Get more information on Advance Directives Market - Request Sample Report

The Advance Directives Market was valued at USD 122.74 billion in 2023 and is anticipated to reach USD 588.40 billion by 2032 with a CAGR 19.04% over the forecast period 2024-2032.

The demand for advance directives is escalating due to factors such as an aging population, increasing chronic illnesses, and growing awareness about end-of-life care. A surge in healthcare costs and the desire for personalized care are further driving the need for clear and accessible advance directives. The COVID-19 pandemic underscored the critical importance of advance care planning (ACP). With a staggering 1 in 5 adults hospitalized and a concerning 1 in 20 requiring a ventilator, many faced the grim reality of potential severe illness or death. As a result, there was a surge in interest in ACP, which allows individuals to document their healthcare preferences for end-of-life care. A recent study of JAMA Network Open in July 2020, found a notable increase in demand for ACP services during the pandemic, highlighting the public's growing recognition of its significance in preparing for potential health crises.

On the supply side, technological advancements are revolutionizing the industry. AI-powered tools offer tailored healthcare information and decision support, while telemedicine expands access to end-of-life planning services. Moreover, a shift towards digital platforms is streamlining the creation, storage, and sharing of advance directives. Despite the potential benefits, the adoption of advance directives (ADs) remains low, particularly among older adults. Factors such as general health, psychological well-being, and attitudes towards death influence AD completion. To increase AD adoption, targeted interventions are necessary. These interventions should focus on providing comprehensive information, addressing physical and psychological health concerns, and offering personalized support to facilitate the AD completion process.

Governments are actively promoting advance directives through a combination of awareness campaigns, financial incentives, and regulatory mandates. Initiatives like "National Healthcare Decisions Day" in the US raise public awareness and provide educational resources. Government healthcare programs like Medicare cover consultations about advance care planning, encouraging proactive discussions.

Legislations such as the Patient Self-Determination Act in the US ensure that healthcare facilities inform patients about their rights to create advance directives and integrate these directives into patient records. Many states have also enacted laws recognizing various forms of advance directives and providing legal frameworks for their implementation.

Beyond legal compliance, the focus is shifting towards a more patient-centered approach. This involves considering individual treatment goals, personal values, and cultural preferences when creating advance directives. By empowering patients with information and support, governments aim to facilitate informed decision-making and ensure that end-of-life care aligns with patients' wishes.

However, challenges persist that is fragmentation within healthcare systems and inadequate interdisciplinary collaboration hinder the seamless implementation of advance directives. Despite these challenges, the overall advance directives market outlook is promising. The convergence of technology, supportive policies, and growing public awareness is expected to propel the advance directives market towards a future where individuals have greater control over their end-of-life care.

The Convergence of Healthcare and Technology in Advance Care Planning

Advance care planning (ACP) is rapidly gaining investor interest. The potential for significant cost savings by reducing hospitalizations, readmissions, and emergency department visits is driving this investment. Studies have shown that ACP services can increase hospice enrolment and decrease intensive care, leading to substantial cost reductions. This financial opportunity hasn't gone unnoticed. Companies focusing on ACP solutions are attracting significant funding. For example, Koda Health recently secured USD 3.5 million to expand nationwide, while Vynca raised USD 30 million, reporting a 64% increase in end-of-life planning documents created in a single year.

As investment in ACP continues to grow, the industry is poised for substantial expansion. This increased funding will likely fuel innovation and improve access to ACP services, ultimately leading to better patient care and outcomes.

Secure online platforms now allow individuals to easily create, store, and access these vital documents. This digital shift enhances accessibility and ensures timely availability for healthcare providers. Additionally, online resources offer comprehensive information about advance directives, empowering individuals to make informed decisions.

While technology undoubtedly offers convenience, it's crucial to prioritize the quality of decision-making. Digital tools must support thoughtful consideration of personal values and goals. By combining technology with effective communication strategies, we can ensure that advance directives accurately reflect individual wishes and are effectively understood by loved ones and healthcare professionals.

Low Adoption Rates of Advance Directives Despite Potential Benefits

Advance directives (ADs) offer the potential to improve end-of-life care by involving patients, families, and medical staff in treatment planning, their adoption rates remain relatively low. For instance, despite their introduction in the US, only one-third of adults have documented ADs.

In Korea, where a similar law was enacted in 2018, family decisions still dominate end-of-life care, with ADs used in only about 30% of cases involving withholding or discontinuing life-sustaining treatment. This suggests that cultural and societal factors significantly impact AD utilization, even in countries with established legal frameworks.

The advance directives services segment constituted a major portion of the overall market with 65% in 2023. These services provide invaluable guidance and support to individuals navigating the complexities of end-of-life planning. As public awareness of advance directives grows, the need for professional guidance in creating and managing these documents will significantly increase.

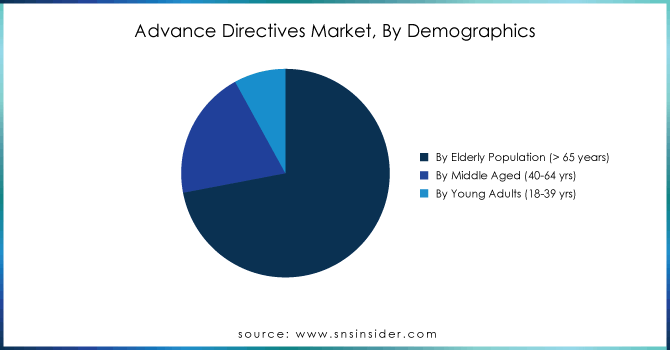

The elderly population was the primary driver of the advance directives market with 72% market share in 2023. With aging populations on the rise globally, the need for end-of-life planning among this demographic is significantly increasing. This segment's growing awareness of advance directives and their potential benefits is expected to fuel substantial market growth.

Get Customized Report as per your Business Requirement - Request For Customized Report

Healthcare providers were the primary drivers of the advance directives market with 75% market share in 2023. Their pivotal role in initiating these conversations, offering guidance, and facilitating the creation of legal documents has significantly contributed to their dominant position within the market.

Regional Analysis

North America dominated the advance directives market with 59% market share in 2023 due to its advanced healthcare infrastructure, supportive regulatory environment, and strong emphasis on patient autonomy. Advance directive discussions have become standard practice within well-established healthcare systems, significantly contributing to market growth.

The Asian advance directives market is experiencing rapid expansion fueled by factors such as aging populations, increasing chronic diseases, and a growing awareness of patient rights. While cultural barriers initially posed challenges, a shift towards patient-centered care and government support are accelerating market growth.

ThroughCare, Inc., Honor My Decisions LLC, ADvault, Inc., ACP Decisions (a DBA of Nous Foundation, Inc.), VyncaCare, Thanacare, Island Health (Canada), WiserCare Inc., New Century Health, Sharp HealthCare, MIDEO, Iris Healthcare (Aledade, Inc.), Affirm Health Inc., Bronson Health Care Group, Inc., Vital Decisions LLC, Koda Health, and others

Recent Developments

In Jan 2023, West Health and Sharp Healthcare have partnered to create a comprehensive care model tailored to the specific needs of the elderly population.

In April 2023, ADvault, Inc. has launched initiatives to improve advance care planning, including collaborations to provide better digital resources and promote open discussions about end-of-life care.

| Report Attributes | Details |

| Market Size in 2023 | US$ 122.74 billion |

| Market Size by 2032 | US$ 588.40 Billion |

| CAGR | CAGR of 19.04 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Demographics [By Elderly Population (> 65 years), By Middle Aged (40-64 yrs), By Young Adults (18-39 yrs)] • By End User [B2B (Providers and Payers), B2C (Patients and Caregivers)] |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | ThroughCare, Inc., Honor My Decisions LLC, ADvault, Inc., ACP Decisions (a DBA of Nous Foundation, Inc.), VyncaCare, Thanacare, Island Health (Canada), WiserCare Inc., New Century Health, Sharp HealthCare, MIDEO, Iris Healthcare (Aledade, Inc.), Affirm Health Inc., Bronson Health Care Group, Inc., Vital Decisions LLC, Koda Health, and others |

| Key Drivers | • The Convergence of Healthcare and Technology in Advance Care Planning |

| Restraints | • Low Adoption Rates of Advance Directives Despite Potential Benefits |

Ans: The estimated compound annual growth rate is 19.04% during the forecast period for the Advance Directives market.

Ans: The projected market value of the Advance Directives market is estimated USD 122.74 billion in 2023 and expected to reach USD 588.40 billion by 2032.

Ans: The convergence of healthcare and technology in advance care planning is one of the drivers of the Advance Directives market.

Ans: Low adoption rates of advance directives despite potential benefits hamper the market growth which is one of the restraints of the Advance Directives market.

Ans: North America is the dominating region with 59% market share in the Advance Directives market.

TABLE OF CONTENTS

1. Introduction

1.1 Market Definition

1.2 Scope

1.3 Research Assumptions

2. Industry Flowchart

3. Research Methodology

4. Market Dynamics

4.1 Drivers

4.2 Restraints

4.3 Opportunities

4.4 Challenges

5. Porter’s 5 Forces Model

6. Pest Analysis

7. Advance Directives Market Segmentation, By Component

7.1 Introduction

7.2 Software

7.3 Services

8. Advance Directives Market Segmentation, By Demographics

8.1 Introduction

8.2 By Elderly Population (> 65 years)

8.3 By Middle Aged (40-64 yrs)

8.4 By Young Adults (18-39 yrs)

9. Advance Directives Market Segmentation, By End User

9.1 Introduction

9.2 B2B (Providers and Payers)

9.3 B2C (Patients and Caregivers)

10. Regional Analysis

10.1 Introduction

10.2 North America

10.2.1 Trend Analysis

10.2.2 North America Advance Directives Market by Country

10.2.3 North America Advance Directives Market By Component

10.2.4 North America Advance Directives Market By Demographics

10.2.5 North America Advance Directives Market By End User

10.2.6 USA

10.2.6.1 USA Advance Directives Market By Component

10.2.6.2 USA Advance Directives Market By Demographics

10.2.6.3 USA Advance Directives Market By End User

10.2.7 Canada

10.2.7.1 Canada Advance Directives Market By Component

10.2.7.2 Canada Advance Directives Market By Demographics

10.2.7.3 Canada Advance Directives Market By End User

10.2.8 Mexico

10.2.8.1 Mexico Advance Directives Market By Component

10.2.8.2 Mexico Advance Directives Market By Demographics

10.2.8.3 Mexico Advance Directives Market By End User

10.3 Europe

10.3.1 Trend Analysis

10.3.2 Eastern Europe

10.3.2.1 Eastern Europe Advance Directives Market by Country

10.3.2.2 Eastern Europe Advance Directives Market By Component

10.3.2.3 Eastern Europe Advance Directives Market By Demographics

10.3.2.4 Eastern Europe Advance Directives Market By End User

10.3.2.5 Poland

10.3.2.5.1 Poland Advance Directives Market By Component

10.3.2.5.2 Poland Advance Directives Market By Demographics

10.3.2.5.3 Poland Advance Directives Market By End User

10.3.2.6 Romania

10.3.2.6.1 Romania Advance Directives Market By Component

10.3.2.6.2 Romania Advance Directives Market By Demographics

10.3.2.6.4 Romania Advance Directives Market By End User

10.3.2.7 Hungary

10.3.2.7.1 Hungary Advance Directives Market By Component

10.3.2.7.2 Hungary Advance Directives Market By Demographics

10.3.2.7.3 Hungary Advance Directives Market By End User

10.3.2.8 Turkey

10.3.2.8.1 Turkey Advance Directives Market By Component

10.3.2.8.2 Turkey Advance Directives Market By Demographics

10.3.2.8.3 Turkey Advance Directives Market By End User

10.3.2.9 Rest of Eastern Europe

10.3.2.9.1 Rest of Eastern Europe Advance Directives Market By Component

10.3.2.9.2 Rest of Eastern Europe Advance Directives Market By Demographics

10.3.2.9.3 Rest of Eastern Europe Advance Directives Market By End User

10.3.3 Western Europe

10.3.3.1 Western Europe Advance Directives Market by Country

10.3.3.2 Western Europe Advance Directives Market By Component

10.3.3.3 Western Europe Advance Directives Market By Demographics

10.3.3.4 Western Europe Advance Directives Market By End User

10.3.3.5 Germany

10.3.3.5.1 Germany Advance Directives Market By Component

10.3.3.5.2 Germany Advance Directives Market By Demographics

10.3.3.5.3 Germany Advance Directives Market By End User

10.3.3.6 France

10.3.3.6.1 France Advance Directives Market By Component

10.3.3.6.2 France Advance Directives Market By Demographics

10.3.3.6.3 France Advance Directives Market By End User

10.3.3.7 UK

10.3.3.7.1 UK Advance Directives Market By Component

10.3.3.7.2 UK Advance Directives Market By Demographics

10.3.3.7.3 UK Advance Directives Market By End User

10.3.3.8 Italy

10.3.3.8.1 Italy Advance Directives Market By Component

10.3.3.8.2 Italy Advance Directives Market By Demographics

10.3.3.8.3 Italy Advance Directives Market By End User

10.3.3.9 Spain

10.3.3.9.1 Spain Advance Directives Market By Component

10.3.3.9.2 Spain Advance Directives Market By Demographics

10.3.3.9.3 Spain Advance Directives Market By End User

10.3.3.10 Netherlands

10.3.3.10.1 Netherlands Advance Directives Market By Component

10.3.3.10.2 Netherlands Advance Directives Market By Demographics

10.3.3.10.3 Netherlands Advance Directives Market By End User

10.3.3.11 Switzerland

10.3.3.11.1 Switzerland Advance Directives Market By Component

10.3.3.11.2 Switzerland Advance Directives Market By Demographics

10.3.3.11.3 Switzerland Advance Directives Market By End User

10.3.3.12 Austria

10.3.3.12.1 Austria Advance Directives Market By Component

10.3.3.12.2 Austria Advance Directives Market By Demographics

10.3.3.12.3 Austria Advance Directives Market By End User

10.3.3.13 Rest of Western Europe

10.3.3.13.1 Rest of Western Europe Advance Directives Market By Component

10.3.3.13.2 Rest of Western Europe Advance Directives Market By Demographics

10.3.3.13.3 Rest of Western Europe Advance Directives Market By End User

10.4 Asia-Pacific

10.4.1 Trend Analysis

10.4.2 Asia-Pacific Advance Directives Market by Country

10.4.3 Asia-Pacific Advance Directives Market By Component

10.4.4 Asia-Pacific Advance Directives Market By Demographics

10.4.5 Asia-Pacific Advance Directives Market By End User

10.4.6 China

10.4.6.1 China Advance Directives Market By Component

10.4.6.2 China Advance Directives Market By Demographics

10.4.6.3 China Advance Directives Market By End User

10.4.7 India

10.4.7.1 India Advance Directives Market By Component

10.4.7.2 India Advance Directives Market By Demographics

10.4.7.3 India Advance Directives Market By End User

10.4.8 Japan

10.4.8.1 Japan Advance Directives Market By Component

10.4.8.2 Japan Advance Directives Market By Demographics

10.4.8.3 Japan Advance Directives Market By End User

10.4.9 South Korea

10.4.9.1 South Korea Advance Directives Market By Component

10.4.9.2 South Korea Advance Directives Market By Demographics

10.4.9.3 South Korea Advance Directives Market By End User

10.4.10 Vietnam

10.4.10.1 Vietnam Advance Directives Market By Component

10.4.10.2 Vietnam Advance Directives Market By Demographics

10.4.10.3 Vietnam Advance Directives Market By End User

10.4.11 Singapore

10.4.11.1 Singapore Advance Directives Market By Component

10.4.11.2 Singapore Advance Directives Market By Demographics

10.4.11.3 Singapore Advance Directives Market By End User

10.4.12 Australia

10.4.12.1 Australia Advance Directives Market By Component

10.4.12.2 Australia Advance Directives Market By Demographics

10.4.12.3 Australia Advance Directives Market By End User

10.4.13 Rest of Asia-Pacific

10.4.13.1 Rest of Asia-Pacific Advance Directives Market By Component

10.4.13.2 Rest of Asia-Pacific Advance Directives Market By Demographics

10.4.13.3 Rest of Asia-Pacific Advance Directives Market By End User

10.5 Middle East & Africa

10.5.1 Trend Analysis

10.5.2 Middle East

10.5.2.1 Middle East Advance Directives Market by Country

10.5.2.2 Middle East Advance Directives Market By Component

10.5.2.3 Middle East Advance Directives Market By Demographics

10.5.2.4 Middle East Advance Directives Market By End User

10.5.2.5 UAE

10.5.2.5.1 UAE Advance Directives Market By Component

10.5.2.5.2 UAE Advance Directives Market By Demographics

10.5.2.5.3 UAE Advance Directives Market By End User

10.5.2.6 Egypt

10.5.2.6.1 Egypt Advance Directives Market By Component

10.5.2.6.2 Egypt Advance Directives Market By Demographics

10.5.2.6.3 Egypt Advance Directives Market By End User

10.5.2.7 Saudi Arabia

10.5.2.7.1 Saudi Arabia Advance Directives Market By Component

10.5.2.7.2 Saudi Arabia Advance Directives Market By Demographics

10.5.2.7.3 Saudi Arabia Advance Directives Market By End User

10.5.2.8 Qatar

10.5.2.8.1 Qatar Advance Directives Market By Component

10.5.2.8.2 Qatar Advance Directives Market By Demographics

10.5.2.8.3 Qatar Advance Directives Market By End User

10.5.2.9 Rest of Middle East

10.5.2.9.1 Rest of Middle East Advance Directives Market By Component

10.5.2.9.2 Rest of Middle East Advance Directives Market By Demographics

10.5.2.9.3 Rest of Middle East Advance Directives Market By End User

10.5.3 Africa

10.5.3.1 Africa Advance Directives Market by Country

10.5.3.2 Africa Advance Directives Market By Component

10.5.3.3 Africa Advance Directives Market By Demographics

10.5.3.4 Africa Advance Directives Market By End User

10.5.3.5 Nigeria

10.5.3.5.1 Nigeria Advance Directives Market By Component

10.5.3.5.2 Nigeria Advance Directives Market By Demographics

10.5.3.5.3 Nigeria Advance Directives Market By End User

10.5.3.6 South Africa

10.5.3.6.1 South Africa Advance Directives Market By Component

10.5.3.6.2 South Africa Advance Directives Market By Demographics

10.5.3.6.3 South Africa Advance Directives Market By End User

10.5.3.7 Rest of Africa

10.5.3.7.1 Rest of Africa Advance Directives Market By Component

10.5.3.7.2 Rest of Africa Advance Directives Market By Demographics

10.5.3.7.3 Rest of Africa Advance Directives Market By End User

10.6 Latin America

10.6.1 Trend Analysis

10.6.2 Latin America Advance Directives Market by country

10.6.3 Latin America Advance Directives Market By Component

10.6.4 Latin America Advance Directives Market By Demographics

10.6.5 Latin America Advance Directives Market By End User

10.6.6 Brazil

10.6.6.1 Brazil Advance Directives Market By Component

10.6.6.2 Brazil Advance Directives Market By Demographics

10.6.6.3 Brazil Advance Directives Market By End User

10.6.7 Argentina

10.6.7.1 Argentina Advance Directives Market By Component

10.6.7.2 Argentina Advance Directives Market By Demographics

10.6.7.3 Argentina Advance Directives Market By End User

10.6.8 Colombia

10.6.8.1 Colombia Advance Directives Market By Component

10.6.8.2 Colombia Advance Directives Market By Demographics

10.6.8.3 Colombia Advance Directives Market By End User

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America Advance Directives Market By Component

10.6.9.2 Rest of Latin America Advance Directives Market By Demographics

10.6.9.3 Rest of Latin America Advance Directives Market By End User

11. Company Profiles

11.1 ThroughCare, Inc.

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 The SNS View

11.2 Honor My Decisions LLC

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 The SNS View

11.3 ADvault, Inc.

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 The SNS View

11.4 ACP Decisions (a DBA of Nous Foundation, Inc.)

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 The SNS View

11.5 VyncaCare

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 The SNS View

11.6 Thanacare

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 The SNS View

11.7 Island Health (Canada)

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 The SNS View

11.8 WiserCare Inc.

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 The SNS View

11.9 New Century Health

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 The SNS View

11.10 Sharp HealthCare

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 The SNS View

12. Competitive Landscape

12.1 Competitive Benchmarking

12.2 Market Share Analysis

12.3 Recent Developments

12.3.1 Industry News

12.3.2 Company News

12.3.3 Mergers & Acquisitions

13. Use Case and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Component

Software

Services

By Demographics

By Elderly Population (> 65 years)

By Middle Aged (40-64 yrs)

By Young Adults (18-39 yrs)

By End User

B2B (Providers and Payers)

B2C (Patients and Caregivers)

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Nicotine Replacement Therapy Market Size was valued at USD 2.83 Billion in 2023, and is expected to reach USD 4.27 Billion by 2032, and grow at a CAGR of 4.83%.

The Anatomic Pathology Track and Trace Solutions Market Size was valued at USD 642.97 million in 2022, and is expected to reach USD 1460.53 million by 2030 and grow at a CAGR of 10.8% over the forecast period 2023-2030.

The Animal Wound Care Market was valued at USD 1.32 Bn in 2023 & will reach USD 2.55 Bn by 2032 & grow at a CAGR of 7.55% from 2024 to 2032.

The Allergic Conjunctivitis Market Size was valued at USD 2.75 Billion in 2023 and is expected to reach USD 4.02 Billion by 2032, growing at a CAGR of 4.31% over the forecast period of 2024-2032.

Pet Insurance Market Size was valued at USD 15.4 Billion in 2023 and is expected to reach USD 68.91 billion by 2032, growing at a CAGR of 18.13% over the forecast period 2024-2032.

The Retinal Vein Occlusion Treatment Market was valued at USD 2.49 billion in 2023 and is expected to reach USD 4.35 billion by 2032, growing at a CAGR of 6.44% from 2024 to 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd