Get More Information on Anastomosis Devices Market - Request Sample Report

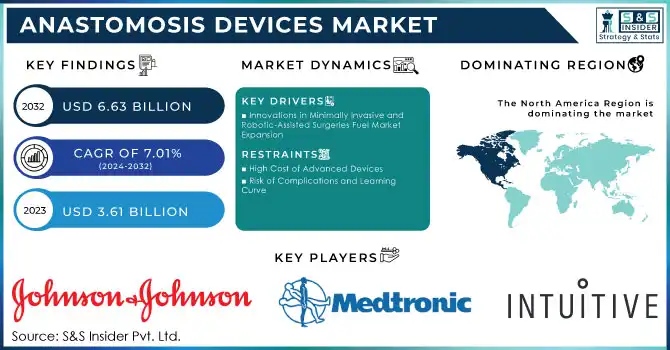

The Anastomosis Devices Market Size was valued at USD 3.61 billion in 2023 and is expected to reach USD 6.63 billion by 2032 and grow at a CAGR of 7.01% over the forecast period 2024-2032.

The anastomosis devices market is experiencing significant growth, propelled by the rising incidence of surgical cases and advances in surgical technologies. Cardiovascular disorders, a leading cause of mortality worldwide, necessitate precise and reliable surgical tools. According to the American Heart Association, over 523 million people globally are affected by cardiovascular diseases, emphasizing the critical need for advanced anastomosis devices in procedures like coronary artery bypass grafting. Similarly, the increasing prevalence of gastrointestinal disorders and the growing number of bariatric surgeries, driven by the obesity epidemic, are further bolstering demand for these devices. Accidental cases also play a significant role in driving the growth of the anastomosis devices market. Trauma-related injuries, such as severe abdominal or gastrointestinal injuries from accidents, often require surgical interventions involving anastomosis procedures. These accidents, which result in ruptured organs or complex internal injuries, necessitate the use of anastomosis devices to restore continuity to the digestive tract or vascular structures. As the number of road accidents, industrial accidents, and other trauma-related injuries rises globally, the demand for anastomosis devices also increases. The increasing prevalence of such incidents, particularly in regions with high accident rates, is expected to contribute to the expansion of the market, driving the adoption of advanced anastomosis technologies to improve patient outcomes and recovery times.

Innovations in anastomosis technology, such as magnetic compression devices and automated suturing systems, have revolutionized surgical practices. For instance, the FDA's recent breakthrough designation for magnetic anastomosis technology underscores its potential to enhance precision and reduce postoperative complications during gastrointestinal surgeries. Reports from Surgical Endoscopy highlight the significant benefits of robotic-assisted anastomosis procedures, including improved accuracy, reduced recovery times, and fewer complications, making them increasingly popular in clinical settings.

Additionally, organ transplantation surgeries, which require high precision during vascular and tissue anastomosis, are rising. Studies from the Organ Donation Alliance reveal that over 100,000 patients in the U.S. are on transplant waiting lists annually, showcasing the growing reliance on innovative surgical tools to improve outcomes. Devices such as the FDA-approved Viola clampless proximal anastomosis device have transformed vascular surgeries, eliminating the need for traditional clamping and reducing associated risks.

Minimally invasive surgical procedures have gained immense traction due to shorter recovery times and reduced patient trauma. Anastomosis devices are critical components in these procedures, making them indispensable in modern surgical practices. Continuous advancements in materials, such as bioabsorbable options, and the integration of robotic systems are expected to further elevate the standard of care, driving sustained growth in this market.

Drivers

Innovations in Minimally Invasive and Robotic-Assisted Surgeries Fuel Market Expansion

The anastomosis devices market is propelled by rising surgical needs across various medical fields, supported by advancements in technology and growing demand for minimally invasive procedures. According to recent data, cardiovascular surgeries account for over 30% of all surgical interventions globally, emphasizing the demand for reliable anastomosis solutions. In gastrointestinal surgery, the adoption of minimally invasive techniques has surged, with studies showing a 50% reduction in postoperative complications when advanced devices like automated suturing systems are utilized.

The increasing prevalence of obesity, affecting 13% of the global adult population, has driven a rise in bariatric surgeries, which rely on precise anastomosis techniques. Additionally, the need for organ transplantation is expanding, with over 100,000 annual transplants performed globally, requiring advanced vascular anastomosis devices to ensure successful outcomes.

Innovations like the Viola clampless proximal anastomosis device, which eliminates the need for traditional clamps, and FDA-approved magnetic compression devices highlight the market's technological progress. Robotic-assisted surgeries, supported by devices designed for enhanced dexterity and precision, are now employed in over 20% of complex surgical cases, according to Surgical Endoscopy.

Furthermore, advancements in bioabsorbable materials for anastomosis devices offer better patient safety and reduced long-term complications, aligning with the shift toward patient-centric healthcare. Collectively, these factors, combined with growing surgical case volumes, underline the dynamic growth and potential of the anastomosis devices market.

Restraints

High Cost of Advanced Devices

The premium pricing of innovative anastomosis devices, particularly robotic-assisted and bioabsorbable models, may limit their adoption, especially in cost-sensitive regions and healthcare systems.

Risk of Complications and Learning Curve

Despite technological advancements, the complexity of using sophisticated anastomosis devices requires specialized training and improper usage can lead to complications, hindering widespread acceptance in some surgical settings.

By Product

Disposable anastomosis devices were the dominant segment in 2023, accounting for a significant share of the market. These devices are favored for their convenience, reduced risk of cross-contamination, and the growing preference for single-use solutions in hospitals and surgical centers. As the global focus on infection control intensifies, the disposable segment's share of the market dominated by 60.0% in 2023. Their one-time-use nature ensures sterility, which is a major factor driving their preference for high-risk surgeries like cardiovascular and gastrointestinal procedures. Additionally, disposable devices are cost-effective for healthcare providers who avoid the costs associated with cleaning and sterilizing reusable instruments.

Reusable anastomosis devices are the fastest-growing segment, with an increasing number of healthcare facilities opting for these devices due to their long-term cost-effectiveness. The reusable segment is expected to see a growth rate of 10% annually. As medical facilities strive to reduce costs in the long term while maintaining high-quality outcomes, reusable devices offer a more sustainable solution, especially in established healthcare settings. The adoption of these devices is further supported by innovations in materials and designs that enhance their durability and ease of use. The growing trend towards environmentally conscious medical practices also supports the growth of the reusable segment, making it a key area of expansion.

By Application

Cardiovascular surgery was the dominant application segment in 2023, accounting for over 40.0% of the overall anastomosis devices market. The high prevalence of cardiovascular diseases, combined with the increasing number of cardiovascular surgical procedures globally, contributed significantly to this dominance. Cardiovascular surgeries such as coronary artery bypass grafting (CABG) and aortic surgeries demand reliable anastomosis solutions, driving the need for advanced devices. The growing adoption of minimally invasive and robotic-assisted cardiovascular procedures further boosts the demand for precise and efficient anastomosis devices in this field.

Gastrointestinal surgery emerged as the fastest-growing application segment, with a projected growth rate of 12% annually. This growth is largely attributed to the increasing number of bariatric surgeries, the rise in gastrointestinal diseases, and the widespread adoption of minimally invasive techniques in this field. As minimally invasive surgeries continue to gain traction, advanced anastomosis devices, such as automated suturing systems, play a critical role in improving outcomes and reducing postoperative complications. The increasing shift towards outpatient care and faster recovery times in gastrointestinal surgeries further enhance the demand for innovative anastomosis devices in this segment.

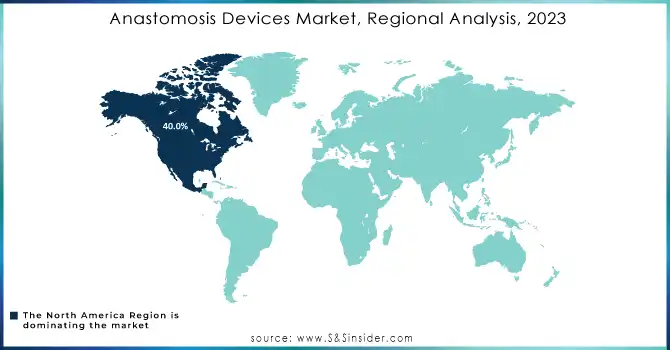

North America held the largest market share, accounting for over 40.0% of the global market in 2023. The dominance of this region can be attributed to the high prevalence of cardiovascular diseases, obesity, and gastrointestinal disorders, along with the advanced healthcare infrastructure and strong adoption of innovative technologies. The U.S. leads the market, supported by substantial investments in healthcare and ongoing innovations in anastomosis devices, including robotic-assisted surgery technologies.

Europe is the second-largest market, contributing around 30% to the global market. The region has seen a rising demand for advanced surgical procedures, particularly in the cardiovascular and gastrointestinal fields. Countries such as Germany, France, and the U.K. are investing in high-tech medical devices, which is propelling market growth. Additionally, Europe’s strong regulatory framework supports the use of safe and efficient anastomosis devices in surgeries.

Asia-Pacific (APAC) is the fastest-growing region, with a projected annual growth rate of 10%. The rapid increase in healthcare access, rising surgical case volumes, and growing awareness of advanced surgical techniques in countries like China, India, and Japan are key drivers. The region’s rising healthcare expenditure and the expanding middle-class population are expected to continue boosting demand for anastomosis devices.

Need Any Customization Research On Anastomosis Devices Market - Inquiry Now

Johnson & Johnson (Ethicon, Inc.) – Endo Stitch, Proximate, Intracorp Staplers

Medtronic Plc – HeartString Proximal Anastomosis System, Tri-Staple

B. Braun Melsungen – Gastrointestinal Suturing Devices, Vascular Anastomosis Devices

Intuitive Surgical Inc. – da Vinci Surgical Systems, EndoWrist Stapler

Artivion, Inc. – Cardio-PA, Artivion Anastomosis Systems

Mizuho Medical Co., Ltd (MIZUHO Corporation) – Vascular Anastomosis Devices

Getinge – Endo GIA Staplers, FlowSurgical Anastomosis System

Peters Surgical – Anastomosis Sutures, Surgical Staplers

Baxter – Vascular Anastomosis Devices, BioSuture Stapler

Vascular Graft Solutions Ltd. – Vascular Anastomosis Devices

Medline Industries, LP – Surgical Sutures, Anastomosis Staplers

Seger Surgical Solutions – Suturing Devices for Anastomosis

LivaNova PLC – Coronary Anastomosis Devices, Vascular Graft Solutions

MAQUET Holding – TA Staplers, Anastomosis Systems

Novare Surgical Systems – Surgical Suturing Devices, Anastomosis Kits

Vitalitec International – Vascular Anastomosis Devices, Surgical Suturing Systems

In Nov 2024, GI Windows Surgical raised USD 37 million to advance the clinical development and commercialization of its Flexagon self-forming magnet technology. The funding will support the continued development of the Flexagon system, which uses magnetic anastomosis to enable less invasive surgical procedures and aims to revolutionize tissue fusion and delivery systems in anastomosis technology.

In Sept 2024, GT Metabolic Solutions received FDA de novo clearance for its first-generation MagDI system, designed for side-to-side duodeno-ileal anastomosis. The system utilizes magnetic compression anastomosis to eliminate the need for bowel incisions, reduce technical variability, and avoid leaving foreign materials behind during minimally invasive procedures.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 3.61 billion |

| Market Size by 2032 | US$ 6.63 billion |

| CAGR | CAGR of 7.01% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Disposable, Reusable) • By Application (Cardiovascular surgery, Gastrointestinal surgery, Others) • By End-use (Hospitals, Ambulatory care centers and clinics) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Johnson & Johnson (Ethicon, Inc.), Medtronic Plc, B. Braun Melsungen, Intuitive Surgical Inc., Artivion, Inc., Mizuho Medical Co., Ltd (MIZUHO Corporation), Getinge, Peters Surgical, Baxter, Vascular Graft Solutions Ltd., Medline Industries, LP, Seger Surgical Solutions, LivaNova PLC, MAQUET Holding, Novare Surgical Systems, Vitalitec International, GT Metabolic Solutions, and GI Windows Surgical. |

| Key Drivers | • Innovations in Minimally Invasive and Robotic-Assisted Surgeries Fuel Market Expansion |

| Restraints | • High Cost of Advanced Devices • Risk of Complications and Learning Curve |

Ans: The estimated compound annual growth rate is 7.01% during the forecast period for the Anastomosis Devices market.

ns: The projected market value of the Anastomosis Devices market is estimated at USD 3.61 Billion in 2023 and is expected to reach USD 6.63 Billion by 2032.

Ans: Innovations in Minimally Invasive and Robotic-Assisted Surgeries Fuel Market Expansion.

Ans: The premium pricing of innovative anastomosis devices, particularly robotic-assisted and bioabsorbable models, may limit their adoption, especially in cost-sensitive regions and healthcare systems.

Ans: North America is the dominant region in the Anastomosis Devices market.

Table of Contents

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Incidence and Prevalence (2023)

5.2 Prescription Trends (2023), by Region

5.3 Device Volume, by Region (2020-2032)

5.4 Healthcare Spending, by Region (Government, Commercial, Private, Out-of-Pocket), 2023

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new Product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. Anastomosis Devices Market Segmentation, by Product

7.1 Chapter Overview

7.2 Disposable

7.2.1 Disposable Market Trends Analysis (2020-2032)

7.2.2 Disposable Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Reusable

7.3.1 Reusable Market Trends Analysis (2020-2032)

7.3.2 Reusable Market Size Estimates and Forecasts to 2032 (USD Billion)

8. Anastomosis Devices Market Segmentation, by Application

8.1 Chapter Overview

8.2 Cardiovascular surgery

8.2.1 Cardiovascular Surgery Market Trends Analysis (2020-2032)

8.2.2 Cardiovascular Surgery Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Gastrointestinal surgery

8.3.1 Gastrointestinal Surgery Market Trends Analysis (2020-2032)

8.3.2 Gastrointestinal Surgery Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Others

8.4.1 Others Market Trends Analysis (2020-2032)

8.4.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. Anastomosis Devices Market Segmentation, by End-use

9.1 Chapter Overview

9.2 Hospitals

9.2.1 Hospitals Market Trends Analysis (2020-2032)

9.2.2 Hospitals Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Ambulatory care centers and clinics

9.3.1 Ambulatory care centers and clinics Market Trends Analysis (2020-2032)

9.3.2 Ambulatory care centers and clinics Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America Anastomosis Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.2.4 North America Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.5 North America Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.2.6.2 USA Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.6.3 USA Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.2.7.2 Canada Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.7.3 Canada Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.2.8.2 Mexico Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.2.8.3 Mexico Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe Anastomosis Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.1.6.2 Poland Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.6.3 Poland Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.1.7.2 Romania Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.7.3 Romania Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.1.8.2 Hungary Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.8.3 Hungary Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.1.9 turkey

10.3.1.9.1 Turkey Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.1.9.2 Turkey Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.9.3 Turkey Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe Anastomosis Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.4 Western Europe Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.5 Western Europe Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.6.2 Germany Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.6.3 Germany Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.7.2 France Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.7.3 France Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.8.2 UK Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.8.3 UK Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.9.2 Italy Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.9.3 Italy Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.10.2 Spain Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.10.3 Spain Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.13.2 Austria Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.13.3 Austria Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific Anastomosis Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia Pacific Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.4 Asia Pacific Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.5 Asia Pacific Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.6.2 China Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.6.3 China Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.7.2 India Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.7.3 India Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.8.2 Japan Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.8.3 Japan Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.9.2 South Korea Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.9.3 South Korea Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.10.2 Vietnam Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.10.3 Vietnam Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.11.2 Singapore Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.11.3 Singapore Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.12.2 Australia Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.12.3 Australia Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia Pacific Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia Pacific Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East Anastomosis Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.1.4 Middle East Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.5 Middle East Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.1.6.2 UAE Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.6.3 UAE Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.1.7.2 Egypt Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.7.3 Egypt Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.1.9.2 Qatar Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.9.3 Qatar Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa Anastomosis Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.2.4 Africa Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.5 Africa Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.2.6.2 South Africa Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.6.3 South Africa Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America Anastomosis Devices Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.6.4 Latin America Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.5 Latin America Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.6.6.2 Brazil Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.6.3 Brazil Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.6.7.2 Argentina Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.7.3 Argentina Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.6.8.2 Colombia Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.8.3 Colombia Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Anastomosis Devices Market Estimates and Forecasts, by Product (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America Anastomosis Devices Market Estimates and Forecasts, by Application (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America Anastomosis Devices Market Estimates and Forecasts, by End-use (2020-2032) (USD Billion)

11. Company Profiles

11.1 Johnson & Johnson (Ethicon, Inc.)

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 Medtronic Plc

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 B. Braun Melsungen

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 Intuitive Surgical Inc.

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Mizuho Medical Co., Ltd (MIZUHO Corporation)

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 Peters Surgical

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 Vascular Graft Solutions Ltd.

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Medline Industries, LP

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Novare Surgical Systems

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 GT Metabolic Solutions

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segmentation

By Product

Disposable

Reusable

By Application

Cardiovascular surgery

Gastrointestinal surgery

Others

By End-use

Hospitals

Ambulatory care centers and clinics

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Molecular Diagnostics Market Size was USD 15.35 Billion in 2023, and expected to reach USD 32.37 Billion by 2032, and grow at a CAGR of 9.07%.

The Protein A Resin Market Size was valued at USD 1.34 billion in 2023, and is expected to reach USD 3.08 billion by 2032, and grow at a CAGR of 9.7% over the forecast period 2024-2032.

The Pancreatic Cancer Treatment Market size was valued at USD 2.8 billion in 2023 and is expected to reach USD 10.53 billion by 2032 and grow at a CAGR of 15.85%.

The Rehabilitation Robots Market was valued at USD 275.21 Mn in 2023 and is expected to reach USD 1335.52 Mn by 2032, growing at a CAGR of 18.76% from 2024-2032.

The Hospital Outsourcing Market Size was valued at USD 347.8 Billion in 2023 and is projected to grow to USD 824.5 Billion by 2032, with a CAGR of 10.1%.

The Preeclampsia Diagnostics Market size was valued at USD 1.22 Billion in 2023 and is expected to reach USD 1.59 Billion By 2032 with a growing CAGR of 2.98% over the forecast period of 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd