The Aircraft MRO Market Size was valued at USD 81.25 billion in 2023 and is expected to reach USD 120.77 billion by 2031 and grow at a CAGR of 5.10% over the forecast period 2024-2031.

Aircraft MRO Market growth is driven by the increasing air travel demand, particularly in emerging economies, which drives a larger global fleet. More aircraft translates to more maintenance needs. For example, Boeing projects 41,000+ new aircraft deliveries over the next 20 years to meet demand. Airlines look to cut costs by outsourcing MRO activities to specialized providers. This allows them to focus on core operations and benefit from the expertise of MRO companies. For Example, Lufthansa Technik is a major third-party MRO provider offering diverse services to airlines like Delta and Emirates. With many aircraft exceeding their expected lifespans, there is increased maintenance demand to keep them airworthy and compliant. A significant portion of narrowbody aircraft globally are older models requiring frequent checks and overhauls. Regulations from agencies like the FAA and EASA mandate rigorous maintenance schedules. This consistently fuels the Aircraft MRO market. For Example, FAA Airworthiness Directives (ADs) outline mandatory inspections and repairs.

To get more information on the Aircraft MRO Market - Request Free Sample Report

New technologies like predictive maintenance and the use of digital tools streamline MRO processes, increase efficiency, and reduce aircraft downtime. For Example, MRO software providers like Ramco Aviation offer solutions for optimized maintenance scheduling and parts management. Airlines and lessors seek aircraft conversions and upgrades, driving demand for MRO specialization in this area. Companies like Israel Aerospace Industries (IAI) specialize in passenger-to-freighter conversions for older aircraft models.

MARKET DYNAMICS

Drivers

Growing passenger demand and air cargo trade will lead to a rise in operational aircraft, boosting demand for MRO services.

As existing airplanes require more frequent maintenance and parts replacement, the MRO market will see increased activity.

New technologies like automation and data analytics will improve efficiency and reduce costs in MRO, making them more attractive.

Stringent safety regulations from aviation authorities will necessitate regular and proper maintenance

Restraint

The high cost associated with the establishment and maintenance of MRO facilities

Fluctuations in the availability and prices of parts and materials can hinder MRO operations.

Opportunities

Development of environmentally friendly MRO practices and technologies.

Growing aviation industries in Asia and Africa will create demand for MRO services in these regions.

As economies develop in these regions, airlines are buying more aircraft to meet rising passenger demand. Larger fleets mean more aircraft needing maintenance. Airports in countries like India, China, Ethiopia, and South Africa are becoming major passenger and cargo hubs. This concentration of aircraft increases MRO demand locally and regionally. Some airlines in these regions operate older aircraft that require more frequent and intensive maintenance, increasing MRO needs. Some locations in Asia and Africa offer lower labor and operating costs for MRO, making them attractive to airlines seeking affordable maintenance options. Boeing collaborates with local MRO providers and establishes joint ventures to expand its footprint in developing countries.

For example, Boeing has partnered with Tata Advanced Systems Limited (TASL) in India for MRO work on the Boeing 737 and other models.

Challenges

Rising fuel costs can impact airline budgets and potentially decrease spending on MRO

Stringent environmental regulations regarding waste disposal and noise pollution can add complexity and cost to MRO activities

Impact of Russia-Ukraine War:

Warfare and sanctions have closed Ukrainian and significant portions of Russian airspace, hindered flight routes, and impacted MRO facilities located in these regions. More than 1000 flights were immediately canceled following Russia's invasion of Ukraine. Restrictions have limited access to spare parts and components for Russian airlines, affecting their ability to maintain Western-built aircraft. Restrictions on working with Russian airlines and a decline in overall air traffic in the region have reduced business opportunities for Western MRO companies. The war has exacerbated existing supply chain disruptions for raw materials like titanium, crucial for aircraft manufacturing and potentially impacting MRO activities as well. Rising fuel prices due to the war can indirectly affect MRO costs as airlines prioritize maintenance activities based on economic feasibility. In 2022, fuel prices reached a 14-year high due to ongoing conflicts. According to the International Air Transport Association (IATA), prices surged by a staggering 70% in the first half of 2022.

Impact of Economic Downturn:

During economic downturns, both business and leisure travel decline. This leads to airlines grounding planes or reducing flight frequencies, in turn, decreasing the overall demand for MRO services. Airlines facing financial strain may postpone non-essential or non-regulatory maintenance to cut costs in the short term. This can lead to a temporary decrease in MRO activity. Economic downturns put pressure on airlines to reduce operational costs. They may seek more competitive MRO providers or explore in-house maintenance capabilities. Smaller MRO providers may struggle to survive during economic hardship. This can lead to consolidation, or some providers may exit the market. Downturns may slow down new aircraft purchases, leading airlines to operate older aircraft for longer periods. This increases MRO needs over time due to the maintenance requirements of aging aircraft.

Market segmentation

By Service Type

Engine Overhaul

Line Maintenance

Modification

Airframe Maintenance

Components

The engine overhaul dominated the Aircraft MRO Market with the highest revenue share of more than 39.5% in 2023. Aircraft engines are complex and expensive components. Overhauling them requires specialized expertise, facilities, and expensive parts. This translates to a significant portion of an aircraft's overall maintenance cost. Aviation regulations (FAA, EASA) mandate regular engine overhauls based on factors like flight hours and cycles (starts and landings). This guarantees a steady demand for engine MRO services. Modern aircraft engines are incredibly reliable but also increasingly complex. Specialized MRO providers are essential for servicing and overhauling them. Overhauling engines restores them to peak efficiency, improving fuel economy and reducing operational costs for airlines. Within engine overhauls, high-cost components like turbines and blades often require individual maintenance, further adding to the revenue pool for this segment.

In April 2024, Honeywell and ITP Aero, a global leader in aircraft propulsion, revealed their intentions to create a new authorized maintenance facility for Honeywell's F124-GA-200 aircraft engines.

In Feb 2023, General Atomics Aeronautical Systems (GA-ASI) solidified an expression of interest (EOI) with Hindustan Aeronautics (HAL) in India to offer support services for the turbo-propeller engines of the MQ-9B aircraft. In this joint endeavor to cater to the Indian market, HAL will be responsible for providing maintenance, repair, and overhaul (MRO) services for the engines at its Engine and Industrial & Marine Gas Turbine (IMGT) division located in Bengaluru, India.

By Organization Type

Airline/Operator MRO

Independent MRO

Original Equipment Manufacturer MRO

Independent MRO led the Aircraft MRO Market in 2023 and is expected to dominate the market during the forecast period. Independent MROs aren't tied to a specific aircraft manufacturer. This allows them to offer services for a wider range of aircraft models, opening a larger customer base. They can also tailor maintenance solutions to individual airline needs. Independent MROs often have lower overhead costs compared to OEM-affiliated providers. This can translate into more competitive pricing for airlines. Independent MROs have established networks across various regions, offering proximity to customers and potentially reducing aircraft downtime during maintenance. Many independent MROs develop expertise in specific engine types, components, or aircraft models. This helps them offer niche services in high demand. Independent MRO may form partnerships with OEMs or parts suppliers, securing access to technical data and parts while maintaining flexibility in service offerings.

For example, Lufthansa Technik has capitalized on the increased demand for aircraft maintenance, repair, and overhaul (MRO) services. Lufthansa Technik showcases its prominent position in engine maintenance by completing the first overhaul of a LEAP-1B engine, which powers the Boeing 737 MAX. As the first independent MRO provider globally, Lufthansa Technik has signed a service agreement for both the LEAP-1A (Airbus A320neo) and LEAP-1B engines, ensuring access to the fleets of tomorrow.

By Aircraft Type

Narrow-Body

Wide-Body

Regional Jet

Others

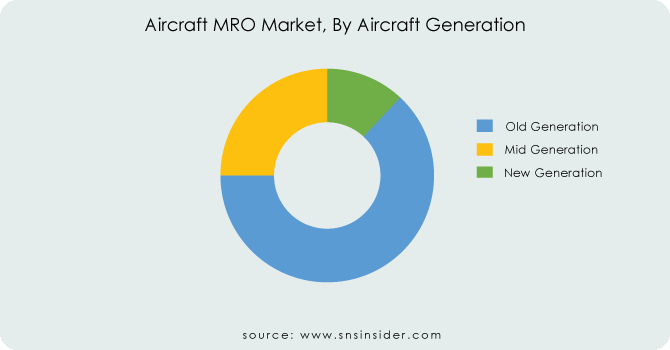

By Aircraft Generation

Old Generation

Mid Generation

New Generation

Need any customization research on the Aircraft MRO Market - Enquiry Now

Regional Analysis

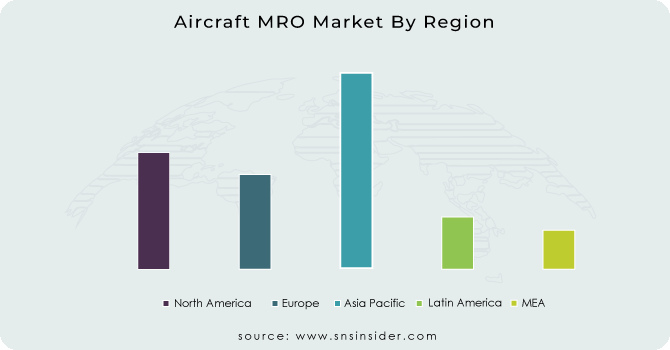

Asia Pacific led the Aircraft MRO Market with the highest revenue share of more than 33.8% in 2023. The Asia Pacific region has seen unprecedented growth in air travel demand, particularly in China, India, and Southeast Asia. This surge is driven by economic development, a burgeoning middle class, and increased tourism. More aircraft in operation naturally lead to a higher demand for maintenance, repair, and overhaul services. To meet the skyrocketing demand, airlines in the Asia Pacific are rapidly adding to their aircraft fleets. Newer aircraft require specialized MRO services, and the region is investing heavily in infrastructure and capabilities to support this expanding fleet.

Many Asia Pacific airlines are strategically outsourcing non-core functions like MRO to specialized providers. This allows airlines to focus on operations while reducing costs. The region boasts a relatively lower cost of skilled labor in comparison to North America and Europe, making it an attractive location for MRO service providers.

Major Companies in the Asia Pacific region which drive the growth of the aircraft MRO market in this region

ST Engineering (Singapore)- In Sept 2023, ST Engineering announced that its Commercial Aerospace business has signed a five-year contract to provide maintenance, repair, and overhaul (MRO) solutions for Lion Air Group's fleet of Boeing 737 MAX aircraft. This partnership establishes Lion Air Group as a pioneer customer for ST Engineering's LEAP-1B MRO services, following ST Engineering's recent inclusion in CFM International's CFM Branded Service Agreement (CBSA) LEAP MRO network in March of this year.

Air Works Group (India)- In Jan 2023, Air Works Group, India's largest independent MRO and aviation services provider, was honored with the prestigious 'Best MRO Services' award for the second year in a row at the 14th Annual Conference and Awards on Civil Aviation and Cargo hosted by ASSOCHAM on January 18, 2023.

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

KEY PLAYERS

The Major Players are Safran SA, Airbus SE, General Electric Company, AAR Corp., Lufthansa Technik, Delta Airlines, Inc., MTU Aero Engines AG, KLM U.K. Engineering Limited, Boeing, Singapore Technologies Engineering Ltd., Hong Kong Aircraft Engineering Company Limited, Raytheon Technologies Corporation, and TAP Maintenance & Engineering.

General Electric Company-Company Financial Analysis

Recent Development:

In April 2024, Safran Aircraft Engines Services Morocco (SAESM), a partnership between Safran Aircraft Engines and Royal Air Maroc, officially opened the expansion of its Nouaceur facility. The plant is located near Mohammed V International Airport in Casablanca.

In Feb 2024, RTX's Pratt & Whitney division expanded its operations in South Asia by inaugurating the India Digital Capability Center (IDCC) in Bengaluru, the capital city of Karnataka.

In May 2022, Boeing announced a strategic partnership with AI Engineering Services Ltd. (AIESL) to enhance Maintenance, Repair, and Overhaul (MRO) services for crucial equipment on key Boeing defense platforms in India. This collaboration will focus on supporting the P-8I aircraft utilized by the Indian Navy and the 777 VIP aircraft operated by the Indian Air Force.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 81.25 Billion |

| Market Size by 2031 | US$ 120.77 Billion |

| CAGR | CAGR of 5.10% From 2024 to 2031 |

| Base Year | 2023 |

| Forecast Period | 2024-2031 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Engine Overhaul, Line Maintenance, Modification, Airframe Maintenance, and Components) • By Organization Type (Airline/Operator MRO, Independent MRO, and Original Equipment Manufacturer MRO) • By Aircraft Type (Narrow-Body, Wide-Body, Regional Jet, and Others) • By Aircraft Generation (Old Generation, Mid Generation, and New Generation) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Safran SA, Airbus SE, General Electric Company, AAR Corp., Lufthansa Technik, Delta Airlines, Inc., MTU Aero Engines AG, KLM U.K. Engineering Limited, Boeing, Singapore Technologies Engineering Ltd., Hong Kong Aircraft Engineering Company Limited, Raytheon Technologies Corporation, and TAP Maintenance & Engineering. |

| DRIVERS | • Growing passenger demand and air cargo trade will lead to a rise in operational aircraft, boosting demand for MRO services. • As existing airplanes require more frequent maintenance and parts replacement, the MRO market will see increased activity. • New technologies like automation and data analytics will improve efficiency and reduce costs in MRO, making them more attractive. • Stringent safety regulations from aviation authorities will necessitate regular and proper maintenance |

| RESTRAINTS | • The high cost associated with the establishment and maintenance of MRO facilities • Fluctuations in the availability and prices of parts and materials can hinder MRO operations. |

Ans: The Aircraft MRO Market was valued at USD 81.25 billion in 2023.

Ans: The expected CAGR of the global Aircraft MRO Market during the forecast period is 5.10%.

Ans: The new-generation segment will grow rapidly in the Aircraft MRO Market from 2024-2031.

Ans: Factors such as high MRO costs, skilled labor shortages, supply chain disruptions, economic volatility, stringent regulations, and the increasing complexity of modern aircraft can restrict the growth of the Aircraft MRO market.

Ans: The China led the Aircraft MRO Market in Asia Pacific region with highest revenue share in 2023.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Impact Analysis

5.1 Impact of Russia-Ukraine Crisis

5.2 Impact of Economic Slowdown on Major Countries

5.2.1 Introduction

5.2.2 United States

5.2.3 Canada

5.2.4 Germany

5.2.5 France

5.2.6 UK

5.2.7 China

5.2.8 Japan

5.2.9 South Korea

5.2.10 India

6. Value Chain Analysis

7. Porter’s 5 Forces Model

8. Pest Analysis

9. Aircraft MRO Market Segmentation, By Service Type

9.1 Introduction

9.2 Trend Analysis

9.3 Engine Overhaul

9.4 Line Maintenance

9.5 Modification

9.6 Airframe Maintenance

9.7 Components

10. Aircraft MRO Market Segmentation, By Organization Type

10.1 Introduction

10.2 Trend Analysis

10.3 Airline/Operator MRO

10.4 Independent MRO

10.5 Original Equipment Manufacturer MRO

11. Aircraft MRO Market Segmentation, By Aircraft Type

11.1 Introduction

11.2 Trend Analysis

11.3 Narrow-Body

11.4 Wide-Body

11.5 Regional Jet

11.6 Others

12. Aircraft MRO Market Segmentation, By Aircraft Generation

12.1 Introduction

12.2 Trend Analysis

12.3 Old Generation

12.4 Mid Generation

12.5 New Generation

13. Regional Analysis

13.1 Introduction

13.2 North America

13.2.1 Trend Analysis

13.2.2 North America Aircraft MRO Market by Country

13.2.3 North America Aircraft MRO Market By Service Type

13.2.4 North America Aircraft MRO Market By Organization Type

13.2.5 North America Aircraft MRO Market By Aircraft Type

13.2.6 North America Aircraft MRO Market By Aircraft Generation

13.2.7 USA

13.2.7.1 USA Aircraft MRO Market By Service Type

13.2.7.2 USA Aircraft MRO Market By Organization Type

13.2.7.3 USA Aircraft MRO Market By Aircraft Type

13.2.7.4 USA Aircraft MRO Market By Aircraft Generation

13.2.8 Canada

13.2.8.1 Canada Aircraft MRO Market By Service Type

13.2.8.2 Canada Aircraft MRO Market By Organization Type

13.2.8.3 Canada Aircraft MRO Market By Aircraft Type

13.2.8.4 Canada Aircraft MRO Market By Aircraft Generation

13.2.9 Mexico

13.2.9.1 Mexico Aircraft MRO Market By Service Type

13.2.9.2 Mexico Aircraft MRO Market By Organization Type

13.2.9.3 Mexico Aircraft MRO Market By Aircraft Type

13.2.9.4 Mexico Aircraft MRO Market By Aircraft Generation

13.3 Europe

13.3.1 Trend Analysis

13.3.2 Eastern Europe

13.3.2.1 Eastern Europe Aircraft MRO Market by Country

13.3.2.2 Eastern Europe Aircraft MRO Market By Service Type

13.3.2.3 Eastern Europe Aircraft MRO Market By Organization Type

13.3.2.4 Eastern Europe Aircraft MRO Market By Aircraft Type

13.3.2.5 Eastern Europe Aircraft MRO Market By Aircraft Generation

13.3.2.6 Poland

13.3.2.6.1 Poland Aircraft MRO Market By Service Type

13.3.2.6.2 Poland Aircraft MRO Market By Organization Type

13.3.2.6.3 Poland Aircraft MRO Market By Aircraft Type

13.3.2.6.4 Poland Aircraft MRO Market By Aircraft Generation

13.3.2.7 Romania

13.3.2.7.1 Romania Aircraft MRO Market By Service Type

13.3.2.7.2 Romania Aircraft MRO Market By Organization Type

13.3.2.7.3 Romania Aircraft MRO Market By Aircraft Type

13.3.2.7.4 Romania Aircraft MRO Market By Aircraft Generation

13.3.2.8 Hungary

13.3.2.8.1 Hungary Aircraft MRO Market By Service Type

13.3.2.8.2 Hungary Aircraft MRO Market By Organization Type

13.3.2.8.3 Hungary Aircraft MRO Market By Aircraft Type

13.3.2.8.4 Hungary Aircraft MRO Market By Aircraft Generation

13.3.2.9 Turkey

13.3.2.9.1 Turkey Aircraft MRO Market By Service Type

13.3.2.9.2 Turkey Aircraft MRO Market By Organization Type

13.3.2.9.3 Turkey Aircraft MRO Market By Aircraft Type

13.3.2.9.4 Turkey Aircraft MRO Market By Aircraft Generation

13.3.2.10 Rest of Eastern Europe

13.3.2.10.1 Rest of Eastern Europe Aircraft MRO Market By Service Type

13.3.2.10.2 Rest of Eastern Europe Aircraft MRO Market By Organization Type

13.3.2.10.3 Rest of Eastern Europe Aircraft MRO Market By Aircraft Type

13.3.2.10.4 Rest of Eastern Europe Aircraft MRO Market By Aircraft Generation

13.3.3 Western Europe

13.3.3.1 Western Europe Aircraft MRO Market by Country

13.3.3.2 Western Europe Aircraft MRO Market By Service Type

13.3.3.3 Western Europe Aircraft MRO Market By Organization Type

13.3.3.4 Western Europe Aircraft MRO Market By Aircraft Type

13.3.3.5 Western Europe Aircraft MRO Market By Aircraft Generation

13.3.3.6 Germany

13.3.3.6.1 Germany Aircraft MRO Market By Service Type

13.3.3.6.2 Germany Aircraft MRO Market By Organization Type

13.3.3.6.3 Germany Aircraft MRO Market By Aircraft Type

13.3.3.6.4 Germany Aircraft MRO Market By Aircraft Generation

13.3.3.7 France

13.3.3.7.1 France Aircraft MRO Market By Service Type

13.3.3.7.2 France Aircraft MRO Market By Organization Type

13.3.3.7.3 France Aircraft MRO Market By Aircraft Type

13.3.3.7.4 France Aircraft MRO Market By Aircraft Generation

13.3.3.8 UK

13.3.3.8.1 UK Aircraft MRO Market By Service Type

13.3.3.8.2 UK Aircraft MRO Market By Organization Type

13.3.3.8.3 UK Aircraft MRO Market By Aircraft Type

13.3.3.8.4 UK Aircraft MRO Market By Aircraft Generation

13.3.3.9 Italy

13.3.3.9.1 Italy Aircraft MRO Market By Service Type

13.3.3.9.2 Italy Aircraft MRO Market By Organization Type

13.3.3.9.3 Italy Aircraft MRO Market By Aircraft Type

13.3.3.9.4 Italy Aircraft MRO Market By Aircraft Generation

13.3.3.10 Spain

13.3.3.10.1 Spain Aircraft MRO Market By Service Type

13.3.3.10.2 Spain Aircraft MRO Market By Organization Type

13.3.3.10.3 Spain Aircraft MRO Market By Aircraft Type

13.3.3.10.4 Spain Aircraft MRO Market By Aircraft Generation

13.3.3.11 Netherlands

13.3.3.11.1 Netherlands Aircraft MRO Market By Service Type

13.3.3.11.2 Netherlands Aircraft MRO Market By Organization Type

13.3.3.11.3 Netherlands Aircraft MRO Market By Aircraft Type

13.3.3.11.4 Netherlands Aircraft MRO Market By Aircraft Generation

13.3.3.12 Switzerland

13.3.3.12.1 Switzerland Aircraft MRO Market By Service Type

13.3.3.12.2 Switzerland Aircraft MRO Market By Organization Type

13.3.3.12.3 Switzerland Aircraft MRO Market By Aircraft Type

13.3.3.12.4 Switzerland Aircraft MRO Market By Aircraft Generation

13.3.3.13 Austria

13.3.3.13.1 Austria Aircraft MRO Market By Service Type

13.3.3.13.2 Austria Aircraft MRO Market By Organization Type

13.3.3.13.3 Austria Aircraft MRO Market By Aircraft Type

13.3.3.13.4 Austria Aircraft MRO Market By Aircraft Generation

13.3.3.14 Rest of Western Europe

13.3.3.14.1 Rest of Western Europe Aircraft MRO Market By Service Type

13.3.3.14.2 Rest of Western Europe Aircraft MRO Market By Organization Type

13.3.3.14.3 Rest of Western Europe Aircraft MRO Market By Aircraft Type

13.3.3.14.4 Rest of Western Europe Aircraft MRO Market By Aircraft Generation

13.4 Asia-Pacific

13.4.1 Trend Analysis

13.4.2 Asia-Pacific Aircraft MRO Market by Country

13.4.3 Asia-Pacific Aircraft MRO Market By Service Type

13.4.4 Asia-Pacific Aircraft MRO Market By Organization Type

13.4.5 Asia-Pacific Aircraft MRO Market By Aircraft Type

13.4.6 Asia-Pacific Aircraft MRO Market By Aircraft Generation

13.4.7 China

13.4.7.1 China Aircraft MRO Market By Service Type

13.4.7.2 China Aircraft MRO Market By Organization Type

13.4.7.3 China Aircraft MRO Market By Aircraft Type

13.4.7.4 China Aircraft MRO Market By Aircraft Generation

13.4.8 India

13.4.8.1 India Aircraft MRO Market By Service Type

13.4.8.2 India Aircraft MRO Market By Organization Type

13.4.8.3 India Aircraft MRO Market By Aircraft Type

13.4.8.4 India Aircraft MRO Market By Aircraft Generation

13.4.9 Japan

13.4.9.1 Japan Aircraft MRO Market By Service Type

13.4.9.2 Japan Aircraft MRO Market By Organization Type

13.4.9.3 Japan Aircraft MRO Market By Aircraft Type

13.4.9.4 Japan Aircraft MRO Market By Aircraft Generation

13.4.10 South Korea

13.4.10.1 South Korea Aircraft MRO Market By Service Type

13.4.10.2 South Korea Aircraft MRO Market By Organization Type

13.4.10.3 South Korea Aircraft MRO Market By Aircraft Type

13.4.10.4 South Korea Aircraft MRO Market By Aircraft Generation

13.4.11 Vietnam

13.4.11.1 Vietnam Aircraft MRO Market By Service Type

13.4.11.2 Vietnam Aircraft MRO Market By Organization Type

13.4.11.3 Vietnam Aircraft MRO Market By Aircraft Type

13.4.11.4 Vietnam Aircraft MRO Market By Aircraft Generation

13.4.12 Singapore

13.4.12.1 Singapore Aircraft MRO Market By Service Type

13.4.12.2 Singapore Aircraft MRO Market By Organization Type

13.4.12.3 Singapore Aircraft MRO Market By Aircraft Type

13.4.12.4 Singapore Aircraft MRO Market By Aircraft Generation

13.4.13 Australia

13.4.13.1 Australia Aircraft MRO Market By Service Type

13.4.13.2 Australia Aircraft MRO Market By Organization Type

13.4.13.3 Australia Aircraft MRO Market By Aircraft Type

13.4.13.4 Australia Aircraft MRO Market By Aircraft Generation

13.4.14 Rest of Asia-Pacific

13.4.14.1 Rest of Asia-Pacific Aircraft MRO Market By Service Type

13.4.14.2 Rest of Asia-Pacific Aircraft MRO Market By Organization Type

13.4.14.3 Rest of Asia-Pacific Aircraft MRO Market By Aircraft Type

13.4.14.4 Rest of Asia-Pacific Aircraft MRO Market By Aircraft Generation

13.5 Middle East & Africa

13.5.1 Trend Analysis

13.5.2 Middle East

13.5.2.1 Middle East Aircraft MRO Market by Country

13.5.2.2 Middle East Aircraft MRO Market By Service Type

13.5.2.3 Middle East Aircraft MRO Market By Organization Type

13.5.2.4 Middle East Aircraft MRO Market By Aircraft Type

13.5.2.5 Middle East Aircraft MRO Market By Aircraft Generation

13.5.2.6 UAE

13.5.2.6.1 UAE Aircraft MRO Market By Service Type

13.5.2.6.2 UAE Aircraft MRO Market By Organization Type

13.5.2.6.3 UAE Aircraft MRO Market By Aircraft Type

13.5.2.6.4 UAE Aircraft MRO Market By Aircraft Generation

13.5.2.7 Egypt

13.5.2.7.1 Egypt Aircraft MRO Market By Service Type

13.5.2.7.2 Egypt Aircraft MRO Market By Organization Type

13.5.2.7.3 Egypt Aircraft MRO Market By Aircraft Type

13.5.2.7.4 Egypt Aircraft MRO Market By Aircraft Generation

13.5.2.8 Saudi Arabia

13.5.2.8.1 Saudi Arabia Aircraft MRO Market By Service Type

13.5.2.8.2 Saudi Arabia Aircraft MRO Market By Organization Type

13.5.2.8.3 Saudi Arabia Aircraft MRO Market By Aircraft Type

13.5.2.8.4 Saudi Arabia Aircraft MRO Market By Aircraft Generation

13.5.2.9 Qatar

13.5.2.9.1 Qatar Aircraft MRO Market By Service Type

13.5.2.9.2 Qatar Aircraft MRO Market By Organization Type

13.5.2.9.3 Qatar Aircraft MRO Market By Aircraft Type

13.5.2.9.4 Qatar Aircraft MRO Market By Aircraft Generation

13.5.2.10 Rest of Middle East

13.5.2.10.1 Rest of Middle East Aircraft MRO Market By Service Type

13.5.2.10.2 Rest of Middle East Aircraft MRO Market By Organization Type

13.5.2.10.3 Rest of Middle East Aircraft MRO Market By Aircraft Type

13.5.2.10.4 Rest of Middle East Aircraft MRO Market By Aircraft Generation

13.5.3 Africa

13.5.3.1 Africa Aircraft MRO Market by Country

13.5.3.2 Africa Aircraft MRO Market By Service Type

13.5.3.3 Africa Aircraft MRO Market By Organization Type

13.5.3.4 Africa Aircraft MRO Market By Aircraft Type

13.5.3.5 Africa Aircraft MRO Market By Aircraft Generation

13.5.3.6 Nigeria

13.5.3.6.1 Nigeria Aircraft MRO Market By Service Type

13.5.3.6.2 Nigeria Aircraft MRO Market By Organization Type

13.5.3.6.3 Nigeria Aircraft MRO Market By Aircraft Type

13.5.3.6.4 Nigeria Aircraft MRO Market By Aircraft Generation

13.5.3.7 South Africa

13.5.3.7.1 South Africa Aircraft MRO Market By Service Type

13.5.3.7.2 South Africa Aircraft MRO Market By Organization Type

13.5.3.7.3 South Africa Aircraft MRO Market By Aircraft Type

13.5.3.7.4 South Africa Aircraft MRO Market By Aircraft Generation

13.5.3.8 Rest of Africa

13.5.3.8.1 Rest of Africa Aircraft MRO Market By Service Type

13.5.3.8.2 Rest of Africa Aircraft MRO Market By Organization Type

13.5.3.8.3 Rest of Africa Aircraft MRO Market By Aircraft Type

13.5.3.8.4 Rest of Africa Aircraft MRO Market By Aircraft Generation

13.6 Latin America

13.6.1 Trend Analysis

13.6.2 Latin America Aircraft MRO Market by Country

13.6.3 Latin America Aircraft MRO Market By Service Type

13.6.4 Latin America Aircraft MRO Market By Organization Type

13.6.5 Latin America Aircraft MRO Market By Aircraft Type

13.6.6 Latin America Aircraft MRO Market By Aircraft Generation

13.6.7 Brazil

13.6.7.1 Brazil Aircraft MRO Market By Service Type

13.6.7.2 Brazil Aircraft MRO Market By Organization Type

13.6.7.3 Brazil Aircraft MRO Market By Aircraft Type

13.6.7.4 Brazil Aircraft MRO Market By Aircraft Generation

13.6.8 Argentina

13.6.8.1 Argentina Aircraft MRO Market By Service Type

13.6.8.2 Argentina Aircraft MRO Market By Organization Type

13.6.8.3 Argentina Aircraft MRO Market By Aircraft Type

13.6.8.4 Argentina Aircraft MRO Market By Aircraft Generation

13.6.9 Colombia

13.6.9.1 Colombia Aircraft MRO Market By Service Type

13.6.9.2 Colombia Aircraft MRO Market By Organization Type

13.6.9.3 Colombia Aircraft MRO Market By Aircraft Type

13.6.9.4 Colombia Aircraft MRO Market By Aircraft Generation

13.6.10 Rest of Latin America

13.6.10.1 Rest of Latin America Aircraft MRO Market By Service Type

13.6.10.2 Rest of Latin America Aircraft MRO Market By Organization Type

13.6.10.3 Rest of Latin America Aircraft MRO Market By Aircraft Type

13.6.10.4 Rest of Latin America Aircraft MRO Market By Aircraft Generation

14. Company Profiles

14.1 Safran SA

14.1.1 Company Overview

14.1.2 Financial

14.1.3 Products/ Services Offered

14.1.4 SWOT Analysis

14.1.5 The SNS View

14.2 Airbus SE

14.2.1 Company Overview

14.2.2 Financial

14.2.3 Products/ Services Offered

14.2.4 SWOT Analysis

14.2.5 The SNS View

14.3 General Electric Company

14.3.1 Company Overview

14.3.2 Financial

14.3.3 Products/ Services Offered

14.3.4 SWOT Analysis

14.3.5 The SNS View

14.4 AAR Corp.

14.4.1 Company Overview

14.4.2 Financial

14.4.3 Products/ Services Offered

14.4.4 SWOT Analysis

14.4.5 The SNS View

14.5 Lufthansa Technik

14.5.1 Company Overview

14.5.2 Financial

14.5.3 Products/ Services Offered

14.5.4 SWOT Analysis

14.5.5 The SNS View

14.6 Delta Airlines, Inc.

14.6.1 Company Overview

14.6.2 Financial

14.6.3 Products/ Services Offered

14.6.4 SWOT Analysis

14.6.5 The SNS View

14.7 MTU Aero Engines AG

14.7.1 Company Overview

14.7.2 Financial

14.7.3 Products/ Services Offered

14.7.4 SWOT Analysis

14.7.5 The SNS View

14.8 KLM U.K. Engineering Limited

14.8.1 Company Overview

14.8.2 Financial

14.8.3 Products/ Services Offered

14.8.4 SWOT Analysis

14.8.5 The SNS View

14.9 Boeing

14.9.1 Company Overview

14.9.2 Financial

14.9.3 Products/ Services Offered

14.9.4 SWOT Analysis

14.9.5 The SNS View

14.10 Singapore Technologies Engineering Ltd.

14.10.1 Company Overview

14.10.2 Financial

14.10.3 Products/ Services Offered

14.10.4 SWOT Analysis

14.10.5 The SNS View

14.11 Hong Kong Aircraft Engineering Company Limited

14.11.1 Company Overview

14.11.2 Financial

14.11.3 Products/ Services Offered

14.11.4 SWOT Analysis

14.11.5 The SNS View

14.12 Raytheon Technologies Corporation

14.12.1 Company Overview

14.12.2 Financial

14.12.3 Products/ Services Offered

14.12.4 SWOT Analysis

14.12.5 The SNS View

14.13 TAP Maintenance & Engineering

14.13.1 Company Overview

14.13.2 Financial

14.13.3 Products/ Services Offered

14.13.4 SWOT Analysis

14.13.5 The SNS View

15. Competitive Landscape

15.1 Competitive Benchmarking

15.2 Market Share Analysis

15.3 Recent Developments

15.3.1 Industry News

15.3.2 Company News

15.3.3 Mergers & Acquisitions

16. Use Case and Best Practices

17. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

The Aviation Fuel Market size was valued at USD 284.3 billion in 2023 and is expected to reach USD 901.4 billion by 2032, growing at a CAGR of 13.6% over the forecast period of 2024-2032.

The Smart Assault Rifle Market Size was valued at USD 17.35 Billion in 2023 and is expected to reach USD 30.64 Billion by 2032 and grow at a CAGR of 6.81% over the forecast period 2024-2032.

The Aircraft Jack Market size was USD 1.70 billion in 2023 and is projected to reach USD 2.36 billion by 2032, reflecting a CAGR of 3.71% during the forecast period from 2024 to 2032.

The Hydrogen Aircraft Market Size was valued at USD 308.09 million in 2023 expected to reach USD 2861.67 million by 2032 and grow at a CAGR of 28.10% over the forecast period 2024-2032.

The Flight Data Monitoring Market Size was valued at USD 2.89 billion in 2023, expected to reach USD 5.82 billion by 2032 with an emerging CAGR of 8.10% over the forecast period 2024-2032.

The 5G From Space Market Size was valued at USD 291.5 million in 2023 and is expected to reach USD 24003.1 million by 2032 and grow at a CAGR of 63.3% over the forecast period 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd