AI Governance Market Report Scope & Overview:

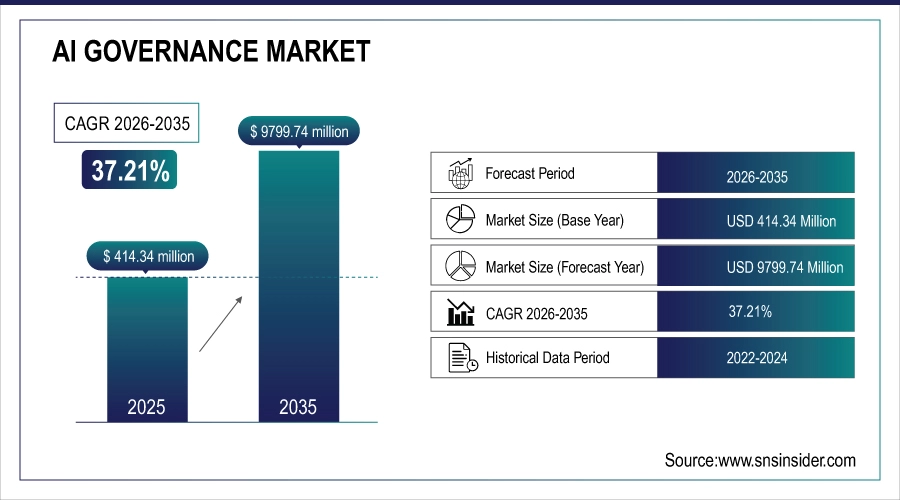

The AI Governance Market is valued at USD 414.34 Million in 2025 and is expected to reach USD 9799.74 Million by 2035, growing at a CAGR of 37.21% over 2026-2035.

The AI Governance Market is experiencing explosive growth driven by the need for organizational risk management, growing regulatory restrictions, and ethical AI issues. To make sure AI systems are open, accountable, equitable, and in compliance with changing international laws, such as the EU AI Act, NIST AI RMF, and sector-specific mandates, organizations from a variety of industries are putting governance frameworks into place. A full ecosystem that addresses algorithmic bias detection, model monitoring, documentation, and audit trail management across the AI lifecycle is created by the convergence of technical governance tools, policy frameworks, and compliance automation.

84% of Fortune 500 companies implemented structured AI governance programs in 2025, reducing regulatory non-compliance risks by 68% while increasing stakeholder trust in AI-driven decision systems through standardized transparency and accountability frameworks.

AI Governance Market Size and Forecast:

-

Market Size in 2025: USD 414.34 Million

-

Market Size by 2035: USD 9799.74 Million

-

CAGR: 37.21% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on AI Governance Market - Request Free Sample Report

AI Governance Market Trends:

-

Accelerated adoption of automated compliance platforms integrating EU AI Act, NIST AI RMF, and sector-specific regulatory requirements.

-

Growing implementation of bias detection and fairness testing tools throughout model development and deployment lifecycle.

-

Increasing demand for AI model inventory management and documentation solutions ensuring audit readiness.

-

Rising integration of governance tools within MLOps pipelines enabling continuous compliance monitoring.

-

Expansion of third-party AI risk assessment and certification services for supply chain governance.

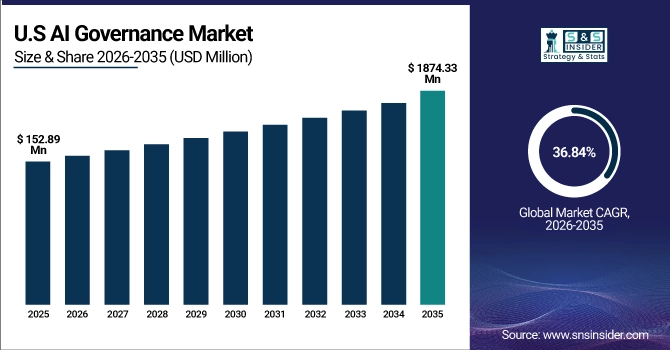

U.S. AI Governance Market is valued at USD 152.89 Million in 2025 and is expected to reach USD 1874.33 Million by 2035, growing at a CAGR of 36.84% over 2026-2035.

The U.S. AI Governance Market is growing driven by sectoral laws, legal risks, and executive instructions on AI safety. In response to FTC regulations, sector-specific compliance, and algorithmic accountability requirements, financial institutions, healthcare providers, and tech firms are implementing governance solutions. This is being aided by the implementation of the NIST framework and pressure from the insurance sector to reduce risk.

AI Governance Market Growth Drivers:

-

Escalating Global Regulatory Pressure and Compliance Mandates Drive Urgent Adoption of AI Governance Frameworks Across Regulated Industries

Organizations implementing AI systems must comply with the growing number of AI-specific laws around the world, such as the EU AI Act, U.S. AI Executive Orders, Singapore's AI Verify, and Canada's AIDA. Strict requirements on risk classification, transparency documentation, bias reduction, and human oversight are imposed by these rules. Businesses who violate the EU AI Act risk severe financial fines (up to 7% of worldwide revenue) and operational limitations. Organizations are forced by this regulatory environment to put in place thorough governance solutions that include risk assessment, documentation management, bias testing, and audit trail maintenance across the course of the AI lifecycle.

79% of regulated entities accelerated AI governance implementation in 2025 following final EU AI Act adoption, with compliance spending increasing 140% year-over-year to meet 2026 enforcement deadlines.

AI Governance Market Restraints:

-

Technical Complexity and Skills Shortage in Algorithmic Auditing and Governance Implementation Slow Adoption Across Mid-Market Organizations

Implementing effective AI governance requires specialized expertise in machine learning operations, regulatory compliance, ethics frameworks, and risk management. Implementation is severely hampered by the lack of individuals globally, who possess both governance subject experience and AI technical understanding. Determining relevant governance criteria, choosing appropriate technologies, and integrating governance procedures into current AI development workflows are challenges faced by many enterprises. Despite explicit regulatory restrictions, this complexity slows market penetration, especially for SMEs and mid-market businesses without specialized AI ethical teams.

68% of mid-market companies delayed comprehensive AI governance adoption due to technical complexity and skills gaps, opting instead for basic documentation solutions lacking robust monitoring capabilities.

AI Governance Market Opportunities:

-

Emerging AI Insurance Market Creates Demand for Standardized Governance Frameworks and Certification Services

The rapidly developing AI liability insurance sector requires standardized risk assessment methodologies and governance certifications. Insurers increasingly mandate specific governance controls as policy prerequisites, creating a market for third-party assessment services and certified governance platforms. This trend establishes governance compliance as both regulatory requirement and commercial necessity for obtaining affordable insurance coverage. Governance solution providers can develop insurer-approved frameworks, certification programs, and continuous monitoring services, create new revenue streams, further accelerating market education and adoption.

In 2025, 73% of AI insurance policies required NIST-aligned governance frameworks, driving 85% growth in third-party assessment services and creating USD 220 Million certification market segment.

AI Governance Market Segment Highlights:

-

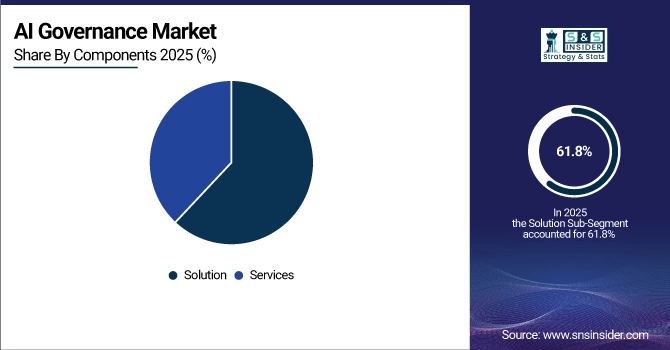

By Components: Solutions led with 61.8% share, while Services is the fastest-growing segment with CAGR of 41.3%.

-

By Deployment: Cloud-based led with 58.4% share, while On-Premises maintains stable growth with CAGR of 32.7%.

-

By Organization Size: Large Enterprises led with 72.9% share, while SMEs is the fastest-growing segment with CAGR of 44.2%.

-

By Vertical: BFSI led with 28.3% share, while Healthcare is the fastest-growing segment with CAGR of 46.8%.

AI Governance Market Segment Analysis:

By Components: Solutions Segment Led the Market, while Services is the Fastest-growing Segment Globally

Solutions dominate the AI governance market, comprising software platforms for model monitoring, bias detection, documentation management, and compliance automation. Market leadership stems from urgent regulatory compliance needs driving immediate software procurement, with solutions delivering measurable risk reduction through continuous algorithmic oversight and audit-ready reporting.

Services represent the fastest-growing component as organizations require expert assistance in framework design, implementation strategy, and ongoing governance program management. Accelerated growth derives from the realization that technology alone cannot address cultural, procedural, and expertise challenges. Service providers help clients navigate evolving regulations, establish cross-functional governance committees, and develop sustainable oversight processes, creating continuous engagement opportunities beyond initial software deployment.

By Deployment: Cloud-based Dominated the Market, while On-Premises Segment Maintains Stable Growth Globally

Cloud-based deployment leads the market due to superior scalability, rapid implementation, and automatic regulatory updates. Cloud governance solutions offer seamless integration with cloud AI services, centralized management for distributed teams, and subscription-based pricing aligning with operational expenditure preferences. Dominance reflects broader cloud adoption trends in enterprise AI infrastructure, where governance platforms must interoperate with cloud-based development environments and model hosting services.

On-Premises deployment maintains stable growth driven by data sovereignty requirements, security sensitivities, and legacy infrastructure constraints in regulated industries. This segment demonstrates consistent demand from security-conscious enterprises and public sector entities, with specialized vendors offering air-gapped deployments and customized integration with existing security infrastructure.

By Organization Size: Large Enterprises Dominated the Market, while SMEs is the Fastest-growing Segment During the Forecast Period

Large Enterprises dominate market share due to complex regulatory exposure, substantial AI investments, and dedicated compliance resources. These organizations face scrutiny from multiple regulators, operate across jurisdictions with conflicting requirements, and deploy numerous high-risk AI systems requiring documented governance. Market leadership reflects both regulatory pressure and strategic recognition that governance enables responsible scaling of AI initiatives.

SMEs represent the fastest-growing segment as regulatory requirements expand to cover smaller organizations and AI deployment becomes democratized. Accelerated growth stems from increasing regulatory awareness, supply chain pressure from enterprise partners, and affordable cloud-based governance solutions tailored to resource-constrained organizations.

By Vertical: BFSI Segment Led the Market, while Healthcare is the Fastest-growing Segment Globally

BFSI leads vertical adoption due to stringent regulatory oversight, high-stakes algorithmic decisioning, and early regulatory clarity in financial AI governance. Financial institutions face specific requirements from banking regulators, securities commissions, and consumer protection agencies regarding algorithmic trading, credit scoring, fraud detection, and customer service AI. Leadership position reflects both compliance necessity and competitive differentiation through trustworthy AI systems.

Healthcare demonstrates the fastest growth as regulatory bodies clarify AI/ML software requirements and patient safety concerns escalate. Accelerated adoption follows FDA guidelines for AI/ML-based medical devices, HIPAA considerations for health data usage, and increasing malpractice litigation involving algorithmic recommendations. Healthcare organizations implement governance to ensure clinical validation, bias mitigation in treatment algorithms, and transparent patient communication about AI-assisted care.

AI Governance Market Regional Analysis:

North America AI Governance Market Insights:

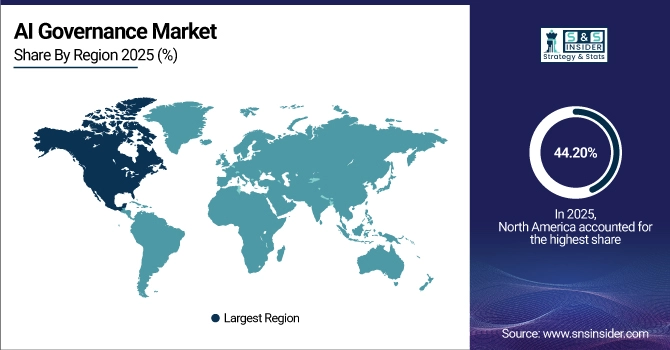

Due to early business adoption, concentrated AI sector presence, and proactive regulatory activities, North America held a 44.20% share in the AI Governance Market in 2025. The creation of the NIST AI RMF framework, industry-specific regulatory guidelines, and a large concentration of multinational corporations putting sophisticated governance programs into place all help the region. Regional market leadership and innovation velocity are further reinforced by significant entrepreneurial investment in governance technologies and academic leadership in AI ethical research.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific AI Governance Market Insights:

Asia Pacific is expected to grow at the fastest CAGR of about 42.80% over 2026–2035, driven by rapidly evolving regulatory landscapes, expanding AI deployment scale, and government-led standardization initiatives. While businesses speed up implementation to preserve export compliance and global competitiveness, nations, such as Singapore, Japan, South Korea, and India are creating national AI governance frameworks. Due to the region's predominance in manufacturing and the growth of digital services, supply chain AI and consumer-facing apps require immediate oversight.

Europe AI Governance Market Insights:

Europe held a significant share in the AI Governance Market in 2025, supported by comprehensive regulatory leadership through EU AI Act implementation. Robust governance investment is driven by the region's strong data protection culture, cross-border compliance requirements, and public sector deployment of AI. In the automotive, industrial, and financial services industries, European businesses exhibit very high adoption rates. In international marketplaces, governance is seen as a competitive advantage that necessitates verifiable algorithmic accountability and ethical compliance.

Middle East & Africa and Latin America AI Governance Market Insights:

The Middle East & Africa and Latin America together showed accelerating growth in the AI Governance Market in 2025, driven by sector-specific legislative reform, growing foreign investment necessitating governance norms, and the deployment of national AI strategies. With growth driven by both local regulatory development and multinational business compliance requirements, the regions show particular strength in government AI governance, applications in the natural resource sector, and financial technology supervision.

AI Governance Market Competitive Landscape:

IBM Corporation

IBM Corporation, founded in 1911, is a global technology leader providing AI governance through its Watson OpenScale and AI Ethics platforms. The company integrates governance capabilities across AI lifecycle management, offering bias detection, explainability, and regulatory compliance features. IBM's established enterprise relationships and research leadership in trustworthy AI position it as comprehensive solution provider for regulated industries globally.

-

January 2025, IBM enhanced its AI Governance platform with automated EU AI Act compliance modules and generative AI monitoring capabilities for enterprise LLM deployments.

Google LLC

Google LLC, established in 1998, provides AI governance through Vertex AI Governance and Responsible AI Toolkit. The company emphasizes scalable governance integration within development workflows, offering model cards, fairness indicators, and continuous monitoring. Google's cloud-native approach and research in ML fairness positions it strongly for organizations seeking integrated governance across AI development and deployment environments.

-

March 2025, Google launched expanded AI governance features in Vertex AI, including automated compliance reporting and cross-model bias analysis for regulated industry requirements.

Microsoft Corporation

Microsoft Corporation, founded in 1975, delivers AI governance through Azure AI Content Safety, Responsible AI Dashboard, and compliance tools. The company focuses on integrated governance across Azure ML services, offering risk assessment, documentation automation, and policy management. Microsoft's enterprise platform dominance and regulatory partnership approach support comprehensive governance implementation.

-

February 2025, Microsoft introduced new Purview AI governance capabilities providing unified visibility and control across organizational AI assets with regulatory template mapping.

AI Governance Market Key Players

-

IBM Corporation

-

Google LLC

-

SAP SE

-

SAS Institute Inc.

-

Salesforce, Inc.

-

H2O.ai, Inc.

-

DataRobot, Inc.

-

Fiddler AI, Inc.

-

Monitaur, Inc.

-

ModelOp, Inc.

-

Holistic AI

-

Trustwise AI

-

Credo AI

-

Aible, Inc.

-

Pathlight Technology

-

Superwise.ai

-

Algorithmic Justice League

-

EqualAI

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 414.34 Million |

| Market Size by 2035 | USD 9799.74 Million |

| CAGR | CAGR 37.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solution And Services) • By Deployment Mode (Cloud And On-Premises) • By Organization Size (Large Enterprises, And Small And Medium-Sized Enterprises) • By Vertical (BFSI, Government And Defense, Healthcare And Life Sciences, Media And Entertainment, Retail, IT And Telecom, Automotive, And Other Verticals) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Google LLC, Microsoft Corporation, SAP SE, SAS Institute Inc., Salesforce, Inc., H2O.ai, Inc., DataRobot, Inc., Fiddler AI, Inc., Monitaur, Inc., Arthur AI, Inc., ModelOp, Inc., Holistic AI, Trustwise AI, Credo AI, Aible, Inc., Pathlight Technology, Superwise.ai, Algorithmic Justice League, EqualAI |

Frequently Asked Questions

Ans: - The estimated market size for the AI Governance market for the year 2035 is USD 9799.74 Million.

Ans- AI Governance Market is valued at USD 414.34 Million in 2025 and is expected to reach USD 9799.74 Million by 2035, growing at a CAGR of 37.21% over 2026-2035.

Ans- In 2025, North America led the AI Governance Market, capturing a significant revenue share of 32.95%.

Ans- one main growth factor for the AI Governance Market is

• The need for effective risk management in AI deployment is leading to investments in AI risk management tools and automated compliance solutions.

Ans- challenges in AI Governance Market are

- Lack of clear and consistent global regulations hinders AI adoption and governance efforts.

- Strict data privacy laws and concerns about data misuse slow down AI development and governance initiatives.

Get in touch