Get more information on 5G Infrastructure Market - Request Sample Report

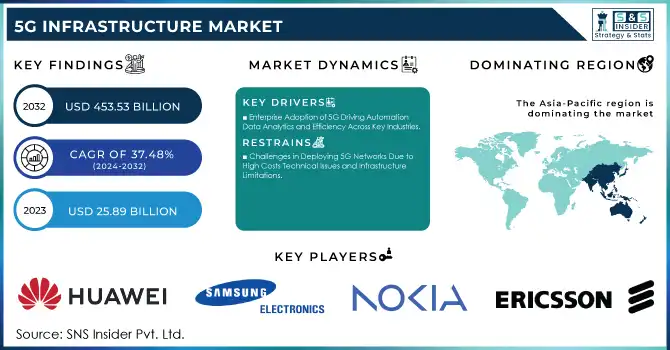

The 5G Infrastructure Market was valued at USD 25.89 billion in 2023 and is expected to reach USD 453.53 billion by 2032, growing at a CAGR of 37.48% over the forecast period 2024-2032.

One of the main reasons is the growing requirement for faster, reliable, high-capacity networks to fulfill the rising data consumption. But there are too many devices connected to devices, like the Internet of Things (IoT), automotive/Infrastructure (autonomous vehicles, smart cities), and even AR/VR. With its ultra-low latency, faster speeds, and the additional bandwidth for all these innovations to work as intended, 5G technology is the enabler of this next stage of evolution. Furthermore, with businesses and consumers moving toward digitization, 5G networks provide high speeds and extensive connectivity for seamless operations, thus driving demand across several verticals. More than 207 billion devices around the world, including consumer electronics, are projected to be connected by 2024. With ultra-low latency, 5G enables delays of just 1 millisecond, while 4G averages 200 milliseconds. Median 5G download speeds in the U.S. were 287.14 Mbps in March 2024, demonstrating marked improvements on a national-scale network as well.

Global governments and telecommunications operators are aggressively investing in 5G throughout the world to guarantee broad access to the next-generation technology. The deployment of 5G incorporates substantial improvements in network architecture and a transition to 5G standalone solutions that are expected to deliver significant advantages and performance over current 4G LTE-based systems. The continued expansion of the market is complemented by the accelerating demand for 5G from a growing number of commercial, industrial, and governmental applications. Technological innovation, rising demand for mobile data, and government initiatives drive the growth of the 5g Infrastructure market. More than 2 billion people around the world are predicted to be using 5G connections by the end of 2024. Globally, 341 commercial 5G networks are now up and running as of September 2024, more than 4G LTE was deployed at a similar phase. With full 5G deployment, the smart production industry represents an economic impact of EUR 90 billion in Europe.

KEY DRIVERS:

Enterprise use cases are materializing as one of the biggest market drivers with companies from the likes of manufacturing to finance leveraging 5G for automation, cloud services, and advanced data analytics. Sectors like manufacturing, healthcare, and logistics are especially looking forward to improved operational efficiency with 5G technology. Industry 4.0, with its features of AI, machine learning, and robotics, needs high-low latency networks to work its magic. These applications require real-time data transmission with minimal latency which is only possible with the large capacity that 5G can provide. Moreover, companies are also expected to deploy private 5G networks to address security concerns, improve reliability, and maximize network performance which in turn is driving the demand for 5G Infrastructure solutions. There will be around 4,700 private 5G network deployments worldwide by 2024, representing 13% of global 5G IoT connections, up to 5.15 million connections. Connected smart manufacturing devices-Up to 75 million devices in manufacturing will connect for industrial automation, which will in turn require 5G connectivity. Connected smart medical devices–around 5.2 million connected medical devices will use 5G for real-time data exchange in healthcare. Automobiles Moreover, by the end of 2024, 40% of logistics companies will be 5G-enabled with supply chain operations.

The increasing rise of smart cities and IoT ecosystems further acts as an important driver. With the global urbanization growth pace, another type of public Infrastructure investment has emerged: smart city Infrastructure investment by governments to ensure a higher quality of life for urban inhabitants and better efficiency of public services offered by governments. This transformation is largely driven by 5G which allows for real-time data collection and analysis from a variety of distributed IoT devices including sensors, smart meters, and surveillance and tracking systems. Such use cases demand high-performance networks for smooth functioning. Things like smarter traffic management, efficient waste disposal networks, and energy consumption monitoring will be made possible by 5G. The increase in the usage of Internet of Things (IoT) devices in industries such as healthcare, agriculture, and transportation, along with the requirement for ultra-high-speed, ultra-low-latency networks, is escalating the market demand for 5G Infrastructure. This is also expected to serve as a highly lucrative opportunity for the market over the upcoming years. At a global scale, investments in smart city initiatives will probably hit USD 400 Billion by 2024. By 2025, more than 60 million traffic lights will probably be operated by smart traffic systems fueled by 5G. On the healthcare front, 400 million connected medical devices will be gained throughout the world and 10,000 good waste management systems will be in use worldwide. Also, worldwide IoT data traffic is projected to reach 79.4 zettabytes by 2025, largely due to 5G applications in all sectors.

RESTRAIN:

The high cost of deploying 5G networks is a significant challenge. Building out the infrastructure needed to implement 5G such as new towers and antennas, and core network upgrades, is expensive. While the above-mentioned technology offers many advantages, many telecom operators and enterprises (especially in developing regions) may not have deep enough pockets to get the above technology on the scale. Moreover, the large required traditional range registration and processes can push back 5G coverage in nations with heavy guideline conditions. The second restraint concerns the technical and operational challenges related to 5G deployment. Unfortunately, achieving this kind of global scale reliability and performance will require enormous upgrades to existing Infrastructure and also, face major obstacles such as signal interference and minimal broadband access in rural/remote areas. Deployment is further complicated by the need to integrate 5G with current 4G networks and the coexistence of multiple technologies.

BY COMMUNICATION INFRASTRUCTURE

RAN (Radio Access Network) held the largest share of the 5G Infrastructure market in 2023, accounting for 45.5%, and is anticipated to grow at the highest CAGR during the forecast period of 2024 to 2032. The reason for this supremacy comes from RAN's essential function in actualizing the high-speed, low-latency features of 5G that are critical for new-age applications like autonomous vehicles, Internet of Things devices, and AR/VR. RAN designs accommodate the wireless link that connects devices to the core network & as the proliferation of 5G increases new demand will turn towards small cells, macro cells, or even all-new massive MIMO RAN solutions. RAN's rapid growth is also attributed to a desire for more capacity, efficiency, and coverage to manage the explosive growth in connected devices and high-traffic apps. When mobile operators grow their 5G networks worldwide, they need to upgrade RAN Infrastructure, so that it can handle rising bandwidth and reliability requirements. Meanwhile, the transition to 5G standalone (NR + Core) networks associated with higher performance development than non-standalone networks will also contribute to RAN growth in the coming years.

BY SPECTRUM BAND

The 5G infrastructure market was dominated by Mid Band (1–6GHz), accounting for 47.9% of the market in 2023 as it provides an ideal balance between coverage, capacity, and speed, making it useful for urban and suburban deployments. This spectrum band strikes an excellent balance of coverage and performance, featuring substantially higher data speeds and lower latency than the Low Band (<1GHz), and better coverage than High Band (24-40GHz). Hence, Mid Band is critical for large national rollouts of 5G for both residential and commercial use cases, particularly in dense urban centers, where network loads are likely to be very high.

The High Band (24-40GHz) witness the fastest CAGR during the forecast period 2024-2032, owing to the ultra-high speed and large bandwidth supporting applications driving the need for massive amounts of data for high data applications such as Augmented reality, Virtual reality, and ultra-high definition video streaming. Despite challenges related to coverage & signal propagation with High Band, the performance characteristics of the High Band make it an important enabler of specific use cases, especially in urban and dense network areas where the need for speed and capacity is the greatest. Continuous upgrades in network infrastructure facilities, such as beamforming and smart antenna technologies, will further propel the growth potential of High Band and subsequently, contribute to the overall market growth.

BY NETWORK ARCHITECTURE

In 2023, the market is dominated by 5G NR Non-Standalone (LTE Combined) capturing 63.6% of the market share as this technology is based on the available LTE infrastructure that reduces the time and cost for the deployment of 5G services. It allows telecom operators to upgrade their existing 4G infrastructure into 5G by building on top of it to avoid costly upgrades or create new assets for capital investments. Non-Standalone architecture is beneficial in the early stages of 5G implementation therefore it allows operators to quickly implement seamless service while providing extensive service area coverage and continued compatibility with existing user devices and networks.

5G Standalone (NR + Core) is predicted to be the fastest growing segment during the years 2024-2032, indicating a transition of the market towards large-scale deployment of 5G functionalities. Standalone architecture independent of LTE, using a 5G core, offering better features (Ultra-low Latency, Massive machine-type communication, Network slicing, etc). Such capabilities are essential for new applications from smart factories, and autonomous cars to critical IoT systems. The Standalone architecture is capable of utilizing the full potential of 5G and not only supporting future 5G-enabled applications but also supporting the next wave of digital transformation, making it an attractive option as telecom operators and industries invest in long-term 5G infrastructure.

BY END USE

In 2023, the residential sector accounted for 41.7% of the overall market share for 5G infrastructure, significantly driven by the increasing demand for better home internet connectivity. The explosion of data-hungry apps like 4K/8K streaming video, online gaming, smart homes, and many others, has boosted the need for super-fast low latency networks and network devices like never before. Meanwhile, the COVID-19 pandemic accelerated the trend towards remote work and online education, which made stable home connectivity all the more critical. The speed, capacity rivaling broadband, and low latency of 5G make it an increasingly appealing option for households living in crowded urban and suburban centers. Driven by the need to make 5G residential services cost-effective and accessible, operators are re-focusing on fixed wireless access (FWA) and further extending its prevalence in this market segment.

The industrial segment is projected to be the fastest growing CAGR in the forecast duration from 2024 to 2032 owing to the early penetration of emerging technologies like IoT, AI, and robotics. Ultra-Reliable Low-Latency Communication Networks is a must-have enabler for the transformation of manufacturing, logistics, and supply chain operations driven by Industry 4.0 initiatives. This instantaneous data transfer and automation is essential for applications such as autonomous vehicles, predictive maintenance, digital twins, and smart factories and 5G makes all of this possible. Industrial use cases, in contrast to residential applications, impose a high requirement on network reliability, security, and performance, and thus, the 5G Standalone architecture characterized by network slicing and edge computing, is indispensable here. Meanwhile, the likes of energy, healthcare, and agriculture are adopting 5G for smart grids, remote surgeries, and precision farming.

REGIONAL ANALYSIS

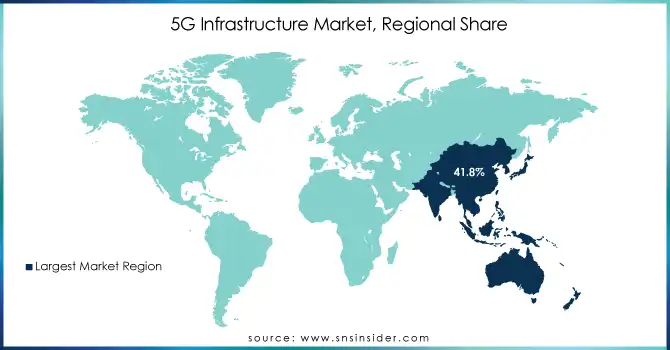

In 2023, Asia Pacific accounted for the largest 5G infrastructure market share of 41.8% as pioneering and large-scale deployments in countries such as China, South Korea, and Japan continue to drive the adoption of advanced 5G technologies. Specifically, China has been at the forefront of 5G rollout and adoption as major telecoms such as China Mobile, China Telecom, and China Unicom work to rapidly expand 5G coverage and push it to advanced applications like smart cities and industrial IoT. South Korea was one of the pioneers in commercializing 5G with SK Telecom being the first mobile carrier to leverage the technology for augmented reality (AR) and ultra-HD broadcasting. 5G is backing robotics and automation in Japan, especially during the preparations for mega events like the Olympics, where it pulled off some of the most advanced use cases in 5G.

North America will record the fastest CAGR over the forecast period from 2024 to 2032, led by major investments and innovations in the U.S. and Canada. The U.S., for example, has seen telecom heavyweights like Verizon, AT&T, and T-Mobile go all in on providing wider 5G coverage in both urban and rural locations. In the case of Verizon, it has been utilizing its fixed wireless access (FWA) solutions to provide high-speed 5G implementation for both home and business users, At the same time, the automotive sector is applying 5G for connected vehicles and self-driving projects. Meanwhile, Canada is also catching up with many telecom providers collaborating with government initiatives to develop 5G infrastructures through smart city projects to advanced healthcare with remote surgeries on ultra-low latency 5G networks.

Do you need any custom research/data on 5G Infrastructure Market - Enquiry Now

Key players

Some of the major players in the 5G Infrastructure Market are:

Huawei Technologies Co. Ltd. (5G Base Stations, 5G Core Network Solutions)

Samsung Electronics Co. Ltd. (5G RAN Solutions, 5G mmWave Equipment)

Nokia Corporation (AirScale Radio Access, 5G Cloud Core)

Ericsson (Ericsson Radio System, 5G Core)

ZTE Corporation (5G RAN Products, 5G Core Network Solutions)

Qualcomm Technologies, Inc. (Snapdragon X55 5G Modem, 5G RAN Platforms)

Intel Corporation (Intel Atom P5900, 5G Network Acceleration Solutions)

Cisco Systems Inc. (5G Carrier Routing System, Ultra Services Platform)

NEC Corporation (Open RAN Solutions, 5G Core Network Products)

Mavenir Systems Inc. (Open RAN Solutions, 5G Core Software)

Hewlett Packard Enterprise Company (5G Core Network Solutions, Edge Computing Platforms)

AT&T Inc. (5G Network Services, 5G Edge Solutions)

Verizon Communications Inc. (5G Ultra Wideband, 5G Home Internet)

T-Mobile US, Inc. (5G Extended Range, 5G Home Internet)

LG Electronics Inc. (5G Small Cells, 5G Network Equipment)

Airspan Networks Inc. (Air5G Platform, Small Cell Solutions)

Comba Telecom Systems Holdings Limited (5G Antennas, RAN Solutions)

Oracle Corporation (5G Network Orchestration, Cloud-Native 5G Core)

Broadcom Inc. (5G ASICs, Networking Chips)

MediaTek Inc. (Dimensity 5G Chipsets, 5G Modem Solutions)

Some of the Raw Material Suppliers for 5G Infrastructure Companies:

DuPont de Nemours, Inc.

AGC Inc.

Rogers Corporation

Soitec

ITEQ Corporation

Asahi Kasei Corporation

Panasonic Industry Co., Ltd.

Kuraray Co., Ltd.

Covestro AG

Celanese Corporation

RECENT TRENDS

In June 2024, Huawei announced its strategic direction for 5G-Advanced (5G-A) at MWC Shanghai 2024, focusing on industry collaboration, ecosystem development, and advancing network technology.

In December 2024, Nokia and EOLO launched Europe’s first 5G standalone mmWave network in Italy, providing ultra-fast broadband to underserved areas. The initiative aims to bridge the digital divide with cutting-edge 5G FWA technology.

In November 2024, AIS and ZTE completed a trial of D3-ELAA technology, integrating 6G concepts into 5G advanced networks in Thailand. The trial demonstrated enhanced user experience with improved connectivity and high-bandwidth services without the need for terminal upgrades.

| Report Attributes | Details |

| Market Size in 2023 | USD 25.89 billion |

| Market Size by 2032 | USD 453.53 billion |

| CAGR | CAGR of 37.48% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Communication Infrastructure (RAN (Radio Access Network), Transport Technology, Core Technology) • By Spectrum Band (Low Band (<1 GHz), Mid Band (1-6GHz), High Band (24-40GHz)) • By Network Architecture (5G NR Non-Standalone (LTE Combined), 5G Standalone (NR + Core)) • By End Use (Residential, Commercial, Industrial, Government)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Huawei Technologies Co. Ltd., Samsung Electronics Co. Ltd., Nokia Corporation, Ericsson, ZTE Corporation, Qualcomm Technologies, Inc., Intel Corporation, Cisco Systems Inc., NEC Corporation, Mavenir Systems Inc., Hewlett Packard Enterprise Company, AT&T Inc., Verizon Communications Inc., T-Mobile US, Inc., LG Electronics Inc., Airspan Networks Inc., Comba Telecom Systems Holdings Limited, Oracle Corporation, Broadcom Inc., MediaTek Inc. |

| Key Drivers | • Enterprise Adoption of 5G Driving Automation Data Analytics and Efficiency Across Key Industries • Rise of Smart Cities and IoT Ecosystems Driving Global 5G Infrastructure Investment and Innovation |

| Market Restraints | • Challenges in Deploying 5G Networks Due to High Costs Technical Issues and Infrastructure Limitations |

Ans. The projected market size for the 5G infrastructure Market is USD 504.4 billion by 2031.

Ans:- The increase in a numtheer of mobile users. and Rapid development of IoT platforms.

Ans:- In 2022, the Asia Pacific region led the market with the largest share.

Ans:- In 2022, the enterprise/corporate category dominated the market, accounting for the majority of sales.

Ans:- The major key players are AT&T, Huawei Devices Co. Ltd., Ericsson, Intel Corporation, Mediatek Inc., Nokia Corporation, Qualcomm Technologies Inc., Hewlett Packard Enterprise, Samsung Electronics Co. Ltd., Verizon.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 5G Infrastructure Adoption Rate (2023)

5.2 5G Infrastructure Network Coverage (2023)

5.3 5G Infrastructure Energy Efficiency

5.4 5G Infrastructure Spectrum Auction Revenue

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and promotional activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. 5G Infrastructure Market Segmentation, By Communication Infrastructure

7.1 Chapter Overview

7.2 RAN (Radio Access Network)

7.2.1 RAN (Radio Access Network) Market Trends Analysis (2020-2032)

7.2.2 RAN (Radio Access Network) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 Transport Technology

7.3.1 Transport Technology Market Trends Analysis (2020-2032)

7.3.2 Transport Technology Market Size Estimates and Forecasts to 2032 (USD Billion)

7.4 Core Technology

7.4.1 Core Technology Market Trends Analysis (2020-2032)

7.4.2 Core Technology Market Size Estimates and Forecasts to 2032 (USD Billion)

8. 5G Infrastructure Market Segmentation, By Spectrum Band

8.1 Chapter Overview

8.2 Low Band (<1 GHz)

8.2.1 Low Band (<1 GHz) Market Trends Analysis (2020-2032)

8.2.2 Low Band (<1 GHz) Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Mid Band (1-6GHz)

8.3.1 Mid Band (1-6GHz) Market Trends Analysis (2020-2032)

8.3.2 Mid Band (1-6GHz) Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 High Band (24-40GHz)

8.4.1 High Band (24-40GHz) Market Trends Analysis (2020-2032)

8.4.2 High Band (24-40GHz) Market Size Estimates and Forecasts to 2032 (USD Billion)

9. 5G Infrastructure Market Segmentation, By Network Architecture

9.1 Chapter Overview

9.2 5G NR Non-Standalone (LTE Combined)

9.2.1 5G NR Non-Standalone (LTE Combined) Market Trends Analysis (2020-2032)

9.2.2 5G NR Non-Standalone (LTE Combined) Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 5G Standalone (NR + Core)

9.3.1 5G Standalone (NR + Core) Market Trends Analysis (2020-2032)

9.3.2 5G Standalone (NR + Core) Market Size Estimates and Forecasts to 2032 (USD Billion)

10. 5G Infrastructure Market Segmentation, By End Use

10.1 Chapter Overview

10.2 Residential

10.2.1 Residential Market Trends Analysis (2020-2032)

10.2.2 Residential Market Size Estimates and Forecasts to 2032 (USD Billion)

10.3 Commercial

10.3.1 Commercial Market Trends Analysis (2020-2032)

10.3.2 Commercial Market Size Estimates and Forecasts to 2032 (USD Billion)

10.4 Industrial

10.4.1 Industrial Market Trends Analysis (2020-2032)

10.4.2 Industrial Market Size Estimates and Forecasts to 2032 (USD Billion)

10.5 Government

10.5.1 Government Market Trends Analysis (2020-2032)

10.5.2 Government Market Size Estimates and Forecasts to 2032 (USD Billion)

11. Regional Analysis

11.1 Chapter Overview

11.2 North America

11.2.1 Trends Analysis

11.2.2 North America 5G Infrastructure Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.2.3 North America 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.2.4 North America 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.2.5 North America 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.2.6 North America 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.7 USA

11.2.7.1 USA 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.2.7.2 USA 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.2.7.3 USA 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.2.7.4 USA 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.8 Canada

11.2.8.1 Canada 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.2.8.2 Canada 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.2.8.3 Canada 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.2.8.4 Canada 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.2.9 Mexico

11.2.9.1 Mexico 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.2.9.2 Mexico 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.2.9.3 Mexico 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.2.9.4 Mexico 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3 Europe

11.3.1 Eastern Europe

11.3.1.1 Trends Analysis

11.3.1.2 Eastern Europe 5G Infrastructure Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.1.3 Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.1.4 Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.1.5 Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.1.6 Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.7 Poland

11.3.1.7.1 Poland 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.1.7.2 Poland 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.1.7.3 Poland 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.1.7.4 Poland 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.8 Romania

11.3.1.8.1 Romania 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.1.8.2 Romania 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.1.8.3 Romania 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.1.8.4 Romania 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.9 Hungary

11.3.1.9.1 Hungary 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.1.9.2 Hungary 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.1.9.3 Hungary 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.1.9.4 Hungary 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.10 turkey

11.3.1.10.1 Turkey 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.1.10.2 Turkey 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.1.10.3 Turkey 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.1.10.4 Turkey 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.1.11 Rest of Eastern Europe

11.3.1.11.1 Rest of Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.1.11.2 Rest of Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.1.11.3 Rest of Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.1.11.4 Rest of Eastern Europe 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2 Western Europe

11.3.2.1 Trends Analysis

11.3.2.2 Western Europe 5G Infrastructure Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.3.2.3 Western Europe 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.4 Western Europe 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.5 Western Europe 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.6 Western Europe 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.7 Germany

11.3.2.7.1 Germany 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.7.2 Germany 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.7.3 Germany 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.7.4 Germany 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.8 France

11.3.2.8.1 France 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.8.2 France 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.8.3 France 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.8.4 France 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.9 UK

11.3.2.9.1 UK 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.9.2 UK 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.9.3 UK 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.9.4 UK 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.10 Italy

11.3.2.10.1 Italy 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.10.2 Italy 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.10.3 Italy 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.10.4 Italy 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.11 Spain

11.3.2.11.1 Spain 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.11.2 Spain 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.11.3 Spain 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.11.4 Spain 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.12 Netherlands

11.3.2.12.1 Netherlands 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.12.2 Netherlands 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.12.3 Netherlands 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.12.4 Netherlands 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.13 Switzerland

11.3.2.13.1 Switzerland 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.13.2 Switzerland 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.13.3 Switzerland 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.13.4 Switzerland 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.14 Austria

11.3.2.14.1 Austria 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.14.2 Austria 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.14.3 Austria 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.14.4 Austria 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.3.2.15 Rest of Western Europe

11.3.2.15.1 Rest of Western Europe 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.3.2.15.2 Rest of Western Europe 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.3.2.15.3 Rest of Western Europe 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.3.2.15.4 Rest of Western Europe 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4 Asia Pacific

11.4.1 Trends Analysis

11.4.2 Asia Pacific 5G Infrastructure Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.4.3 Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.4 Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.5 Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.6 Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.7 China

11.4.7.1 China 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.7.2 China 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.7.3 China 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.7.4 China 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.8 India

11.4.8.1 India 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.8.2 India 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.8.3 India 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.8.4 India 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.9 Japan

11.4.9.1 Japan 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.9.2 Japan 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.9.3 Japan 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.9.4 Japan 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.10 South Korea

11.4.10.1 South Korea 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.10.2 South Korea 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.10.3 South Korea 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.10.4 South Korea 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.11 Vietnam

11.4.11.1 Vietnam 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.11.2 Vietnam 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.11.3 Vietnam 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.11.4 Vietnam 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.12 Singapore

11.4.12.1 Singapore 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.12.2 Singapore 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.12.3 Singapore 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.12.4 Singapore 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.13 Australia

11.4.13.1 Australia 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.13.2 Australia 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.13.3 Australia 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.13.4 Australia 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.4.14 Rest of Asia Pacific

11.4.14.1 Rest of Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.4.14.2 Rest of Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.4.14.3 Rest of Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.4.14.4 Rest of Asia Pacific 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5 Middle East and Africa

11.5.1 Middle East

11.5.1.1 Trends Analysis

11.5.1.2 Middle East 5G Infrastructure Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.1.3 Middle East 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.1.4 Middle East 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.1.5 Middle East 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.1.6 Middle East 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.7 UAE

11.5.1.7.1 UAE 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.1.7.2 UAE 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.1.7.3 UAE 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.1.7.4 UAE 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.8 Egypt

11.5.1.8.1 Egypt 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.1.8.2 Egypt 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.1.8.3 Egypt 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.1.8.4 Egypt 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.9 Saudi Arabia

11.5.1.9.1 Saudi Arabia 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.1.9.2 Saudi Arabia 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.1.9.3 Saudi Arabia 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.1.9.4 Saudi Arabia 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.10 Qatar

11.5.1.10.1 Qatar 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.1.10.2 Qatar 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.1.10.3 Qatar 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.1.10.4 Qatar 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.1.11 Rest of Middle East

11.5.1.11.1 Rest of Middle East 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.1.11.2 Rest of Middle East 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.1.11.3 Rest of Middle East 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.1.11.4 Rest of Middle East 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2 Africa

11.5.2.1 Trends Analysis

11.5.2.2 Africa 5G Infrastructure Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.5.2.3 Africa 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.2.4 Africa 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.2.5 Africa 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.2.6 Africa 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.7 South Africa

11.5.2.7.1 South Africa 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.2.7.2 South Africa 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.2.7.3 South Africa 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.2.7.4 South Africa 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.8 Nigeria

11.5.2.8.1 Nigeria 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.2.8.2 Nigeria 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.2.8.3 Nigeria 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.2.8.4 Nigeria 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.5.2.9 Rest of Africa

11.5.2.9.1 Rest of Africa 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.5.2.9.2 Rest of Africa 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.5.2.9.3 Rest of Africa 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.5.2.9.4 Rest of Africa 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6 Latin America

11.6.1 Trends Analysis

11.6.2 Latin America 5G Infrastructure Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

11.6.3 Latin America 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.6.4 Latin America 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.6.5 Latin America 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.6.6 Latin America 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.7 Brazil

11.6.7.1 Brazil 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.6.7.2 Brazil 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.6.7.3 Brazil 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.6.7.4 Brazil 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.8 Argentina

11.6.8.1 Argentina 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.6.8.2 Argentina 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.6.8.3 Argentina 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.6.8.4 Argentina 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.9 Colombia

11.6.9.1 Colombia 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.6.9.2 Colombia 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.6.9.3 Colombia 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.6.9.4 Colombia 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

11.6.10 Rest of Latin America

11.6.10.1 Rest of Latin America 5G Infrastructure Market Estimates and Forecasts, By Communication Infrastructure (2020-2032) (USD Billion)

11.6.10.2 Rest of Latin America 5G Infrastructure Market Estimates and Forecasts, By Spectrum Band (2020-2032) (USD Billion)

11.6.10.3 Rest of Latin America 5G Infrastructure Market Estimates and Forecasts, By Network Architecture (2020-2032) (USD Billion)

11.6.10.4 Rest of Latin America 5G Infrastructure Market Estimates and Forecasts, By End Use (2020-2032) (USD Billion)

12. Company Profiles

12.1 Huawei Technologies Co. Ltd

12.1.1 Company Overview

12.1.2 Financial

12.1.3 Products/ Services Offered

12.1.4 SWOT Analysis

12.2 Samsung Electronics Co. Ltd.

12.2.1 Company Overview

12.2.2 Financial

12.2.3 Products/ Services Offered

12.2.4 SWOT Analysis

12.3 Nokia Corporation

12.3.1 Company Overview

12.3.2 Financial

12.3.3 Products/ Services Offered

12.3.4 SWOT Analysis

12.4 Ericsson.

12.4.1 Company Overview

12.4.2 Financial

12.4.3 Products/ Services Offered

12.4.4 SWOT Analysis

12.5 ZTE Corporation

12.5.1 Company Overview

12.5.2 Financial

12.5.3 Products/ Services Offered

12.5.4 SWOT Analysis

12.6 Qualcomm Technologies, Inc

12.6.1 Company Overview

12.6.2 Financial

12.6.3 Products/ Services Offered

12.6.4 SWOT Analysis

12.7 Intel Corporation

12.7.1 Company Overview

12.7.2 Financial

12.7.3 Products/ Services Offered

12.7.4 SWOT Analysis

12.8 Cisco Systems Inc

12.8.1 Company Overview

12.8.2 Financial

12.8.3 Products/ Services Offered

12.8.4 SWOT Analysis

12.9 NEC Corporation

12.9.1 Company Overview

12.9.2 Financial

12.9.3 Products/ Services Offered

12.9.4 SWOT Analysis

12.10 Mavenir Systems Inc.

12.10.1 Company Overview

12.10.2 Financial

12.10.3 Products/ Services Offered

12.10.4 SWOT Analysis

13. Use Cases and Best Practices

14. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Communication Infrastructure

RAN (Radio Access Network)

Transport Technology

Core Technology

By Spectrum Band

Low Band (<1 GHz)

Mid Band (1-6GHz)

High Band (24-40GHz)

By Network Architecture

5G NR Non-Standalone (LTE Combined)

5G Standalone (NR + Core)

By End Use

Residential

Commercial

Industrial

Government

Request for Segment Customization as per your Business Requirement: Segment Customization Request

REGIONAL COVERAGE:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of the Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Product Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Product Matrix which gives a detailed comparison of the product portfolio of each company

Geographic Analysis

Additional countries in any of the regions

Company Information

Detailed analysis and profiling of additional market players (Up to five)

The Generative AI Chipset Market Size was valued at USD 37.29 Billion in 2023 and will reach USD 454.50 Billion by 2032 and grow at a CAGR of 32.2% by 2032.

The Authentication And Brand Protection Market was valued at USD 3.1 billion in 2023 and is expected to reach USD 6.9 billion by 2032, growing at a CAGR of 9.23% from 2024-2032.

Arm Based Servers Market was valued at USD 6.87 billion in 2023 and is expected to reach USD 22.79 billion by 2032, growing at a CAGR of 14.32% by 2032

The Learning Management System (LMS) Market Size was valued at USD 20.9 Bn in 2023 and will reach USD 95.4 Bn by 2032, growing at a CAGR of 18.4% by 2032.

The Web Performance Market was valued at USD 5.86 billion in 2023 and is projected to reach USD 12.70 billion by 2032, growing at a CAGR of 9.04% by 2032

The Lighting as a Service Market Size was valued at USD 1.23 Billion in 2023 & will reach USD 16.34 Billion by 2032 & grow at a CAGR of 33.3% by 2024-2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd