counterfeit Packaging Market By Technology

12.3.2.8.3 Turkey Anti-counterfeit Packaging Market By End Use

12.3.2.9 Rest of Eastern Europe

12.3.2.9.1 Rest of Eastern Europe Anti-counterfeit Packaging Market By Packaging Format

12.3.2.9.2 Rest of Eastern Europe Anti-counterfeit Packaging Market By Technology

12.3.2.9.3 Rest of Eastern Europe Anti-counterfeit Packaging Market By End Use

12.3.3 Western Europe

12.3.3.1 Western Europe Anti-counterfeit Packaging Market by Country

12.3.3.2 Western Europe Anti-counterfeit Packaging Market By Packaging Format

12.3.3.3 Western Europe Anti-counterfeit Packaging Market By Technology

12.3.3.4 Western Europe Anti-counterfeit Packaging Market By End Use

12.3.3.5 Germany

12.3.3.5.1 Germany Anti-counterfeit Packaging Market By Packaging Format

12.3.3.5.2 Germany Anti-counterfeit Packaging Market By Technology

12.3.3.5.3 Germany Anti-counterfeit Packaging Market By End Use

12.3.3.6 France

12.3.3.6.1 France Anti-counterfeit Packaging Market By Packaging Format

12.3.3.6.2 France Anti-counterfeit Packaging Market By Technology

12.3.3.6.3 France Anti-counterfeit Packaging Market By End Use

12.3.3.7 UK

12.3.3.7.1 UK Anti-counterfeit Packaging Market By Packaging Format

12.3.3.7.2 UK Anti-counterfeit Packaging Market By Technology

12.3.3.7.3 UK Anti-counterfeit Packaging Market By End Use

12.3.3.8 Italy

12.3.3.8.1 Italy Anti-counterfeit Packaging Market By Packaging Format

12.3.3.8.2 Italy Anti-counterfeit Packaging Market By Technology

12.3.3.8.3 Italy Anti-counterfeit Packaging Market By End Use

12.3.3.9 Spain

12.3.3.9.1 Spain Anti-counterfeit Packaging Market By Packaging Format

12.3.3.9.2 Spain Anti-counterfeit Packaging Market By Technology

12.3.3.9.3 Spain Anti-counterfeit Packaging Market By End Use

12.3.3.10 Netherlands

12.3.3.10.1 Netherlands Anti-counterfeit Packaging Market By Packaging Format

12.3.3.10.2 Netherlands Anti-counterfeit Packaging Market By Technology

12.3.3.10.3 Netherlands Anti-counterfeit Packaging Market By End Use

12.3.3.11 Switzerland

12.3.3.11.1 Switzerland Anti-counterfeit Packaging Market By Packaging Format

12.3.3.11.2 Switzerland Anti-counterfeit Packaging Market By Technology

12.3.3.11.3 Switzerland Anti-counterfeit Packaging Market By End Use

12.3.3.1.12 Austria

12.3.3.12.1 Austria Anti-counterfeit Packaging Market By Packaging Format

12.3.3.12.2 Austria Anti-counterfeit Packaging Market By Technology

12.3.3.12.3 Austria Anti-counterfeit Packaging Market By End Use

12.3.3.13 Rest of Western Europe

12.3.3.13.1 Rest of Western Europe Anti-counterfeit Packaging Market By Packaging Format

12.3.3.13.2 Rest of Western Europe Anti-counterfeit Packaging Market By Technology

12.3.3.13.3 Rest of Western Europe Anti-counterfeit Packaging Market By End Use

12.4 Asia-Pacific

12.4.1 Trend Analysis

12.4.2 Asia-Pacific Anti-counterfeit Packaging Market by Country

12.4.3 Asia-Pacific Anti-counterfeit Packaging Market By Packaging Format

12.4.4 Asia-Pacific Anti-counterfeit Packaging Market By Technology

12.4.5 Asia-Pacific Anti-counterfeit Packaging Market By End Use

12.4.6 China

12.4.6.1 China Anti-counterfeit Packaging Market By Packaging Format

12.4.6.2 China Anti-counterfeit Packaging Market By Technology

12.4.6.3 China Anti-counterfeit Packaging Market By End Use

12.4.7 India

12.4.7.1 India Anti-counterfeit Packaging Market By Packaging Format

12.4.7.2 India Anti-counterfeit Packaging Market By Technology

12.4.7.3 India Anti-counterfeit Packaging Market By End Use

12.4.8 Japan

12.4.8.1 Japan Anti-counterfeit Packaging Market By Packaging Format

12.4.8.2 Japan Anti-counterfeit Packaging Market By Technology

12.4.8.3 Japan Anti-counterfeit Packaging Market By End Use

12.4.9 South Korea

12.4.9.1 South Korea Anti-counterfeit Packaging Market By Packaging Format

12.4.9.2 South Korea Anti-counterfeit Packaging Market By Technology

12.4.9.3 South Korea Anti-counterfeit Packaging Market By End Use

12.4.10 Vietnam

12.4.10.1 Vietnam Anti-counterfeit Packaging Market By Packaging Format

12.4.10.2 Vietnam Anti-counterfeit Packaging Market By Technology

12.4.10.3 Vietnam Anti-counterfeit Packaging Market By End Use

12.4.11 Singapore

12.4.11.1 Singapore Anti-counterfeit Packaging Market By Packaging Format

12.4.11.2 Singapore Anti-counterfeit Packaging Market By Technology

12.4.11.3 Singapore Anti-counterfeit Packaging Market By End Use

12.4.12 Australia

12.4.12.1 Australia Anti-counterfeit Packaging Market By Packaging Format

12.4.12.2 Australia Anti-counterfeit Packaging Market By Technology

12.4.12.3 Australia Anti-counterfeit Packaging Market By End Use

12.4.13 Rest of Asia-Pacific

12.4.13.1 Rest of Asia-Pacific Anti-counterfeit Packaging Market By Packaging Format

12.4.13.2 Rest of Asia-Pacific Anti-counterfeit Packaging Market By Technology

12.4.13.3 Rest of Asia-Pacific Anti-counterfeit Packaging Market By End Use

12.5 Middle East & Africa

12.5.1 Trend Analysis

12.5.2 Middle East

12.5.2.1 Middle East Anti-counterfeit Packaging Market by Country

12.5.2.2 Middle East Anti-counterfeit Packaging Market By Packaging Format

12.5.2.3 Middle East Anti-counterfeit Packaging Market By Technology

12.5.2.4 Middle East Anti-counterfeit Packaging Market By End Use

12.5.2.5 UAE

12.5.2.5.1 UAE Anti-counterfeit Packaging Market By Packaging Format

12.5.2.5.2 UAE Anti-counterfeit Packaging Market By Technology

12.5.2.5.3 UAE Anti-counterfeit Packaging Market By End Use

12.5.2.6 Egypt

12.5.2.6.1 Egypt Anti-counterfeit Packaging Market By Packaging Format

12.5.2.6.2 Egypt Anti-counterfeit Packaging Market By Technology

12.5.2.6.3 Egypt Anti-counterfeit Packaging Market By End Use

12.5.2.7 Saudi Arabia

12.5.2.7.1 Saudi Arabia Anti-counterfeit Packaging Market By Packaging Format

12.5.2.7.2 Saudi Arabia Anti-counterfeit Packaging Market By Technology

12.5.2.7.3 Saudi Arabia Anti-counterfeit Packaging Market By End Use

12.5.2.8 Qatar

12.5.2.8.1 Qatar Anti-counterfeit Packaging Market By Packaging Format

12.5.2.8.2 Qatar Anti-counterfeit Packaging Market By Technology

12.5.2.8.3 Qatar Anti-counterfeit Packaging Market By End Use

12.5.2.9 Rest of Middle East

12.5.2.9.1 Rest of Middle East Anti-counterfeit Packaging Market By Packaging Format

12.5.2.9.2 Rest of Middle East Anti-counterfeit Packaging Market By Technology

12.5.2.9.3 Rest of Middle East Anti-counterfeit Packaging Market By End Use

12.5.3 Africa

12.5.3.1 Africa Anti-counterfeit Packaging Market by Country

12.5.3.2 Africa Anti-counterfeit Packaging Market By Packaging Format

12.5.3.3 Africa Anti-counterfeit Packaging Market By Technology

12.5.3.4 Africa Anti-counterfeit Packaging Market By End Use

12.5.3.5 Nigeria

12.5.3.5.1 Nigeria Anti-counterfeit Packaging Market By Packaging Format

12.5.3.5.2 Nigeria Anti-counterfeit Packaging Market By Technology

12.5.3.5.3 Nigeria Anti-counterfeit Packaging Market By End Use

12.5.3.6 South Africa

12.5.3.6.1 South Africa Anti-counterfeit Packaging Market By Packaging Format

12.5.3.6.2 South Africa Anti-counterfeit Packaging Market By Technology

12.5.3.6.3 South Africa Anti-counterfeit Packaging Market By End Use

12.5.3.7 Rest of Africa

12.5.3.7.1 Rest of Africa Anti-counterfeit Packaging Market By Packaging Format

12.5.3.7.2 Rest of Africa Anti-counterfeit Packaging Market By Technology

12.5.3.7.3 Rest of Africa Anti-counterfeit Packaging Market By End Use

12.6 Latin America

12.6.1 Trend Analysis

12.6.2 Latin America Anti-counterfeit Packaging Market by country

12.6.3 Latin America Anti-counterfeit Packaging Market By Packaging Format

12.6.4 Latin America Anti-counterfeit Packaging Market By Technology

12.6.5 Latin America Anti-counterfeit Packaging Market By End Use

12.6.6 Brazil

12.6.6.1 Brazil Anti-counterfeit Packaging Market By Packaging Format

12.6.6.2 Brazil Anti-counterfeit Packaging Market By Technology

12.6.6.3 Brazil Anti-counterfeit Packaging Market By End Use

12.6.7 Argentina

12.6.7.1 Argentina Anti-counterfeit Packaging Market By Packaging Format

12.6.7.2 Argentina Anti-counterfeit Packaging Market By Technology

12.6.7.3 Argentina Anti-counterfeit Packaging Market By End Use

12.6.8 Colombia

12.6.8.1 Colombia Anti-counterfeit Packaging Market By Packaging Format

12.6.8.2 Colombia Anti-counterfeit Packaging Market By Technology

12.6.8.3 Colombia Anti-counterfeit Packaging Market By End Use

12.6.9 Rest of Latin America

12.6.9.1 Rest of Latin America Anti-counterfeit Packaging Market By Packaging Format

12.6.9.2 Rest of Latin America Anti-counterfeit Packaging Market By Technology

12.6.9.3 Rest of Latin America Anti-counterfeit Packaging Market By End Use

13. Company Profiles

13.1 Zebra Technologies Corporation

13.1.1 Company Overview

13.1.2 Financial

13.1.3 Products/ Services Offered

13.1.4 SWOT Analysis

13.1.5 The SNS View

13.2 3M Company

13.2.1 Company Overview

13.2.2 Financial

13.2.3 Products/ Services Offered

13.2.4 SWOT Analysis

13.2.5 The SNS View

13.3 SAVI Technology

13.3.1 Company Overview

13.3.2 Financial

13.3.3 Products/ Services Offered

13.3.4 SWOT Analysis

13.3.5 The SNS View

13.4 EDGYN

13.4.1 Company Overview

13.4.2 Financial

13.4.3 Products/ Services Offered

13.4.4 SWOT Analysis

13.4.5 The SNS View

13.5 Authentix Inc

13.5.1 Company Overview

13.5.2 Financial

13.5.3 Products/ Services Offered

13.5.4 SWOT Analysis

13.5.5 The SNS View

13.6 Applied DNA Science

13.6.1 Company Overview

13.6.2 Financial

13.6.3 Products/ Services Offered

13.6.4 SWOT Analysis

13.6.5 The SNS View

13.7 CCL Industries

13.7.1 Company Overview

13.7.2 Financial

13.7.3 Products/ Services Offered

13.7.4 SWOT Analysis

13.7.5 The SNS View

13.8 Micro Tag Temed Ltd

13.8.1 Company Overview

13.8.2 Financial

13.8.3 Products/ Services Offered

13.8.4 SWOT Analysis

13.8.5 The SNS View

13.9 Advance Track & Trace

13.9.1 Company Overview

13.9.2 Financial

13.9.3 Products/ Services Offered

13.9.4 SWOT Analysis

13.9.5 The SNS View

13.10 DuPont

13.10.1 Company Overview

13.10.2 Financial

13.10.3 Products/ Services Offered

13.10.4 SWOT Analysis

13.10.5 The SNS View

14. Competitive Landscape

14.1 Competitive Benchmarking

14.2 Market Share Analysis

14.3 Recent Developments

14.3.1 Industry News

14.3.2 Company News

14.3.3 Mergers & Acquisitions

15. Use Case and Best Practices

16. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Packaging Tape Printing Market was USD 18.3 Billion by 2023 and expected to reach at USD 30.60 Billion by 2032 and grow at a CAGR of 5.89% by 2024-2032.

The Plastic Caps & Closures Market size was USD 49.01 billion in 2023 and is expected to Reach USD 75.29 billion by 2031 and grow at a CAGR of 5.5 % over the forecast period of 2024-2031.

The Self-healing Concrete Market Size was valued at USD 88.85 Billion in 2023 and is expected to reach USD 1612.76 Billion by 2032 and grow at a CAGR of 38% over the forecast period 2024-2032.

The Paper Straw Market size was USD 2 billion in 2023 and is expected to Reach USD 10.99 billion by 2031 and grow at a CAGR of 20.85% over the forecast period of 2024-2031.

The Edible Water Bottles Market Size was valued at USD 128.12 million in 2023 and is expected to reach USD 283.75 million by 2031 and grow at a CAGR of 10.45% over the forecast period 2024-2031

The Shoe Packaging Market size was USD 6.44 billion in 2023 and is expected to Reach USD 8.49 billion by 2031 and grow at a CAGR of 3.51 % over the forecast period of 2024-2031.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd