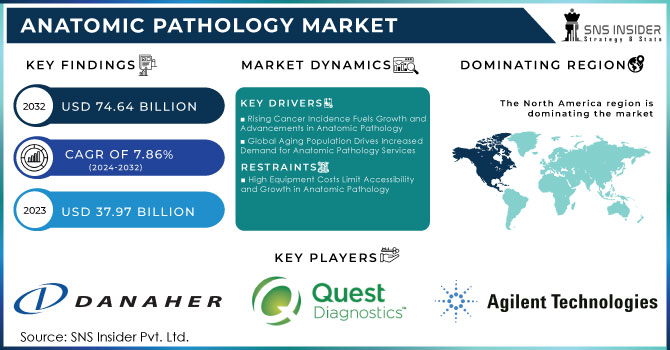

The Anatomic Pathology Market Size was valued at USD 37.97 billion in 2023 and is expected to reach USD 74.64 billion by 2032, growing at a CAGR of 7.86% from 2024-2032.

Get More Information on Anatomic Pathology Market - Request Sample Report

Anatomic pathology is growing rapidly because of the rising demand for advanced diagnostic techniques involving molecular pathology and personalized medicine. With 95% of clinical pathways being dependent upon access to pathology services, it becomes obvious how tissue analysis plays a critical role, especially when it is becoming progressively surmised that pathology will become more and more predominant in personalized treatments. This is again gigantic-500 million biochemistry and 130 million hematology tests per annum. As health care continues to shift to patient-centered care and an approach based on individual care, the increase in pathology is essential to maintain such advanced medical practices.

AI tools are speeding up diagnostics by boosting the accuracy of cancer cases and other complex diseases. More than 300,000 tests are conducted daily in the UK, and digital innovations are helping combat the volume. The global digital pathology market is expected to grow to USD 2.03 billion by 2027, and AI is greatly assisting in increasing accuracy while minimizing human error and optimizing workflow efficiency. This integration also leads to faster turnaround times and supports both healthcare providers and patients as 50 million lab reports are dispatched to GPs every year in the UK.

International efforts ensure that pathology services are enhanced in emerging markets and contribute to growth in this field. Another initiative that the CAP Foundation offers is the Global Pathology Development Grant. These grants are as much as USD 10,000 in funding for impactful global efforts. Another way improving global health is pushing pathology forward is in the increasing demand for advanced diagnostic services as healthcare systems in developing regions build. As many as 14 tests per year can be handled for the average citizen of England and Wales, and thus these expanded services underscore the important role pathology plays in contemporary healthcare locally and around the world.

DRIVERS

Rising Cancer Incidence Fuels Growth and Advancements in Anatomic Pathology

The primary source of expansion for the anatomic pathology lab is the upsurge in cancer cases. In 2022, there were approximately 20 million new instances of cancer, and by 2050, it is expected to surpass 35 million due to population growth. The highest number of cases are accounted for by lung cancer at 2.5 million, followed by female breast cancer at 2.3 million cases, and colorectal cancer at 1.9 million cases. This increased diagnosis of cancer necessitates more pathology labs to service the early detection and personalized treatment provisions. The anatomic pathology labs transform with advancements in technologies as they handle complex, larger volumes of tests for rapid and accurate diagnoses. Increasingly important, this growth is precisely aimed at bringing down the rising healthcare burden of cancer and other critical diseases across the globe.

Global Aging Population Drives Increased Demand for Anatomic Pathology Services

The worldwide aging population is a major demand driver of anatomic pathology services because of the rise in the related diseases to age, which includes: cancer, cardiovascular conditions, and neurological disorders. The proportion of those 65 and older will increase more than double, from around 761 million in 2021 to nearly 1.6 billion in 2050. Most of that growth will take place in regions such as Northern Africa, Western Asia, and sub-Saharan Africa. The demographic transition is further accelerating the prevalence of chronic diseases, such as cardiovascular diseases, which contributed to 19.8 million deaths in 2022. Anatomic pathology, therefore, plays an important role in early diagnosis and management of these diseases. As the elderly population increases, pathology labs are expanding to meet increased demand for precise diagnostic services more so in age-related diseases. This is an important trend, with advanced diagnostic tools now being very much the basis for how health is managed for an aging global population.

RESTRAINTS

High Equipment Costs Limit Accessibility and Growth in Anatomic Pathology

Advanced technology and equipment pose an important constraint on the anatomic pathology market. Diagnostic tools such as digital pathology systems, molecular diagnostics, and AI-driven solutions require significant investment. For instance, a digital pathology scanner can vary from USD 12,000 to USD 72,000; a biochemistry analyzer can cost anywhere in the range of USD 4,800 to USD 30,000. With a microscope and histopathology instruments costing great amounts of money too, these are huge upfront costs for most labs, which makes things even worse. Therefore, they cannot afford to buy these cutting-edge diagnostic facilities, thereby increasing the disparity between resource-rich and resource-poor labs.

BY APPLICATION

Disease diagnosis generated 58% of anatomic pathology market revenue in 2023, mainly due to the increasing demand to detect diseases early, which includes cancers, cardiovascular diseases, and infectious diseases. Such diseases need a microscopic view of tissues and biopsies that are mainly essential in diagnosing correctly. Increasing chronic disease prevalence has also made this the most important and massive segment of the pathology industry.

Drug discovery and development is anticipated to be growth-oriented with a CAGR of 8.88% in the forecast period from 2024 to 2032, led by the rising adoption of molecular pathology and genetic analysis which is a crucial part of drug target discovery, advancing precision medicine, and improving drug development processes. Such developments are furthering personalized and efficient therapeutic procedures, hence experiencing significant growth in this aspect.

BY PRODUCT

The consumables dominate in the anatomic pathology, which accounted for 69% of the market share in 2023 mainly due to a repeated requirement of reagents, slides, and staining kits. The consumables are required for regular day-to-day lab routines, making them sustain their demand in the pathology test. They are much less expensive than equipment and require repeated usage; hence, their percentage is very significant in the market.

Instruments are expected to grow at the highest CAGR of 8.98% from 2024 to 2032. Advancements in diagnostic technology such as digital pathology systems and high-throughput analyzers will be the driving factor in this segment. With an increasing demand for preciseness and automation by more pathology labs, the adoption of advanced instruments will be expedited and drive growth in the segment.

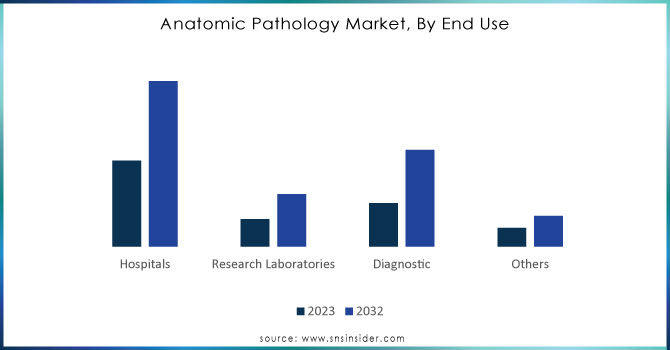

BY END USE

The anatomic pathology market was led by hospitals, with a share of 49% in 2023. The demand for high-volume procedure services is increasingly rising, especially in cancer diagnosis and complex disease management. It is primarily the hospitals that provide integrated diagnostic and treatment services, hence making them the core center for the pathology market.

The Diagnostic Laboratories segment is expected to witness the highest CAGR during the forecast period at 9.36%, with its growth being contributed by the increasing specialized diagnostic testing, growth in the laboratories services, and also increasing outpatient testing. Operational costs concerning diagnostic labs are lower when compared to hospitals. Therefore, several patients flocked to these diagnostic labs for precise and cost-effective diagnostic solutions.

Need Any Customization Research On Anatomic Pathology Market - Inquiry Now

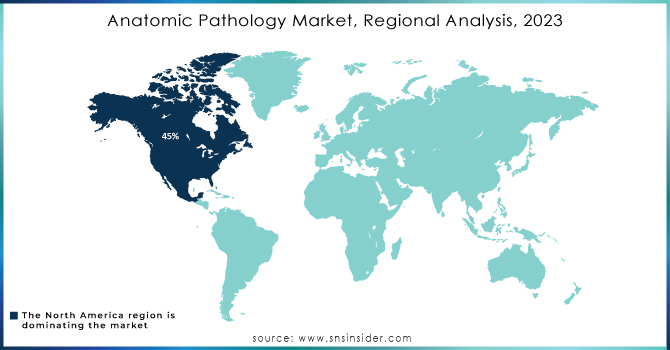

North America dominated the anatomic pathology market with 45% of revenue share in 2023, mainly due to its advanced healthcare system, high spending, and increasing necessity for diagnostic services. The requirement for proper diagnostic solution is critical as 1,958,310 new cancer cases and 609,820 cancer deaths are expected to occur in the U.S in 2023. The advanced medical infrastructure along with a high prevalence of diseases further cements its position in the pathology market.

Asia Pacific is likely to hold the highest CAGR of 8.52% during the forecast period from 2024 to 2032. The regional digital health market that touches a billion lives is on track to reach USD 100 billion by 2025 from USD 37 billion in 2020. Even so, its average Asian governments allocate only 4.5% of GDP to healthcare, much lower than the OECD average of 12%, thus capping the upside potential of healthcare growth. These factors combined with an aging population and growing awareness of disease contribute to the demand for anatomic pathology market in the region.

LATEST NEWS-

NYU Langone Health launched a digital pathology program in 2024, and it has phased out the old microscopes with high-definition images. This allows immediate sharing of these images across the hospital network, enhancing efficiency in the diseased diagnosis process.

In 2024, the Head of Pathology at Roche Diagnostics reported that the mission of Roche Diagnostics was to revolutionize cancer research by marrying their know-how in tissue diagnostics with cutting-edge AI innovations that will bring innovation to the field and shape the course of future cancer diagnostics and research.

Danaher Corporation (Leica Biosystems - Automated Slide Scanners, Tissue Stainers)

PHC Holdings Corporation (Epredia - Pathology Imaging Systems, Tissue Microarray Processors)

Quest Diagnostics (Ameripath - Molecular Diagnostic Kits, Cytology Reagents)

Laboratory Corporation of America Holdings (LabCorp Pathology - Immunohistochemistry Kits, Digital Pathology Software)

F. Hoffmann-La Roche AG (Ventana - Immunohistochemistry Stains, Automated Slide Stainers)

Agilent Technologies (SureScan - Digital Pathology Imaging, Nucleic Acid Extraction Kits)

Cardinal Health (Histology Lab Equipment, Diagnostic Reagents)

Sakura Finetek USA (Tissue Embedding Systems, Automated Slide Scanners)

NeoGenomics Laboratories (Genomic Testing Kits, Oncology Pathology Services)

BioGenex (Immunohistochemistry Reagents, Diagnostic Antibodies)

Mylan N.V. (Molecular Diagnostics Kits, Pathology Reagents)

Teva Pharmaceutical Industries (Oncology Pathology Services, Immunohistochemistry Reagents)

Sanofi (Cancer Diagnostic Kits, Pathology Testing Reagents)

Pfizer Inc. (Oncology Diagnostics, Biomarker Testing Reagents)

GlaxoSmithKline (Pathology Testing Kits, Cancer Biomarkers)

Novartis AG (Gene Expression Testing, Tumor Pathology Kits)

Bayer AG (Pathology Diagnostic Kits, Tumor Marker Assays)

Eli Lilly (Cancer Biomarker Testing, Molecular Diagnostics)

Merck & Co. (Pathology Testing Services, Genetic Testing Kits)

llergan (Cancer Diagnostics, Histology Staining Kits)

AstraZeneca (Oncology Pathology Kits, Diagnostic Antibodies)

Johnson & Johnson (Histology Lab Equipment, Molecular Diagnostic Solutions)

Cipla Inc. (Molecular Pathology Reagents, Cancer Diagnostics)

Bausch Health Companies (Histology Diagnostic Kits, Digital Pathology Solutions)

Abbott (Molecular Diagnostics, Cancer Detection Kits)

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 37.97 Billion |

| Market Size by 2032 | USD 76.64 Billion |

| CAGR | CAGR of 7.86% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product & Services (Instruments, Consumables, Services) • By Application (Disease Diagnosis, Drug Discovery and Development, Others) • By End-use (Hospitals, Research Laboratories, Diagnostic Laboratories, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Danaher Corporation, PHC Holdings Corporation, Quest Diagnostics, Laboratory Corporation of America Holdings, F. Hoffmann-La Roche AG, Agilent Technologies, Cardinal Health, Sakura Finetek USA, NeoGenomics Laboratories, BioGenex, Mylan N.V., Teva Pharmaceutical Industries, Sanofi, Pfizer Inc., GlaxoSmithKline, Novartis AG, Bayer AG, Eli Lilly, Merck & Co., Allergan, AstraZeneca, Johnson & Johnson, Cipla Inc., Bausch Health Companies, Abbott |

| Key Drivers | • Rising Cancer Incidence Fuels Growth and Advancements in Anatomic Pathology • Global Aging Population Drives Increased Demand for Anatomic Pathology Services |

| RESTRAINTS | • High Equipment Costs Limit Accessibility and Growth in Anatomic Pathology |

Ans: Anatomic Pathology Market, By was valued at USD 37.97 billion in 2023 and is expected to reach USD 74.64 billion by 2032, growing at a CAGR of 7.86% from 2024-2032.

Ans: AI boosts diagnostic accuracy, minimizes human error, and helps with faster test results and efficient workflows.

Ans: With millions of new cancer cases expected, more pathology labs are needed for early detection and treatment.

Ans: Asia Pacific is projected to grow at a CAGR of 8.52% due to an aging population and increasing healthcare demands, despite spending only 4.5% of GDP on healthcare.

Ans: Digital pathology scanners cost between $12,000 and $72,000, and biochemistry analyzers range from $4,800 to $30,000, creating a barrier to adoption in resource-poor settings.

Table of Contents:

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023)

5.2 Lab Growth, (2023), by Region

5.3 Test Volume, by region

5.4 Healthcare Spending: Expenditure data by government, insurers, and out-of-pocket by patients.

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and supply chain strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Anatomic Pathology Market Segmentation, by Product & Services

7.1 Chapter Overview

7.2 Instruments

7.2.1 Instruments Market Trends Analysis (2020-2032)

7.2.2 Instruments Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.3 Microtomes & Cryostat

7.2.3.1 Microtomes & Cryostat Market Trends Analysis (2020-2032)

7.2.3.2 Microtomes & Cryostat Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.4 Tissue Processors

7.2.4.1 Tissue Processors Market Trends Analysis (2020-2032)

7.2.4.2 Tissue Processors Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.5 Automatic Stainers

7.2.5.1 Automatic Stainers Market Trends Analysis (2020-2032)

7.2.5.2 Automatic Stainers Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.6 Other Products

7.2.6.1 Other Products Market Trends Analysis (2020-2032)

7.2.6.2 Other Products Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.7 Whole Slide Imaging (WSI) Scanners

7.2.7.1 Whole Slide Imaging (WSI) Scanners Market Trends Analysis (2020-2032)

7.2.7.2 Whole Slide Imaging (WSI) Scanners Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Consumables

7.3.1 Consumables Market Trends Analysis (2020-2032)

7.3.2 Consumables Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.3 Reagents & Antibodies

7.2.3.1 Reagents & Antibodies Market Trends Analysis (2020-2032)

7.2.3.2 Reagents & Antibodies Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.4 Probes & Kits

7.2.4.1 Probes & Kits Market Trends Analysis (2020-2032)

7.2.4.2 Probes & Kits Market Size Estimates and Forecasts to 2032 (USD Billion)

7.2.5 Others

7.2.5.1 Others Market Trends Analysis (2020-2032)

7.2.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Services

7.4.1 Services Market Trends Analysis (2020-2032)

7.4.2 Services Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Anatomic Pathology Market Segmentation, by Application

8.1 Chapter Overview

8.2 Disease Diagnosis

8.2.1 Disease Diagnosis Market Trends Analysis (2020-2032)

8.2.2 Disease Diagnosis Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Drug Discovery and Development

8.3.1 Drug Discovery and Development Market Trends Analysis (2020-2032)

8.3.2 Drug Discovery and Development Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Others

8.4.1 Others Market Trends Analysis (2020-2032)

8.4.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Anatomic Pathology Market Segmentation, by End User

9.1 Chapter Overview

9.2 Hospitals

9.2.1 Hospitals Market Trends Analysis (2020-2032)

9.2.2 Hospitals Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Research Laboratories

9.3.1 Research Laboratories Market Trends Analysis (2020-2032)

9.3.2 Research Laboratories Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Diagnostic Laboratories

9.4.1 Diagnostic Laboratories Market Trends Analysis (2020-2032)

9.4.2 Diagnostic Laboratories Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Others

9.5.1 Others Market Trends Analysis (2020-2032)

9.5.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Anatomic Pathology Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.2.4 North America Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.5 North America Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.2.6.2 USA Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.6.3 USA Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.2.7.2 Canada Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.7.3 Canada Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.2.8.2 Mexico Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.8.3 Mexico Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Anatomic Pathology Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.1.6.2 Poland Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.6.3 Poland Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.1.7.2 Romania Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.7.3 Romania Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Anatomic Pathology Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.4 Western Europe Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.5 Western Europe Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.6.2 Germany Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.6.3 Germany Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.7.2 France Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.7.3 France Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.8.2 UK Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.8.3 UK Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.9.2 Italy Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.9.3 Italy Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.10.2 Spain Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.10.3 Spain Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.13.2 Austria Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.13.3 Austria Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Anatomic Pathology Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia Pacific Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.4 Asia Pacific Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.5 Asia Pacific Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.6.2 China Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.6.3 China Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.7.2 India Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.7.3 India Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.8.2 Japan Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.8.3 Japan Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.9.2 South Korea Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.9.3 South Korea Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.10.2 Vietnam Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.10.3 Vietnam Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.11.2 Singapore Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.11.3 Singapore Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.12.2 Australia Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.12.3 Australia Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia Pacific Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia Pacific Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Anatomic Pathology Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.1.4 Middle East Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.5 Middle East Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.1.6.2 UAE Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.6.3 UAE Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Anatomic Pathology Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.2.4 Africa Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.5 Africa Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Anatomic Pathology Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.6.4 Latin America Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.5 Latin America Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.6.6.2 Brazil Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.6.3 Brazil Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.6.7.2 Argentina Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.7.3 Argentina Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.6.8.2 Colombia Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.8.3 Colombia Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Anatomic Pathology Market Estimates and Forecasts, by Product & Services (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Anatomic Pathology Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Anatomic Pathology Market Estimates and Forecasts, by End User (2020-2032) (USD Billion)

11. Company Profiles

11.1 Danaher Corporation

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 PHC Holdings Corporation

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Quest Diagnostics

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Agilent Technologies

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Cardinal Health

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 BioGenex

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Mylan N.V.

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Sanofi

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Novartis AG

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 Pfizer Inc.

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

By Product & Services

Instruments

Microtomes & Cryostat

Tissue Processors

Automatic Stainers

Whole Slide Imaging (WSI) Scanners

Other Products

Consumables

Reagents & Antibodies

Probes & Kits

Others

Services

By Application

Disease Diagnosis

Drug Discovery and Development

Others

By End-use

Hospitals

Research Laboratories

Diagnostic Laboratories

Others

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

Platelet Rich Plasma Market was valued at USD 0.75 billion in 2023 & is expected to reach USD 2.62 billion by 2032, growing at a CAGR of 14.98% from 2024-2032.

Long Read Sequencing Market was valued at USD 595.91 million in 2023 and is expected to reach USD 6977.05 million by 2032, growing at a CAGR of 31.53% from 2024-2032.

The Multi-Cancer Early Detection Market was valued at USD 1.07 billion in 2023 and is expected to reach USD 4.40 billion by 2032, growing at a CAGR of 17.04% over the forecast period of 2024-2032.

The Benign Prostatic Hyperplasia (BPH) Treatment Market Size was valued at USD 1.57 billion in 2023 and is expected to reach USD 3.38 billion by 2032 and grow at a CAGR of 8.92% over the forecast period 2024-2032.

The Personalized Medicine Market was valued at USD 530.01 billion in 2023, and is expected to reach USD 1,078.17 billion by 2032, and grow at a CAGR of 8.21% over the forecast period 2024-2032.

The Aerosol Drug Delivery Devices Market was valued at USD 26.4 billion in 2023 and is projected to reach USD 80.43 billion by 2032, growing at a 13.19% CAGR.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd