Get More Information on Anesthesia Equipment Market - Request Sample Report

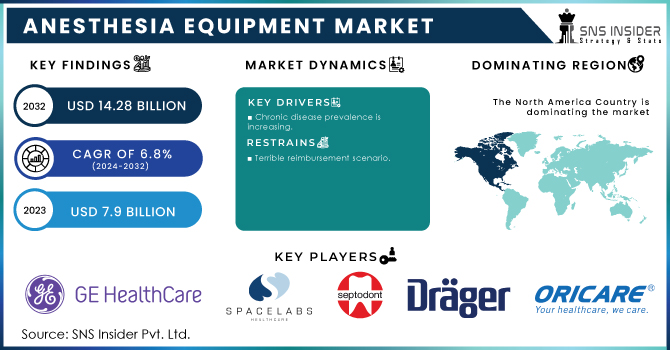

The Anesthesia Equipment Market size was estimated at USD 7.9 billion in 2023 and is expected to reach USD 14.28 billion by 2032 with a growing CAGR of 6.8% during the forecast period of 2024-2032.

The new research report consists of a market and industry trend analysis. The new research study includes industry trends, pricing analysis, patent analysis, conference and webinar materials, important stakeholders, and market purchasing behavior. This market's expansion can be traced mostly to the world's expanding senior population. Arthritis, osteoporosis, lumbar spinal stenosis (LSS), gastroesophageal reflux disease (GERD), and benign prostatic hypertrophy are all common age-related diseases and ailments. LSS is particularly frequent in adults over the age of 50, with the majority of patients in this age group requiring surgical operations to address it. According to the American Academy of Orthopaedic Surgeons (AAOS), around 2.4 million Americans will be impacted by this illness by 2021. As the senior population grows, the overall number of procedures performed in the United States is likely to rise.

As a result, the demand for respiratory equipment is increasing, promoting industry growth. Cigarette smoking is responsible for about 480,000 fatalities in the United States each year, according to CDC data published in June 2021. Secondhand smoke exposure was responsible for 41,000 of these deaths. The rising cost of building healthcare facilities in developing countries is likely to drive up demand for anesthetic and respiratory equipment. Because of the growing number of respiratory ailments and traffic accidents, the industry value of anesthesia and respiratory equipment will continue to rise. Long-term market expansion will also be encouraged by the growing attention of major firms to technological advancements. A lack of technological resources in low- and middle-income countries will stymie the industry's expansion.

DRIVERS

Chronic disease prevalence is increasing.

RESTRAIN

Terrible reimbursement scenario

Currently, developing countries' healthcare systems face numerous issues as a result of rising healthcare expenses, an increase in the frequency of chronic diseases, and an aging population (combined with an increase in age-related disorders). To address these difficulties, governments in several nations are overhauling their healthcare reimbursement systems. Except in Japan, reimbursement is extremely restricted or nonexistent in Asian countries. As a result, low or decreasing reimbursement rates in developed nations and unclear payment regulations in emerging countries hinder the global adoption of surgical operations. As a result, demand for anesthetic equipment will be constrained during the predicted period.

OPPORTUNITY

Rapid expansion in poor countries.

CHALLENGES

Budget cuts in hospitals.

Changes in regulatory rules in large markets such as the United States have had a substantial impact on hospital finances in recent years. The Affordable Care Act (ACA), which went into effect in the United States in 2010, brought stiffer federal rules, requiring many hospitals to reduce their capital spending budgets. Similar budgetary cuts are being noticed in hospitals throughout Europe, owing mostly to the recent economic recession. As a result of such budget cuts, many hospitals are unable to acquire expensive medical gadgets and instead choose lower-cost alternatives (such as used devices) or upgrade existing medical equipment and devices. Hospital funding in the United States has been severely slashed. According to an American Hospital Association analysis, government funding cuts to hospitals will total USD 218 billion by 2028, causing institutions to allocate fewer resources on an annual basis.

Emphasis on Emergency Medicine During times of conflict, healthcare resources may be diverted to emergency medical care, trauma treatment, and other pressing needs. This could move the focus away from elective operations that require anesthetic equipment. Global Collaborations and Partnerships Collaborations and partnerships in the healthcare sector may be impacted based on the stance of various countries and international organizations. This could have an influence on the flow of anesthetic equipment-related information, expertise, and resources. Remote Consultations and Telemedicine If conflict-related causes restrict physical access to healthcare institutions, telemedicine and online consultations may become more important. This could affect how anesthetic consultations are conducted as well as the demand for specific types of anesthesia equipment.

IMPACT OF ONGOING RECESSION

Market for Used Equipment In times of economic instability, healthcare facilities may consider purchasing used or refurbished equipment instead of investing in new equipment as a cost-cutting option. This could have an effect on the sales of new anesthetic equipment. Disruptions in the Supply Chain Disruptions in global supply chains caused by the recession might have an impact on the manufacture and distribution of anesthetic equipment. Equipment availability may be impacted by component shortages or production delays. Anesthesia equipment manufacturers may encounter issues due to decreased demand, affecting their revenues. This could result in adjustments to their pricing strategy, customer assistance, or even the possible consolidation of market companies.Cancer is the biggest cause of mortality worldwide, with an anticipated 10 million deaths in 2020, according to the WHO.According to Cancer Research UK, 27.5 million new cancer cases will be reported in 2040, a 61.7% rise from 2018. In 2020, Africa, Asia, Latin America, and the Caribbean accounted for 62.6% of new cancer diagnoses, while the same regions also accounted for 72.6% of global cancer fatalities. The rising cancer burden can be attributable to a variety of variables, including population increase and aging, as well as changes in the prevalence of certain cancer causes associated with social and economic development. Based on these figures, basic and translational cancer research remains critical.

By Type

Anesthesia Devices

Anesthesia Workstation

Anesthesia Delivery Machines

Anesthesia Ventilators

Other Devices

Anesthesia Disposables

Anesthesia Circuits (Breathing Circuits)

Anesthesia Masks

Endotracheal Tubes (ETTS)

Laryngeal Mask Airways (LMAS)

Other Accessories

By Application

Orthopedics

Neurology

Urology

Cardiology

Others

By End User

Hospitals

Clinics

Other End User

REGIONAL ANALYSES

Throughout the forecast period, North America is expected to outperform the rest of the world. The United States has the largest share of the pie in North America, owing to the rapid increase in the number of illnesses, such as obesity, cardiovascular issues, and various types of malignant growths, which has contributed to the rise in the number of medical procedures, both open and minimally intrusive. The increase in the number of minimally invasive medical methods for persistent infections has aided the US industry. In the United States, the number of ailments such as cancer and cardiovascular disease is rapidly increasing.

Do You Need any Customization Research on Anesthesia Equipment Market - Enquire Now

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

The major players are GE Healthcare, Spacelabs Healthcare, Septodont Inc, Draegerwerk AG & Co. KGaA, Beijing Aeonmed Co., Ltd., HEYER Medical AG, ORICARE, Inc,Philips Healthcare, Becton Dickinson and Company, Getinge AB, 3M, General Electric, SunMed, Teleflex Incorporated, Ambu A/S and others.

Fisher & Paykel Healthcare Corporation: In 2022, Fisher & Paykel Healthcare Corporation Limited introduced two new devices designed exclusively for anesthetic applications. Following several years of research and development, the company launched the Optiflow Switch and Optiflow Trace nasal high-flow interface devices in select countries.

Mindray: In 2022, The A8 and A9 anesthetic workstations were introduced by Mindray. They are innovative platforms that raise the bar for classical anesthesia in the perioperative setting.

| Report Attributes | Details |

| Market Size in 2023 | US$ 7.9 Bn |

| Market Size by 2032 | US$ 14.28 Bn |

| CAGR | CAGR of 6.8% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Anesthesia Devices, Anesthesia Workstation, Anesthesia Delivery Machines, Anesthesia Ventilators, Anesthesia Monitors, Other Devices, Anesthesia Disposables, Anesthesia Circuits (Breathing Circuits), Anesthesia Masks, Endotracheal Tubes (ETTS), Laryngeal Mask Airways (LMAS), Other Accessories) • By Application (Orthopedics, Neurology, Respiratory Care, Urology, Cardiology, Others) • By End User (Hospitals, Clinics, Ambulatory Surgical Centers, Other End Users) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]). Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles | GE Healthcare, Spacelabs Healthcare., Septodont Inc, Draegerwerk AG & Co. KGaA, Beijing Aeonmed Co., Ltd. HEYER Medical AG, ORICARE, Inc,Philips Healthcare, Becton Dickinson and Company, Getinge AB, 3M, General Electric, SunMed, Teleflex Incorporated, Ambu A/S |

| Key Drivers | • Chronic disease prevalence is increasing. |

| Market Restraints | • Terrible reimbursement scenario |

Ans: The Anesthesia Equipment Market is expected to grow at 6.8% CAGR from 2024 to 2032.

Ans: According to our analysis, the Anesthesia Equipment Market is anticipated to reach USD 14.28 billion By 2032.

Ans: The leading participants in the,GE Healthcare, Spacelabs Healthcare., Septodont Inc, Draegerwerk AG & Co. KGaA, Beijing Aeonmed Co., Ltd. HEYER Medical AG, ORICARE, Inc,Philips Healthcare, Becton Dickinson and Company.

Ans: Market players increasing organic and inorganic expansion tactics, such as new launches and alliances, are likely to fuel market growth throughout the forecast period.

Ans: Yes, you may request customization based on your company's needs.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Research Methodology

3. Market Dynamics

3.1 Drivers

3.2 Restraints

3.3 Opportunities

3.4 Challenges

4. Impact Analysis

4.1 Impact of the Ukraine- Russia war

4.2 Impact of ongoing Recession

4.2.1 Introduction

4.2.2 Impact on major economies

4.2.2.1 US

4.2.2.2 Canada

4.2.2.3 Germany

4.2.2.4 France

4.2.2.5 United Kingdom

4.2.2.6 China

4.2.2.7 Japan

4.2.2.8 South Korea

4.2.2.9 Rest of the World

5. Value Chain Analysis

6. Porter’s 5 forces model

7. PEST Analysis

8. Anesthesia Equipment Market,By Type

8.1 Anesthesia Devices

8.2 Anesthesia Workstation

8.3 Anesthesia Delivery Machines

8.4 Anesthesia Ventilators

8.5 Anesthesia Monitors

8.6 Other Devices

8.7 Anesthesia Disposables

8.8 Anesthesia Circuits (Breathing Circuits)

8.9 Anesthesia Masks

8.10 Endotracheal Tubes (ETTS)

8.11 Laryngeal Mask Airways (LMAS)

8.12 Other Accessories

9. Anesthesia Equipment Market, By Application

9.1 Orthopedics

9.2 Neurology

9.3 Respiratory Care

9.4 Urology

9.5 Cardiology

9.6 Others

10. Anesthesia Equipment Market, By End User

10. 1Hospitals

10.2 Clinics

10.3 Ambulatory Surgical Centers

10.4 Other End Users

11. Regional Analysis

11.1 Introduction

11.2 North America

11.2.1 North America Anesthesia Equipment Market by country

11.2.2North America Anesthesia Equipment Market by Type

11.2.3 North America Anesthesia Equipment Market by Application

11.2.4 North America Anesthesia Equipment Market by End-user

11.2.5 USA

11.2.5.1 USA Anesthesia Equipment Market by Type

11.2.5.2 USA Anesthesia Equipment Market by Application

11.2.5.3 USA Anesthesia Equipment Market by End-user

11.2.6 Canada

11.2.6.1 Canada Anesthesia Equipment Market by Type

11.2.6.2 Canada Anesthesia Equipment Market by Application

11.2.6.3 Canada Anesthesia Equipment Market by End-user

11.2.7 Mexico

11.2.7.1 Mexico Anesthesia Equipment Market by Type

11.2.7.2 Mexico Anesthesia Equipment Market by Application

11.2.7.3 Mexico Anesthesia Equipment Market by End-user

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Eastern Europe Anesthesia Equipment Market by country

11.3.1.2 Eastern Europe Anesthesia Equipment Market by Type

11.3.1.3 Eastern Europe Anesthesia Equipment Market by Application

11.3.1.4 Eastern Europe Anesthesia Equipment Market by End-user

11.3.1.5 Poland

11.3.1.5.1 Poland Anesthesia Equipment Market by Type

11.3.1.5.2 Poland Anesthesia Equipment Market by Application

11.3.1.5.3 Poland Anesthesia Equipment Market by End-user

11.3.1.6 Romania

11.3.1.6.1 Romania Anesthesia Equipment Market by Type

11.3.1.6.2 Romania Anesthesia Equipment Market by Application

11.3.1.6.4 Romania Anesthesia Equipment Market by End-user

11.3.1.7 Turkey

11.3.1.7.1 Turkey Anesthesia Equipment Market by Type

11.3.1.7.2 Turkey Anesthesia Equipment Market by Application

11.3.1.7.3 Turkey Anesthesia Equipment Market by End-user

11.3.1.8 Rest of Eastern Europe

11.3.1.8.1 Rest of Eastern Europe Anesthesia Equipment Market by Type

11.3.1.8.2 Rest of Eastern Europe Anesthesia Equipment Market by Application

11.3.1.8.3 Rest of Eastern Europe Anesthesia Equipment Market by End-user

11.3.2 Western Europe

11.3.2.1 Western Europe Anesthesia Equipment Market by Type

11.3.2.2 Western Europe Anesthesia Equipment Market by Application

11.3.2.3 Western Europe Anesthesia Equipment Market by End-user

11.3.2.4 Germany

11.3.2.4.1 Germany Anesthesia Equipment Market by Type

11.3.2.4.2 Germany Anesthesia Equipment Market by Application

11.3.2.4.3 Germany Anesthesia Equipment Market by End-user

11.3.2.5 France

11.3.2.5.1 France Anesthesia Equipment Market by Type

11.3.2.5.2 France Anesthesia Equipment Market by Application

11.3.2.5.3 France Anesthesia Equipment Market by End-user

11.3.2.6 UK

11.3.2.6.1 UK Anesthesia Equipment Market by Type

11.3.2.6.2 UK Anesthesia Equipment Market by Application

11.3.2.6.3 UK Anesthesia Equipment Market by End-user

11.3.2.7 Italy

11.3.2.7.1 Italy Anesthesia Equipment Market by Type

11.3.2.7.2 Italy Anesthesia Equipment Market by Application

11.3.2.7.3 Italy Anesthesia Equipment Market by End-user

11.3.2.8 Spain

11.3.2.8.1 Spain Anesthesia Equipment Market by Type

11.3.2.8.2 Spain Anesthesia Equipment Market by Application

11.3.2.8.3 Spain Anesthesia Equipment Market by End-user

11.3.2.9 Netherlands

11.3.2.9.1 Netherlands Anesthesia Equipment Market by Type

11.3.2.9.2 Netherlands Anesthesia Equipment Market by Application

11.3.2.9.3 Netherlands Anesthesia Equipment Market by End-user

11.3.2.10 Switzerland

11.3.2.10.1 Switzerland Anesthesia Equipment Market by Type

11.3.2.10.2 Switzerland Anesthesia Equipment Market by Application

11.3.2.10.3 Switzerland Anesthesia Equipment Market by End-user

11.3.2.11.1 Austria

11.3.2.11.2 Austria Anesthesia Equipment Market by Type

11.3.2.11.3 Austria Anesthesia Equipment Market by Application

11.3.2.11.4 Austria Anesthesia Equipment Market by End-user

11.3.2.12 Rest of Western Europe

11.3.2.12.1 Rest of Western Europe Anesthesia Equipment Market by Type

11.3.2.12.2 Rest of Western Europe Anesthesia Equipment Market by Application

11.3.2.12.3 Rest of Western Europe Anesthesia Equipment Market by End-user

11.4 Asia-Pacific

11.4.1 Asia-Pacific Anesthesia Equipment Market by country

11.4.2 Asia-Pacific Anesthesia Equipment Market by Type

11.4.3 Asia-Pacific Anesthesia Equipment Market by Application

11.4.4 Asia-Pacific Anesthesia Equipment Market by End-user

11.4.5 China

11.4.5.1 China Anesthesia Equipment Market by Type

11.4.5.2 China Anesthesia Equipment Market by Application

11.4.5.3 China Anesthesia Equipment Market End-user

11.4.6 India

11.4.6.1 India Anesthesia Equipment Market by Type

11.4.6.2 India Anesthesia Equipment Market by Application

11.4.6.3 India Anesthesia Equipment Market by End-user

11.4.7 Japan

11.4.7.1 Japan Anesthesia Equipment Market by Type

11.4.7.2 Japan Anesthesia Equipment Market by Application

11.4.7.3 Japan Anesthesia Equipment Market by End-user

11.4.8 South Korea

11.4.8.1 South Korea Anesthesia Equipment Market by Type

11.4.8.2 South Korea Anesthesia Equipment Market by Application

11.4.8.3 South Korea Anesthesia Equipment Market by End-user

11.4.9 Vietnam

11.4.9.1 Vietnam Anesthesia Equipment Market by Type

11.4.9.2 Vietnam Anesthesia Equipment Market by Application

11.4.9.3 Vietnam Anesthesia Equipment Market by End-user

11.4.10 Singapore

11.4.10.1 Singapore Anesthesia Equipment Market by Type

11.4.10.2 Singapore Anesthesia Equipment Market by Application

11.4.10.3 Singapore Anesthesia Equipment Market by End-user

11.4.11 Australia

11.4.11.1 Australia Anesthesia Equipment Market by Type

11.4.11.2 Australia Anesthesia Equipment Market by Application

11.4.11.3 Australia Anesthesia Equipment Market by End-user

11.4.12 Rest of Asia-Pacific

11.4.12.1 Rest of Asia-Pacific Anesthesia Equipment Market by Type

11.4.12.2 Rest of Asia-Pacific Anesthesia Equipment Market by Application

11.4.12.3 Rest of Asia-Pacific Anesthesia Equipment Market by End-user

11.5 Middle East & Africa

11.5.1 Middle East

11.5.1.1 Middle East Anesthesia Equipment Market by country

11.5.1.2 Middle East Anesthesia Equipment Market by Type

11.5.1.3 Middle East Anesthesia Equipment Market by Application

11.5.1.4 Middle East Anesthesia Equipment Market by End-user

11.5.1.5 UAE

11.5.1.5.1 UAE Anesthesia Equipment Market by Type

11.5.1.5.2 UAE Anesthesia Equipment Market by Application

11.5.1.5.3 UAE Anesthesia Equipment Market by End-user

11.5.1.6 Egypt

11.5.1.6.1 Egypt Anesthesia Equipment Market by Type

11.5.1.6.2 Egypt Anesthesia Equipment Market by Application

11.5.1.6.3 Egypt Anesthesia Equipment Market by End-user

11.5.1.7 Saudi Arabia

11.5.1.7.1 Saudi Arabia Anesthesia Equipment Market by Type

11.5.1.7.2 Saudi Arabia Anesthesia Equipment Market by Application

11.5.1.7.3 Saudi Arabia Anesthesia Equipment Market by End-user

11.5.1.8 Qatar

11.5.1.8.1 Qatar Anesthesia Equipment Market by Type

11.5.1.8.2 Qatar Anesthesia Equipment Market by Application

11.5.1.8.3 Qatar Anesthesia Equipment Market by End-user

11.5.1.9 Rest of Middle East

11.5.1.9.1 Rest of Middle East Anesthesia Equipment Market by Type

11.5.1.9.2 Rest of Middle East Anesthesia Equipment Market by Application

11.5.1.9.3 Rest of Middle East Anesthesia Equipment Market by End-user

11.5.2 Africa

11.5.2.1 Africa Anesthesia Equipment Market by country

11.5.2.2 Africa Anesthesia Equipment Market by Type

11.5.2.3 Africa Anesthesia Equipment Market by Application

11.5.2.4 Africa Anesthesia Equipment Market by End-user

11.5.2.5 Nigeria

11.5.2.5.1 Nigeria Anesthesia Equipment Market by Type

11.5.2.5.2 Nigeria Anesthesia Equipment Market by Application

11.5.2.5.3 Nigeria Anesthesia Equipment Market by End-user

11.5.2.6 South Africa

11.5.2.6.1 South Africa Anesthesia Equipment Market by Type

11.5.2.6.2 South Africa Anesthesia Equipment Market by Application

11.5.2.6.3 South Africa Anesthesia Equipment Market by End-user

11.5.2.7 Rest of Africa

11.5.2.7.1 Rest of Africa Anesthesia Equipment Market by Type

11.5.2.7.2 Rest of Africa Anesthesia Equipment Market by Application

11.5.2.7.3 Rest of Africa Anesthesia Equipment Market by End-user

11.6 Latin America

11.6.1 Latin America Anesthesia Equipment Market by country

11.6.2 Latin America Anesthesia Equipment Market by Type

11.6.3 Latin America Anesthesia Equipment Market by Application

11.6.4 Latin America Anesthesia Equipment Market by End-user

11.6.5 Brazil

11.6.5.1 Brazil America Wheelchair by Type

11.6.5.2 Brazil America Wheelchair by Application

11.6.5.3 Brazil America Wheelchair by End-user

11.6.6 Argentina

11.6.6.1 Argentina America Wheelchair by Type

11.6.6.2 Argentina America Wheelchair by Application

11.6.6.3 Argentina America Wheelchair by End-user

11.6.7 Colombia

11.6.7.1 Colombia America Wheelchair by Type

11.6.7.2 Colombia America Wheelchair by Application

11.6.7.3 Colombia America Wheelchair by End-user

11.6.8 Rest of Latin America

11.6.8.1 Rest of Latin America Wheelchair by Type

11.6.8.2 Rest of Latin America Wheelchair by Application

11.6.8.3 Rest of Latin America Wheelchair by End-user

12. Company profile

12.1 GE Healthcare.

12.1.1 Company Overview

12.1.2 Financials

12.1.3 Product/Services/Offerings

12.1.4 SWOT Analysis

12.1.5 The SNS View

12.2 Spacelabs Healthcare.

12.2.1 Company Overview

12.2.2 Financials

12.2.3 Product/Services/Offerings

12.2.4 SWOT Analysis

12.2.5 The SNS View

12.3 , Septodont Inc.

12.3.1 Company Overview

12.3.2 Financials

12.3.3 Product/Services/Offerings

12.3.4 SWOT Analysis

12.3.5 The SNS View

12.4 Draegerwerk AG & Co. KGaA.

12.4.1 Company Overview

12.4.2 Financials

12.4.3 Product/Services/Offerings

12.4.4 SWOT Analysis

12.4.5 The SNS View

12.5 Beijing Aeonmed Co., Ltd.

12.5.1 Company Overview

12.5.2 Financials

12.5.3 Product/Services/Offerings

12.5.4 SWOT Analysis

12.5.5 The SNS View

12.6 HEYER Medical AG.

12.6.1 Company Overview

12.6.2 Financials

12.6.3 Product/Services/Offerings

12.6.4 SWOT Analysis

12.6.5 The SNS View

12.7 ORICARE, Inc.

12.7.1 Company Overview

12.7.2 Financials

12.7.3 Product/Services/Offerings

12.7.4 SWOT Analysis

12.7.5 The SNS View

12.8 Philips Healthcare.

12.8.2 Financials

12.8.3 Product/Services/Offerings

12.8.4 SWOT Analysis

12.8.5 The SNS View

12.9 Becton Dickinson and Company.

12.9.1 Company Overview

12.9.2 Financials

12.9.3 Product/Services/Offerings

12.9.4 SWOT Analysis

12.9.5 The SNS View

12.10 Getinge AB.

12.10.1 Company Overview

12.10.2 Financials

12.10.3 Product/Services/Offerings

12.10.4 SWOT Analysis

12.10.5 The SNS View

13. Competitive Landscape

13.1 Competitive Bench marking

13.2 Market Share Analysis

13.3 Recent Developments

13.3.1 Industry News

13.3.2 Company News

13.3.3 Mergers & Acquisitions

14. Use Case and Best Practices

15. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Pancreatic and Biliary Stents Market was valued at USD 354.2 Mn in 2023 and is expected to reach 511.47 Mn in 2031, and grow at a CAGR of 4.7% over the forecast period of 2024-2031.

The Single-Use Bioreactors Market Size was valued at USD 3872.40 million in 2023 and is expected to reach USD 13784.83 million by 2031 and grow at a CAGR of 17.2% over the forecast period 2024-2031.

The Gene Therapy Market Size was valued at USD 9.2 Billion in 2023, and is expected to reach USD 54.39 Billion by 2032, and grow at a CAGR of 23.12%.

The Colorectal Cancer Screening Market size was valued at USD 15.36 billion in 2023 and is expected to reach USD 27.83 billion by 2032, growing at a CAGR of 6.85% from 2024-2032.

The Molecular Biology Enzymes, Reagents, and Kits Market was valued at USD 23.01 billion in 2023 and is expected to reach USD 52.78 billion by 2032, growing at a CAGR of 9.68% over the forecast period of 2024-2032.

Veterinary Microchips Market Size was valued at USD 686.3 million in 2023 and is expected to reach USD 1637.41 million by 2032, growing at a CAGR of 10.16% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd