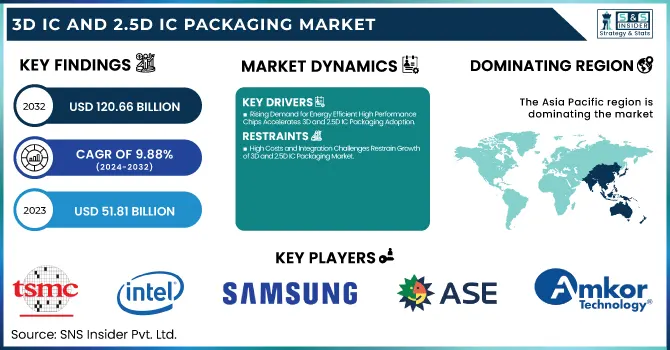

The 3D IC and 2.5D IC Packaging Market was valued at USD 51.81 billion in 2023 and is expected to reach USD 120.66 billion by 2032, growing at a CAGR of 9.88% over the forecast period 2024-2032.

To Get more information on 3D IC and 2.5D IC Packaging Market - Request Free Sample Report

The 3D IC and 2.5D IC packaging market is changing quickly towards his architecture, with modularization where a chip is designed, which can be more performant and scalable. With the advanced packaging demands, especially at the leading-edge nodes, converting and optimizing fab capacity are significantly being adjusted. High-density interconnect (HDI) PCBs are starting to become a key PCB type for 5G infrastructure to enable higher data rates and integration. At the same time, heterogeneous integration is rapidly gaining attention over monolithic methods, enabling multiple, disparate chipsets and functionalities to be combined into a single package for minimizing cost, area, power, and performance.

The U.S. 3D IC and 2.5D IC Packaging Market is estimated to be USD 11.13 Billion in 2023 and is projected to grow at a CAGR of 9.74%. The growth of the U.S. 3D IC and 2.5D IC Packaging Market is attributed to the upbeat investment in semiconductor innovation increment in computer power consumption especially driven by artificial intelligence (AI) and high-performance computers (HPC) coupled with the implementation of government initiatives including the CHIPS Act. Companies such as Intel, advancing packaging technologies, are expected to improve the performance, power efficiency, and integration density of chips.

Key Drivers:

Rising Demand for Energy Efficient High Performance Chips Accelerates 3D and 2.5D IC Packaging Adoption

Increasing demand for high-performance and energy-efficient semiconductor devices is one of the key factors driving the market for 3D IC and 2.5D IC packaging. Today, with fast-growing applications such as artificial intelligence (AI), high-performance computing (HPC), and 5G technology where both space and data grow immensely, the standard packaging approach is not nearly enough to provide the speed, bandwidth, and power efficiency needed. Now, the introduction of 3D ICs and 2.5D ICs provide better interconnect, higher bandwidth, smaller form factors, and thermal performance better suited for next-gen devices. In addition, dominant semiconductor players ramping up investments in heterogeneous integration and chipset-based designs are further boosting this advanced packaging technology adoption.

Restrain:

High Costs and Integration Challenges Restrain Growth of 3D and 2.5D IC Packaging Market

High design, development, and manufacturing costs are some of the major restraints in the 3D IC and 2.5D IC packaging market. While this is the future of semiconductor packaging, advanced packaging is much more costly than traditional packaging due to the complex equipment, unique materials, and high levels of expertise needed for 3D integration. Additionally, 3D/2.5D ICs introduce further integration challenges due to their requirement for through-silicon via (TSV) and interposer technology which compounds the cost and increases time-to-market further. However, those prices can be hard to reach, particularly for small- and medium-sized semiconductor companies or for applications where cost-effectiveness must be prioritized.

Opportunity:

Automotive EV and Chip Sovereignty Drive Global Demand for Robust 3D and 2.5D IC Packaging

A new one is automotive, to be especially focused on EV and autonomous driving. Detectors, radar, and AI-based processors are getting integrated into vehicles, which in turn need smaller high-volume semiconductor packages. To meet these needs, the high performance and inherent reliability of inherently robust 3D/2.5D ICs make them ideal for operation in harsh environments. Moreover, as governments worldwide are pursuing digital transfusion with ambitions of chip sovereignty, North America, Europe, and Asia Pacific regions are all experiencing an influx of backing and treasuries creating paths for regionally advanced packaging to be produced and commercialized. This results in real opportunities for existing players and start-ups along the semiconductor supply chain.

Challenges:

Thermal Issues Yield Loss and Design Complexity Hinder Widespread Adoption of 3D and 2.5D IC Packaging

The massive adoption still does not happen due to technical challenges of thermal management, yield issues, and design complexity. When multiple chips are stacked or placed adjacently, heat dissipation becomes even more of a challenge, especially for performance roadmaps like AI or data centers. Moreover, the testing and validation of the integrity of such small outline and multiple-layer assembly is a challenge, resulting in yield loss during manufacturing. Limited design standards, the immaturity of the ecosystem, and the lack of supply chain integration make it difficult for wider scale of these technologies and limit applications with flexible solutions.

By Packaging Technology

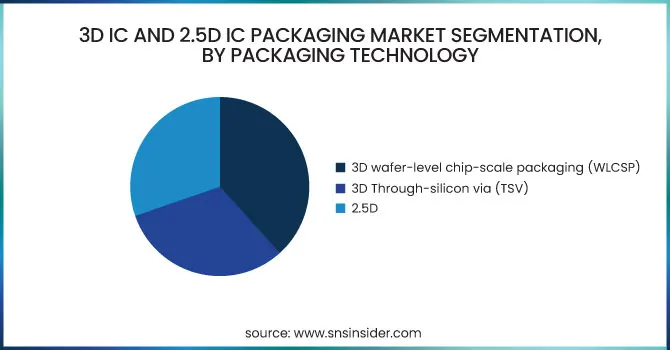

In 2023, the 3D wafer-level chip-scale packaging (WLCSP), favored in consumer electronics, translated to a market share of 38.3%, through smartphones, tablets, and wearables. WLCSP provides a small footprint, lower packaging expense, and optimal electrical performance, making it well-suited for high-volume applications where space and cost are at a premium. It allows for direct chip mounting on printed circuit boards without the need for conventional substrates and has made it the technology of choice among manufacturers seeking miniaturization and efficiency at scale.

The 3D Through-Silicon Via (TSV) segment is expected to grow at the highest CAGR from 2024 to 2032 due to rising demand for high-bandwidth and high-performance applications. TSV allows chips to be stacked more vertically with much shorter interconnect paths that require lower energy to move data and have lower latency. It suits many high-performance applications, including advanced computing, AI, data centers, and memory, where integration density and performance are critical. With advancements in these technologies, TSV is ready for extensive integration into business verticals.

By Application

The 3D IC and 2.5D IC packaging market were led by Memory, which accounted for a hefty 34.3% share in 2023 on the back of the growing market for high-bandwidth memory (HBM), 3D NAND, and stacked DRAM. These technologies are essential for use cases where immense data transport is needed like AI, in the cloud, and advanced gaming systems. 2.5D and 3D packaging solutions provide higher density, efficiency, and lower latency with lower power delivery to facilitate next-generation memory integration for extreme data center and HPC environments.

The MEMS/Sensors segment is projected to grow at the fastest CAGR from 2024 to 2032, which is driven by the increasing demand from the automotive, healthcare, industrial automation, and consumer electronics industries. MEMS sensors need tiny and high-performance package solutions that can provide reliable and efficient MEMS sensor packaging as devices are getting smaller and smarter. Demand for advanced packaging in MEMS applications continues to increase due to trends toward IoT, smart wearables, and autonomous systems.

By End User

The 3D IC and 2.5D IC packaging market is dominated by the Consumer Electronics segment, which accounted for a 33.7% share in 2023, on account of high-volume production of smartphones, tablets, smart wearables, and AR/VR devices. Such devices require small form factors, increased performance, and low power consumption all qualities achievable through the use of 3D and 2.5D packaging technologies i.e. WLCSP and Interposer based. These packaging methods are gradually penetrating consumer devices due to the increasing high-end features, such as AI chips, high-resolution imaging, and better processors.

The Automotive industry accounted for the fastest CAGR during the forecast period of 2024 to 2032 owing to the rapid developments in electric vehicles (EVs), autonomous driving systems, and in-vehicle infotainment technologies. Such applications demand packaging solutions that are durable, reliable, and thermally efficient. The increasing use of sensors, radar, LiDAR, and AI-driven control units in today's automotive vehicles is driving automotive manufacturers to quickly adopt or deploy 3D/2.5D IC packaging.

Regional Analysis

The Asia Pacific 3D IC and 2.5D IC Packaging market held the largest market share of 43.3% in 2023 and is expected to grow at the highest CAGR during the forecast period (2024-2032) due to a strong semiconductor ecosystem and aggressive technology adoption in the region. This area is the base for global semiconductor giants TSMC, Samsung Electronics, and ASE Group which almost have leading industry-level advanced packaging technology all together. Demand from consumer electronics, automotive, and AI computing drives continued investment in R&D and capital equipment by Taiwan, South Korea, Japan, and China. The regional hegemony in this area can be observed by TSMC expanding into 3D chipset integration and Samsung focusing on HBM and advanced logic packaging. Moreover, increasing government initiatives in the region such as the Made in China 2025 plan and growing investments in the developing semiconductor fabrication ecosystem in India will further consolidate Asia Pacific's high share and growth rate.

Get Customized Report as per Your Business Requirement - Enquiry Now

Some of the major players in the 3D IC and 2.5D IC Packaging Market are:

TSMC (CoWoS),

Intel (Foveros),

Samsung Electronics (X-Cube),

ASE Group (VIPack),

Amkor Technology (SLIM),

JCET Group (3D eWLB),

SPIL - Siliconware Precision Industries (2.5D SiP),

Powertech Technology Inc. (3D TSV Packaging),

Micron Technology (HBM2E Memory),

IBM (3D TSV Integration),

UMC (2.5D Interposer Technology),

Deca Technologies (M-Series),

Cadence Design Systems (3D-IC Advanced Package Design Tool),

Synopsys (3DIC Compiler),

Marvell Technology (2.5D Data Center SoC).

In December 2024, TSMC's Wafer Manufacturing 2.0 revolutionized advanced packaging by integrating packaging, testing, and photomask production into core wafer fabrication.

In June 2024, Siemens partnered with Samsung Foundry to expand 3D-IC enablement tools and optimize EDA solutions for Samsung’s latest process nodes, boosting innovation in AI, 5G, and automotive design.

| Report Attributes | Details |

| Market Size in 2023 | USD 51.81 Billion |

| Market Size by 2032 | USD 120.66 Billion |

| CAGR | CAGR of 9.88% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Packaging Technology (3D wafer-level chip-scale packaging (WLCSP), 3D Through-silicon via (TSV), 2.5D) • By Application (Logic, Imaging & Optoelectronics, Memory, MEMS/Sensors, LED, Others) • By End User (Consumer Electronics, Industrial, Telecommunications, Automotive, Military & Aerospace, Medical Devices) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | TSMC, Intel, Samsung Electronics, ASE Group, Amkor Technology, JCET Group, SPIL, Powertech Technology Inc., Micron Technology, IBM, UMC, Deca Technologies, Cadence Design Systems, Synopsys, Marvell Technology. |

Ans: The 3D IC and 2.5D IC Packaging Market is expected to grow at a CAGR of 9.88% during 2024-2032.

Ans: 3D IC and 2.5D IC Packaging Market size was USD 51.81 billion in 2023 and is expected to Reach USD 120.66 billion by 2032.

Ans: The major growth factor of the 3D IC and 2.5D IC Packaging Market is the rising demand for high-performance, compact, and energy-efficient semiconductor solutions in AI, 5G, and advanced computing applications.

Ans: The 3D wafer-level chip-scale packaging (WLCSP) segment dominated the 3D IC and 2.5D IC Packaging Market in 2023.

Ans: Asia Pacific dominated the 3D IC and 2.5D IC Packaging Market in 2023.

Table of Content

1. Introduction

1.1 Market Definition

1.2 Scope (Inclusion and Exclusions)

1.3 Research Assumptions

2. Executive Summary

2.1 Market Overview

2.2 Regional Synopsis

2.3 Competitive Summary

3. Research Methodology

3.1 Top-Down Approach

3.2 Bottom-up Approach

3.3. Data Validation

3.4 Primary Interviews

4. Market Dynamics Impact Analysis

4.1 Market Driving Factors Analysis

4.1.1 Drivers

4.1.2 Restraints

4.1.3 Opportunities

4.1.4 Challenges

4.2 PESTLE Analysis

4.3 Porter’s Five Forces Model

5. Statistical Insights and Trends Reporting

5.1 Chip Design Trends

5.2 Fab Capacity Utilization

5.3 HDI PCB Usage in 5G Infrastructure

5.4 Integration Trends: Monolithic vs. Heterogeneous

6. Competitive Landscape

6.1 List of Major Companies, By Region

6.2 Market Share Analysis, By Region

6.3 Product Benchmarking

6.3.1 Product specifications and features

6.3.2 Pricing

6.4 Strategic Initiatives

6.4.1 Marketing and Promotional Activities

6.4.2 Distribution and Supply Chain Strategies

6.4.3 Expansion plans and new product launches

6.4.4 Strategic partnerships and collaborations

6.5 Technological Advancements

6.6 Market Positioning and Branding

7. 3D IC and 2.5D IC Packaging Market Segmentation, By Packaging Technology

7.1 Chapter Overview

7.2 3D wafer-level chip-scale packaging (WLCSP)

7.2.1 3D wafer-level chip-scale packaging (WLCSP) Market Trends Analysis (2020-2032)

7.2.2 3D wafer-level chip-scale packaging (WLCSP) Market Size Estimates and Forecasts to 2032 (USD Billion)

7.3 3D Through-silicon via (TSV)

7.3.1 3D Through-silicon via (TSV) Market Trends Analysis (2020-2032)

7.3.2 3D Through-silicon via (TSV) Market Size Estimates and Forecasts to 2032 (USD Billion)

8. 3D IC and 2.5D IC Packaging Market Segmentation, By Application

8.1 Chapter Overview

8.2 Logic

8.2.1 Logic Market Trends Analysis (2020-2032)

8.2.2 Logic Market Size Estimates and Forecasts to 2032 (USD Billion)

8.3 Imaging & Optoelectronics

8.3.1 Imaging & Optoelectronics Market Trends Analysis (2020-2032)

8.3.2 Imaging & Optoelectronics Market Size Estimates and Forecasts to 2032 (USD Billion)

8.4 Memory

8.4.1 Memory Market Trends Analysis (2020-2032)

8.4.2 Memory Market Size Estimates and Forecasts to 2032 (USD Billion)

8.5 MEMS/Sensors

8.5.1 MEMS/Sensors Market Trends Analysis (2020-2032)

8.5.2 MEMS/Sensors Market Size Estimates and Forecasts to 2032 (USD Billion)

8.6 LED

8.6.1 LED Market Trends Analysis (2020-2032)

8.6.2 LED Market Size Estimates and Forecasts to 2032 (USD Billion)

8.7 Others

8.7.1 Others Market Trends Analysis (2020-2032)

8.7.2 Others Market Size Estimates and Forecasts to 2032 (USD Billion)

9. 3D IC and 2.5D IC Packaging Market Segmentation, By End User

9.1 Chapter Overview

9.2 Consumer Electronics

9.2.1 Consumer Electronics Market Trends Analysis (2020-2032)

9.2.2 Consumer Electronics Market Size Estimates and Forecasts to 2032 (USD Billion)

9.3 Industrial

9.3.1 Industrial Market Trends Analysis (2020-2032)

9.3.2 Industrial Market Size Estimates and Forecasts to 2032 (USD Billion)

9.4 Telecommunications

9.4.1 Telecommunications Market Trends Analysis (2020-2032)

9.4.2 Telecommunications Market Size Estimates and Forecasts to 2032 (USD Billion)

9.5 Automotive

9.5.1 Automotive Market Trends Analysis (2020-2032)

9.5.2 Automotive Market Size Estimates and Forecasts to 2032 (USD Billion)

9.6 Military & Aerospace

9.6.1 Military & Aerospace Market Trends Analysis (2020-2032)

9.6.2 Military & Aerospace Market Size Estimates and Forecasts to 2032 (USD Billion)

9.7 Medical Devices

9.7.1 Medical Devices Market Trends Analysis (2020-2032)

9.7.2 Medical Devices Market Size Estimates and Forecasts to 2032 (USD Billion)

10. Regional Analysis

10.1 Chapter Overview

10.2 North America

10.2.1 Trends Analysis

10.2.2 North America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.2.3 North America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.2.4 North America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.5 North America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.2.6 USA

10.2.6.1 USA 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.2.6.2 USA 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.6.3 USA 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.2.7 Canada

10.2.7.1 Canada 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.2.7.2 Canada 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.7.3 Canada 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.2.8 Mexico

10.2.8.1 Mexico 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.2.8.2 Mexico 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.2.8.3 Mexico 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3 Europe

10.3.1 Eastern Europe

10.3.1.1 Trends Analysis

10.3.1.2 Eastern Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.1.3 Eastern Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.1.4 Eastern Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.5 Eastern Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.1.6 Poland

10.3.1.6.1 Poland 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.1.6.2 Poland 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.6.3 Poland 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.1.7 Romania

10.3.1.7.1 Romania 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.1.7.2 Romania 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.7.3 Romania 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.1.8 Hungary

10.3.1.8.1 Hungary 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.1.8.2 Hungary 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.8.3 Hungary 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.1.9 Turkey

10.3.1.9.1 Turkey 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.1.9.2 Turkey 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.9.3 Turkey 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.1.10 Rest of Eastern Europe

10.3.1.10.1 Rest of Eastern Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.1.10.2 Rest of Eastern Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.1.10.3 Rest of Eastern Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2 Western Europe

10.3.2.1 Trends Analysis

10.3.2.2 Western Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.3.2.3 Western Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.4 Western Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.5 Western Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.6 Germany

10.3.2.6.1 Germany 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.6.2 Germany 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.6.3 Germany 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.7 France

10.3.2.7.1 France 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.7.2 France 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.7.3 France 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.8 UK

10.3.2.8.1 UK 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.8.2 UK 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.8.3 UK 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.9 Italy

10.3.2.9.1 Italy 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.9.2 Italy 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.9.3 Italy 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.10 Spain

10.3.2.10.1 Spain 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.10.2 Spain 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.10.3 Spain 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.11 Netherlands

10.3.2.11.1 Netherlands 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.11.2 Netherlands 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.11.3 Netherlands 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.12 Switzerland

10.3.2.12.1 Switzerland 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.12.2 Switzerland 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.12.3 Switzerland 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.13 Austria

10.3.2.13.1 Austria 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.13.2 Austria 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.13.3 Austria 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.3.2.14 Rest of Western Europe

10.3.2.14.1 Rest of Western Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.3.2.14.2 Rest of Western Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.3.2.14.3 Rest of Western Europe 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4 Asia Pacific

10.4.1 Trends Analysis

10.4.2 Asia Pacific 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.4.3 Asia Pacific 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.4 Asia Pacific 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.5 Asia Pacific 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.6 China

10.4.6.1 China 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.6.2 China 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.6.3 China 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.7 India

10.4.7.1 India 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.7.2 India 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.7.3 India 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.8 Japan

10.4.8.1 Japan 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.8.2 Japan 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.8.3 Japan 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.9 South Korea

10.4.9.1 South Korea 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.9.2 South Korea 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.9.3 South Korea 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.10 Vietnam

10.4.10.1 Vietnam 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.10.2 Vietnam 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.10.3 Vietnam 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.11 Singapore

10.4.11.1 Singapore 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.11.2 Singapore 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.11.3 Singapore 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.12 Australia

10.4.12.1 Australia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.12.2 Australia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.12.3 Australia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.4.13 Rest of Asia Pacific

10.4.13.1 Rest of Asia Pacific 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.4.13.2 Rest of Asia Pacific 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.4.13.3 Rest of Asia Pacific 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5 Middle East and Africa

10.5.1 Middle East

10.5.1.1 Trends Analysis

10.5.1.2 Middle East 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.1.3 Middle East 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.1.4 Middle East 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.5 Middle East 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.1.6 UAE

10.5.1.6.1 UAE 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.1.6.2 UAE 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.6.3 UAE 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.1.7 Egypt

10.5.1.7.1 Egypt 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.1.7.2 Egypt 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.7.3 Egypt 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.1.8 Saudi Arabia

10.5.1.8.1 Saudi Arabia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.1.8.2 Saudi Arabia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.8.3 Saudi Arabia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.1.9 Qatar

10.5.1.9.1 Qatar 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.1.9.2 Qatar 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.9.3 Qatar 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.1.10 Rest of Middle East

10.5.1.10.1 Rest of Middle East 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.1.10.2 Rest of Middle East 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.1.10.3 Rest of Middle East 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.2 Africa

10.5.2.1 Trends Analysis

10.5.2.2 Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.5.2.3 Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.2.4 Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.5 Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.2.6 South Africa

10.5.2.6.1 South Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.2.6.2 South Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.6.3 South Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.2.7 Nigeria

10.5.2.7.1 Nigeria 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.2.7.2 Nigeria 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.7.3 Nigeria 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.5.2.8 Rest of Africa

10.5.2.8.1 Rest of Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.5.2.8.2 Rest of Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.5.2.8.3 Rest of Africa 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.6 Latin America

10.6.1 Trends Analysis

10.6.2 Latin America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, by Country (2020-2032) (USD Billion)

10.6.3 Latin America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.6.4 Latin America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.5 Latin America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.6.6 Brazil

10.6.6.1 Brazil 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.6.6.2 Brazil 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.6.3 Brazil 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.6.7 Argentina

10.6.7.1 Argentina 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.6.7.2 Argentina 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.7.3 Argentina 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.6.8 Colombia

10.6.8.1 Colombia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.6.8.2 Colombia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.8.3 Colombia 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

10.6.9 Rest of Latin America

10.6.9.1 Rest of Latin America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Packaging Technology (2020-2032) (USD Billion)

10.6.9.2 Rest of Latin America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By Application (2020-2032) (USD Billion)

10.6.9.3 Rest of Latin America 3D IC and 2.5D IC Packaging Market Estimates and Forecasts, By End User (2020-2032) (USD Billion)

11. Company Profiles

11.1 TSMC.

11.1.1 Company Overview

11.1.2 Financial

11.1.3 Products/ Services Offered

11.1.4 SWOT Analysis

11.2 Intel.

11.2.1 Company Overview

11.2.2 Financial

11.2.3 Products/ Services Offered

11.2.4 SWOT Analysis

11.3 Samsung Electronics.

11.3.1 Company Overview

11.3.2 Financial

11.3.3 Products/ Services Offered

11.3.4 SWOT Analysis

11.4 ASE Group.

11.4.1 Company Overview

11.4.2 Financial

11.4.3 Products/ Services Offered

11.4.4 SWOT Analysis

11.5 Amkor Technology.

11.5.1 Company Overview

11.5.2 Financial

11.5.3 Products/ Services Offered

11.5.4 SWOT Analysis

11.6 JCET Group

11.6.1 Company Overview

11.6.2 Financial

11.6.3 Products/ Services Offered

11.6.4 SWOT Analysis

11.7 SPIL - Siliconware Precision Industries.

11.7.1 Company Overview

11.7.2 Financial

11.7.3 Products/ Services Offered

11.7.4 SWOT Analysis

11.8 Powertech Technology Inc.

11.8.1 Company Overview

11.8.2 Financial

11.8.3 Products/ Services Offered

11.8.4 SWOT Analysis

11.9 Micron Technology

11.9.1 Company Overview

11.9.2 Financial

11.9.3 Products/ Services Offered

11.9.4 SWOT Analysis

11.10 IBM

11.10.1 Company Overview

11.10.2 Financial

11.10.3 Products/ Services Offered

11.10.4 SWOT Analysis

12. Use Cases and Best Practices

13. Conclusion

An accurate research report requires proper strategizing as well as implementation. There are multiple factors involved in the completion of good and accurate research report and selecting the best methodology to compete the research is the toughest part. Since the research reports we provide play a crucial role in any company’s decision-making process, therefore we at SNS Insider always believe that we should choose the best method which gives us results closer to reality. This allows us to reach at a stage wherein we can provide our clients best and accurate investment to output ratio.

Each report that we prepare takes a timeframe of 350-400 business hours for production. Starting from the selection of titles through a couple of in-depth brain storming session to the final QC process before uploading our titles on our website we dedicate around 350 working hours. The titles are selected based on their current market cap and the foreseen CAGR and growth.

The 5 steps process:

Step 1: Secondary Research:

Secondary Research or Desk Research is as the name suggests is a research process wherein, we collect data through the readily available information. In this process we use various paid and unpaid databases which our team has access to and gather data through the same. This includes examining of listed companies’ annual reports, Journals, SEC filling etc. Apart from this our team has access to various associations across the globe across different industries. Lastly, we have exchange relationships with various university as well as individual libraries.

Step 2: Primary Research

When we talk about primary research, it is a type of study in which the researchers collect relevant data samples directly, rather than relying on previously collected data. This type of research is focused on gaining content specific facts that can be sued to solve specific problems. Since the collected data is fresh and first hand therefore it makes the study more accurate and genuine.

We at SNS Insider have divided Primary Research into 2 parts.

Part 1 wherein we interview the KOLs of major players as well as the upcoming ones across various geographic regions. This allows us to have their view over the market scenario and acts as an important tool to come closer to the accurate market numbers. As many as 45 paid and unpaid primary interviews are taken from both the demand and supply side of the industry to make sure we land at an accurate judgement and analysis of the market.

This step involves the triangulation of data wherein our team analyses the interview transcripts, online survey responses and observation of on filed participants. The below mentioned chart should give a better understanding of the part 1 of the primary interview.

Part 2: In this part of primary research the data collected via secondary research and the part 1 of the primary research is validated with the interviews from individual consultants and subject matter experts.

Consultants are those set of people who have at least 12 years of experience and expertise within the industry whereas Subject Matter Experts are those with at least 15 years of experience behind their back within the same space. The data with the help of two main processes i.e., FGDs (Focused Group Discussions) and IDs (Individual Discussions). This gives us a 3rd party nonbiased primary view of the market scenario making it a more dependable one while collation of the data pointers.

Step 3: Data Bank Validation

Once all the information is collected via primary and secondary sources, we run that information for data validation. At our intelligence centre our research heads track a lot of information related to the market which includes the quarterly reports, the daily stock prices, and other relevant information. Our data bank server gets updated every fortnight and that is how the information which we collected using our primary and secondary information is revalidated in real time.

Step 4: QA/QC Process

After all the data collection and validation our team does a final level of quality check and quality assurance to get rid of any unwanted or undesired mistakes. This might include but not limited to getting rid of the any typos, duplication of numbers or missing of any important information. The people involved in this process include technical content writers, research heads and graphics people. Once this process is completed the title gets uploader on our platform for our clients to read it.

Step 5: Final QC/QA Process:

This is the last process and comes when the client has ordered the study. In this process a final QA/QC is done before the study is emailed to the client. Since we believe in giving our clients a good experience of our research studies, therefore, to make sure that we do not lack at our end in any way humanly possible we do a final round of quality check and then dispatch the study to the client.

Key Segments:

By Packaging Technology

3D wafer-level chip-scale packaging (WLCSP)

3D Through-silicon via (TSV)

2.5D

By Application

Logic

Imaging & Optoelectronics

Memory

MEMS/Sensors

LED

Others

By End User

Consumer Electronics

Industrial

Telecommunications

Automotive

Military & Aerospace

Medical Devices

Request for Segment Customization as per your Business Requirement: Segment Customization Request

Regional Coverage:

North America

US

Canada

Mexico

Europe

Eastern Europe

Poland

Romania

Hungary

Turkey

Rest of Eastern Europe

Western Europe

Germany

France

UK

Italy

Spain

Netherlands

Switzerland

Austria

Rest of Western Europe

Asia Pacific

China

India

Japan

South Korea

Vietnam

Singapore

Australia

Rest of Asia Pacific

Middle East & Africa

Middle East

UAE

Egypt

Saudi Arabia

Qatar

Rest of Middle East

Africa

Nigeria

South Africa

Rest of Africa

Latin America

Brazil

Argentina

Colombia

Rest of Latin America

Request for Country Level Research Report: Country Level Customization Request

Available Customization

With the given market data, SNS Insider offers customization as per the company’s specific needs. The following customization options are available for the report:

Detailed Volume Analysis

Criss-Cross segment analysis (e.g. Product X Application)

Competitive Product Benchmarking

Geographic Analysis

Additional countries in any of the regions

Customized Data Representation

Detailed analysis and profiling of additional market players

The Embedded Security Market Size was valued at USD 7.07 Billion in 2023 and is expected to grow at 6.60% CAGR to reach USD 12.52 Billion by 2032.

The Thermal Camera Market Size was valued at USD 3.86 Billion in 2023 and is expected to grow at a CAGR of 6.44% to reach USD 6.76 Billion by 2032.

The Mid Wave Infrared (MWIR) Sensors Market Size was valued at USD 3.82 billion in 2023 and is expected to grow at a CAGR of 20.51% During 2024-2032.

The Semiconductor Metrology and Inspection Equipment Market Size is expected to reach USD 12.36 billion by 2032, grow at a CAGR of 6.50% by Forecast.

The Fault Detection and Classification Market size was valued at USD 4.70 billion in 2023 and is expected to grow to USD 10.01 billion by 2032 and grow at a CAGR of 8.83% over the forecast period of 2024-2032.

The Infrared Thermography Market Size was valued at USD 433.5 Million in 2023 and is expected to grow at 5.95% CAGR to reach USD 729.1 Million by 2032.

Hi! Click one of our member below to chat on Phone

© 2025 All Rights Reserved by SNS Insider Pvt Ltd